May 14, 2026

The Geometry of Frontier Risk: Why Major Oil Companies Target Unproven Basins

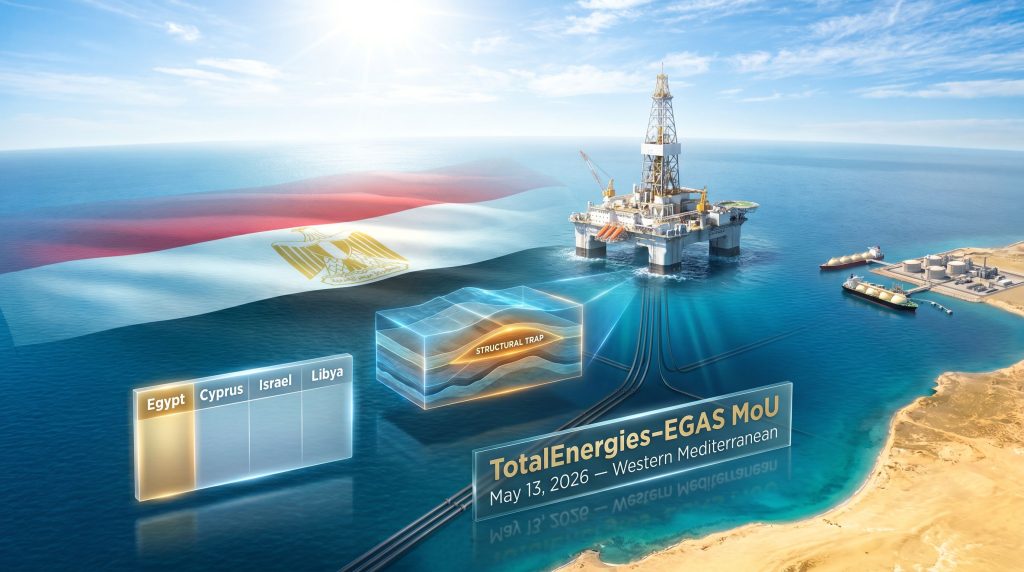

There is a counterintuitive logic embedded in how the world's largest energy companies allocate exploration capital. When acreage in proven basins becomes expensive, contested, or depleted, frontier environments quietly move up the priority list. The question is never whether frontier exploration is risky. It always is. The question is whether the risk-adjusted opportunity is compelling enough, and whether the technical and commercial infrastructure exists to convert geological potential into bankable reserves. That calculus is playing out right now across the Western Mediterranean, and the TotalEnergies EGAS offshore Egypt exploration MoU signed on May 13, 2026 represents one of the clearest signals yet that attention is shifting to Egypt's underexplored northwestern continental margin.

When big ASX news breaks, our subscribers know first

Egypt's Northwest Offshore: A Frontier Within a Producing Nation

Egypt occupies an unusual position in regional energy geopolitics. It is simultaneously a mature gas-producing nation with declining legacy fields, a re-export hub with functioning LNG infrastructure, and a frontier exploration destination where large swaths of offshore acreage remain poorly characterised at depth.

The Eastern Mediterranean's production story is well documented. The Zohr field, discovered by ENI in 2015 in Egyptian waters, reshaped regional gas supply dynamics by adding substantial deepwater reserves to Egypt's production base. The Leviathan and Tamar fields off Israel's coast confirmed the Levantine Basin's prolific character. These discoveries collectively repositioned the Eastern Mediterranean as a strategically significant gas province.

What received far less attention was the northwest. Egypt's northwestern offshore zone, including the waters associated with the Herodotus Basin, remained comparatively underexplored even as the eastern plays attracted billions in capital. The Herodotus Basin is a deepwater sedimentary structure with geological characteristics that researchers and exploration teams have increasingly identified as warranting serious evaluation, though its subsurface potential is far less defined than the Levantine Basin's now-established play types.

This asymmetry of knowledge and capital is precisely what makes frontier agreements like the TotalEnergies EGAS offshore Egypt exploration MoU analytically significant. Frontier acreage is not valuable because it is proven. It is valuable because the cost of entry is low, the upside can be disproportionately large, and the first party to acquire reliable subsurface data holds a structural advantage over any competitor arriving later.

Egypt's Gas Architecture and the Reserve Replacement Imperative

Egypt's transformation from a net gas importer into a meaningful LNG exporter following the Zohr development required substantial capital and institutional commitment. However, sustaining that export position over the long term is not guaranteed. Legacy fields age, production profiles decline, and new feedstock must continuously enter the supply chain to keep LNG terminals operating at commercially viable throughput levels. The LNG supply outlook for 2025 and beyond underscores just how competitive this market has become.

Egypt operates two liquefaction facilities with international significance: the Idku LNG Terminal and the Damietta LNG Terminal. Both facilities represent sunk infrastructure that can only generate returns if domestic gas production remains sufficient to satisfy both internal consumption and export commitments. The pressure on Egyptian upstream planners to identify and develop new reserves is therefore structural, not cyclical. It exists regardless of short-term oil price movements or commodity cycles.

This is the systemic context within which the northwest offshore frontier takes on strategic importance. New deepwater discoveries in that region would not merely add to Egypt's reserve inventory. They would directly underpin the commercial viability of infrastructure that already exists and has already been paid for.

Anatomy of the TotalEnergies EGAS Offshore Egypt Exploration MoU

The MoU was formally executed on May 13, 2026, with Egyptian Prime Minister Dr. Mostafa Madbouly present at the signing ceremony. According to EGAS's official communication, the two companies intend to conduct natural gas exploration activities across a substantial area in the Western Mediterranean region, with a technical cooperation framework covering preliminary exploration and subsurface evaluation activities as the foundation of the arrangement.

It is important to understand what an MoU at this stage does and does not represent. In upstream oil and gas, a memorandum of understanding is a pre-commercial instrument. It is not a production licence, not a production sharing agreement (PSA), and not a binding drilling commitment. It establishes the conditions under which two parties will cooperate on joint technical work before either party makes an irreversible capital commitment.

The practical significance of this structure is that it allows TotalEnergies to acquire subsurface knowledge and evaluate the commercial case for deeper engagement without committing to a full exploration licence upfront. For EGAS and the Egyptian government, the MoU attracts a technically capable international partner whose evaluation work adds value to Egyptian acreage data regardless of whether it proceeds to a binding agreement.

Why Prime Ministerial Presence Carries Weight in Upstream Deal-Making

The witnessing of this MoU signing by Egypt's Prime Minister was not a formality. In upstream investment circles, the level of political attention directed at an agreement sends a clear signal about how a host government prioritises a particular partnership. According to EGAS's own reporting on the event, Dr. Madbouly confirmed the Egyptian government's support for attracting further investment in exploration and upstream activities through incentives and facilitation measures provided to international partners.

This kind of high-level sovereign engagement reduces what petroleum economists describe as above-ground risk. For an international operator conducting due diligence on a potential exploration commitment, knowing that a host government views a project as a priority can materially affect internal risk assessments and investment committee deliberations. Furthermore, TotalEnergies' agreement with EGAS reflects a broader pattern of sovereign-backed partnerships that carry added weight in frontier markets.

TotalEnergies' Mediterranean Mosaic: Portfolio Logic Behind the Timing

The timing of the TotalEnergies EGAS offshore Egypt exploration MoU is not incidental. It was executed on May 13, 2026, one day after TotalEnergies finalised offshore exploration agreements in Syria involving partnerships with ConocoPhillips and QatarEnergy.

This clustering of Mediterranean commitments within a 48-hour window reveals something important about how major international oil companies build exploration portfolios in geopolitically complex regions. Rather than concentrating capital in a single high-conviction play, the strategy involves acquiring optionality across multiple frontier positions simultaneously. Understanding the broader geopolitical risk landscape helps contextualise why diversification across Mediterranean jurisdictions has become strategically attractive.

The table below summarises TotalEnergies' known Mediterranean exploration activity around this period:

| Agreement | Date | Region | Partners | Stage |

|---|---|---|---|---|

| EGAS MoU – Northwest Egypt | May 13, 2026 | Western Mediterranean | EGAS | Technical cooperation framework |

| Syria Offshore Block 3 | May 12, 2026 | Eastern Mediterranean | ConocoPhillips, QatarEnergy | Exploration agreement |

| Neho Block – Offshore Egypt | Prior to 2026 | Offshore Egypt | EGAS | Active concession |

| Tarif Deep-1 – Egypt | Prior to 2026 | Onshore Egypt | EGAS | Active drilling programme |

TotalEnergies was not entering Egypt as a newcomer when this MoU was signed. The company already held an active offshore concession in the Neho Block and had ongoing drilling activity through the Tarif Deep-1 onshore programme. This existing footprint provides operational familiarity, institutional relationships with EGAS, and importantly, subsurface datasets that can inform geological modelling of adjacent or geologically analogous areas.

Three Scenarios: From MoU to Material Outcome

Frontier exploration agreements are inherently probabilistic. The eventual commercial outcome of the TotalEnergies EGAS offshore Egypt exploration MoU depends on subsurface results, commodity prices, competitive dynamics, and regulatory processes that are not yet determined. Three scenarios represent the plausible range of outcomes:

Scenario A: Accelerated Commercialisation

- Subsurface evaluation confirms material gas accumulations in the target area

- The MoU converts into a formal PSA within 18 to 36 months

- TotalEnergies becomes operator of a new deepwater block with EGAS as state co-venturer

- New reserves contribute to Egypt's export capacity in the post-2030 period

Scenario B: Extended Technical Evaluation

- Early seismic reprocessing produces inconclusive results requiring additional data acquisition

- Both parties agree to extend the MoU framework pending new 3D seismic campaigns

- Exploration timeline extends beyond five years before any drilling commitment is made

- The MoU functions as a strategic placeholder while portfolio risk is managed

Scenario C: Competitive Licensing Dynamics

- Other major operators accelerate interest in adjacent northwest Egyptian acreage

- Egypt uses the TotalEnergies MoU as a catalyst to launch a competitive licensing round

- TotalEnergies must compete against rivals including ENI, BP, or Shell for formal concession rights

- First-mover data advantage may or may not translate into preferred access

Disclaimer: The above scenarios are speculative frameworks constructed for analytical purposes. They do not constitute investment advice or predictions about commercial outcomes. Actual results will depend on subsurface findings, regulatory decisions, and market conditions that are not currently determinable.

The Technical Workflow: From Cooperation Framework to Drillable Prospect

Understanding what the MoU enables technically requires a working knowledge of how deepwater frontier exploration actually progresses from initial agreement to investment-ready decision.

Stage 1: Subsurface Data Compilation and Reprocessing

The first phase of any frontier evaluation involves compiling all available existing data. In northwest Egyptian waters, this typically includes legacy 2D seismic lines acquired during earlier regional surveys, potential field data from gravity and magnetic surveys, and any well data from historical exploration on the outer shelf. Modern reprocessing algorithms, including pre-stack depth migration and full-waveform inversion techniques, can extract significantly more geological information from legacy datasets than was possible when those surveys were originally acquired.

This stage is relatively low-cost compared to new data acquisition and typically spans six to eighteen months depending on data volume and complexity.

Stage 2: New Seismic Acquisition and Prospect Generation

If reprocessing of legacy data identifies structural features warranting closer examination, the next step is targeted 3D seismic acquisition over priority areas. Three-dimensional seismic surveys provide the volumetric subsurface imaging needed to map trap geometry, evaluate seal continuity, and identify potential reservoir intervals.

During this phase, exploration geoscientists apply amplitude versus offset (AVO) analysis, which examines how seismic reflection strength changes with the angle of incidence to identify potential hydrocarbon indicators. Rock physics modelling is used to translate seismic observations into predictions about reservoir properties such as porosity and fluid content.

The output of this stage is a prospect inventory with associated resource estimates and geological risk ratings that can be evaluated against competing investment opportunities within a company's global portfolio.

Stage 3: Regulatory and Commercial Transition

Successful prospect generation does not automatically trigger drilling. The transition from MoU-stage technical cooperation to formal exploration commitment requires negotiation of a production sharing agreement defining cost recovery mechanisms, profit sharing ratios, work programme obligations, and relinquishment schedules. Environmental and social baseline studies must be completed to satisfy regulatory requirements before drilling approval is granted.

In deepwater environments such as those associated with the Herodotus Basin, water depths and operational complexity place substantial demands on any drilling programme. Deepwater exploration wells in frontier settings require specialist drillships, complex well designs, and extended planning cycles. Thorough pre-drill subsurface evaluation is not merely procedural; it is the primary mechanism through which exploration companies justify the capital commitment required.

Comparing Egypt's Upstream Appeal Against Regional Peers

Egypt's competitive position as an upstream destination is shaped by several factors that distinguish it from other Mediterranean frontier markets:

| Dimension | Egypt | Cyprus | Israel | Libya |

|---|---|---|---|---|

| Regulatory framework stability | High | High | High | Low |

| Existing LNG export infrastructure | Extensive | Limited | Moderate | Degraded |

| State partner institutional capacity | Strong (EGAS) | Moderate | Moderate | Weak |

| Deepwater frontier exploration upside | High (northwest) | Moderate | Moderate | High but largely untested |

| Recent major IOC activity | Active (TotalEnergies, ENI) | Active | Active | Emerging |

| Maritime boundary definition | Broadly defined | Partially defined | Broadly defined | Contested |

Egypt's most significant competitive advantage from an upstream investment perspective is its LNG export infrastructure. The presence of functioning liquefaction terminals at Idku and Damietta means that any gas discovered in the northwest offshore region has a pre-existing pathway to international markets. This materially shortens the commercial development timeline compared to frontier discoveries in jurisdictions where export infrastructure would need to be built from scratch.

The next major ASX story will hit our subscribers first

Natural Gas in 2026: The Transition Fuel That Won't Stand Still

The broader context for understanding why a company of TotalEnergies' scale is committing to deepwater frontier gas exploration in 2026 requires engaging with the energy transition debate honestly. TotalEnergies has positioned natural gas as a central component of its multi-energy strategy, describing it as a bridge fuel that supports decarbonisation by displacing higher-emission coal and oil in power generation and industrial applications. Furthermore, energy transition demand for cleaner-burning fuels continues to reinforce the strategic rationale for new gas discoveries in well-located basins.

The commercial case for new deepwater gas discoveries is further reinforced by European energy security considerations. Following structural disruptions to Russian gas supply in 2022, European buyers have sought to diversify their LNG import sources. Mediterranean-sourced LNG from Egypt represents a geographically proximate, politically preferable alternative to more distant supply chains. Monitoring natural gas price trends will therefore remain critical as TotalEnergies advances its evaluation work in northwest Egyptian waters.

This demand-side dynamic does not guarantee commercial success for any specific exploration project. However, it does ensure that material gas discoveries in the Western Mediterranean would enter a market with identifiable buyers and established pricing mechanisms, strengthening the investment case for frontier exploration. Analysts tracking developments in this space can find further detail in reporting on TotalEnergies' deepwater targets off the Egyptian coast.

Frequently Asked Questions

What is the TotalEnergies EGAS offshore Egypt exploration MoU?

The TotalEnergies EGAS offshore Egypt exploration MoU is a technical cooperation framework executed on May 13, 2026, establishing a joint programme of preliminary exploration and subsurface evaluation across a substantial offshore area in Egypt's northwest Mediterranean region. It was witnessed by Egyptian Prime Minister Dr. Mostafa Madbouly.

Does the MoU represent a binding exploration commitment?

No. The MoU is a pre-commercial instrument. It enables joint technical studies and data evaluation to proceed but does not constitute a production licence, a production sharing agreement, or a binding drilling obligation.

What is the Herodotus Basin and why does it matter?

The Herodotus Basin is a deepwater sedimentary structure in the Western Mediterranean with geological characteristics that suggest potential for natural gas accumulations. It is comparatively underexplored relative to the Eastern Mediterranean's Levantine Basin, which contains the Zohr, Leviathan, and Tamar fields.

What existing operations does TotalEnergies hold in Egypt?

Prior to this MoU, TotalEnergies held an active offshore concession in Egypt's Neho Block and was conducting drilling activity through the Tarif Deep-1 onshore programme, both in partnership with EGAS.

How does this agreement fit TotalEnergies' broader Mediterranean strategy?

The Egypt MoU is one component of a cluster of Mediterranean exploration commitments executed in May 2026. One day prior, TotalEnergies finalised offshore exploration agreements in Syria involving ConocoPhillips and QatarEnergy, reflecting a portfolio-building strategy that acquires optionality across multiple frontier positions simultaneously.

Key Strategic Takeaways

- First-mover data advantage: The MoU positions TotalEnergies to acquire frontier subsurface knowledge in northwest Egyptian waters before formal licensing rounds create competitive pressure.

- Infrastructure-ready pathway: Any gas discoveries in the northwest offshore area would benefit from Egypt's existing LNG terminals, shortening the commercialisation timeline compared to infrastructure-free frontier plays.

- Sovereign endorsement as a risk signal: Prime Ministerial witnessing of the MoU elevates its political weight and reduces above-ground regulatory risk perceptions for TotalEnergies' investment committees.

- Pre-drill risk management: The MoU structure allows rigorous subsurface evaluation before irreversible capital is committed, which is standard practice for responsible deepwater frontier exploration.

- Portfolio diversification logic: The simultaneous clustering of Mediterranean commitments across Egypt and Syria reflects a deliberate strategy to accumulate exploration optionality across jurisdictions with different risk profiles.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking statements and scenario analyses involve inherent uncertainty and should not be relied upon as predictions of commercial outcomes. Readers should conduct independent research before making any investment decisions related to companies or projects discussed herein.

Want to Spot the Next Major Resource Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements across 30+ commodities, delivering real-time alerts on significant mineral discoveries — explore historic examples of major discovery returns to understand the opportunity, then start your 14-day free trial at Discovery Alert to position yourself ahead of the market.