June 10, 2026

Why the Architecture of U.S. Sanctions Is Being Tested Like Never Before

For decades, the United States has relied on economic sanctions as one of its most powerful foreign policy instruments. The logic is straightforward: restrict access to revenue, and you restrict a government's ability to fund its ambitions. Against Iran, this framework has been applied with particular intensity, targeting the country's crude oil exports as the primary mechanism of economic coercion. Yet the effectiveness of any sanctions regime ultimately depends on the compliance of the countries consuming the sanctioned goods. When the world's largest oil importer decides to keep buying, the architecture begins to crack.

That tension is now at the centre of a high-stakes diplomatic moment. The prospect of Trump lifting sanctions on Chinese firms buying Iran oil has sent ripples through energy markets, foreign policy circles, and the broader debate over whether secondary sanctions retain meaningful deterrent power when confronted with economies of China's scale.

When big ASX news breaks, our subscribers know first

The Mechanics of Maximum Pressure: How the Sanctions Framework Targets Iranian Oil

The U.S. sanctions strategy against Iran operates on two levels. Primary sanctions prohibit American entities from engaging with Iranian counterparts. Secondary sanctions extend enforcement reach to foreign companies and individuals that conduct business with designated Iranian entities, threatening to cut them off from U.S. financial markets and dollar-denominated transactions.

The critical vulnerability in this structure is the enforcement gap. Washington can designate a foreign firm, but actually disrupting that firm's operations requires the cooperation of its banking partners, insurers, and trading counterparts. When a Chinese independent refinery purchases Iranian crude, the transactional infrastructure often bypasses the dollar system entirely, using yuan-denominated settlements, shadow fleet tankers, and unofficial intermediaries that operate outside conventional financial channels.

This is why Chinese independent refineries, commonly called teapot refineries due to their relatively smaller but highly flexible processing capacity compared to major state-owned facilities, became so central to the Iranian oil trade. These refineries, concentrated in provinces like Shandong, are price-sensitive buyers that have demonstrated a consistent willingness to purchase discounted Iranian barrels at rates meaningfully below Brent and WTI crude benchmarks.

Iranian crude has historically traded at discounts of $5 to $15 per barrel below comparable Middle Eastern grades, offering teapot refiners a structural cost advantage that makes the compliance risk commercially tolerable in the absence of aggressive enforcement.

Hengli Petrochemical: The High-Profile Designation That Changed the Equation

The sanctioning of Hengli Petrochemical, the Dalian-based refinery and petrochemical complex, represented a strategic escalation in U.S. enforcement posture. Rather than continuing to focus solely on Iranian exporters, the U.S. Treasury shifted its targeting downstream toward the buyers themselves. This was a structurally significant change because it threatened a firm with genuine global commercial ties, including relationships with Western technology providers and financial institutions.

Hengli is not a small independent operator. It operates one of China's most sophisticated refining and petrochemical complexes, with a crude processing capacity of approximately 20 million tonnes per year. Designating a facility of this scale sent an unmistakable signal that the U.S. was prepared to escalate enforcement beyond symbolic targets.

The potential reversal of this designation, if it proceeds, would carry equally significant implications. It would signal that high-profile designations can be unwound through diplomatic negotiation, fundamentally altering the deterrent calculus for any future enforcement action.

Trump's Signal and the Diplomatic Context Behind It

The remarks made by President Trump regarding a forthcoming decision on sanctions for Chinese oil buyers were delivered during his return from China, where discussions with President Xi Jinping covered a broad range of bilateral and geopolitical issues. The timing matters as much as the content. For context on the broader trade dynamics at play, the ongoing U.S.–China trade war has significantly shaped the diplomatic environment in which these discussions are taking place.

Presidential statements on sanctions carry market-moving weight even before formal policy action because they compress the perceived probability distribution of future outcomes. Traders and risk managers do not wait for official announcements; they reprice exposure the moment executive intent becomes visible. Furthermore, the Trump tariff impact on bilateral negotiations has added additional pressure to both sides to seek areas of mutual accommodation.

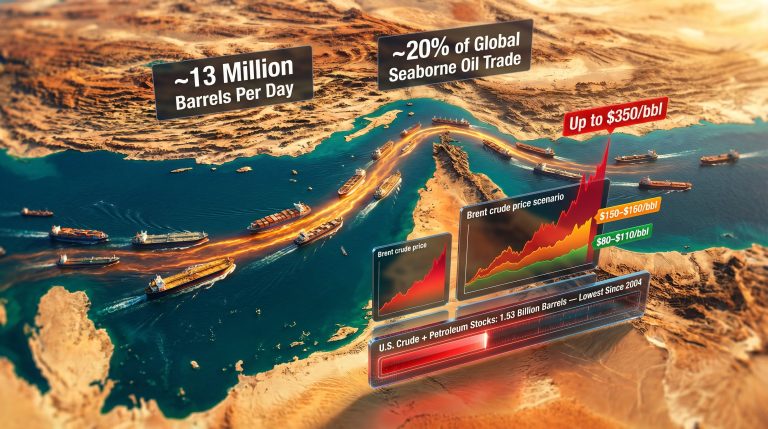

Xi Jinping's reported support for reopening the Strait of Hormuz added another dimension to the conversation. The Strait has remained closed since U.S.–Iran hostilities commenced on February 28, 2026, a period of approximately 11 weeks as of mid-May 2026. The closure has disrupted the movement of roughly 20% of global petroleum supplies, affecting importers across Asia, Europe, and beyond.

| Strait of Hormuz: Key Facts | Detail |

|---|---|

| Share of global oil transit | ~20% of world petroleum supply |

| Closure commencement date | February 28, 2026 |

| Approximate closure duration (as of May 2026) | ~11 weeks |

| Primary affected importers | China, India, Japan, South Korea, EU nations |

| Transit chokepoint significance | World's most critical oil shipping lane |

The Strait's closure and the sanctions regime on Iranian oil are separate but interlocking constraints on global supply. Lifting sanctions on Chinese buyers without reopening the Strait would increase the commercial willingness to purchase Iranian crude but would not resolve the physical logistics of getting it to market. Conversely, reopening the Strait without addressing sanctions would leave Chinese refiners exposed to legal risk even as the shipping lane becomes accessible.

Who Benefits, Who Bears the Cost: Mapping the Stakeholder Landscape

Iran: Revenue Restoration With Structural Limits

Iran's government budget is heavily reliant on hydrocarbon revenues. Estimates from the International Monetary Fund and independent energy analysts have consistently placed oil export receipts at 40% to 50% of Iranian government revenues in non-sanctions periods. The reimposition of maximum pressure has severely compressed that revenue stream.

A rollback of sanctions on Chinese buyers would increase Iranian export volumes relatively quickly. Iran has maintained production capacity even under sanctions, storing crude on tankers and selling at discount. The immediate uplift from confirmed sanctions relief could add several hundred thousand barrels per day of incremental supply to the market within 60 to 90 days of any formal policy change.

China: Dual Strategic Benefit

For Beijing, the potential removal of sanctions on its refining sector delivers value on two fronts simultaneously. It reduces the cost of energy imports by restoring access to discounted Iranian barrels, and it removes a source of friction in the broader U.S.–China commercial relationship. Chinese state-owned enterprises have generally maintained more cautious postures toward sanctioned Iranian oil than independent teapot refiners, meaning the relief would disproportionately benefit the independent refining sector and its regional economies.

The United States: Credibility Versus Pragmatism

The domestic political calculus for the Trump administration involves managing hawkish Iran policy constituencies against the broader strategic objective of reaching a negotiated accommodation with Beijing on trade. A sanctions rollback framed as a diplomatic concession extracted from China in exchange for Strait of Hormuz cooperation could be presented as a foreign policy win rather than a retreat.

The longer-term risk, however, is credibility erosion. Secondary sanctions derive their power from the belief that designations are durable and enforcement is consistent. A pattern of using sanctions designations as short-term negotiating chips — imposing them and then offering to remove them within compressed diplomatic timelines — reduces their deterrent value for future applications.

Global Oil Markets: Pricing Uncertainty Before Confirmation

Market participants have already begun pricing in the possibility of increased Iranian supply even before any formal policy change. This dynamic, where anticipated future supply suppresses current risk premiums, is a well-documented feature of commodity markets responding to geopolitical signals.

The directional impact on Brent crude and WTI would be bearish if sanctions relief is confirmed, as it would increase available supply into a market already navigating the complexities of OPEC's market influence and production management. The magnitude of the price impact depends on how quickly Iranian volumes ramp up and whether Strait of Hormuz reopening occurs concurrently.

The Broader Sanctions Architecture: Structural Limits in a Multipolar World

The challenges facing U.S. secondary sanctions enforcement against Chinese energy firms are not isolated to the Iranian case. Similar dynamics have played out in the context of Russian oil exports following the 2022 invasion of Ukraine, where price cap mechanisms faced persistent circumvention through shadow fleets, third-country intermediaries, and non-dollar settlement systems. In addition, the rise of geopolitical trade tensions more broadly has accelerated the development of alternative financial and logistical infrastructure among sanctioned states.

What these cases collectively reveal is that secondary sanctions are most effective when:

- The targeted country lacks alternative financing and logistics infrastructure

- Major consuming nations cooperate with enforcement or face equivalent economic penalties

- The sanctioned commodity lacks sufficient alternative supply sources to replace lost volumes

Against China, none of these conditions are fully met. Beijing has developed alternative financial infrastructure, maintains strategic relationships with Gulf producers and Iranian counterparts, and operates a refining sector large enough to absorb enforcement costs when the commercial incentives are sufficiently attractive.

The next major ASX story will hit our subscribers first

Asian Energy Markets: The Ripple Effects Beyond China

India's Competitive Position

India has its own history of purchasing Iranian crude, interrupted by the reimposition of U.S. sanctions. Indian refiners, particularly state-owned majors like Indian Oil Corporation and Bharat Petroleum, have refined Iranian crude in the past and retain the technical capability to process it. A sanctions rollback that normalises Chinese purchases could create competitive pressure on India to seek similar accommodations, or risk being outcompeted for discounted Iranian barrels.

India faces a genuine geopolitical balancing act. Its strategic partnership with the United States creates incentives for compliance with U.S. sanctions frameworks. Its energy import dependency, with crude imports accounting for roughly 85% of domestic consumption, creates powerful commercial incentives to access the cheapest available supply.

Japan and South Korea: Strait Exposure and Supply Security

Northeast Asian importers have been among the most acutely affected by the Strait of Hormuz closure. Japan imports approximately 90% of its crude oil from Middle Eastern producers, and South Korea's exposure is similarly concentrated. Both nations have been forced to draw down strategic petroleum reserves and pursue alternative supply arrangements during the closure period.

For Tokyo and Seoul, the prospect of Strait reopening combined with increased Iranian supply availability represents a meaningful improvement in their energy security outlook, even if the formal sanctions architecture affects them less directly than it does Chinese buyers.

OPEC+ and Gulf State Responses

Saudi Arabia and the UAE face a structurally uncomfortable scenario if Iranian supply increases significantly. Every additional barrel of Iranian crude reaching market is effectively competing with Gulf producer volumes, threatening to push prices below the fiscal breakeven levels that Gulf governments require to balance their budgets.

Saudi Arabia's fiscal breakeven oil price has been estimated at approximately $80 per barrel in recent years, a level that OPEC+ production management has struggled to consistently maintain given rising non-OPEC supply and demand uncertainty. A sustained increase in Iranian export volumes would intensify that pressure considerably.

Three Scenarios for What Comes Next

Scenario 1: Full Rollback

All designated Chinese refiners have sanctions lifted. Iranian export volumes increase materially within 60 to 90 days. Brent crude faces downward pressure as additional supply enters the market. The maximum pressure framework loses significant credibility as a deterrent tool, but the Trump administration gains diplomatic currency with Beijing. This scenario is most likely if U.S.–China trade negotiations reach a comprehensive near-term agreement. CNN reports that the administration's signals have already drawn considerable attention from energy policy analysts and market watchers.

Scenario 2: Selective Exemptions

A middle-ground outcome modelled on the Obama-era waiver system, where specific firms receive time-limited exemptions conditional on reducing purchase volumes or meeting other diplomatic criteria. This approach preserves the formal architecture of the sanctions regime while offering tactical concessions. It has historical precedent and allows the administration to maintain policy continuity while demonstrating flexibility.

Scenario 3: No Action

Trump's remarks function as diplomatic signalling without formal policy follow-through. Markets self-correct as the probability of relief diminishes. The maximum pressure framework remains intact, but its credibility has been partially eroded by the public suggestion that sanctions could be traded away. Historically, stated intentions without rapid execution tend to produce short-term price movements that reverse within two to four weeks as traders reprice the probability distribution back toward the status quo. As Fortune notes, this pattern of signalling without follow-through carries its own strategic costs for U.S. foreign policy credibility.

Frequently Asked Questions

What sanctions did the U.S. impose on Chinese firms buying Iranian oil?

The U.S. Treasury designated several Chinese independent oil refineries under sanctions frameworks designed to restrict entities that purchase Iranian crude. These designations are intended to cut off affected firms from U.S. financial infrastructure and dollar-denominated transactions, creating significant operational complications for companies with any exposure to Western financial systems.

Is Trump's announcement a confirmed policy change?

As of the reporting date of May 16, 2026, this remains a stated intention under active consideration, not a confirmed policy change. No formal executive action or Treasury designation reversal had been announced at the time of publication. Investors and market participants should treat this as a directional signal rather than confirmed policy.

How does the Strait of Hormuz closure compound the sanctions issue?

The Strait's closure operates as an independent physical supply constraint separate from the legal sanctions framework. Together they represent two distinct barriers to Iranian crude reaching major consuming markets. Resolving one without the other provides only partial relief to the global supply picture.

What does this mean for long-term U.S. sanctions credibility?

The transactional use of sanctions designations as negotiating instruments rather than durable policy commitments introduces uncertainty into the deterrence calculus. If foreign entities believe that designations can be reversed through diplomatic engagement, the compliance incentive weakens across all future sanctions applications, not only those targeting Trump lifting sanctions on Chinese firms buying Iran oil.

Disclaimer: This article is intended for informational and analytical purposes only. It does not constitute financial, investment, or legal advice. Forecasts, scenario analyses, and market projections involve inherent uncertainty and should not be relied upon as the basis for investment decisions. Readers should conduct independent research and consult qualified professionals before making any financial or policy-related decisions.

Want to Stay Ahead of the Next Major Resource Discovery Driving Global Markets?

Geopolitical shifts reshaping global energy supply chains can create significant opportunities in ASX-listed resource stocks — and Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment a significant mineral discovery hits the ASX, turning complex data across 30+ commodities into clear, actionable insights for investors at every level. Explore how historic discoveries have generated exceptional returns and begin your 14-day free trial today to position yourself ahead of the market.