June 25, 2026

The Hidden Bottleneck Reshaping How the World Sources Critical Minerals

The global energy transition has exposed a structural fragility that most supply chain planners underestimated for decades. Approximately 90% of the world's critical mineral processing and refining capacity is concentrated within a single jurisdiction, according to the Institute for Energy Research. This concentration creates cascading risk for Western manufacturers, electric vehicle producers, and defence contractors who depend on a steady flow of refined inputs. Furthermore, the critical minerals demand surge tied to decarbonisation is making this bottleneck increasingly acute. When geopolitical tensions tighten, the entire downstream ecosystem feels the pressure simultaneously.

That vulnerability is now driving a fundamental reorientation of where mining capital flows. Governments and institutional investors are no longer evaluating African mineral jurisdictions purely on geological merit. They are stress-testing regulatory environments, asking harder questions about sovereign risk, and looking for the combination of endowment and predictability that justifies decade-long capital commitments. Tanzania, East Africa's dominant mining economy, is increasingly answering those questions in ways its regional peers have not yet managed.

When big ASX news breaks, our subscribers know first

Tanzania's Mineral Endowment: A Portfolio Built for the Energy Transition

Tanzania's geological position within the Tanzania Craton, one of the oldest and most stable Precambrian shield formations on the continent, has long been associated with gold mineralisation. What is less widely understood is how that same ancient geology hosts a remarkably diverse portfolio of critical minerals whose demand profiles align almost precisely with global decarbonisation targets.

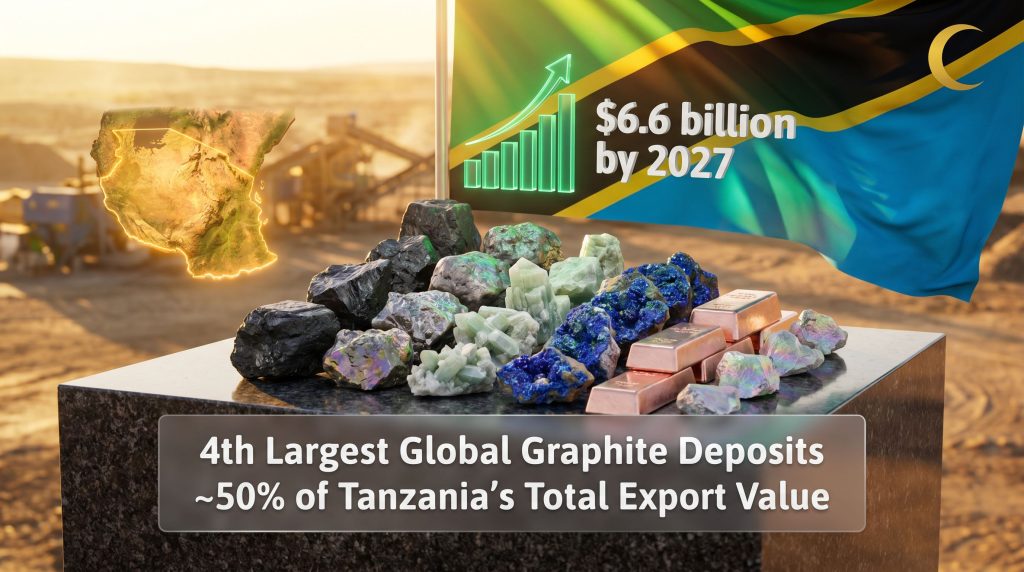

Critical minerals now account for roughly 50% to 55% of Tanzania's total national export value, positioning the sector as the country's third-largest industry and cementing Tanzania's status as the leading mining economy in East Africa, according to data from the Tanzania Investment Centre. The mineral mix includes some genuinely strategic assets.

| Critical Mineral | Global Significance | Primary Strategic Application |

|---|---|---|

| Graphite | 4th largest global deposits | EV battery anodes, industrial lubricants |

| Nickel | Significant reserves | Battery cathodes, stainless steel |

| Rare Earth Elements | Emerging producer status | Clean energy tech, defence electronics |

| Lithium | Growing exploration base | Battery cells, grid-scale energy storage |

| Cobalt | Identified deposits | EV batteries, aerospace alloys |

| Copper | Established resource base | Electrical infrastructure, renewables |

Tanzania's graphite deposits deserve particular attention from investors specialising in battery materials. The country holds the world's fourth-largest graphite reserves, and natural flake graphite remains the preferred anode material for lithium-ion batteries at scale. Synthetic graphite alternatives exist but carry significantly higher production energy costs, meaning natural graphite from stable jurisdictions commands a structural premium in long-term supply agreements.

What Tanzania's Critical Minerals Strategy Actually Proposes

The Tanzania Critical and Strategic Minerals Strategy, currently progressing through stakeholder consultation as of 2026, represents a deliberate architectural shift in how the country intends to participate in global supply chains. Rather than accepting its historical role as a raw commodity exporter, the Tanzania critical minerals strategy's central ambition is to capture more of the value chain domestically through processing, beneficiation, and eventually manufacturing integration.

The framework rests on five interconnected pillars, each targeting a different constraint on Tanzania's mining sector development.

Pillar 1: Expanding the Geological Knowledge Base

Perhaps the least visible but most consequential pillar is the Geological Survey of Tanzania's planned High-Resolution Airborne Geophysical Survey. The target is coverage of more than 50% of Tanzania's territory by 2030, up from a baseline of approximately 16%. This figure is striking when considered from an investor perspective: the majority of Tanzania's landmass has never been systematically characterised at the resolution required for modern exploration targeting.

Airborne geophysical surveys, which typically use combinations of magnetics, radiometrics, and electromagnetic sensing, generate the subsurface data layers that exploration geologists use to prioritise drill targeting. Higher-quality data translates directly into reduced exploration expenditure per discovery and faster project advancement timelines. For junior miners and major producers alike, a government-funded survey expansion of this scale effectively de-risks the earliest and most capital-intensive stage of the project lifecycle.

Pillar 2: Domestic Value Addition

The strategy explicitly prioritises in-country beneficiation for graphite, nickel, rare earths, and lithium. The UK-Tanzania Mutual Prosperity Partnership (MPP), signed in April 2024, provides a bilateral channel for technology transfer and manufacturing capability development that supports this objective. Understanding the MPP's scope is important: it is a trade and investment facilitation framework, not a project-specific funding commitment.

Pillars 3 Through 5: Infrastructure, Local Content, and Investment Facilitation

The remaining pillars address road, rail, and port upgrades to reduce logistics costs; local content mandates requiring the use of domestically sourced goods and services; and investment facilitation through the Tanzania Investment Centre. However, it is worth noting that special economic zones also play a complementary role in attracting processing investment, as recommended by the UONGOZI Institute, which operates as a one-stop processing mechanism with tax exemption frameworks and simplified licensing pathways.

Structural Insight: The five-pillar architecture is significant because it addresses supply chain integration at multiple stages simultaneously, rather than focusing exclusively on attracting upstream extraction capital. This distinguishes Tanzania's approach from many African mining jurisdictions that have prioritised royalty optimisation over ecosystem development.

How the 2026/27 Budget Translates Strategy Into Binding Policy

Tanzania's 2026/27 budget, presented in June 2026, is the country's largest spending plan to date. With nearly three-quarters of revenue raised domestically and a GDP growth target of 6.3% for 2026, the budget frames mining as a core engine of fiscal expansion rather than a discretionary revenue source.

Beneath the headline figures, two targeted reforms reveal the tactical intelligence behind Tanzania's long-term minerals positioning, as detailed by PwC Tanzania's National Budget Bulletin.

Reform 1: Framework Agreement Streamlining

The existing process required that tax exemptions embedded within Cabinet-approved Framework Agreements be subsequently republished via separate Government Notices (GNs) before taking legal effect. This procedural duplication created a gap between an investor receiving Cabinet approval and the exemptions actually becoming operative.

Under the proposed reform, Cabinet-approved Framework Agreement exemptions become directly applicable without the GN publication step. The practical consequences are significant on several dimensions:

- Investors modelling project economics can treat approved exemptions as confirmed inputs rather than probabilistic assumptions

- VAT treatment and fuel toll administration become cleaner and more predictable across project timelines

- The removal of the GN requirement has historically also disrupted corrupt intermediary networks that exploited the gap between approval and publication

- Multi-billion-dollar rare earth and battery minerals projects, which typically require investment decisions 8 to 12 years before peak production, are particularly sensitive to this kind of regulatory certainty

Framework Agreements themselves are an important technical instrument that is not widely understood outside specialist mining investment circles. Unlike general mining legislation, which applies uniformly across the sector, Framework Agreements are tailored, company-specific instruments negotiated between the government and individual large-scale project developers. They can address stabilisation clauses, infrastructure cost-sharing arrangements, and specific fiscal treatment. The reform does not change what these agreements contain; it changes how reliably their provisions take effect.

Reform 2: The Mineral Research Fund

The proposal to allocate 10% of gross mineral revenue collections into a dedicated Mineral Research Fund is less immediately visible to large institutional investors but arguably more structurally important for the sector's long-term productivity.

Small-scale miners in Tanzania employ thousands of people and account for approximately 40% of the country's mineral revenue, according to industry reporting cited by the Daily News Tanzania. Yet this segment has historically operated with significant information disadvantages relative to the large-scale sector: limited access to geological data, outdated extraction techniques, and minimal price transparency.

The Mineral Research Fund directly targets this productivity gap. Its objectives span geological knowledge improvement, expanded exploration capacity, and technical support services specifically calibrated to the needs of artisanal and small-scale mining (ASM) operators. The government's separate initiative establishing more than 40 mineral markets and buying centres across the country over the past five years complements this by creating formal market access infrastructure and reducing the mineral smuggling that has historically suppressed official revenue figures.

Tanzania vs. the DRC: Two Contrasting Models for Mineral Market Power

The strategic contrast between Tanzania's approach and the Democratic Republic of Congo's cobalt management strategy is instructive for understanding the full spectrum of options available to mineral-rich African nations. Indeed, the DRC cobalt export controls represent one of the starkest examples of how supply restriction can reshape global commodity markets.

The DRC has historically supplied more than 60% of the world's cobalt. When cobalt prices reached a nine-year low in 2025, the DRC responded by implementing annual export caps, beginning at 18,125 tonnes for 2025 with a gradual increase planned over subsequent years, according to SP Global Market Intelligence. This supply restriction mechanism was designed to create a price floor and restore leverage over global cobalt markets.

| Strategic Dimension | DRC Cobalt Model | Tanzania Minerals Model |

|---|---|---|

| Primary competitive lever | Export volume restriction | Regulatory certainty and investor climate |

| Signal to long-term investors | Unpredictability and supply risk | Stability and procedural transparency |

| Revenue mechanism | Price floor through supply control | Volume growth through investment attraction |

| Value addition focus | Limited in current framework | Central to national strategy |

| Small-scale sector integration | Ad hoc | Formally structured through Research Fund |

| Geological data availability | Constrained | Targeted expansion to 50%+ coverage by 2030 |

Both approaches reflect genuine strategic logic. The DRC's model leverages market concentration for price management, while Tanzania's model competes on operating environment quality. The critical question is which approach attracts the processing and manufacturing investment that ultimately determines long-term sector value, rather than just extraction volume.

The Implementation Risk That Policy Documents Cannot Resolve

Investor Caution: Tanzania's minerals strategy is well-designed on paper. The variable that separates successful mineral economies from perpetually promising ones is institutional execution capacity, not policy ambition.

Several unresolved implementation questions warrant careful monitoring by investors evaluating Tanzania exposure:

- Documentation standards for the new Framework Agreement provisions have not been fully specified, creating near-term uncertainty about what investors must demonstrate to trigger streamlined exemptions.

- Benefit-sharing definitions within the equitable economic sharing provisions remain subject to interpretation, which matters for project-level financial modelling.

- Applicability to existing agreements versus new ones is not yet clarified, creating a two-tier operating environment risk during the transition period.

- Institutional staffing gaps within key regulatory bodies and the Tanzania Revenue Authority have historically caused approval delays that offset the formal regulatory improvements.

The resource nationalism legacy of Tanzania's mining sector since the 2010s remains present in investor memory. International capital is watching implementation evidence rather than announcement content, and that distinction carries real weight for project financing timelines.

The next major ASX story will hit our subscribers first

What the Financial Trajectory Signals for Investors

| Metric | Current Position | Projected Target |

|---|---|---|

| Mining sector value | Approaching baseline | $6.6 billion by 2027 |

| Revenue growth target | Established baseline | +33% over three years |

| Foreign and local investment | Surpassed $1 billion | Continued growth trajectory |

| Small-scale miner revenue share | ~40% of mineral revenue | Targeted uplift via Research Fund |

| Geological survey coverage | ~16% of territory | >50% by 2030 |

The UONGOZI Institute has recommended using Export Processing Zones (EPZs) and Special Economic Zones (SEZs) as structured cluster environments for large-scale mineral processing plants. This model has precedent in Southeast Asian manufacturing economies and offers Tanzania a mechanism to attract processing investment with defined fiscal incentives while maintaining domestic policy flexibility outside the zones. Consequently, the Tanzania critical minerals strategy framework positions these zones as critical enablers of downstream value capture rather than optional policy instruments.

Three Scenarios for Tanzania's Minerals Future

Scenario 1: Accelerated Integration (Bull Case)

Full Framework Agreement reform operationalisation within 12 months attracts multi-billion-dollar rare earth and graphite processing commitments by 2028. Geological survey expansion unlocks new deposit discoveries that broaden the investment pipeline. Tanzania establishes itself as the preferred East African node in Western-aligned critical mineral supply chains.

Scenario 2: Incremental Progress (Base Case)

Reforms improve investor confidence selectively. Large-scale capital inflows materialise in graphite and nickel but rare earth processing investment lags. The small-scale sector benefits meaningfully from the Mineral Research Fund. Tanzania grows its share of global critical mineral supply but remains primarily an extraction economy through 2030.

Scenario 3: Implementation Stall (Bear Case)

Institutional capacity constraints delay reform operationalisation. Investor memory of resource nationalism persists without clear enforcement evidence. Competing jurisdictions including Zambia, Zimbabwe, and Mozambique capture a disproportionate share of the supply chain diversification capital flow redirected from China. In addition, the energy security risks facing Western nations may accelerate capital flight toward more established processing economies if Tanzania's reforms stall.

FAQ: Tanzania Critical Minerals Strategy Explained

What minerals are central to Tanzania's critical minerals strategy?

The strategy prioritises graphite, where Tanzania holds the world's fourth-largest deposits, alongside nickel, rare earth elements, lithium, cobalt, and copper. All are essential inputs for clean energy technologies, EV battery supply chains, and advanced electronics manufacturing.

What is the Tanzania Critical and Strategic Minerals Strategy?

It is a formal national policy framework currently in stakeholder consultation as of 2026, designed to govern exploration, extraction, beneficiation, and supply chain integration of critical minerals. Its core objective is the transition from raw commodity export to high-value processing and manufacturing.

How does the 2026/27 budget reform the Framework Agreement process?

The budget removes the requirement for tax exemptions within Cabinet-approved Framework Agreements to be separately republished via Government Notices before taking effect. This eliminates a procedural layer that has historically created delays, compliance costs, and opportunities for corruption.

What is the Mineral Research Fund and who does it serve?

The proposed fund will receive 10% of gross mineral revenue collections. Its primary beneficiaries are small-scale miners who currently lack access to geological data, modern extraction techniques, and market infrastructure, despite contributing approximately 40% of Tanzania's mineral revenue.

How does Tanzania's approach differ from the DRC's cobalt strategy?

The DRC uses export volume restrictions to create price floors in global cobalt markets. Tanzania's strategy prioritises regulatory predictability, geological transparency, and downstream value addition incentives, positioning itself as a lower sovereign-risk, long-term investment destination. Furthermore, China's rare earth strategy offers yet another model of supply chain leverage that Tanzania's policymakers are closely observing as they refine their own approach.

What is the projected value of Tanzania's mining sector by 2027?

The sector is projected to reach approximately $6.6 billion in value by 2027, representing a targeted revenue increase of around 33% over three years, supported by combined foreign and local investment that has already exceeded $1 billion. For broader context on how Tanzania's minerals policy compares with international legislative frameworks, independent analysis provides useful benchmarking for investors.

Disclaimer: This article contains forward-looking projections and scenario analyses based on publicly available policy documents, budget announcements, and industry research. These projections involve material uncertainty and should not be construed as financial advice. Investors should conduct independent due diligence before making any investment decisions related to Tanzania's mining sector or associated equities.

Want to Identify the Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly converting complex geological data into actionable investment insights across graphite, nickel, rare earths, and beyond. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated extraordinary returns, and begin your 14-day free trial today to position yourself ahead of the market.