August 2, 2026

How U.S. Metal Trade Policy Became Industrial Strategy: Understanding the 2026 Section 232 Proclamation

Few policy instruments reshape global supply chains as quietly yet as decisively as tariff architecture. When governments recalibrate how duties are calculated, which products fall within scope, and what compliance pathways exist for foreign manufacturers, the downstream effects ripple through procurement departments, capital investment committees, and trade finance desks worldwide. The Trump steel aluminum and copper tariffs proclamation signed on April 2, 2026, represents precisely this kind of structural recalibration, one that goes well beyond a simple rate adjustment to reframe how the United States deploys trade law as industrial policy.

When big ASX news breaks, our subscribers know first

The Section 232 Framework: National Security as Trade Law Architecture

How Presidential Authority Over Metal Imports Is Legally Grounded

Section 232 of the Trade Expansion Act of 1962 grants the executive branch the authority to impose import restrictions when a product or commodity is determined to threaten national security. Unlike conventional trade remedies such as anti-dumping or countervailing duty investigations, Section 232 actions bypass the standard multi-agency adjudication process and vest significant discretionary power in the presidency. This makes the legal instrument unusually agile as a policy tool, capable of being amended, expanded, or restructured through proclamation rather than legislation.

The original application of Section 232 to steel and aluminum in 2018 established the foundational logic: that a hollowed-out domestic metals industry creates a strategic vulnerability, particularly during military mobilisation or supply chain disruptions of the kind witnessed during the COVID-19 pandemic. Each subsequent amendment has built on that premise, gradually expanding both the product scope and the sophistication of the rate structure.

Why Steel, Aluminum, and Copper Are Treated as Strategic Commodities

The classification of these three metals as national security assets is not arbitrary. Each plays a distinct and non-substitutable role in defence and critical infrastructure. The steel and aluminum tariffs impact on international manufacturing has, furthermore, reinforced why policymakers treat these metals as strategic instruments rather than ordinary trade policy tools:

- Steel is foundational to shipbuilding, armoured vehicle production, military construction, and heavy weapons systems.

- Aluminum is critical for aerospace, naval vessels, and lightweight military platforms where weight-to-strength ratios are operationally significant.

- Copper has historically been treated as an industrial bellwether, but its expanding role in defence electronics, electric vehicle drivetrains, grid-scale battery storage systems, and military communications infrastructure has elevated its strategic profile considerably.

The inclusion of copper in the April 2026 proclamation is particularly notable. Unlike steel and aluminum, copper had not been a primary focus of Section 232 enforcement. Its formal integration into the framework reflects a broader recognition that the energy transition and defence modernisation are converging around a shared set of base metals, copper chief among them.

The April 2026 Proclamation: A Structural Redesign, Not a Routine Amendment

From Flat Rates to Tiered Incentive Architecture

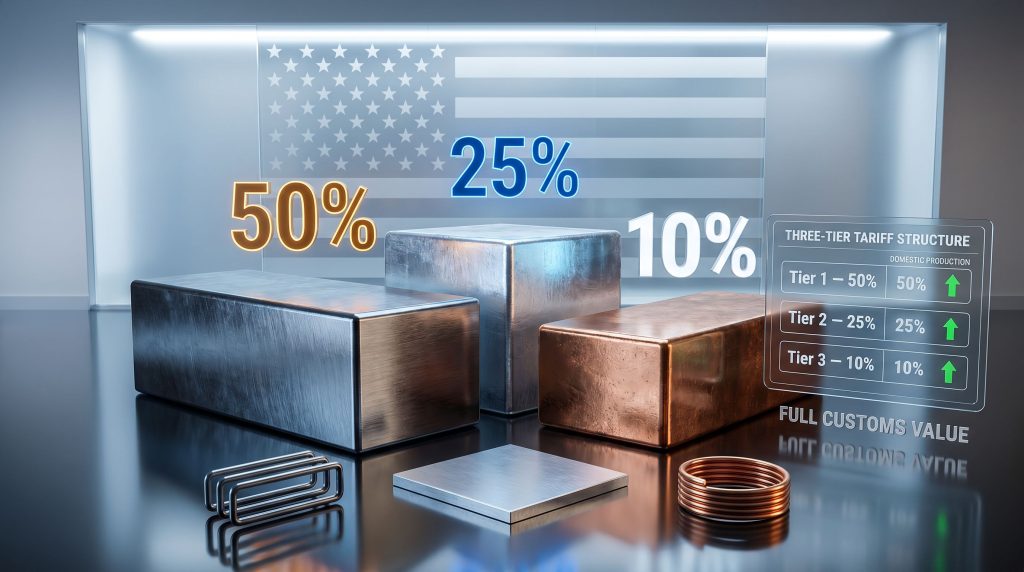

The most significant aspect of the April 2, 2026 proclamation is not any individual rate change but the shift to a fundamentally different structural logic. Earlier Section 232 actions applied broadly uniform rates across wide product categories. The 2026 proclamation introduces a three-tier framework that differentiates between products based on both type and domestic content composition.

| Tariff Tier | Rate | Products Covered |

|---|---|---|

| Tier 1 – Primary Metals and Close Derivatives | 50% | Core steel, aluminum, and copper products |

| Tier 2 – Broader Derivative Articles | 25% | Agricultural machinery, HVAC equipment, steel racks, aluminum lithographic plates |

| Tier 3 – U.S. Content Qualifying Products | 10% | Equipment incorporating at least 85% U.S. melted/poured or smelted/cast metal by weight |

This tiered architecture introduces an incentive logic absent from earlier iterations. Rather than simply taxing imports, the framework actively rewards supply chains that incorporate U.S.-origin metals, creating a pathway for foreign manufacturers to reduce their tariff exposure by sourcing American steel and aluminum for their production processes.

The Full Customs Value Shift: A Quietly Significant Change

One of the least-discussed but most consequential elements of the proclamation is the shift from metal-content-only tariff calculation to full customs value application. Under previous rules, many derivative products were taxed only on the proportion of their value attributable to the embedded steel or aluminum. Under the amended framework, the entire declared customs value of the imported product becomes the tariff base.

For complex manufactured goods, this distinction is financially material. A piece of agricultural equipment with a declared customs value of $200,000 but embedded steel content worth $40,000 previously attracted duties on $40,000. Under the revised framework, the full $200,000 becomes the tariff base, multiplying the effective duty burden by a factor of five in that scenario.

Products Added and Adjusted Within the Tariff Scope

The proclamation expanded and refined product coverage in several directions simultaneously. According to the White House fact sheet, the amendments represent a deliberate recalibration of derivative product classifications:

Newly added at 25%:

- Steel racks (warehouse and logistics infrastructure applications)

- Aluminum lithographic plates (printing and publishing supply chains)

Added at 15% for trade deal country imports:

- Mobile industrial equipment including bulldozers and forklifts

Reduced from 25% to 15%:

- Certain categories of agricultural machinery

- Residential heating, air conditioning, and ventilation equipment

The partial relief extended to agricultural machinery and HVAC equipment reflects political sensitivity around input costs for the farming sector and residential construction markets, both of which carry significant domestic political weight.

Key Enforcement Dates and the Investment Window Logic

Timeline of the Proclamation's Phased Implementation

Understanding the sequencing of the proclamation's enforcement is essential for importers and procurement planners:

| Date | Milestone |

|---|---|

| April 2, 2026 | Proclamation signed by President Trump |

| April 6, 2026 | Core provisions effective for goods entered or withdrawn from bonded warehouses |

| June 8, 2026 | Secondary tranche of derivative product adjustments takes effect (12:01 a.m. EST) |

| December 31, 2027 | Current rate structure expires |

Why the Sunset Clause Is a Policy Tool, Not a Limitation

The December 31, 2027 expiry date has been characterised by the White House as a deliberate design feature. The stated rationale is that a defined policy window generates urgency in domestic capital allocation decisions. Manufacturers evaluating whether to invest in domestic melting, casting, or fabrication capacity face a clearer decision framework when the tariff differential has a known duration.

This approach mirrors the logic seen in investment tax credits with expiry dates, where time-bounded incentives consistently generate faster capital commitment than open-ended policies. The sunset structure also creates leverage for future renegotiation, as trading partners seeking permanent rate relief must engage with U.S. trade policy on terms shaped by the existing framework.

The 85% Domestic Content Compliance Pathway

How Foreign Manufacturers Can Qualify for the 10% Preferential Rate

The most architecturally innovative element of the proclamation is the domestic content compliance pathway. Foreign manufacturers whose capital equipment incorporates at least 85% U.S.-origin steel or aluminum by weight, verified as melted and poured, or smelted and cast within the United States, may qualify for the preferential 10% tariff tier.

This provision creates a direct financial incentive for global supply chains to integrate American metal inputs, effectively using tariff differentials as a mechanism to build demand for domestic steel and aluminum producers. The verification requirement (melted and poured, or smelted and cast) is deliberately specific, designed to prevent paper compliance through minimal processing of imported metal within U.S. borders.

The 85% threshold is set high enough to require genuine supply chain restructuring, not superficial sourcing adjustments. This is the mechanism through which the proclamation functions as industrial policy rather than simple trade restriction.

Compliance Implications for Global Manufacturers

For multinational capital equipment manufacturers, the compliance pathway introduces a complex calculation. The 15 percentage point tariff differential between the 10% qualifying rate and the 25% standard derivative rate must be weighed against the cost of sourcing U.S. metals at potentially higher input prices than globally available alternatives. In industries with thin operating margins, this differential can be decisive.

Copper's Elevation to Strategic Trade Policy Status

What the Section 232 Inclusion Means for Copper Markets

Copper's formal integration into the Section 232 framework marks a meaningful evolution in U.S. critical materials policy. Historically, copper was treated as an important industrial input but not a national security concern. The convergence of several structural trends has, however, changed that assessment. Furthermore, the broader U.S. copper tariff impacts are already being felt across procurement and investment decisions in energy-intensive industries.

- The average electric vehicle contains approximately four times more copper than a conventional internal combustion engine vehicle, with estimates ranging from 60 to 83 kilograms per EV depending on the platform.

- Grid-scale electricity storage and renewable energy infrastructure require substantially higher copper intensities per megawatt of capacity than legacy fossil fuel systems.

- Modern defence systems, from radar to communications to electronic warfare platforms, have become increasingly copper-intensive as digital systems replace mechanical components.

The downstream implications for electrical manufacturers, EV supply chains, and defence contractors are significant. Copper tariffs add to input cost pressures already present from broader supply chain regionalisation trends, and they interact with existing critical minerals policy frameworks in ways that are still being worked through by affected industries.

The next major ASX story will hit our subscribers first

Industry Exposure Across the Amended Tariff Regime

Sectors Facing the Highest Effective Tariff Impact

The structural shift to full customs value calculation, combined with expanded product coverage, creates differentiated exposure across manufacturing sectors. In addition, the global commodity tariff effects of policies like this one extend well beyond U.S. borders, influencing sourcing decisions in Asia, Europe, and South America alike.

Heavy equipment and industrial machinery face the broadest exposure, given their high customs values relative to metal content proportions. The full customs value shift amplifies effective tariff incidence significantly for this sector.

Warehousing and logistics operators importing steel racking systems from overseas suppliers now face 25% duties on products previously outside the tariff scope, a change with direct implications for distribution centre build-out costs.

Printing and publishing supply chains dependent on imported aluminum lithographic plates similarly encounter new cost pressures, with no domestic content pathway readily applicable to consumable industrial inputs of this type.

Agricultural equipment manufacturers receive partial relief through the rate reduction to 15% but continue to face structural cost increases relative to the pre-Section 232 baseline, particularly given the full customs value calculation methodology.

HVAC and building systems suppliers benefit from the same 15% reduced rate but remain subject to a materially higher tariff burden than was present before Section 232 derivative expansion.

How Trade Deal Countries Are Treated Differently

The 15% Preferential Rate for Qualifying Nations

The proclamation introduces differentiated treatment for imports from countries that qualify as trade deal partners under U.S. law. Mobile industrial equipment, including bulldozers and forklifts, is subject to a 15% tariff when sourced from these qualifying nations, compared to the standard rate that would otherwise apply.

This differentiation preserves and reinforces the strategic value of bilateral and multilateral trade agreements as tools of tariff management for both the United States and its trading partners. Nations without formal trade agreements with the U.S. face a structurally higher cost environment for their industrial equipment exports, creating a tangible incentive to pursue or maintain trade deal relationships.

Economic Tensions Embedded in the Policy Design

The Import Substitution and Cost Inflation Paradox

The central economic tension of the proclamation is the tradeoff between its stated goal of rebuilding domestic industrial capacity and the near-term cost pressures it imposes on downstream manufacturing. This dynamic is well-documented in trade economics literature and is not unique to Section 232 actions.

Domestic steel, aluminum, and copper producers stand to benefit from enhanced price protection and increased demand from manufacturers seeking to qualify for the 10% domestic content tier. However, industries that cannot practically restructure their supply chains within the 2027 sunset window face genuine margin compression, particularly in low-differentiation manufacturing segments where cost pass-through to end customers is constrained by competitive dynamics.

Historical precedent from the 2018 Section 232 actions offers some guidance. Research from the Economic Policy Institute and independent economists found mixed results, with domestic metal producers experiencing revenue gains while downstream manufacturers in sectors like automotive, appliances, and construction faced measurable cost increases. The 2026 proclamation's more sophisticated architecture, including the domestic content incentive tier, attempts to mitigate some of these downstream costs, though its effectiveness will depend on the pace at which supply chains can practically restructure.

Retaliatory Risk and Diplomatic Trade-Offs

Any significant expansion of Section 232 scope carries retaliatory risk. The 2018 steel and aluminum tariffs prompted counter-measures from the European Union, Canada, and China targeting U.S. agricultural and manufactured goods. The extension of tariff coverage to copper derivatives and the expansion to new product categories in 2026 creates fresh surface area for trading partners to identify retaliatory targets.

The differentiated treatment of trade deal countries through the 15% preferential pathway for mobile industrial equipment partially mitigates this risk for allied economies, preserving preferential access as a diplomatic lever while maintaining the core protectionist architecture of the framework.

FAQ: Trump Steel Aluminum and Copper Tariffs Proclamation

What is the Trump steel aluminum and copper tariffs proclamation?

Signed on April 2, 2026, the proclamation amends the existing Section 232 national security tariff regime covering steel, aluminum, and copper imports. It introduces a tiered rate structure of 10%, 25%, and 50%, shifts tariff calculation to full customs value, expands product coverage, and creates a domestic content compliance pathway for manufacturers seeking preferential treatment.

When did the amended tariff provisions take effect?

Core provisions became effective on April 6, 2026. A secondary tranche covering derivative product adjustments took effect on June 8, 2026 for goods imported or withdrawn from bonded warehouses after 12:01 a.m. EST on that date.

What is the 85% domestic content rule?

Imported capital equipment that incorporates at least 85% U.S.-melted and poured or smelted and cast steel or aluminum by weight qualifies for a reduced 10% tariff rate, creating a direct incentive for global manufacturers to integrate U.S.-origin metals into their production processes.

Which new products entered the tariff scope?

Steel racks and aluminum lithographic plates were added to the 25% tariff tier. Mobile industrial equipment, including bulldozers and forklifts, became subject to a 15% tariff when imported from qualifying trade deal countries.

How long does the current tariff structure remain in force?

The current rate architecture is set to remain effective until December 31, 2027, a sunset period the White House framed as designed to concentrate near-term domestic industrial investment decisions.

Why was copper added to the Section 232 framework?

Copper's expanding strategic role in defence electronics, EV manufacturing, and electrical grid modernisation led to its inclusion within the Section 232 national security framework, alongside steel and aluminum which have been covered since 2018. Consequently, the copper tariffs and trade implications are now drawing significant attention from both investors and supply chain managers globally.

Beyond Tariffs: Reading the Proclamation as Long-Term Industrial Architecture

What the Rate Structure Signals About U.S. Industrial Policy Direction

The April 2026 proclamation is most accurately understood not as a trade restriction but as an industrial policy instrument using tariff architecture as its primary mechanism. The three-tier rate structure, the domestic content compliance pathway, the full customs value calculation shift, and the defined investment window collectively constitute a framework designed to alter the economics of manufacturing location decisions over a multi-year horizon.

For importers, manufacturers, and trade policy analysts, the key structural takeaways are:

- Tariffs now apply to full customs value, not embedded metal content, materially increasing effective duty burdens on complex manufactured goods.

- The 10% / 25% / 50% tiered architecture differentiates by product type and domestic content, introducing supply chain restructuring incentives not present in earlier Section 232 actions.

- Copper has been formally elevated to strategic trade policy status, with downstream implications for EV, defence, and electrical infrastructure supply chains.

- The December 31, 2027 sunset creates a defined window within which sourcing decisions, investment commitments, and compliance restructuring carry maximum policy urgency.

- The 85% domestic content threshold is designed to require genuine supply chain integration, not superficial compliance adjustments.

- Trade deal country status continues to carry meaningful tariff preference value for mobile industrial equipment imports.

The proclamation's architecture reflects a deliberate attempt to use tariff policy to do what subsidy programmes and domestic content mandates have historically struggled to achieve at scale: make it economically rational for global manufacturers to build American metals into their supply chains. The broader context of the Trump critical minerals strategy makes clear that this proclamation is one component of a much larger industrial policy agenda. Rather than requiring compliance, the arithmetic of tariff avoidance makes U.S. metal integration the most cost-effective choice available.

This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. Tariff policy is subject to change through executive action, litigation, or legislative intervention. Readers with specific trade compliance obligations should consult qualified legal and customs advisory professionals.

Want to Know Which ASX Miners Stand to Gain From the Shifting Metals Landscape?

As copper, steel, and aluminium reshape global industrial strategy, the ASX exploration and mining sector is responding in real time — and Discovery Alert's proprietary Discovery IQ model scans every ASX announcement the moment it drops, delivering actionable alerts on significant mineral discoveries before the broader market has a chance to react. Explore historic discovery returns on Discovery Alert's discoveries page and start your 14-day free trial today to position yourself ahead of the next major find.