June 14, 2026

When Open Pits Run Out of Room: The Strategic Logic Behind Underground PGM Mining

Every open-pit mine carries within it the seed of its own obsolescence. As surface ore bodies are progressively excavated, the economic geometry of surface stripping eventually inverts: the cost of removing ever-greater volumes of waste rock to access diminishing ore grades eventually surpasses the cost of going underground. For platinum group metal operations situated along South Africa's Bushveld Complex, this inflection point is not a distant theoretical concern. It is a scheduled operational reality, and how a mining company prepares for it determines whether a world-class asset becomes a legacy operation or a stranded one.

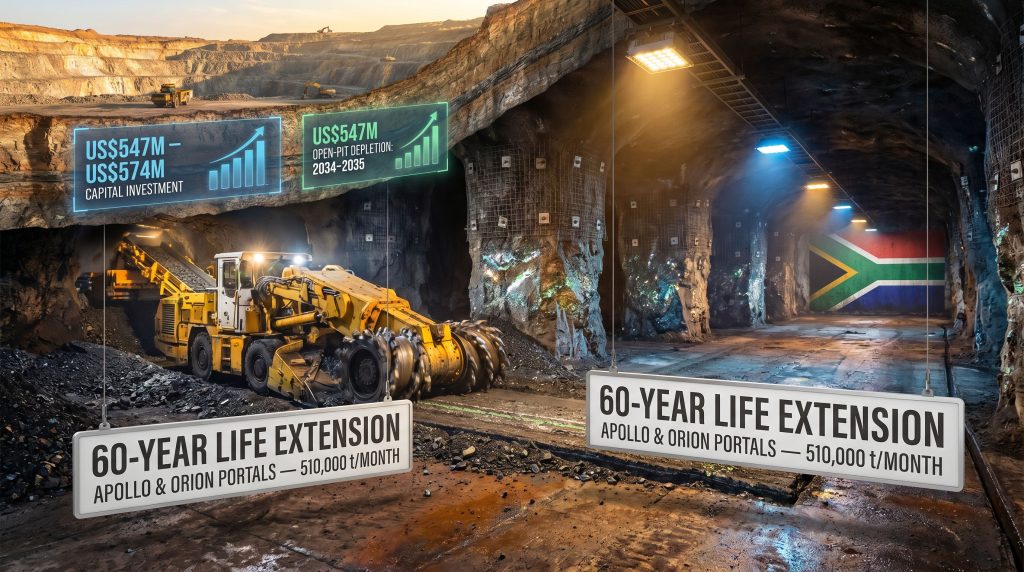

The Tharisa underground mining transition represents one of the most substantive examples of pre-engineered mine life extension currently underway in the global PGM sector. With a capital commitment ranging between US$547 million and US$574 million, a phased dual-portal development strategy, and a projected 60-year extension of operational life, the project reframes what long-duration supply security looks like in a commodity class increasingly critical to the energy transition.

When big ASX news breaks, our subscribers know first

The Open-Pit Horizon and Why It Matters

Tharisa's open-pit operation, which currently processes ore at a rate of 5.6 million tonnes per annum (Mtpa), is projected to reach depletion somewhere between 2034 and 2035. That timeline is not a surprise to the company's management. The transition to underground mining was embedded in Tharisa's long-range operational planning from its earliest stages, reflecting an understanding that the ore body's real value lay not just in its accessible surface expression, but in its deeper, laterally continuous reef geometry.

This distinction matters considerably for investors assessing mine-type transitions. Many underground conversions across the African mining sector have been reactive, triggered by deteriorating open-pit economics, balance sheet pressure, or unexpected reserve downgrades. Tharisa's transition is architecturally different. It was conceived as a natural operational progression rather than a crisis-driven pivot, and that pre-planned character reduces the execution uncertainty that typically weighs on valuations during major mine-type conversions.

The transition from open-pit to underground was not an emergency response to declining surface grades. It was a deliberate, long-range engineering outcome that the company had anticipated and prepared for over many years.

The first underground blast, achieved in late March 2026, marked the physical beginning of subsurface access development. Formal transition work commenced in 2025, with underground ore production expected to ramp progressively through the latter half of the decade as the two development portals advance through their respective ore zones. Furthermore, the phased transition plan published by Tharisa outlines the precise engineering sequence underpinning this progression.

How the Underground Project Is Structured: Apollo and Orion

The underground project is built around a phased, dual-portal architecture designed to open two parallel ore extraction corridors into the deposit.

Phase 1: Apollo Portal (Western Access)

The Apollo portal, positioned on the western side of the ore body, constitutes the first development vector. Apollo serves as the primary infrastructure corridor for early underground ore delivery, prioritising western ore zones to maintain feed continuity to the existing processing plant during the open-pit wind-down period. This sequencing is critical. Any gap in plant feed during the transition period would directly impair revenue and compress the economic bridge between surface and underground production.

Phase 2: Orion Portal (Eastern Expansion)

The Orion portal, located on the eastern side of the deposit, forms the second major development phase. Rather than replacing Apollo, Orion is designed to complement it by creating a parallel extraction corridor that, when combined with Apollo, delivers the project's full throughput target.

| Development Phase | Portal | Location | Primary Function |

|---|---|---|---|

| Phase 1 | Apollo | Western ore body | Primary access and early ore production |

| Phase 2 | Orion | Eastern ore body | Parallel extraction corridor |

| Combined Target | Both | Full ore body | ~510,000 tonnes per month |

The combined throughput of approximately 510,000 tonnes per month from both portals is engineered to feed directly into the existing 5.6 Mtpa surface processing infrastructure. This integration is one of the most important capital efficiency factors in the project's financial architecture. Rather than constructing a new processing facility to service the underground operation, Tharisa leverages its existing plant, tailings management systems, and surface infrastructure, consequently compressing both capital intensity and construction risk compared to a greenfield underground development.

Bord-and-Pillar Mining: The Method Behind the Transition

The selection of the bord-and-pillar mining method for the Tharisa underground mining transition is not arbitrary. It reflects a precise alignment between extraction methodology and ore body geometry.

Bord-and-pillar is an underground mining engineering technique in which ore is removed in a systematic grid pattern, with structured columns of unmined material, called pillars, left in place to support the overlying rock mass. The excavated spaces between pillars, known as bords, are where the actual ore extraction occurs. The method is highly amenable to mechanisation, allows for predictable ground control outcomes in appropriate geological settings, and supports high production rates relative to development capital.

Bord-and-pillar is among the most widely deployed mining methods across South Africa's platinum belt, including at several major Bushveld Complex operations. Its proven track record in the region provides a critical risk management advantage for the Tharisa transition.

Tharisa's reef geometry, characterised by laterally continuous, shallow-dipping chromite and PGM mineralisation, aligns closely with the geological profile for which bord-and-pillar was designed. Flat-lying tabular deposits require a different approach to three-dimensional extraction than steeply dipping or irregular ore bodies, and bord-and-pillar's grid-based logic suits the systematic nature of Tharisa's reef architecture.

A less widely understood dimension of bord-and-pillar operations is the strategic optionality embedded in pillar recovery. In later mining phases, pillars can potentially be mined out using secondary extraction techniques, unlocking additional resource value from ore that was deliberately left in place during primary extraction. This adds a layer of resource upside that is not always visible in initial reserve statements.

Capital Commitment and Financial Architecture

At US$547 million to US$574 million, the capital requirement for the Tharisa underground mining transition is substantial. The variation in estimates across reporting periods reflects the iterative nature of project costing as engineering design advances from concept through feasibility to execution.

| Financial and Operational Metric | Value |

|---|---|

| Estimated transition capital | US$547M to US$574M |

| Underground throughput target | ~510,000 tonnes per month |

| Processing plant capacity (existing) | 5.6 Mtpa |

| Projected mine life extension | ~60 years |

| Open-pit depletion timeline | ~2034 to 2035 |

To contextualise this capital commitment, consider the alternative. Developing a comparable greenfield underground PGM mine from initial resource discovery through to sustained production typically demands significantly higher capital per tonne of reserve, combined with a development lead time of anywhere between 10 and 15 years. Tharisa's brownfield transition avoids the most capital-intensive elements of that pathway. The existing processing plant, tailings facility, water management infrastructure, access roads, and trained workforce all carry forward into the underground phase, reducing the effective capital cost per tonne of future production.

The primary cost escalation risks over a multi-year capital programme of this scale include:

- Inflationary pressures on steel, cement, and explosives in South Africa's current operating environment

- Skilled underground labour availability and wage escalation in a sector competing for experienced personnel

- Schedule slippage driven by geotechnical surprises at depth, including unexpected water ingress or rock mass variability

- Currency exposure on imported capital equipment against rand-denominated operating costs

None of these risks are unique to Tharisa, but they are inherent features of any multi-year underground capital programme and should inform investor expectations around capital delivery.

PGM Supply Security and the 60-Year Asset

South Africa contributes approximately 70 to 80 percent of global platinum supply, with the majority of that production sourced from the Bushveld Complex, the world's largest known repository of platinum group metals. The health and longevity of individual operations within this complex carry direct implications for global PGM supply chains, particularly as demand profiles for these metals evolve. Indeed, PGM supply constraints across the Bushveld Complex continue to shape long-term commodity market outlooks.

Platinum group metals serve three primary demand sectors:

- Automotive catalytic converters for internal combustion engine vehicles, representing the largest current demand source for platinum and palladium

- Hydrogen fuel cell technology, where platinum serves as the primary catalyst in proton exchange membrane fuel cells, positioning it as a critical input for the hydrogen economy

- Industrial chemical processes, including nitric acid production and petroleum refining, where PGMs function as irreplaceable process catalysts

Against this demand backdrop, a 60-year mine life extension at an established Bushveld Complex operation carries long-term supply significance. Most new PGM project proposals globally struggle to demonstrate even 20 to 30 years of resource life certainty, and new mine development pipelines for PGMs remain constrained by permitting timelines, capital market conditions, and grade scarcity.

The timing of Tharisa's underground transition also intersects with a broader structural trend across sub-Saharan Africa's mining sector. A growing number of established open-pit operations are now evaluating or executing underground transitions as first-generation surface reserves approach depletion. For instance, the Anglo Platinum mega-mine development illustrates how major producers are similarly investing in long-duration underground assets across the same geological province.

The next major ASX story will hit our subscribers first

ESG Dimensions of Going Underground

Underground mining operations generally carry a meaningfully smaller surface disturbance footprint than their open-pit equivalents. As the Tharisa underground mining transition progresses and the open pit reaches end-of-life, the reduction in active pit expansion, waste rock movement, open blasting, and associated dust and noise impacts represents a tangible improvement in the operation's environmental profile.

For ESG-focused institutional investors, this transition trajectory is a relevant consideration. The surface rehabilitation of legacy open-pit infrastructure combined with a subsurface extraction model reduces the visible landscape impact of the operation. Furthermore, mine reclamation importance is increasingly factored into institutional investment frameworks when evaluating the long-term sustainability of resource sector allocations.

In addition, the operation's role in supplying PGMs critical to hydrogen fuel cells and emissions control technology connects Tharisa directly to the broader energy transition mining narrative, reinforcing the strategic relevance of the asset beyond conventional commodity cycles.

Key Risks Investors Should Understand

Beyond capital execution risk, the Tharisa underground transition introduces several geotechnical and operational complexities absent from surface mining:

- Ground control management: Underground environments require ongoing assessment of seismicity, pillar stability, and hanging wall behaviour, particularly as mining advances to greater depths

- Water ingress: The Bushveld Complex geology includes zones of groundwater connectivity that can challenge underground workings and require active dewatering infrastructure

- Transition period feed management: The simultaneous wind-down of open-pit production and ramp-up of underground ore delivery creates a scheduling challenge where any feed shortfall to the processing plant directly impacts throughput and revenue

- Labour and skills requirements: Underground mining demands different skill sets from surface operations, requiring workforce development investment ahead of full underground production

The phased Apollo-then-Orion development sequence is specifically designed to manage the feed continuity risk by establishing underground production progressively before the open pit reaches depletion. Execution discipline around this sequencing will be a critical indicator of project delivery quality. As noted by Mining Weekly's analysis of the transition, the sequencing strategy reflects careful consideration of both geological and commercial realities.

Frequently Asked Questions

When did the Tharisa underground mining transition formally begin?

Formal transition work commenced in 2025, with the first underground blast recorded in late March 2026, marking the start of active subsurface access development.

How long will the underground project extend Tharisa's mine life?

The underground project is designed to extend operational life by approximately 60 years beyond the projected open-pit depletion date of around 2034 to 2035.

What mining method is being used underground?

Tharisa has selected the bord-and-pillar method, a mechanised underground technique well-suited to the flat-lying, tabular geometry of its chromite and PGM reef deposits.

What is the capital cost of the transition?

Estimates range between US$547 million and US$574 million, reflecting different reporting periods and updated engineering assessments.

What is the planned underground production rate?

The combined Apollo and Orion portal system is designed to deliver approximately 510,000 tonnes per month, feeding into the existing 5.6 Mtpa surface processing plant.

What the Tharisa Underground Transition Signals for the Sector

The Tharisa underground mining transition is not simply an operational engineering milestone for one company. It is a case study in how long-duration PGM assets can be structured to outlast the finite horizons of surface mining. The deliberate, pre-planned nature of the transition, the capital-efficient integration with existing processing infrastructure, and the 60-year life extension it unlocks together represent a model that will attract increasing attention from investors and operators across Africa's maturing mining landscape.

- A 60-year life extension repositions the asset from mid-life to generational

- The phased Apollo-Orion framework provides structured, risk-managed production continuity

- US$547M to US$574M in capital delivers a brownfield underground operation at a fraction of greenfield development cost

- Bord-and-pillar methodology aligns with proven regional practice and Tharisa's geological conditions

- Existing processing infrastructure integration is the single largest capital efficiency advantage in the project

- The transition positions Tharisa as a long-duration supplier in a supply-constrained, energy-transition-critical commodity

This article contains forward-looking statements and projections related to mine development timelines, capital estimates, and production targets. These involve inherent uncertainties and should not be construed as financial advice. Readers should conduct independent due diligence before making investment decisions.

For broader perspectives on African mining investment trends, operational developments, and industry analysis, visit the Mining Indaba content platform.

Want to Identify the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex mineral data into clear, actionable insights for both short-term traders and long-term investors — explore historic discoveries that have generated substantial returns and begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.