July 27, 2026

Global commodity traders increasingly recognise the Trafigura and Smackover lithium offtake agreement as a strategic response to unprecedented supply chain pressures in critical minerals markets. As electric vehicle proliferation accelerates beyond traditional forecasting models, the intersection of battery demand and emerging infrastructure creates complex procurement challenges that require sophisticated risk management frameworks. Furthermore, understanding how institutional buyers structure long-term supply agreements reveals fundamental shifts in strategic resource allocation across the battery materials value chain.

Strategic Risk Management in Critical Minerals Markets

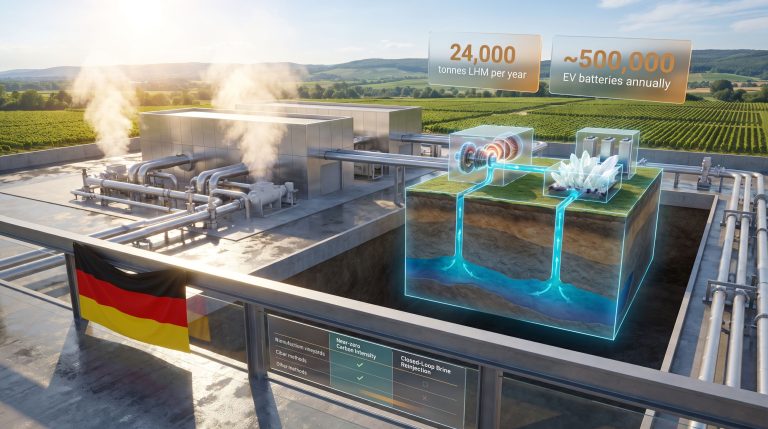

Global commodity traders increasingly view lithium supply chains through geopolitical risk assessment frameworks that prioritise geographic diversification and operational stability. The Trafigura and Smackover lithium offtake agreement exemplifies this strategic approach, with Trafigura committing to purchase 8,000 metric tonnes of battery-grade lithium carbonate annually over ten years from the South West Arkansas (SWA) Project.

Supply chain vulnerability assessment drives these procurement decisions through systematic evaluation of multiple factors. Projects with 38% proven/indicated reserves like the SWA Project provide superior risk profiles compared to exploration-stage developments. Additionally, direct lithium extraction (DLE) deployment reduces operational complexity versus traditional evaporation methods requiring 18-24 month production cycles.

Arkansas's existing brine extraction heritage from oil, gas, and bromine operations creates operational advantages that complement modern lithium brine market insights. Moreover, domestic U.S. projects avoid political risks associated with South American lithium regions, providing greater supply security.

Portfolio diversification strategies require balancing exposure across different extraction methods and geographic regions. The joint venture structure between Standard Lithium (55%) and Equinor ASA (45%) demonstrates risk-sharing mechanisms that institutional investors favour for large-scale resource development.

Market timing considerations make 10-year agreements particularly attractive during commodity price volatility. Long-term contracts provide optimal risk-adjusted returns by establishing floor prices while maintaining upside exposure through escalation clauses tied to inflation indices.

When big ASX news breaks, our subscribers know first

The Economics of Take-or-Pay Structures in Battery Materials

Take-or-pay mechanisms function as sophisticated financial engineering tools that reduce project financing costs while providing demand validation for institutional lenders. The 80,000-tonne commitment in the Trafigura and Smackover lithium offtake agreement represents material supply security for global commodity distribution networks.

Financial engineering benefits emerge through multiple channels. Guaranteed purchase commitments enable higher leverage ratios (typically 60-70% debt financing versus 40-50% for spot-exposed projects). Contract cash flows eliminate commodity hedging requirements, whilst lender comfort reduces demand risk assumptions in project financing models.

Price discovery mechanisms in long-term contracts establish market benchmarks through quarterly or annual pricing review provisions that decouple price negotiations from contract performance requirements. Floor prices protect project economics during commodity downturns while escalation clauses allow market repricing during inflationary periods.

Counterparty risk evaluation requires comprehensive due diligence frameworks assessing project viability through resource confidence levels, operational technology maturity, and regulatory approval status. Trafigura's creditworthiness as a Fortune 500 commodity trader with global trading infrastructure significantly reduces counterparty risk profiles for project developers, as evidenced by their recent lithium procurement agreements.

"Long-term offtake agreements serve as collateral instruments that demonstrate demand validation to institutional lenders, reducing perceived project risk and improving financing terms for projects requiring USD 1-2 billion capital investments."

How Direct Lithium Extraction Transforms North American Resource Development

Direct lithium extraction represents a paradigm shift from land-intensive evaporation cycles to rapid, contained processing that reduces production timelines from 18-24 months to 3-6 months. The SWA Project's DLE deployment leverages years of testing and refinement to achieve commercial-scale viability.

Operational efficiency metrics demonstrate substantial improvements across multiple parameters. DLE achieves recovery rates of 70-90% compared to traditional evaporation's 50-60%, whilst reducing production timelines and water consumption by 50-90%. Land footprint requirements decrease by 80-95%, creating streamlined environmental permitting processes.

Capital expenditure optimisation occurs through reduced infrastructure requirements for processing facilities, pipeline systems, and storage capacity. While DLE requires higher upfront capital for specialised extraction equipment, per-tonne operating costs at scale prove significantly lower than traditional methods.

Environmental impact reduction creates regulatory advantages through decreased water stress and land footprint requirements. The SWA Project's brine reinjection process maintains reservoir pressure while reducing surface water depletion, addressing critical environmental concerns in lithium development.

Technology deployment mechanics involve selective lithium extraction from underground brine using specialised materials and chemical processes. Battery-grade purity (>99.5% lithium carbonate) becomes achievable through DLE without extensive additional processing, streamlining the production pathway.

Regional Competitive Advantages in Arkansas

The Smackover Formation presents distinct competitive advantages through existing industrial infrastructure, regional workforce expertise, and reduced water stress compared to lithium-rich regions in western United States and South America. Arkansas's long history of brine extraction creates foundational capabilities for rapid lithium project development.

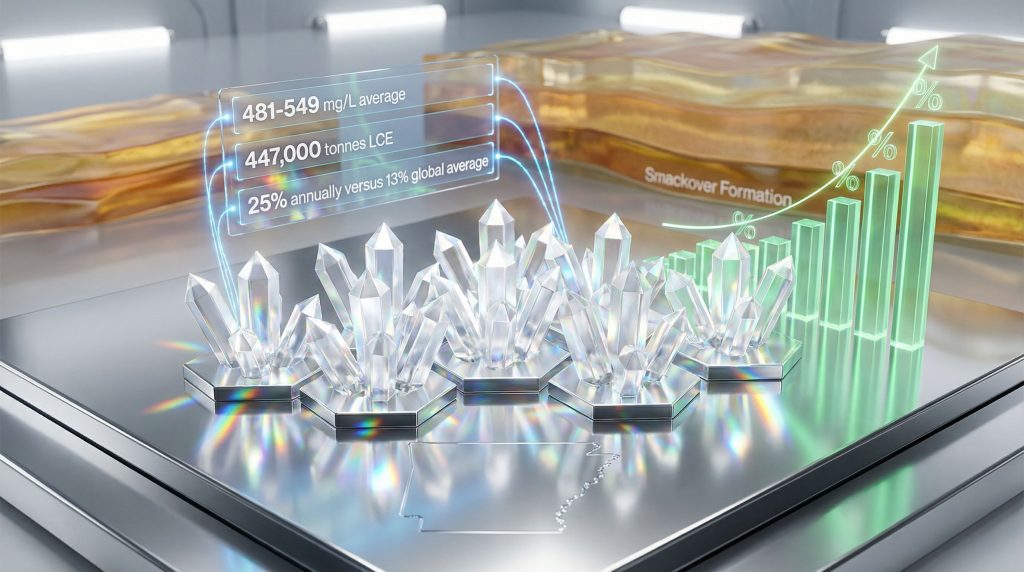

Geological resource quality metrics demonstrate premium-grade potential with initial lithium concentrations of 549 mg/L representing upper-middle range of commercial-grade deposits. Lifecycle average concentrations of 481 mg/L maintain consistent economics over 20-year operational life, supported by 1.17 million tonnes LCE total measured and indicated resources.

The project encompasses 30,000 acres of brine leases with initial focus on 20,800+ acre Reynolds Brine Unit. Infrastructure leverage opportunities reduce capital requirements through existing well networks from oil and gas operations that can be retrofitted for lithium extraction and brine reinjection.

Workforce readiness assessment reveals decades of experience in brine handling and subsurface operations among Arkansas technical workers. Skills in wells, piping, pump systems, and reservoir management transfer directly to lithium extraction operations, reducing hiring and training costs.

Transportation cost advantages emerge from Arkansas's proximity to battery manufacturers in the Southeast U.S., Midwest, and Mexico versus West Coast alternatives. The region's central location provides logistics efficiency for North American supply chain integration, complementing broader mining industry evolution trends.

Market Growth Vector Analysis

Electric vehicle adoption curves drive fundamental demand growth patterns that favour long-term supply positioning. U.S. lithium demand for EV batteries projects 25% annual growth over the next decade, significantly exceeding the 13% global average, creating substantial domestic supply gap opportunities.

Energy storage market expansion represents a secondary growth vector as grid-scale battery deployment accelerates. Large battery systems supporting renewable energy integration require massive lithium supplies, with the U.S. energy storage market projected to grow 29% annually.

Industrial application diversification beyond transportation creates additional demand pressures. Data centre battery backup systems require reliable power supply for AI infrastructure, whilst grid stabilisation batteries manage renewable energy intermittency. Furthermore, industrial equipment batteries power fork lifts, mining equipment, and specialised machinery.

Supply-demand balance projections indicate significant gaps between projected consumption growth and planned production capacity additions. Domestic U.S. lithium production remains minimal compared to import requirements, creating strategic vulnerability in critical mineral supply chains.

Price volatility management through long-term contracts provides both buyers and sellers with planning certainty. The 10-year duration of the Trafigura and Smackover lithium offtake agreement demonstrates institutional commitment to price stability over commodity market cycles, similar to Thacker Pass lithium production strategies.

Strategic Implications for North American Battery Supply Chains

Domestic supply chain resilience building requires systematic reduction of import dependencies through strategic mineral development. The SWA Project's expected 2028 production start aligns with accelerating North American battery manufacturing capacity additions.

Critical mineral security frameworks benefit from projects that combine resource quality, technological maturity, and financing certainty. Proven reserves of 447,000 tonnes LCE representing 38% of measured/indicated resources provide long-term supply visibility for strategic planning.

Manufacturing cluster development opportunities arise from co-location benefits between lithium production and battery manufacturing. Arkansas's central location within North America creates logistics advantages for supply chain optimisation.

Joint venture structure optimisation demonstrates effective risk-sharing mechanisms between operational expertise (Standard Lithium) and financial capacity (Equinor ASA). The 55/45 ownership structure balances operational control with capital contribution requirements.

"The combination of proven technology, quality resources, institutional partnerships, and long-term offtake commitments positions the SWA Project as a reference case for domestic critical mineral development strategies."

The next major ASX story will hit our subscribers first

Financing Structures for Large-Scale Lithium Projects

Project finance innovation in critical minerals leverages offtake agreements as collateral for development capital. The Trafigura commitment provides revenue certainty that enables higher leverage ratios and improved financing terms for the USD 1-2 billion capital requirements typical of commercial lithium operations.

Offtake agreement monetisation occurs through several mechanisms. Cash flow certainty supports debt service calculations, whilst Trafigura's investment-grade credit rating reduces lender risk perception. Volume guarantees eliminate demand-side uncertainty, and price floors protect downside scenarios.

Government support integration through grants and incentives can be incorporated into capital structure design without compromising project independence. Policy frameworks supporting domestic critical mineral development create additional financing options that complement capital raising strategies.

Risk capital allocation models require milestone-based funding release mechanisms that align development progress with capital deployment. The targeted 2026 final investment decision and 2028 commercial production timeline provide clear development milestones for investor evaluation.

Competitive Positioning in U.S. Lithium Markets

Market entry timing analysis reveals advantages for projects achieving commercial production during the 2028-2030 timeframe when domestic demand growth accelerates beyond current supply planning. The SWA Project's production timeline positions it favourably within this demand expansion period.

First-mover advantage assessment considers both market positioning benefits and technology maturity risks. DLE deployment at commercial scale provides operational experience that competitors must replicate, creating sustainable competitive positioning.

Competitive response scenarios from established players require strategic evaluation of capacity expansion options versus new project development. Existing producers may prefer expansion of proven operations rather than greenfield development in new regions.

Value chain integration opportunities extend beyond lithium carbonate production toward downstream processing capabilities. Strategic partnerships with battery manufacturers or chemical processing facilities could enhance project returns.

Market share capture strategies balance volume commitments like the 8,000 tonnes annual Trafigura agreement against pricing flexibility for spot market opportunities. Long-term contracted volumes provide revenue stability whilst maintaining upside exposure, reflecting innovative lithium industry practices.

Investment Themes Driving Capital Allocation

Institutional investor priorities increasingly emphasise ESG mandate alignment through sustainable extraction methods and reduced environmental impact. DLE technology's 50-90% water consumption reduction and 80-95% land footprint reduction address critical environmental criteria.

Portfolio diversification benefits position critical minerals as alternative asset class exposure with commodity characteristics but growth equity returns potential. The 20-year project lifespan exceeds typical mining operations, providing extended cash flow generation.

Strategic acquirer interest patterns reflect vertical integration drivers as battery manufacturers seek upstream supply security. The automotive industry's transition to electrification creates acquisition pressures for quality lithium assets, as demonstrated by recent industry developments.

Geographic diversification imperatives reduce concentration risk in traditional lithium regions experiencing political or regulatory uncertainty. North American projects provide jurisdictional stability that institutional investors increasingly value.

Risk-adjusted return expectations for lithium projects must account for commodity price volatility, operational complexity, and regulatory approval timelines. Projects with contracted offtake, proven technology, and experienced operators typically achieve premium valuations.

Disclaimer: This analysis contains forward-looking projections based on current market conditions and technological assumptions. Lithium markets remain subject to significant volatility, regulatory changes, and technological developments that could materially affect project outcomes. Investors should conduct independent due diligence and consider professional advice before making investment decisions. Resource estimates, production timelines, and financial projections are subject to geological, operational, and market risks that could result in different outcomes than those presented.

Considering Your Next Move in Critical Minerals Investing?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, empowering investors to capitalise on emerging opportunities before broader market recognition. Begin your 14-day free trial today to access real-time insights that could position you ahead of major lithium and critical minerals developments across the Australian market.