July 20, 2026

The Quiet Mineral That Could Determine the Pace of the Global Energy Transition

Before a single lithium-ion battery cell powers an electric vehicle, before any charge flows through a drivetrain, a supply chain decision made years earlier determines whether that vehicle can be built at all. Tesla reducing dependence on China graphite imports has become one of the most closely watched strategic pivots in modern manufacturing, and the mineral at the centre of that decision is not lithium, not cobalt, and not nickel. It is graphite, and its role in the EV revolution remains one of the most underappreciated structural vulnerabilities in modern energy policy.

The numbers are striking. A single EV battery pack requires roughly ten times more graphite by weight than lithium, yet graphite rarely commands the same policy attention or investment urgency. This asymmetry between graphite's physical indispensability and its relative obscurity in public discourse has created a dangerous blind spot, one that geopolitical events in late 2024 forced into sharp relief.

When big ASX news breaks, our subscribers know first

Why China's Graphite Position Is Deeper Than Most Investors Realise

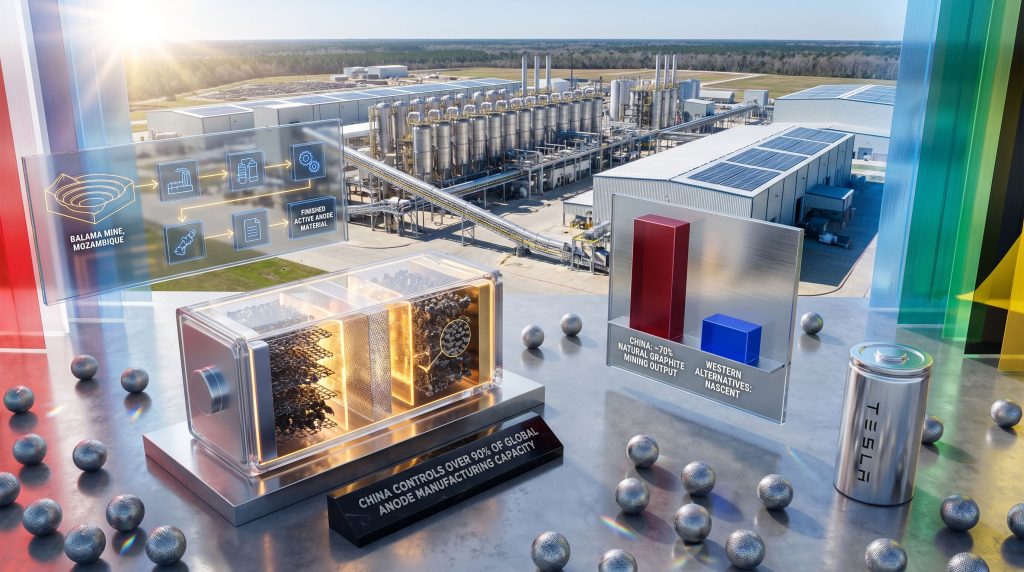

Understanding the true depth of China's graphite dominance requires separating two distinct parts of the supply chain that are often conflated: mining and processing. According to Benchmark Mineral Intelligence, China accounts for approximately 70% of global natural graphite mining output. That figure alone is significant. However, it is the processing stage where China's advantage becomes genuinely structural.

China controls over 90% of global anode manufacturing capacity, the refining and processing stage that converts raw graphite ore into the battery-grade Active Anode Material (AAM) that cell manufacturers actually require. This processing dominance is the product of decades of industrial policy, infrastructure investment, and accumulated technical expertise that Western nations have not replicated. Concerns around the global graphite shortage have further amplified the urgency of addressing this imbalance.

"The graphite supply chain risk is not primarily a mining problem. It is a processing and refining problem. Building mines outside China without building refineries solves only half the equation."

Western nations have historically directed critical mineral investment toward upstream exploration and extraction. The downstream processing stages, spheronisation, purification, surface coating, and electrochemical qualification, have remained almost entirely within Chinese industrial infrastructure. This is the chokepoint that Tesla and other major battery manufacturers now confront when attempting to diversify away from Chinese graphite.

The December 2024 Export Control Shock and What It Revealed

In December 2024, China introduced targeted export controls on graphite products directed at the United States. The restrictions arrived with minimal advance notice, exposing a structural fragility that procurement models built around stable Chinese supply had failed to adequately account for. Furthermore, China's export restrictions on other critical materials had already signalled that such disruptions were a genuine policy tool, not merely a theoretical risk.

The impact was immediate and instructive. Battery manufacturers operating on just-in-time inventory models found themselves with limited buffer stock and no immediately scalable alternative. The shock was not merely logistical; it reframed graphite from a procurement line item into a national energy security variable.

| Risk Factor | Pre-2024 Assessment | Post-December 2024 Reality |

|---|---|---|

| Supply continuity | Assumed stable | Actively disrupted by policy action |

| Cost competitiveness | Chinese supply cheapest globally | Tariff and restriction costs rising sharply |

| Geopolitical exposure | Moderate background risk | Confirmed as a live policy-driven threat |

| Alternative source readiness | Nascent, underfunded | Accelerating but still underdeveloped |

The simultaneous operation of U.S. tariff policy and Chinese export restrictions created a dual-pressure environment that fundamentally altered the cost-benefit calculus of maintaining Chinese graphite dependency. For the first time, the geopolitical risk premium on Chinese supply became quantifiable in real-time commercial terms.

Tesla's Dual-Track Graphite Strategy: Bridge and Hedge Simultaneously

Tesla's approach to graphite supply diversification defies simple characterisation. On one hand, the company has continued to seek tariff exemptions on Chinese graphite imports as recently as 2026, formally acknowledging in exemption requests that it had been unable to identify non-Chinese sources capable of simultaneously meeting its volume requirements, purity specifications, and battery qualification standards.

This candid admission from one of the world's most sophisticated manufacturers illustrates the gap between strategic aspiration and operational reality in critical mineral supply chains. In addition, the broader battery raw materials market continues to evolve rapidly, placing further pressure on manufacturers to accelerate their diversification timelines.

On the other hand, Tesla has maintained and expanded supply agreements specifically designed to develop non-Chinese sourcing pipelines, absorbing higher costs and extended qualification timelines that shorter-term procurement logic would not justify. The company's sustained engagement with Syrah Resources is the clearest expression of this longer-horizon thinking.

"Tesla is operating a dual-track graphite strategy: maintaining Chinese supply as an operational bridge while investing in Western supply infrastructure as a long-term hedge. This is not contradiction; it is risk-managed transition management."

This approach reflects a broader strategic shift occurring across advanced manufacturing sectors: energy security is being weighted alongside, and in some cases above, immediate cost efficiency. The December 2024 export control episode provided concrete evidence for why that weighting is rational, even if it carries short-term commercial cost.

The Syrah Resources Partnership: Anatomy of the West's Most Strategic Graphite Facility

What Makes Vidalia Unique in the Global Anode Landscape

Syrah Resources operates what is currently the only vertically integrated graphite anode production facility of meaningful commercial scale located outside China. The Vidalia plant, situated in Louisiana, processes raw graphite sourced from Syrah's Balama mine in Mozambique into Active Anode Material, the battery-ready form of graphite that cell manufacturers require as direct input.

This vertical integration, spanning from African mine to American processing facility, represents precisely the end-to-end supply chain architecture that Western battery manufacturers require to genuinely reduce Chinese dependency rather than simply shift one upstream bottleneck to another location.

The Commercial Timeline: A Relationship Tested by Near-Termination

The foundational supply agreement between Tesla and Syrah Resources was established in 2021, under terms committing Syrah to supply 8,000 metric tonnes of Active Anode Material across a four-year period. The intervening years tested that relationship severely.

Tesla issued a termination notice in July 2025, subsequently extending the remedy period on four separate occasions before ultimately withdrawing the termination notice entirely. The decision to withdraw followed Syrah's demonstration that the Vidalia facility could produce conforming Active Anode Material meeting the required specifications, though final qualification against Tesla's specific battery cell requirements remains outstanding.

The repeated near-termination events, and Tesla's ultimate decision to remain in the agreement, reveal something important about how major OEMs are evaluating non-Chinese supply partnerships. The tolerance for operational friction and delayed milestones is substantially higher than it would be in a purely commercial procurement relationship, suggesting that strategic supply chain architecture objectives are overriding short-term performance metrics.

U.S. Department of Energy Involvement

The U.S. Department of Energy has actively supported the Vidalia project, approving commercial deadline extensions and providing federal funding as part of a broader objective to localise critical battery material supply chains within domestic or allied-nation borders. This institutional support, alongside growing awareness of critical minerals and energy security, has been a material enabler of the project's survival through its operational challenges.

How Vidalia Compares to Chinese Anode Production: An Honest Assessment

| Dimension | Vidalia Facility (Syrah Resources) | Chinese Anode Industry |

|---|---|---|

| Location | Louisiana, USA | Primarily Shandong, Inner Mongolia |

| Raw material source | Balama mine, Mozambique | Domestic Chinese natural graphite |

| Processing integration | Fully vertically integrated | Vertically integrated at massive scale |

| Annual contracted volume | 8,000 MT (Tesla agreement) | Millions of MT across multiple producers |

| OEM qualification status | Conforming material produced; final qualification pending | Fully qualified across major global OEMs |

The scale differential is the most important number in this comparison. China's anode manufacturing industry operates at a volume that Western facilities cannot replicate within any realistic 3-to-5 year investment horizon without an unprecedented mobilisation of capital and technical expertise. The Vidalia facility's strategic value lies not in volume replacement but in proof of concept at commercial scale, demonstrating that non-Chinese AAM production is technically and commercially feasible.

The next major ASX story will hit our subscribers first

Step-by-Step: How Non-Chinese Graphite Becomes Battery-Ready Anode Material

Understanding why building supply chains outside China is technically challenging requires following the actual production process from mine to battery:

- Natural graphite mining – Raw graphite ore is extracted from geological deposits such as the Balama mine in Mozambique, one of the largest flake graphite deposits globally.

- Concentration and purification – Ore is processed through flotation and chemical treatment to increase graphite content and remove silicate and other impurities.

- Spheronisation – Graphite flakes are mechanically shaped into spherical particles, a critical step that optimises how lithium ions intercalate within the anode during charging and discharging cycles.

- Surface coating and treatment – Coatings, typically carbon-based, are applied to improve the material's electrochemical performance, first-cycle efficiency, and long-term cycle life.

- Active Anode Material production – The finished, battery-grade material is produced and characterised against electrochemical specifications.

- Cell manufacturer qualification – The AAM is tested within actual battery cell formats and validated against the specific performance requirements of the OEM, a process that can take 12 to 24 months.

- Commercial supply at sustained scale – Qualified material must be delivered consistently at volumes matching battery production schedules.

"Steps 3 through 6 represent the processing and qualification stages where Chinese manufacturers hold overwhelming capability advantages. Western supply chain development must prioritise these stages, not just step 1."

A lesser-known technical detail that carries significant investment implications: the spheronisation step generates substantial waste material, often yielding only 30% to 40% usable spherical graphite from the input flake. Chinese manufacturers have developed efficient recycling streams for this waste material over decades of industrial operation. Western facilities starting from scratch must either absorb the economics of that waste or invest in secondary processing infrastructure simultaneously, adding cost and complexity that is rarely captured in headline capacity figures.

Alternative Pathways: Silicon Anodes and Synthetic Graphite

The Silicon Anode Proposition

Group14 CEO Rick Luebbe has articulated a compelling strategic case: reducing dependence on graphite simultaneously reduces exposure to a single dominant supplier nation and diversifies regional supply chains at the material level, not just the geographic level. Silicon-based anode materials offer higher energy density than graphite and, if produced domestically, would eliminate China's processing advantage at the anode stage entirely.

The technical obstacles facing silicon anodes, particularly volumetric expansion during lithiation that degrades cell structure over charge cycles, remain significant. However, progress in silicon-carbon composite architectures is accelerating, and commercial deployment in premium EV segments is increasingly anticipated within this decade.

Synthetic Graphite as a Domestic Alternative

Synthetic graphite, manufactured from petroleum coke through high-temperature graphitisation, offers a pathway to domestic U.S. production that entirely bypasses Chinese mining and natural graphite processing. Panasonic, in partnership with Novonix, is developing U.S.-based synthetic graphite capacity with Department of Energy support.

Synthetic graphite carries a cost premium over natural graphite alternatives and requires energy-intensive production processes, but its supply chain geography is far more controllable. For manufacturers prioritising supply certainty over marginal cost optimisation, synthetic graphite represents a structurally different value proposition than natural graphite sourced from politically exposed geographies.

Allied-Nation Mining Expansion

Graphite mining projects at various development stages in Canada, Tanzania, and Australia are expanding the potential upstream supply base beyond Chinese-controlled sources. However, a critical and frequently overlooked point: without corresponding investment in processing infrastructure, raw graphite ore extracted in allied nations must still be sent to China for spheronisation, coating, and anode manufacturing. The battery supply chain expansion efforts underway across allied nations underscore how critical it is to build processing capacity alongside mining development.

The Economic Trade-offs of Diversifying Away from Chinese Graphite

The cost premium associated with non-Chinese graphite supply is real and should not be minimised. Chinese natural graphite and anode material has historically been priced significantly below Western alternatives due to lower labour costs, established infrastructure, state industrial support, and extraordinary scale economies accumulated over two decades of battery material industrialisation.

Non-Chinese supply chains carry meaningful cost premiums that U.S. federal incentives partially offset but do not eliminate. The more important economic insight, however, is that traditional procurement models have systematically underpriced the geopolitical risk embedded in Chinese supply. Tesla's sourcing pivot to Mozambique demonstrates concretely that the cost advantages of Chinese supply can be neutralised almost instantaneously by supply disruption, converting what appeared to be a cost saving into a supply chain emergency.

Companies that invested early in supply diversification, accepting short-term cost premiums, are now positioned to avoid the operational disruption and reputational costs of supply chain failure during precisely the period when EV production ramp-up is most strategically important.

Outlook: Three Horizons for Western Graphite Supply Chain Independence

Near Term: 2025 to 2027

- Chinese graphite will remain the dominant source of anode material for most Western EV manufacturers through at least 2027.

- Facilities like Vidalia will achieve commercial qualification and begin delivering meaningful non-Chinese volumes, but will not replace Chinese supply at scale.

- U.S. tariff and export control dynamics will continue raising the effective cost of Chinese dependency, accelerating private capital investment in alternative supply development.

Medium Term: 2028 to 2032

- Domestic U.S. synthetic graphite capacity from producers including Novonix is expected to reach commercial scale, providing a geographically secure alternative to natural graphite imports.

- Silicon anode technology is likely to achieve meaningful commercial deployment in premium EV segments, beginning to reduce per-vehicle graphite demand intensity.

- Allied-nation processing infrastructure, if investment momentum is sustained, could deliver a genuinely diversified natural graphite anode supply chain for the first time.

The Structural Question That Determines the Outcome

The pace of Tesla reducing dependence on China graphite imports, and the broader Western battery industry doing the same, is ultimately determined by three variables: the continuity of capital deployment, the consistency of policy support across electoral cycles, and the time required for OEM qualification processes. All three are subject to political and commercial uncertainty that no supply chain model can fully eliminate.

Tesla's decision to sustain its Syrah Resources partnership through four near-termination events signals that at least one of the world's most consequential battery manufacturers is prepared to absorb short-term commercial friction to secure long-term supply chain resilience. Whether that commitment is replicated across the broader industry at sufficient scale and speed remains the defining open question for critical mineral energy security planning through the end of this decade.

"The Vidalia facility proves that non-Chinese AAM production is technically and commercially feasible. The question is whether investment, policy continuity, and OEM commitment will sustain the pace required to meaningfully reduce Chinese dependency before the next supply disruption event arrives."

This article contains forward-looking statements regarding supply chain development timelines, technology commercialisation, and market trajectories. These represent analytical assessments based on currently available information and should not be construed as investment advice. Actual outcomes may differ materially from projections due to geopolitical, commercial, technical, and regulatory factors beyond any party's control.

Want to Stay Ahead of the Next Major Critical Minerals Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including graphite and other battery materials central to the energy transition — instantly transforming complex geological announcements into actionable investment insights. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.