May 11, 2026

The Investor Logic Reshaping African Energy Markets

For decades, the conventional wisdom governing African LNG investment rested on a single variable: reserve size. The bigger the gas field, the more compelling the investment thesis. That logic is now being systematically dismantled by a succession of operational failures across the continent's most resource-rich corridors, and the capital is moving accordingly.

What has emerged in its place is a more nuanced investor framework, one that weights political continuity, geographic access, and the quality of commercial partnership terms as heavily as the volume of hydrocarbons in the ground. Tanzania sits at the intersection of all three criteria, and that is why the Tanzania LNG project, a $42 billion development targeting first gas by approximately 2034, has attracted a consortium of global energy majors that reads like a who's who of the industry.

When big ASX news breaks, our subscribers know first

Why West Africa and Southern Africa Lost the LNG Investment Narrative

Nigeria's Reserve Paradox

Nigeria holds in excess of 200 trillion cubic feet (TCF) of natural gas, a reserve base that should logically position it as one of the world's great LNG exporters. The reality on the ground tells a different story. Persistent pipeline vandalism and oil theft across the Niger Delta have created a structural gap between what Nigeria theoretically holds and what it can practically deliver to export terminals. When shipments routinely fail to reach the coast, the size of the reserve becomes commercially irrelevant.

The Niger Delta problem is not a temporary disruption. It reflects decades of unresolved socioeconomic grievance, inadequate infrastructure protection, and a fragmented security environment that no single company or government agency has successfully resolved. For energy majors evaluating decade-long capital commitments, this structural unpredictability represents an unbankable risk profile regardless of underlying geology.

Mozambique's Forced Architectural Pivot

The Mozambique LNG story represents perhaps the most instructive case study in how political risk can transform a flagship African energy project into a cautionary tale. TotalEnergies' operations in Cabo Delgado were halted under Force Majeure in 2021 following a lethal insurgency that rendered onshore infrastructure indefensible. Those operations only restarted in 2026, representing a multi-year suspension that inflicted costs far beyond the simple loss of production revenue.

The financial consequence that is less widely understood is what the insurgency forced TotalEnergies to build: a floating export facility, essentially a maritime dock, to bypass onshore instability entirely. This architectural workaround was not budgeted in the original project economics. It added substantial unplanned capital expenditure to a project that was already targeting 12 to 13 million tonnes per annum (mtpa) of export capacity, and it introduced an entirely new category of operational complexity. Floating LNG infrastructure is technically demanding, weather-sensitive, and significantly more expensive to maintain than equivalent onshore terminals.

Mozambique's gas reserves remain large, its export ambitions remain substantial, but security threats continue to define the risk calculus for any new capital deployment in the corridor. That persistent uncertainty has redirected serious investor attention northward, as explored in depth by Business Insider Africa's coverage of African energy competition.

The New Investment Trifecta

What has replaced reserve volume as the primary investment signal is a more composite assessment framework. Energy majors are now evaluating African LNG opportunities through three simultaneous lenses:

- Political stability that is institutional rather than personality-dependent, capable of surviving electoral cycles without disrupting project economics

- Geographic access that reduces supply chain vulnerability and provides structural advantages in terms of market reach and transit risk

- Fiscal partnership quality, meaning commercial terms that allow investors to meet their hurdle rates while ensuring the host nation captures meaningful economic benefit

Tanzania scores competitively on all three dimensions. Its 57.54 TCF of proven reserves, with roughly 86% located offshore in the Indian Ocean, are smaller than Nigeria's but far more bankable under this evolved evaluation framework. The country's governance record, bolstered by its response to brief post-election unrest in October 2025, and the deliberate commercial architecture of the LNG deal itself, have combined to position Tanzania as Africa's most credible large-scale LNG development opportunity.

The central question in African LNG investment has shifted from how much gas does a country have? to how reliably can it be extracted, processed, and exported? Tanzania's answer to the second question is increasingly persuasive.

What the Tanzania LNG Project Actually Involves

Project Fundamentals at a Glance

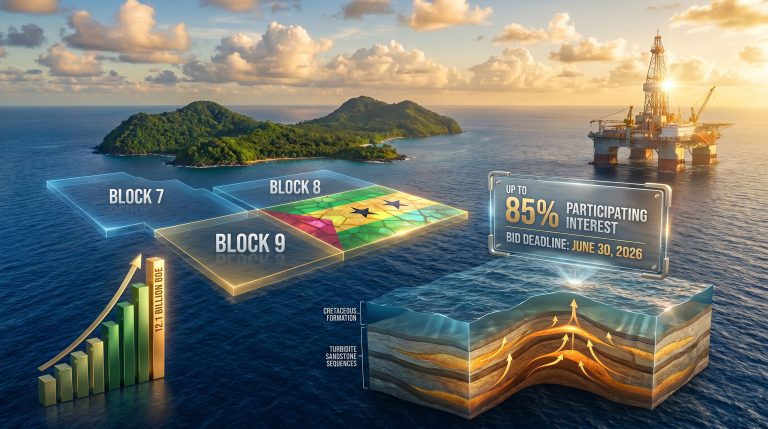

The Tanzania LNG project, also referenced as the Likong'o-Mchinga LNG Project, is a proposed onshore liquefaction and export facility to be built in the Lindi Region of southern Tanzania. Its gas supply is drawn from Blocks 1, 2, and 4 of the Rovuma Basin, with the offshore concentration of reserves giving the project deep resource longevity but also significant subsea engineering requirements.

| Parameter | Detail |

|---|---|

| Proven Gas Reserves Targeted | ~57.54 TCF (Blocks 1, 2, and 4) |

| Offshore Reserve Share | ~86% |

| Initial Liquefaction Capacity | ~10 mtpa |

| Full Build-Out Target | Up to 15 mtpa |

| Total Project Investment | ~$42 billion |

| FID Target | ~2028 |

| Deal Conclusion Target | Mid-2026 |

| First Gas Target | ~2034 |

| Export Infrastructure | Onshore terminal, Lindi Region |

At the projected 10 mtpa export capacity, Tanzania's LNG output would account for approximately 2 to 2.5% of global LNG trade, which reached roughly 411 million tonnes in 2024. At the higher-end 15 mtpa scenario, that share rises to approximately 3.6% of 2024 global volumes. Furthermore, given that the global LNG supply outlook points to demand growing at around 4% annually through the late 2020s, Tanzania would be entering an expanding market at first gas, provided the project stays on schedule.

The Consortium Behind the Capital

The Tanzania LNG project is structured around a consortium that distributes technical expertise, financial exposure, and operational responsibility across multiple parties:

- TPDC (Tanzania Petroleum Development Corporation): The state-owned entity representing Tanzania's sovereign equity interest in the project

- Shell: Joint operator, holding interests in Blocks 1 and 4

- Equinor: Joint operator for Block 2, contributing Norwegian technical expertise in deepwater offshore development

- ExxonMobil: Equity partner bringing additional balance sheet depth and project finance experience

- Pavilion Energy and Medco Energi: Additional consortium participants providing regional knowledge and financing capacity

The multi-operator structure is not merely an administrative arrangement. It functions as a risk distribution mechanism, ensuring that no single partner carries disproportionate technical or commercial exposure. When one operator encounters operational difficulty or financing constraint, the consortium structure provides structural resilience that bilateral deals cannot replicate.

What Distinguishes This Deal Commercially

One of the less widely discussed features of the Tanzania LNG project's commercial architecture is the domestic gas allocation framework embedded in the negotiations. Tanzania has secured a structure requiring a meaningful portion of produced gas to be directed toward national industries, including power generation, fertiliser manufacturing, and the broader petrochemical sector.

This provision transforms the economic logic of the project beyond the simple export revenue calculation. Domestic access to affordable gas could catalyse a wave of industrial development in Tanzania that operates independently of LNG export pricing cycles. Fertiliser production capacity fed by domestic gas, for example, would reduce agricultural input costs and support food security at a scale that royalty payments alone cannot achieve. This is the structural mechanism by which the Tanzania LNG project differentiates itself from the extractive template that has defined much of Africa's resource history.

A Decade of Delays: How Tanzania's LNG Project Finally Reached Pre-FID Status

The Development Timeline

Understanding why the Tanzania LNG project is only now approaching a Final Investment Decision requires situating it within a prolonged history of negotiation, fiscal dispute, and market disruption.

| Period | Development |

|---|---|

| 2011-2013 | Exploration drilling across Blocks 1, 2, and 4; discovery of 20-23 TCF; over $2 billion invested by consortium partners |

| 2016-2018 | Onshore site selection completed; early production targets established |

| 2021 | Global LNG price dislocation; Equinor records a significant write-down on Tanzania project value amid low oil prices and governance uncertainty |

| 2021-2026 | Mozambique LNG Force Majeure period; regional investor confidence weakened |

| 2022 | Framework agreement progresses with Shell and Equinor; HGA and PSA targeted |

| October 2025 | Brief post-election unrest in Tanzania; government reconciliation agenda activated |

| Mid-2026 | Deal conclusion targeted |

| 2028 | FID projected |

| ~2034 | First gas delivery |

The Governance Friction That Nearly Killed the Project

The years of stagnation between initial discovery and a credible FID pathway were not primarily caused by geological, technical, or even market factors. They were caused by fiscal and governance misalignment. Under an earlier administration, Tanzania's negotiating posture toward international energy companies incorporated aggressive local content mandates and revenue-sharing structures that failed to satisfy the commercial hurdle rates of major energy companies operating multi-decade capital programmes.

The consequences were concrete. Equinor recorded a substantial write-down on its Tanzania LNG position in 2021, a financial signal that communicated how close the project came to permanent shelving. When a company of Equinor's scale and sophistication concludes that a project's book value must be reduced, it reflects a genuine assessment that the probability of value realisation has fallen materially. That is not a negotiating tactic. It is an accounting statement about viability.

President Hassan's Strategic Reset

The arrival of President Samia Suluhu Hassan in office in 2021 initiated a deliberate reorientation of Tanzania's energy investment posture. Rather than treating international energy companies as adversaries to be managed, the Hassan administration framed the relationship as a strategic partnership through which Tanzania's economic transformation could be accelerated.

President Hassan articulated this vision publicly in November 2025, describing the $42 billion LNG project not merely as an engineering achievement but as the foundation of Tanzania's next phase of economic development. This framing matters because it signals to international capital that the project's commercial architecture is aligned with national development objectives rather than in tension with them.

The government's response to post-election unrest in October 2025 reinforced this message. When political violence briefly disrupted Tanzania's historical record of stability, the administration's rapid reconciliation effort demonstrated that institutional governance capacity, not just individual leadership, was available to contain disruption. For long-term infrastructure investors, that distinction between personality-dependent stability and institutional stability is critical.

The Indian Ocean Advantage: Why Geography Is a Financial Asset

Bypassing the World's Most Contested Chokepoint

The Strait of Hormuz crisis, which has disrupted Middle Eastern energy export reliability, has elevated what market analysts describe as a security premium for non-Hormuz LNG supply. Approximately one-fifth of global LNG trade transits the Strait of Hormuz under normal conditions. When that transit route faces disruption, every cargo originating from the Persian Gulf acquires an additional risk layer that buyers must price into their procurement decisions.

Tanzania's Indian Ocean coastline eliminates that exposure entirely. LNG tankers loaded at the proposed Lindi Region terminal can reach Asian and European import destinations without passing through either the Strait of Hormuz or the Suez Canal under stress scenarios. This is not a marginal advantage. In an environment where energy security has become a primary procurement criterion for governments and utilities in India, Japan, South Korea, and China, supply that bypasses geopolitical chokepoints commands genuine buyer preference. The broader geopolitical risk landscape across energy and metals markets further reinforces the premium placed on supply chain resilience.

Tanzania vs. Mozambique: The Operational Comparison

The most instructive regional comparison is not Tanzania versus Nigeria, but Tanzania versus Mozambique, given the two countries share geological proximity in the Rovuma Basin.

| Factor | Tanzania | Mozambique |

|---|---|---|

| Proven Gas Reserves | ~57.54 TCF | ~100+ TCF |

| LNG Capacity Target | 10-15 mtpa | 12-13 mtpa |

| Operational Status | Pre-FID; advanced negotiations | Restarted 2026 after Force Majeure (2021-2026) |

| Export Infrastructure Model | Onshore terminal (planned) | Floating export infrastructure required |

| Political Risk Profile | Low-moderate; October 2025 unrest resolved | Elevated; ongoing Cabo Delgado insurgency |

| Investor Sentiment | Improving | Cautious; significant unplanned costs incurred |

The infrastructure comparison is particularly revealing. Tanzania's onshore terminal design reflects a project environment where developers can build conventional, cost-efficient liquefaction infrastructure because the security environment permits it. Mozambique's floating dock, by contrast, represents the capital consequence of building in a conflict zone: a technically demanding, operationally complex, and significantly more expensive solution to a problem that governance stability would have eliminated.

Tanzania's Critical Minerals Sector: The Parallel Economic Engine

A Resource Endowment That Extends Beyond Hydrocarbons

The Tanzania LNG project does not operate in isolation from the country's broader resource economy. Tanzania holds substantial deposits of gold, nickel, graphite, and niobium, alongside a wider cluster of minerals directly relevant to the global energy transition supply chain. By 2024, the minerals sector contributed just over 10% of Tanzania's GDP and accounted for more than 50% of non-traditional exports. President Hassan highlighted this mineral wealth alongside the LNG project in a November 2025 speech, framing the country's resource endowment as a dual-track economic development platform. In fact, understanding critical minerals and energy security as interlinked priorities is increasingly central to how major economies are structuring long-term supply agreements.

The Graphite Position: A Critical Battery Supply Chain Input

Tanzania's graphite reserves deserve specific attention because they represent a strategic position in the supply chain for lithium-ion battery anodes, a direct input into electric vehicle manufacturing.

| Graphite Metric | Detail |

|---|---|

| Share of Global Graphite Reserves | ~6% |

| Projected Annual Output (by ~2028) | 300,000+ tonnes |

| Projected Global Ranking | Top-5 producer |

| Primary Industrial Application | Battery anode material for EV supply chains |

Reaching top-5 global producer status by approximately 2028, with an annual output pipeline exceeding 300,000 tonnes, positions Tanzania not just as a commodity exporter but as a structurally important participant in the clean energy supply chain. The same political stability and geographic infrastructure that underpin the LNG project's investment case also benefit graphite mining and processing operations. There is a compounding logic here: governance quality and institutional reliability amplify the value of every category of Tanzania's resource endowment simultaneously.

The Convergence Thesis: LNG Revenue Funding Transition Minerals

There is an underappreciated strategic alignment between Tanzania's LNG export revenues and the capital investment required to scale its critical minerals processing capacity. LNG projects at this scale generate substantial government revenue streams through royalties, corporate taxes, and profit participation mechanisms. Those revenues, if channelled through transparent fiscal management, could fund the industrial infrastructure required to move Tanzania's critical minerals export profile from raw ore toward processed and value-added products.

This is the convergence thesis: that Tanzania's positioning at the intersection of the current energy economy and the transition energy economy creates a compounding development opportunity available to very few nations. Furthermore, the rising critical minerals demand driven by the global energy transition means LNG revenues and critical minerals royalties are not competing priorities but mutually reinforcing revenue streams serving the same national development agenda.

The next major ASX story will hit our subscribers first

Sizing Tanzania's Opportunity Against Global LNG Markets

What 10 to 15 mtpa Actually Means at Global Scale

Global LNG trade reached approximately 411 million tonnes in 2024. At Tanzania's initial target capacity of 10 mtpa, the country's exports would represent roughly 2 to 2.5% of that total. At the full build-out target of 15 mtpa, that share rises to approximately 3.6%. These numbers are modest in percentage terms, but their significance must be contextualised through the lens of Tanzania's current economic scale.

| Economic Metric | Figure |

|---|---|

| Tanzania's Annual GDP (approximate) | ~$80 billion |

| LNG Project Investment Value | ~$42 billion |

| Investment as % of Annual GDP | ~52% |

| Minerals' Contribution to GDP (2024) | ~10% |

| Minerals' Share of Non-Traditional Exports | >50% |

| Projected LNG Contribution to GDP Growth | ~8% (projected) |

A capital injection equivalent to more than half of Tanzania's annual GDP, structured as a long-term productive asset rather than a one-time transfer, represents an economic transformation event, not merely a growth increment. Australia's own experience managing large-scale LNG development offers a comparable reference point, with resource and energy exports demonstrating both the substantial rewards and the structural challenges that accompany this scale of hydrocarbon development.

Who Will Buy Tanzania's LNG?

Asian markets represent the primary demand anchor for Tanzanian LNG, driven by the import expansion programmes underway across the Indian subcontinent and Northeast Asia:

- India: Rapidly expanding LNG import terminal capacity; geographic proximity to Tanzania's Indian Ocean export point creates particularly competitive freight economics

- China: Continuing LNG import growth driven by coal-to-gas switching programmes in industrial and residential sectors

- Japan and South Korea: Both mature LNG importers with long-term supply diversification mandates and preference for non-Hormuz-exposed sources

- European buyers: Accelerating demand for supply diversification following geopolitical disruptions to Russian pipeline gas, with Tanzania's non-Hormuz routing adding a secondary security benefit

The presence of Asian and European buyers already engaged in preliminary discussions ahead of FID is a material demand-side signal. It suggests that the commercial risk in the Tanzania LNG project is concentrated on the supply-side execution challenge, not on finding customers for the gas once it flows.

What Are the Remaining Risks Between Now and First Gas?

Fiscal and Commercial Execution Risk

The most immediate and concrete risk to the Tanzania LNG project's FID trajectory is the final resolution of fiscal terms. The Host Government Agreement and Production Sharing Agreement must simultaneously satisfy the commercial return requirements of Shell, Equinor, and ExxonMobil, which are managing multi-decade capital programmes against defined hurdle rates, while also delivering on Tanzania's domestic gas allocation commitments and government revenue expectations. These objectives are not inherently incompatible, but the negotiating complexity involved in balancing them across a six-party consortium should not be underestimated.

The precedent set by Equinor's earlier write-down demonstrates what happens when commercial terms fall outside acceptable parameters for an extended period. A repeat of that dynamic would be more damaging in the current context, because the project has been publicly framed as approaching conclusion. A further collapse in negotiations would carry reputational consequences for Tanzania as an investment destination that would be difficult to recover from quickly. Reuters has reported that Tanzania expects to sign the deal before June 2026, underlining the urgency with which both government and consortium partners are approaching the final negotiating phase.

Market Timing and Competing Supply

The 10-year lead time between FID (projected 2028) and first gas (projected 2034) requires Tanzania to make a long-dated bet on the structure of global LNG demand in the mid-to-late 2030s. Several factors could work against this position:

- Capacity expansion programmes in Qatar, the United States, and Australia could increase global LNG supply significantly by 2034, compressing spot market pricing

- Accelerating renewable energy deployment in key Asian markets could reduce the rate of LNG import demand growth, particularly in China and South Korea

- Shipping and logistics economics may shift as LNG fleet composition evolves

These are not arguments against the project, but they are arguments for ensuring that FID does not slip further toward 2030 or beyond. Every year of pre-FID delay narrows the operational window in which Tanzania can capture premium demand conditions and establish long-term offtake relationships before competing supply volumes reshape market dynamics.

Political Continuity and Institutional Risk

The investment-friendly environment that has made Tanzania's LNG project viable under the current administration must be evaluated for its durability across political cycles. Tanzania's governance framework has historically demonstrated meaningful continuity, but the October 2025 post-election unrest served as a reminder that political risk cannot be eliminated, only managed.

The greatest vulnerability facing the Tanzania LNG project is not geological or technical in nature. It is the compounding cost of time. Each additional year of pre-FID delay reduces the commercial window available between capital deployment and the point at which competing supply or demand-side structural shifts could erode the project's financial rationale.

Frequently Asked Questions About the Tanzania LNG Project

What exactly is the Tanzania LNG project?

The Tanzania LNG project is a proposed $42 billion liquefied natural gas development centred on the Lindi Region of southern Tanzania. It draws gas from Blocks 1, 2, and 4 of the offshore Rovuma Basin, which collectively hold approximately 57.54 TCF of proven reserves, with roughly 86% located offshore in the Indian Ocean. The project is designed to produce between 10 and 15 mtpa of LNG for export. Key consortium partners include Shell, Equinor, ExxonMobil, Pavilion Energy, Medco Energi, and Tanzania's state-owned TPDC.

When is the Final Investment Decision expected?

Under the current project timeline, deal conclusion is targeted for mid-2026, with capital deployment expected from 2028 (FID) and first gas delivery projected around 2034.

How does Tanzania compare to Mozambique as an LNG investment destination?

Mozambique holds larger reserves (100+ TCF versus Tanzania's 57.54 TCF) and was targeting similar export capacity. However, a lethal insurgency in Cabo Delgado forced TotalEnergies to invoke Force Majeure in 2021, halt operations until 2026, and invest in expensive floating export infrastructure to bypass onshore instability. Tanzania's lower political risk profile and planned onshore terminal represent a materially different risk-adjusted investment proposition.

Who are the most likely buyers of Tanzania's LNG?

Asian import markets, particularly India, China, Japan, and South Korea, represent the primary demand base. European buyers seeking supply chain diversification away from Russian pipeline gas and Middle Eastern sources provide an additional demand layer. Tanzania's Indian Ocean location creates competitive freight economics for Indian subcontinent buyers in particular, and eliminates Strait of Hormuz transit risk exposure entirely.

What is the size of Tanzania's proven gas reserves?

Tanzania holds approximately 57.54 TCF of proven natural gas reserves sourced from Blocks 1, 2, and 4 of the Rovuma Basin. Approximately 86% of these reserves are located offshore in the Indian Ocean.

How will Tanzanian citizens benefit from the LNG project?

Beyond export revenue flows to the national treasury, the commercial framework includes a provision ensuring a meaningful portion of produced gas serves domestic industries including power generation, fertiliser production, and petrochemical manufacturing. At full operation, the project is projected to contribute approximately 8% to Tanzania's GDP growth trajectory, alongside direct and indirect employment creation and industrial development in the Lindi Region.

Three Scenarios for Tanzania's LNG Future

Scenario 1: FID Achieved by 2028 (Base Case)

Deal documentation is concluded by mid-2026, legal agreements are finalised across the consortium, and FID proceeds on schedule in 2028. Construction commences across the two-train liquefaction facility, and first gas is delivered around 2034. Under this pathway, Tanzania becomes East Africa's leading LNG exporter within the decade, with LNG revenues compounding alongside critical minerals export growth to accelerate the country's broader industrialisation agenda.

Scenario 2: Delayed FID (2029-2031)

Residual friction on fiscal terms or domestic gas allocation percentages pushes the FID window into the early 2030s. First gas is delayed to 2037 or beyond, and Tanzania enters a global LNG market that may already reflect the capacity additions underway in Qatar and the United States. Some erosion of demand-side advantage from Asian buyers is possible as renewable energy penetration in China and South Korea reduces import growth rates below current projections.

Scenario 3: Consortium Restructuring or Partner Exit

A major partner withdrawal, echoing the dynamics of Equinor's earlier write-down period, or a political transition that disrupts the current negotiating framework, forces the project into restructuring. Under this scenario, significant reputational damage accrues to Tanzania as an investment destination, and the timeline to first gas extends materially regardless of any subsequent reconstitution of the consortium.

What a Successful Tanzania LNG Outcome Means for the Continent

The Tanzania LNG project carries implications that extend well beyond its direct economic impact on one nation. A successfully executed FID-to-first-gas pathway would provide something that African energy development has lacked for decades: a replicable blueprint demonstrating that governance quality, geographic advantage, and commercially fair partnership terms can combine to deliver a mega-project in sub-Saharan Africa without the operational failures that have characterised comparable ambitions elsewhere on the continent.

East Africa's other nations with offshore hydrocarbon potential would be watching closely. A Tanzania success story transforms the regional investment narrative in ways that no amount of reserve-size statistics or policy framework announcements can achieve on their own. It would validate the proposition that the continent's energy sector is capable of delivering on its potential when the right governance conditions are in place.

Readers seeking additional context on East African energy markets and the Tanzania LNG project's development history may find value in related reporting from Business Insider Africa, which covers African energy market dynamics and investment trends across the continent. This article contains forward-looking projections regarding timelines, production targets, GDP impacts, and market demand scenarios. These projections involve material uncertainty and should not be treated as financial advice. Actual outcomes may differ significantly from those described.

Want to Spot the Next Major Resource Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering actionable alerts on significant mineral discoveries — from critical minerals powering the energy transition to the commodities reshaping global supply chains — so subscribers can act ahead of the broader market. Explore historic discoveries and their exceptional returns, then begin your 14-day free trial to secure your market-leading edge.