June 22, 2026

Global energy markets face unprecedented vulnerabilities as structural dependencies on narrow geographic corridors expose the fundamental fragility of international supply chains. The concentration of critical energy flows through specific maritime passages creates systemic risks that extend far beyond regional conflicts, with tension in the Middle East affecting oil prices through cascading effects across interconnected economic systems worldwide.

Understanding Energy Corridor Dependencies and Market Vulnerabilities

The global energy infrastructure operates through a series of critical chokepoints that collectively control the majority of international petroleum flows. These geographic bottlenecks represent more than simple transportation routes; they function as essential arteries for the world economy, where disruption creates immediate and far-reaching consequences across multiple sectors.

Geographic Concentration of Global Energy Flows

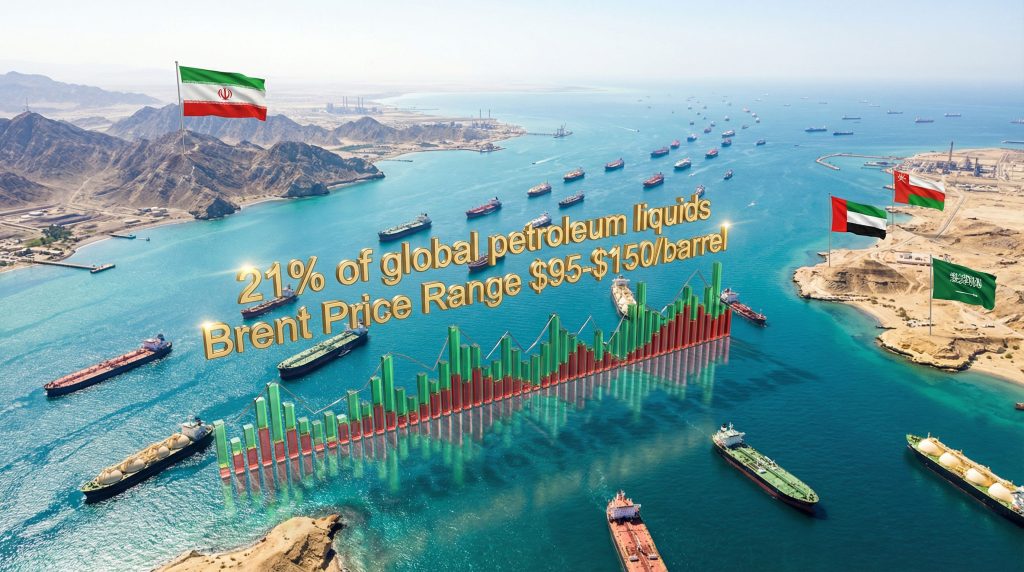

Current data reveals that approximately one-fifth of global crude oil transits through the Strait of Hormuz, making it the world's most strategically important energy passage. This narrow waterway, measuring just 21 miles at its narrowest point, serves as a critical conduit for both crude oil and liquefied natural gas (LNG) supply to major importing nations across Asia, Europe, and beyond.

The International Energy Agency has characterised recent supply disruptions as the biggest oil supply disruption ever, highlighting the unprecedented scale of current market stress. Furthermore, this assessment underscores the vulnerability inherent in global energy systems that rely heavily on concentrated shipping lanes.

Key statistical indicators demonstrate the scope of this dependency:

- 21% of global petroleum liquids flow through the Strait of Hormuz daily

- Approximately 20% of worldwide LNG shipments transit this corridor

- Limited alternative routing capacity exists for redirecting substantial cargo volumes

- Transit time penalties of 2-3 weeks apply when using alternative routes around Africa

Infrastructure Vulnerability Assessment Mechanisms

The current crisis has exposed significant weaknesses in alternative transportation infrastructure. Maritime chokepoints create single points of failure where relatively small-scale disruptions can generate disproportionate global impacts. Recent events demonstrate how diplomatic coordination has become necessary for individual vessel passage, with countries like Thailand and Malaysia securing transit rights through bilateral negotiations with regional powers.

Transportation cost escalation during disruptions follows predictable patterns, with insurance premium increases typically ranging from 200-500% for vessels transiting high-risk areas. These additional costs cascade through supply chains, ultimately affecting end-user pricing across multiple commodity categories.

Regional refining capacity constraints compound transportation bottlenecks. When crude supplies face disruption, refineries cannot easily substitute feedstock sources due to technical specifications and existing supply contracts, creating additional pressure points throughout the energy value chain.

When big ASX news breaks, our subscribers know first

Market Psychology and Risk Premium Pricing Mechanisms

Energy markets demonstrate heightened sensitivity to geopolitical developments, with tension in the Middle East affecting oil prices through multiple transmission channels. Price volatility reflects not only physical supply constraints but also psychological factors that influence trading behaviour and capital allocation decisions.

Fear-Based Trading Pattern Analysis

Recent market data illustrates the profound impact of uncertainty on energy pricing. Brent futures surged $5.79 or 5.7% to settle at $108.01 per barrel, while WTI futures gained $4.16, or 4.6% to close at $94.48 per barrel during a single trading session. These movements occurred despite the previous session showing declines of more than 2%, demonstrating the rapid sentiment shifts characterising current market conditions.

Since the onset of regional conflicts, Brent futures have increased nearly 50%, while WTI has risen 41%, representing substantial risk premium accumulation over relatively short timeframes. Such dramatic price appreciation reflects market participants pricing in extended disruption scenarios rather than temporary supply interruptions.

Timothy Snyder, Chief Economist at Matador Economics, observed that confusion and frustration regarding the authenticity of diplomatic communications drives investors toward capital preservation strategies rather than directional commodity positioning. This flight to safety mentality amplifies volatility as speculative capital exits energy markets.

Algorithmic Trading Response Patterns

Trading volume for front-month Brent contracts reached the lowest levels since February 27, the day before major military escalation began. This volume compression indicates several market dynamics:

- Reduced algorithmic trading activity as uncertainty parameters exceed model thresholds

- Lower retail and speculative participation due to elevated volatility

- Possible institutional position liquidation to reduce portfolio risk exposure

- Market thinning that amplifies price movements on smaller transaction volumes

These technical factors create feedback loops where reduced liquidity magnifies price swings, contributing to the elevated volatility characteristic of crisis periods.

Hedge Fund Positioning and Capital Flows

Professional investment managers demonstrate increasing preference for defensive positioning during periods of geopolitical uncertainty. The rotation into safer assets reflects institutional recognition that energy markets may remain volatile for extended periods, making traditional momentum and trend-following strategies less effective.

Capital flow patterns suggest that energy-focused hedge funds face significant challenges in current market conditions. Traditional arbitrage opportunities diminish when spot market pricing becomes disconnected from fundamental supply-demand relationships due to geopolitical risk premiums.

Economic Sector Vulnerability to Energy Price Shocks

Energy price escalation creates uneven impacts across different economic sectors, with transportation, manufacturing, and energy-intensive industries facing the most immediate pressures. Understanding these transmission mechanisms helps identify which parts of the economy are most vulnerable to sustained energy price elevation.

Transportation and Logistics Cost Transmission

The transportation sector experiences direct exposure to fuel cost increases through multiple channels. Commercial aviation, maritime shipping, and ground transportation all face immediate margin pressure when energy prices rise rapidly.

Maritime shipping costs demonstrate particular sensitivity to energy price shocks, with fuel representing 20-30% of total operating expenses for container vessels. Current supply chain disruptions compound these pressures as Iraqi oil production has slumped, with storage tanks reaching high and critical levels according to energy officials. Iraq's status as the second-biggest OPEC crude producer behind Saudi Arabia makes these production constraints particularly significant for global supply balances.

Additional pressure comes from Russia's export capacity reduction, with at least 40% of oil export capacity halted following military actions and vessel seizures. The Kirishi refinery, one of the largest in Russia, halted processing due to infrastructure damage, further constraining global refining capacity.

Manufacturing Input Cost Escalation Analysis

Energy-intensive manufacturing sectors face compound challenges from both direct energy costs and feedstock price increases. Petrochemical production, steel manufacturing, and aluminium processing represent particularly vulnerable industrial categories.

Petrochemical feedstock costs demonstrate high correlation with crude oil pricing, as many chemical processes rely on petroleum-derived raw materials. When crude prices increase 50% over several months, petrochemical producers typically experience margin compression of 15-25% unless they can pass costs through to customers.

Regional competitive dynamics shift during energy price shocks, with manufacturers in regions with lower energy costs gaining temporary advantages. This effect becomes pronounced during extended disruption periods, potentially influencing long-term industrial location decisions.

Macroeconomic Impact Assessment and Policy Implications

Sustained energy price elevation creates broader macroeconomic consequences that extend well beyond direct energy consumers. Central bank policy responses, inflation dynamics, and international trade balances all demonstrate sensitivity to energy market developments.

Inflation Transmission Mechanism Analysis

Energy price increases transmit through the economy via multiple pathways, creating both direct and indirect inflationary pressures. Direct effects appear immediately in transportation costs and utility bills, while indirect effects emerge through supply chain cost increases and wage adjustment pressures.

Current pricing scenarios suggest different inflation outcomes based on conflict duration:

| Conflict Duration | Brent Price Range ($/barrel) | Global GDP Impact | Key Economic Indicators |

|---|---|---|---|

| 1-3 months | $95-$110 | -0.2% to -0.4% | Moderate inflation spike |

| 3-6 months | $105-$130 | -0.5% to -0.8% | Recession risk elevation |

| 6+ months | $120-$150+ | -0.8% to -1.5% | Stagflation concerns |

With current Brent pricing at $108.01 per barrel, markets appear to be pricing scenarios consistent with medium-duration conflicts rather than rapid resolution expectations.

Central Bank Policy Response Frameworks

Central banks face complex trade-offs when responding to energy-driven inflation. Traditional monetary policy tools prove less effective against supply-side price shocks, as interest rate increases cannot directly address physical supply constraints.

The Federal Reserve, European Central Bank, and other major central banks typically adopt cautious approaches during energy crises, attempting to distinguish between temporary price spikes and persistent inflationary trends. However, extended energy price elevation may eventually force more aggressive policy responses if inflation expectations become unanchored.

Current Account Balance Implications

Energy-importing nations face deteriorating trade balances when oil prices rise substantially. Countries heavily dependent on energy imports may experience current account deficits expanding by 0.5-1.0% of GDP for every $20 increase in average annual oil prices.

Emerging market economies demonstrate particular vulnerability to energy price shocks due to limited fiscal resources and higher energy intensity in their economic structures. Currency weakness often amplifies these pressures by increasing the domestic cost of energy imports.

Financial Market Risk Management Evolution

Energy price volatility drives significant changes in financial market behaviour, affecting everything from equity valuations to derivative pricing structures. Understanding these adaptations helps illuminate how markets price long-term energy security risks.

Investment Strategy Realignments

Professional investors demonstrate increasing focus on energy security themes when constructing portfolios. Traditional sector allocation models require adjustment when energy markets experience sustained volatility and geopolitical risk premiums.

Energy sector equity valuations often exhibit counterintuitive behaviour during supply crises. While higher commodity prices typically support energy company revenues, geopolitical uncertainty and operational risks can simultaneously depress valuation multiples, creating complex investment dynamics. Furthermore, our recent oil price rally analysis reveals additional market complexities during volatile periods.

Derivative Market Risk Management Innovation

Oil futures markets experience structural changes during extended geopolitical crises. Traditional backwardation and contango patterns may become distorted when physical supply constraints interact with financial market positioning.

Volatility trading strategies require substantial modification when energy markets experience persistent uncertainty. Option pricing models struggle with elevated and unstable volatility parameters, making traditional hedging approaches less effective.

Cross-commodity hedging instruments gain importance as correlation patterns shift during crisis periods. Natural gas, coal, and renewable energy markets may exhibit different price relationships compared to normal market conditions.

Global Supply Chain Adaptation Strategies

International supply chains demonstrate remarkable adaptability when faced with persistent energy market disruptions. Current developments reveal both immediate tactical adjustments and longer-term strategic repositioning across multiple industries.

Diplomatic Route Management Systems

Recent developments indicate emerging patterns of selective passage management through critical shipping corridors. Thai oil tankers successfully transited following diplomatic coordination, while Malaysia announced that its vessels were being allowed passage through previously restricted areas.

These arrangements suggest the development of nationality-based or bilateral corridor management systems, where vessel passage depends on diplomatic relationships rather than purely commercial considerations. Iran's receptiveness to EU transit requests, with Spain noted as the first EU state receiving such concessions, demonstrates how geopolitical relationships increasingly influence commercial logistics.

International Coordination Framework Development

France's engagement with approximately 35 countries regarding proposals for post-conflict corridor reopening missions represents significant multilateral coordination efforts. Such initiatives indicate potential institutionalisation of energy security cooperation beyond traditional bilateral arrangements.

These coordination mechanisms may establish precedents for managing future energy security challenges, potentially creating formalised international frameworks for maintaining critical shipping lane access during geopolitical tensions. In addition, recent Venezuela oil policy impact demonstrates how diplomatic decisions shape global energy flows.

Regional Manufacturing Hub Acceleration

Supply chain managers increasingly prioritise geographic diversification to reduce dependence on single-source regions or transportation corridors. This trend accelerates during extended periods of energy market instability, as companies seek to minimise exposure to geopolitical risk.

Regional manufacturing hub development receives increased investment attention when traditional supply chains face persistent disruption risks. Countries with stable energy access and strategic geographic positioning may experience accelerated industrial development as companies relocate operations.

The next major ASX story will hit our subscribers first

Long-Term Structural Market Transformation

Current energy market disruptions are likely to generate lasting changes in how global energy systems operate, with implications extending well beyond the resolution of immediate geopolitical tensions.

Energy Security Infrastructure Investment

The Pentagon's planning to deploy thousands of airborne troops to the Gulf reflects recognition that energy corridor security requires long-term strategic commitment rather than temporary crisis response. Such military positioning indicates potential institutionalisation of security frameworks around critical energy infrastructure.

Infrastructure investment decision frameworks increasingly incorporate geopolitical risk assessment as a primary consideration rather than a secondary factor. Traditional cost-benefit analyses now require substantial risk premium calculations that account for potential supply disruption scenarios.

Consequently, the OPEC production influence becomes more significant as traditional market mechanisms face increasing pressure from geopolitical factors.

Market Structure Evolution Predictions

Energy markets may experience fundamental shifts in contract structures and pricing mechanisms as participants seek greater supply security. Long-term supply agreements may gain preference over spot market transactions, even when such arrangements carry higher average costs.

Regional pricing hub development faces acceleration as markets seek to reduce dependence on globally integrated pricing systems. Local and regional energy markets may command premium prices in exchange for reduced exposure to international geopolitical risks.

However, tension in the Middle East affecting oil prices will continue to influence global energy markets regardless of structural adaptations. The US‑China trade war effects further complicate these dynamics by creating additional supply chain pressures.

Financial Instrument Innovation Requirements

Traditional energy hedging instruments require substantial modification to address extended periods of geopolitical uncertainty. Insurance products, derivative structures, and financing arrangements all need adaptation to function effectively in environments characterised by persistent supply chain risks.

The development of sovereign guarantee programmes and international insurance pools may become necessary to maintain viable international energy trade during periods of elevated geopolitical risk. Such mechanisms would represent significant evolution from current market-based risk management approaches.

Furthermore, the transition to renewable energy transformations offers potential long-term solutions to reduce dependence on volatile fossil fuel markets. Recent analysis by leading energy research institutions suggests that diversification strategies may provide increased energy security over time.

For instance, while tension in the Middle East affecting oil prices remains a persistent concern, alternative energy sources could gradually reduce exposure to traditional geopolitical risks. This transformation represents one of the most significant structural changes facing global energy markets in the coming decade.

This analysis is based on market data and expert assessments as of March 2026. Energy market conditions remain highly dynamic, and actual outcomes may differ from projections. Investors should conduct independent analysis and consult financial advisors before making investment decisions based on energy market volatility.

Ready to capitalise on energy sector volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including energy-related commodities that benefit during global supply disruptions. With major infrastructure vulnerabilities creating unprecedented opportunities in alternative energy and critical minerals, subscribers gain actionable insights to position themselves ahead of market movements through our dedicated discoveries page showcasing historic returns.