July 8, 2026

The Architecture of a Dual-Mandate Reserve Strategy

Across the global monetary landscape, a quiet but consequential reorientation is underway. Central banks in emerging economies are systematically rebuilding their reserve portfolios around hard assets, with gold at the centre of this shift. Tanzania central bank gold purchases represent one of the most structurally sophisticated examples of this trend, reflecting a calculated response to dollar weaponisation, sanctions-driven asset freezes, and the vulnerability of holding reserves predominantly in a single foreign currency.

According to World Gold Council data, central banks globally added over 1,000 tonnes of gold to their reserves in both 2022 and 2023, with emerging-market institutions driving the majority of net purchases. This pace of accumulation represents the most sustained period of official-sector gold buying since the collapse of the Bretton Woods system in the early 1970s. Furthermore, within this broader current, Tanzania's approach stands apart — not just because of the scale of accumulation, but because of how the country is doing it.

When big ASX news breaks, our subscribers know first

Why Tanzania Is Structurally Positioned Differently from Other African Buyers

Most emerging-market central banks acquiring gold must purchase it on international markets, settling in US dollars and drawing down the very foreign exchange reserves they are trying to diversify away from. Tanzania has, however, engineered a different pathway entirely.

As one of Sub-Saharan Africa's most significant gold-producing nations, Tanzania holds a natural structural advantage: it can source reserve-grade gold domestically, paying producers in Tanzanian shillings rather than depleting its foreign currency holdings. This mechanism is the conceptual foundation of the Domestic Gold Purchase Programme (DGPP), and it transforms a conventional reserve-building exercise into something considerably more sophisticated.

The DGPP does not require Tanzania to spend dollars to accumulate gold. Instead, it leverages domestic mineral output to build a hard-asset reserve position while injecting local currency into the mining economy. This is a fundamentally different model from what most peer nations are executing.

By contrast, nations like Kenya maintain predominantly US dollar-dominated reserve positions with minimal gold exposure, while Nigeria's mixed approach has historically involved commodity-linked instruments without meaningful domestic sourcing. Ghana has pursued gold reserve accumulation more aggressively in recent years, partly through a gold-for-oil programme, but this was largely a reactive measure during a severe foreign exchange crisis. Tanzania's DGPP is, by design, a proactive and systematic instrument — a distinction that also reflects the broader significance of African mineral endowments in reshaping continental monetary strategies.

Inside the Domestic Gold Purchase Programme: How It Actually Works

Programme Origins and Institutional Mandate

The DGPP was formally launched in September 2023, though the Bank of Tanzania conducted an initial 400 kg acquisition in April 2023 as a pilot phase. From October 2024 onward, the programme shifted into a structured, scaled operation with formalised supply chain architecture and mandatory participation requirements.

Bank of Tanzania Governor Emmanuel Tutuba has characterised the initiative as serving four interconnected policy objectives: strengthening foreign exchange reserves, supporting Tanzanian shilling stability, reinforcing overall financial system resilience, and contributing to sustainable long-term economic growth.

The Operational Flow: Step by Step

Understanding how the DGPP functions at a transactional level reveals why it has achieved relatively rapid uptake among producers who might otherwise route gold through informal channels.

- Local miners and licensed gold traders bring their output to designated collection points authorised under the programme.

- Gold is independently assessed and valued at the prevailing London Bullion Market Association (LBMA) spot price on the date of the transaction, ensuring transparent, internationally benchmarked pricing.

- Payment is disbursed to the seller in Tanzanian shillings within 24 hours of the completed transaction.

- Gold passes through licensed refinery infrastructure to meet reserve-grade quality standards before entering the Bank of Tanzania's official reserves.

The 24-hour payment settlement window is arguably the programme's most strategically important design feature. Informal gold buyers in artisanal mining regions typically operate with opaque pricing and delayed or partial payments. By matching London spot price with near-instant settlement in local currency, the DGPP removes the primary commercial incentive for miners to engage with informal networks.

Sabgold Limited and the Refinery Node Infrastructure

An often-overlooked dimension of the DGPP's architecture is the deliberate investment in domestic refinery capacity as part of the supply chain. On May 29, 2026, Sabgold Limited, a refinery licensed and operating in Kahama within the Shinyanga region, was officially designated as a gold collection and refining centre for Tanzania central bank gold purchases.

This designation matters beyond administrative formality. Shinyanga is one of Tanzania's most productive gold-bearing regions, historically known as the "Land of Gold" in Swahili cultural tradition. Positioning an authorised refinery node within this region reduces logistical friction for local producers, shortens the physical supply chain, and signals a commitment to embedding reserve infrastructure within the country's productive mining geography rather than centralising all operations in Dar es Salaam.

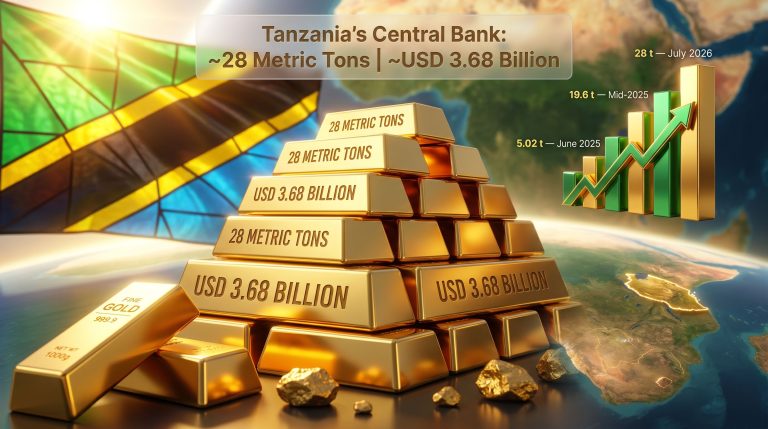

Tanzania's Gold Reserve Accumulation: The Numbers in Context

The quantitative story is striking in its pace and scale.

| Metric | Detail |

|---|---|

| Total Gold Acquired (as of mid-2026) | ~28 metric tonnes |

| Estimated Total Value | ~$3.68 billion (approx. 10 trillion Tanzanian shillings) |

| Programme Launch | September 2023 (pilot: April 2023) |

| Structured Domestic Purchases Begin | October 2024 |

| Accumulation Period | Approximately 18 months (to mid-2026) |

| Bank Accounts Opened for Producers | 4,000+ |

| Annual Acquisition Target (current FY) | 6 metric tonnes |

| Mandatory Reservation Requirement | 20% of gold output reserved for central bank |

| Payment Settlement Window | Within 24 hours at LBMA spot price |

To put the 28 metric tonne figure into perspective: this volume, accumulated over roughly 18 months of structured purchasing, represents a meaningful addition to Tanzania's official reserve position. At mid-2026 gold prices, $3.68 billion in gold reserves is a significant buffer for an economy of Tanzania's scale, providing a non-dollar anchor against external currency pressures.

The 20% Mandatory Reservation Rule: Regulatory Architecture and Sector Impact

What the Rule Requires

The Tanzania Mining Commission implemented a directive requiring all mining operators and traders to set aside 20% of their gold production for sale to the central bank at LBMA spot price. This mandatory reservation requirement took effect on October 1 and applies across the mining sector, from large-scale operators to registered small-scale producers.

The policy rationale is straightforward: voluntary participation, however incentivised, cannot guarantee the consistent and predictable supply flows the DGPP requires to meet its annual acquisition target of 6 metric tonnes. The mandatory component creates a supply floor, insulating the programme from periods of low voluntary participation that might otherwise coincide with elevated informal market activity during global gold price rallies.

Implications for Artisanal and Small-Scale Mining

The intersection of the mandatory reservation rule with the voluntary incentive structure creates a nuanced dynamic for Tanzania's artisanal and small-scale mining (ASM) sector. On one hand, the 24-hour London-priced payment model is genuinely attractive. On the other, smaller operators face compliance costs and administrative requirements that larger, formalised mining companies absorb more easily.

The positive externality of programme participation is, however, tangible. More than 4,000 bank accounts have been opened for gold producers as a direct consequence of the DGPP's enrolment process. For a sector historically characterised by cash transactions and financial exclusion, this represents a structural integration of previously informal economic actors into the regulated financial system.

The DGPP functions as a rare convergence of monetary policy and sectoral development strategy, using the incentive of fair, fast gold payment to progressively bring artisanal producers within the formal economy's institutional perimeter.

This financial inclusion dimension has downstream consequences for tax compliance, credit access, and mineral governance — all of which tend to improve when producers hold verifiable banking relationships.

Macroeconomic Rationale: What Gold Reserves Actually Do for Tanzania

Non-Dollar Buffer Against Currency Depreciation

The Tanzanian shilling, like most Sub-Saharan African currencies, carries meaningful exposure to dollar liquidity cycles. When global risk appetite contracts, or when the US Federal Reserve tightens monetary policy, currencies in emerging economies typically face depreciation pressure, regardless of domestic economic conditions.

Gold reserves provide a non-correlated buffer asset. Unlike US Treasuries or dollar-denominated bonds, gold as ultimate money does not lose value during dollar-driven EM currency selloffs — precisely why it appeals to reserve managers seeking to decouple their balance sheets from dollar volatility without replacing one foreign-currency dependency with another.

Bank of Tanzania officials have explicitly noted that the country does not face a foreign exchange crisis comparable to the acute pressures experienced by Ghana, Kenya, or Nigeria in recent years. This is a critical distinction: the DGPP is a proactive reserve strengthening exercise, not a crisis management tool.

Infrastructure Financing Through Strategic Reserve Liquidity

A less widely discussed dimension of the DGPP is its planned liquidity component. The Bank of Tanzania's board has approved a framework that includes the potential partial sale of accumulated gold reserves to finance major national infrastructure projects.

This planned mechanism reflects sophisticated reserve management thinking. The distinction between strategic reserve liquidation and distress-driven reserve drawdowns is important: in the former, a central bank sells a portion of accumulated hard assets to fund long-term productive investments at a time of its own choosing, without external pressure. In the latter, reserves are liquidated reactively to defend a currency or service debt obligations. Tanzania's framework consequently positions gold not merely as a static store of value but as a liquid, deployable asset within a broader fiscal and infrastructure investment strategy.

The next major ASX story will hit our subscribers first

Comparative Framework: How Tanzania's Model Stacks Up Against African Peers

| Country | Primary Reserve Strategy | Gold Exposure | Domestic Sourcing? |

|---|---|---|---|

| Tanzania | DGPP domestic gold purchase programme | Increasing significantly | Yes, core model feature |

| Ghana | IMF-supported programme + gold purchase scheme | Moderate | Partial |

| Kenya | USD-dominated reserve base | Low | No |

| Nigeria | Mixed commodity-linked approach | Low-moderate | Limited |

| South Africa | Historically gold-backed (legacy position) | High (historical) | Partial |

Note: Reserve composition figures are indicative for comparative framing. Readers should consult IMF International Financial Statistics and World Gold Council data for current verified positions.

What separates Tanzania's model structurally is the combination of domestic currency payment, embedded refinery infrastructure, and a dual mandate that treats reserve accumulation and mining sector formalisation as co-equal objectives. This approach also reflects growing interest in central bank gold demand as a structural rather than cyclical phenomenon among emerging-market institutions.

Risks, Limitations, and the Case for Reserve Portfolio Balance

Gold Price Volatility and Mark-to-Market Exposure

No reserve strategy is without risk. Tanzania's growing concentration in gold introduces meaningful mark-to-market exposure to global gold price cycles. A 15–20% correction in gold prices — which has occurred multiple times in the past two decades — would reduce the stated value of accumulated reserves by approximately $550–740 million based on current holdings.

This is not necessarily a crisis-level risk for a central bank holding gold as a long-term reserve asset rather than a short-term trading position, but it is a material consideration in reserve management planning.

Concentration Risk and Portfolio Construction

Best-practice reserve management frameworks, including guidelines from the IMF and the Bank for International Settlements, generally recommend diversified reserve portfolios rather than heavy concentration in any single asset class. As Tanzania's gold share of total reserves grows, reserve managers will need to actively monitor whether the portfolio remains appropriately balanced.

The planned partial liquidation mechanism, if executed at favourable price points, could serve as an organic rebalancing tool — converting gold into infrastructure assets rather than simply accumulating metal indefinitely. This approach also aligns with broader discussions about gold in the monetary system and how central banks are reassessing hard-asset roles in reserve portfolios.

Operational Integrity in the ASM Supply Chain

Artisanal and small-scale gold mining environments present inherent challenges for supply chain integrity. Ensuring that gold entering the DGPP meets reserve-grade purity standards, that provenance documentation is robust, and that refinery capacity can scale with programme ambitions are all operational dimensions that require sustained institutional attention.

The designation of Sabgold Limited as an authorised refinery node addresses part of this challenge, but as the programme targets 6 metric tonnes annually, the adequacy of refinery throughput capacity will be a critical watch item going forward.

What Tanzania's Programme Signals for African Monetary Policy More Broadly

Tanzania's DGPP is not an isolated experiment. It is one expression of a wider intellectual shift in how resource-rich African economies are rethinking the relationship between their mineral endowments and their monetary sovereignty. Indeed, central bank gold reserves across the developing world are increasingly viewed as instruments of strategic autonomy rather than simply passive financial buffers.

For other African gold-producing nations considering similar models, Tanzania's experience suggests three prerequisites are essential: domestic refinery capacity at meaningful scale, an artisanal and small-scale mining sector large enough to provide consistent supply volume, and regulatory enforcement capability sufficient to make mandatory reservation rules credible rather than nominal.

The geopolitical backdrop matters too. In a post-2022 global monetary environment, where US dollar sanctions against Russia demonstrated the real-world vulnerability of foreign-currency reserves, central banks across the developing world have recalibrated their thinking about what it means to hold a truly sovereign reserve asset.

Tanzania's decision to build reserves from the ground up — literally sourcing gold from its own soil, paid in its own currency, refined within its own borders — is a coherent strategic response to a global monetary environment where the rules of reserve management are being actively rewritten.

Key Takeaways at a Glance

- 28 metric tonnes of gold accumulated over approximately 18 months, valued at ~$3.68 billion, positions Tanzania as one of Africa's most active domestic gold reserve builders.

- The DGPP's 24-hour payment at LBMA spot price is the programme's primary tool for competing with informal market channels.

- A 20% mandatory reservation rule ensures supply continuity beyond voluntary participation, creating a structural floor for programme throughput.

- More than 4,000 new bank accounts opened for producers represent a measurable financial inclusion outcome embedded within a monetary policy programme.

- Sabgold Limited's designation as a refinery node in the Shinyanga region reflects deliberate supply chain infrastructure investment within productive mining geography.

- The strategy is explicitly proactive — not reactive — designed to reduce dollar-denominated reserve concentration ahead of any foreign exchange stress scenario.

- A board-approved framework for partial gold liquidation to fund infrastructure demonstrates reserve management sophistication rather than fiscal distress.

- Tanzania central bank gold purchases consequently represent one of the most complete models of resource-backed monetary sovereignty currently operating in the developing world.

Disclaimer: This article contains forward-looking statements and analytical projections regarding reserve strategies, macroeconomic outcomes, and policy frameworks. These represent analytical perspectives and should not be construed as financial or investment advice. Reserve composition figures for comparative countries are indicative only; readers should consult official IMF and World Gold Council publications for verified current data. Gold price scenario analyses are illustrative and do not constitute forecasts.

Want to Track the Next Major Gold Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX gold and mineral discoveries, transforming complex geological data into actionable investment insights for both traders and long-term investors — explore historic discovery returns to understand what early positioning can mean, then begin your 14-day free trial at Discovery Alert to secure your market-leading edge.