May 12, 2026

Critical metals markets have historically demonstrated their potential for extreme price volatility during periods of geopolitical uncertainty and supply chain disruption. These raw materials, essential for both civilian technology and military applications, often experience demand surges that far exceed available production capacity, creating investment opportunities that can reshape entire sectors within commodity markets. Furthermore, the growing focus on critical minerals energy security has intensified global demand for strategic materials like tungsten, with wolframpreise in südkorea reflecting this broader transformation.

The strategic positioning of tungsten within global defense infrastructure has intensified significantly since early 2025, as military procurement programs worldwide seek to secure reliable access to materials that cannot be easily substituted in high-performance applications. This market transformation extends beyond simple supply and demand mechanics, involving complex geopolitical considerations that influence pricing structures across multiple jurisdictions.

Marktdynamik hinter rekordhohen Wolframpreisen in der Region

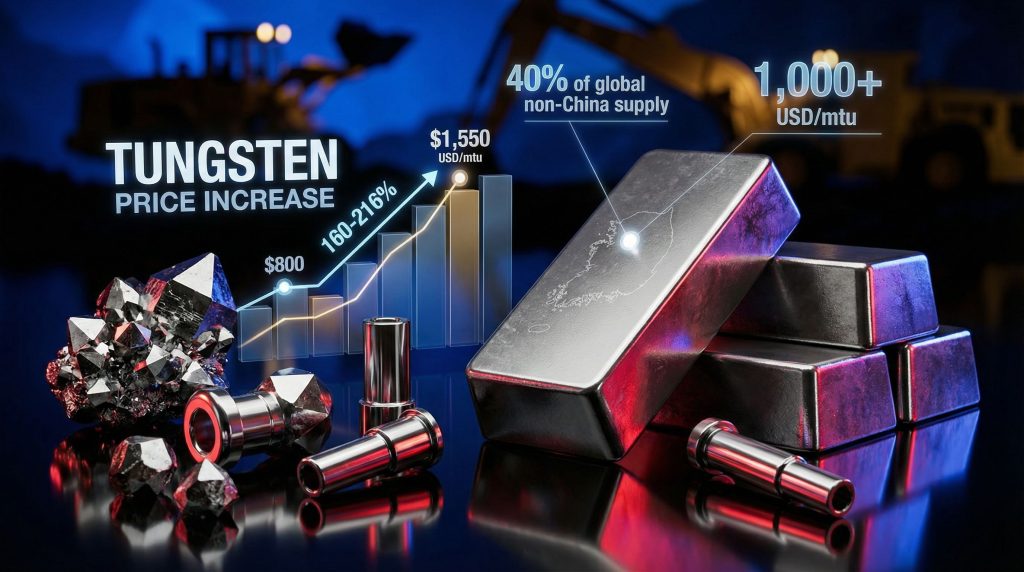

Tungsten concentrate prices have experienced unprecedented acceleration throughout 2025 and into 2026, with market participants reporting values reaching approximately 220,000 USD per tonne by March 2026. This price level represents a fundamental shift in market dynamics that extends far beyond typical commodity cycle patterns. Moreover, these developments align with broader critical minerals strategy 2025 initiatives focused on securing supply chain resilience.

Strukturelle Preistreiber und regionale Unterschiede

The current tungsten price environment reflects several converging factors that have created sustained upward pressure on global markets. Military procurement acceleration has emerged as a primary driver, with ongoing conflicts in the Middle East and Ukraine spurring increased defense spending across NATO member countries and allied nations.

Key price development factors include:

• Geopolitical supply constraints limiting access to traditional sources

• Industrial demand growth in aerospace and defence manufacturing

• Currency fluctuations affecting international trade flows

• Energy costs impacting mining operations globally

Regional pricing variations have become more pronounced, with Asian markets experiencing the most dramatic increases. South Korean tungsten concentrate pricing has emerged as a benchmark for non-Chinese supply sources, reflecting the strategic importance of diversified sourcing options for Western manufacturing sectors. Consequently, wolframpreise in südkorea have become increasingly critical for global market assessment.

The differential between production costs and market prices has created extraordinary margin opportunities for producers with operational assets. Industry analysis suggests production costs ranging from 200-300 USD per metric tonne unit (MTU) compared to current market prices exceeding 1,000 USD per MTU in spot transactions.

Geopolitische Einflüsse auf die Preisbildung

China's dominant position in global tungsten supply chains has created vulnerabilities that governments and corporations are actively addressing through strategic diversification initiatives. The implementation of export restrictions and quality controls has further constrained available supply for international markets.

US legislative measures, including the planned executive order on critical minerals beginning in 2027, have accelerated the search for alternative supply sources. This regulatory environment has elevated the strategic value of South Korean production capacity, positioning the region as a critical component in Western supply chain security frameworks.

Government policies across major economies are increasingly focused on securing access to critical materials that support both civilian technology advancement and military readiness, creating sustained demand pressure that transcends typical market cycles.

When big ASX news breaks, our subscribers know first

Sangdong-Mine als Katalysator für globale Versorgungsströme

The Sangdong tungsten mine, operated by Almonty Industries, represents the largest non-Chinese tungsten development project currently advancing toward production. Located in South Korea's strategic mineral corridor, this operation is positioned to supply approximately 40% of global non-Chinese tungsten concentrate demand once at full capacity.

Produktionskapazitäten und Marktintegration

Sangdong's development timeline aligns with growing market demand for supply chain diversification, with first production targeted for late 2026. The mine's proximity to existing infrastructure and processing facilities provides operational advantages that reduce typical development risks associated with greenfield mining projects.

Technical specifications for the operation include:

• Annual processing capacity: 1.2 million tonnes of ore

• Target concentrate production: 3,000-4,000 tonnes annually

• Resource grade: Average 0.54% WO3 content

• Mine life: Initially planned for 27 years based on current reserves

The economic structure underlying Sangdong's development reflects current market conditions, with off-take agreements reportedly structured around minimum pricing of 19 USD per pound for tungsten concentrate. This pricing foundation provides cash flow stability while allowing participation in potential upside from continued price appreciation.

| Production Phase | Annual Output (tonnes) | Market Share (Non-China) | Revenue Projection (USD millions) |

|---|---|---|---|

| Phase 1 (2026-2028) | 3,000 | 25% | 180-220 |

| Phase 2 (2029-2031) | 4,000 | 33% | 240-290 |

| Full Production (2032+) | 4,500 | 40% | 270-325 |

Technische Verarbeitung und Qualitätsstandards

Tungsten concentrate quality specifications have become increasingly important as end-users seek consistent chemical composition and physical characteristics for specialised applications. Sangdong's processing infrastructure is designed to produce concentrate grades exceeding 65% WO3 content, meeting international standards for both military and civilian applications.

The operation's technical advantages include:

- Existing infrastructure reducing capital investment requirements

- Established transportation networks connecting to international shipping routes

- Skilled workforce availability from regional mining expertise

- Environmental permitting already completed for production restart

Processing economics benefit from economies of scale, with unit costs declining as production volumes increase. The mine's ore handling systems can accommodate variable feed grades whilst maintaining consistent concentrate quality, providing operational flexibility during market transitions.

Strategische Szenarien für den südkoreanischen Wolframsektor

South Korea's emergence as a significant tungsten producer occurs within a broader context of supply chain reconfiguration across critical materials sectors. The convergence of two major projects within close geographical proximity creates potential for regional supply cluster development. In addition, mining innovation trends are supporting enhanced efficiency in tungsten extraction and processing operations.

Versorgungssicherheit durch geografische Diversifizierung

The strategic importance of reducing dependence on Chinese tungsten supply has intensified as geopolitical tensions affect trade relationships. Current market structure shows China maintaining approximately 80-86% of global tungsten production, creating systemic risks for industries requiring reliable access to this critical material.

South Korea's positioning within Western allied frameworks provides additional strategic value beyond simple supply diversification. The country's established trade relationships with major consuming nations facilitate integration into existing industrial supply chains without requiring fundamental restructuring of logistics networks.

Key diversification benefits include:

• Political stability reducing supply disruption risks

• Established quality standards meeting international specifications

• Transportation infrastructure supporting efficient distribution

• Currency stability facilitating long-term contract negotiations

Trade flow analysis indicates growing South Korean tungsten exports to Germany, with bilateral trade volume reaching approximately 250,850 USD in 2024. This represents early-stage development of what could become significant commercial relationships as production capacity expands.

Superzyklus-Szenario durch strukturelle Knappheit

Market analysis suggests potential for sustained price elevation extending beyond typical commodity cycles, with some projections indicating tungsten prices could reach 2,000 USD per tonne by 2027. This scenario assumes continued geopolitical tensions and limited new supply development outside established producing regions.

The structural nature of current supply constraints suggests that price increases may persist longer than historical patterns would indicate, creating opportunities for sustained profitability in well-positioned projects.

Factors supporting extended price strength include:

- Limited substitute materials for high-performance applications

- Long development timelines for new mining projects

- Regulatory barriers affecting mine permitting and development

- Capital intensity requirements for tungsten processing facilities

The supercycle scenario assumes continued military procurement growth, with defence spending increases supporting demand growth rates of 8-12% annually through 2030. Civilian applications in aerospace and industrial manufacturing provide additional demand stability during economic downturns.

Industrielle Nachfragetransformation

Military applications continue driving immediate demand growth, with tungsten's unique properties making it essential for armour-piercing ammunition, missile systems, and advanced aircraft components. These applications demonstrate limited price sensitivity due to performance requirements that cannot be met with alternative materials.

Military demand growth by application:

• Kinetic penetrators: 15-20% annual growth

• Rocket nozzles: 10-15% annual growth

• Aircraft components: 8-12% annual growth

• Naval applications: 12-18% annual growth

Civilian technology sectors present substantial long-term growth potential, particularly in renewable energy infrastructure and advanced manufacturing. Wind turbine components, electric vehicle charging systems, and semiconductor manufacturing equipment increasingly utilise tungsten alloys for critical performance characteristics.

Südkoreas Position als strategischer Wolframlieferant

The development of South Korean tungsten production capacity addresses growing demand for supply chain security among major consuming nations. Government support for critical mineral development through policy initiatives has created favourable conditions for mining investment and operational development.

Handelsbeziehungen und Exportentwicklung

South Korea's trade relationships with major tungsten-consuming countries provide established channels for market penetration as production capacity comes online. The country's integration within multilateral trade frameworks facilitates access to markets where supply security considerations influence purchasing decisions.

Export development strategies focus on high-value applications where quality and reliability command premium pricing. This approach maximises revenue potential whilst building long-term customer relationships that support sustained demand during market downturns. However, commodity market volatility remains a key consideration for export planning strategies.

| Export Destination | 2024 Volume (tonnes) | 2025 Projection (tonnes) | 2026 Target (tonnes) |

|---|---|---|---|

| United States | 45 | 120 | 300 |

| Germany | 28 | 85 | 180 |

| Japan | 62 | 110 | 240 |

| United Kingdom | 18 | 55 | 140 |

Infrastruktur und logistische Vorteile

South Korea's advanced port facilities and shipping infrastructure provide competitive advantages for tungsten concentrate exports to global markets. The country's strategic location within major shipping routes reduces transportation costs and delivery times compared to more remote producing regions.

Quality control systems aligned with international standards ensure consistent product specifications that meet demanding industrial applications. This capability becomes particularly important as end-users seek reliable suppliers for critical manufacturing processes where material consistency affects product performance.

Logistical infrastructure advantages:

• Deep-water ports accommodating large bulk carriers

• Container facilities for smaller speciality shipments

• Rail connections linking mines to export terminals

• Storage capacity enabling inventory management flexibility

Investitionsimplikationen der aktuellen Preisentwicklung

Current tungsten price levels have fundamentally altered investment economics for development projects, with potential returns reaching levels not seen in previous commodity cycles. Discounted cash flow analyses indicate internal rates of return exceeding 30% for well-positioned projects at current price assumptions.

Bewertungsmodelle bei erhöhten Preislevels

Traditional tungsten project valuations assumed long-term prices in the range of 300-400 USD per MTU, reflecting historical averages adjusted for inflation and production cost increases. Current market conditions require revised modelling assumptions that incorporate sustained higher pricing scenarios.

Investment sensitivity analysis reveals:

• Base case (800 USD/MTU): IRR 25-30%, NPV $150-200 million

• Current prices (1,200 USD/MTU): IRR 40-45%, NPV $300-400 million

• Upside scenario (1,600 USD/MTU): IRR 55-65%, NPV $500-650 million

Risk assessment frameworks must account for potential price volatility and the possibility of market normalisation as new supply sources develop. However, the strategic nature of tungsten demand provides downside protection not present in many other commodity sectors.

Kapitalmarktreaktionen und Finanzierungslandschaft

Equity markets have responded positively to tungsten exposure, with publicly traded companies experiencing significant valuation increases. This market recognition has improved access to development capital and reduced financing costs for qualified projects.

Venture capital and strategic investors have increased activity in the tungsten sector, recognising both financial return potential and strategic value creation opportunities. Government-backed investment initiatives in allied countries provide additional funding sources for projects that enhance supply chain security.

Financing trends include:

- Reduced equity dilution due to improved project economics

- Streaming agreements providing upfront capital for future production

- Strategic partnerships with end-users seeking supply security

- Government grants supporting critical mineral development

Auswirkungen auf industrielle Nachfrage und Substitution

High tungsten prices have prompted industrial users to examine alternative materials and process modifications that could reduce consumption requirements. However, the unique physical properties of tungsten limit substitution possibilities in many critical applications.

Substitutionseffekte und Nachfrageelastizität

Price elasticity analysis indicates that tungsten demand remains relatively inelastic across most applications, particularly in military and aerospace sectors where performance requirements take precedence over cost considerations. Substitution attempts typically result in reduced performance or increased system complexity that offsets cost savings.

Applications by substitution potential:

• High substitution risk: Consumer electronics, some industrial tooling

• Medium substitution risk: Medical devices, certain automotive components

• Low substitution risk: Military applications, aerospace components

• No substitution: Specialised alloys, high-temperature applications

Industrial adaptation strategies focus on efficiency improvements rather than material substitution. Manufacturing processes are being optimised to reduce waste and maximise utilisation of tungsten-containing components, extending service life and reducing replacement frequency.

Strategische Bevorratung und Lagerhaltung

Government stockpiling programmes have intensified as tungsten's strategic importance becomes more apparent. National security considerations drive inventory accumulation beyond commercial requirements, providing additional demand support during price corrections.

Strategic stockpiling represents a form of price insurance for governments, providing supply security whilst supporting market prices during periods of reduced industrial demand.

Private sector inventory strategies have evolved to balance carrying costs against supply security benefits. Companies with significant tungsten consumption are extending contract terms and building strategic reserves to reduce procurement risk. However, the volatile nature of tungsten pricing requires careful consideration of inventory management strategies.

The next major ASX story will hit our subscribers first

Marktentwicklung und Preisprognosen bis 2027

Medium-term market development depends on the balance between expanding supply capacity and continued demand growth across military and civilian applications. Current project pipelines suggest limited new production capacity additions before 2028, supporting continued price strength.

Angebotsprognosen und Produktionsentwicklung

Non-Chinese tungsten production capacity is expected to increase gradually as development projects advance through construction and commissioning phases. However, the technical complexity and capital requirements for tungsten operations limit the pace of capacity additions.

Global production forecast (metric tonnes WO3):

| Year | China Production | Non-China Production | Total Global | Price Scenario (USD/MTU) |

|---|---|---|---|---|

| 2026 | 68,000 | 12,000 | 80,000 | 1,000-1,400 |

| 2027 | 70,000 | 15,000 | 85,000 | 900-1,300 |

| 2028 | 72,000 | 18,000 | 90,000 | 800-1,200 |

| 2029 | 75,000 | 22,000 | 97,000 | 700-1,100 |

| 2030 | 78,000 | 26,000 | 104,000 | 600-1,000 |

Preismodellierung unter verschiedenen Szenarien

Base case scenario assumes gradual supply increase balancing continued demand growth, with prices stabilising in the 800-1,000 USD per MTU range by 2028. This scenario incorporates normal economic growth and measured expansion of tungsten applications.

Bull case scenario reflects sustained geopolitical tensions and accelerated military procurement, maintaining prices above 1,200 USD per MTU through 2027. Additional supply constraints from environmental regulations or operational challenges could extend elevated pricing further.

Bear case scenario assumes global economic recession reducing industrial demand whilst new supply capacity comes online faster than anticipated. Even under these conditions, strategic stockpiling and military demand provide price support above 600 USD per MTU.

Market volatility is expected to remain elevated as supply and demand adjustments occur. Price discovery mechanisms may become more transparent as trading volumes increase and financial instruments develop for risk management purposes. Furthermore, wolframpreise in südkorea will continue serving as a critical benchmark for non-Chinese supply pricing.

Häufig gestellte Fragen zu Wolframpreisen und Marktdynamik

Grundlegende Marktmechanismen

Warum ist Wolfram strategisch kritisch?

Tungsten possesses unique physical properties including the highest melting point of any metal (3,422°C) and exceptional density (19.3 g/cm³). These characteristics make it irreplaceable in applications requiring extreme temperature resistance and kinetic energy transfer, particularly in military and aerospace systems.

Wie beeinflussen chinesische Maßnahmen den Weltmarkt?

China's export policies and production quotas directly affect global supply availability, given the country's dominant market position. Quality standards and administrative procedures can create supply bottlenecks even when production capacity exists, amplifying price volatility during periods of strong demand.

Welche Rolle spielt Südkorea für die Versorgungssicherheit?

South Korea's strategic location and political stability within Western alliance frameworks make it an ideal alternative supply source. The country's advanced industrial infrastructure supports both mining operations and downstream processing capabilities required for integrated tungsten supply chains.

Investment- und Handelsfragen

Wie können Unternehmen Preisrisiken absichern?

Risk management strategies include long-term supply contracts with price escalation clauses, strategic inventory building, and partnership arrangements with mining companies. Some financial institutions are developing tungsten price derivatives, though liquidity remains limited compared to other metals markets.

Welche Qualitätsunterschiede bestehen zwischen Produzenten?

Tungsten concentrate quality varies primarily in WO3 content (typically 60-75%) and impurity levels affecting downstream processing. Premium grades command price premiums of 5-15% above standard specifications, particularly for applications requiring consistent chemical composition.

Wie entwickeln sich Transport- und Logistikkosten?

Shipping costs for tungsten concentrate remain relatively stable due to high unit values offsetting freight rate fluctuations. Container shipping provides flexibility for smaller volumes, whilst bulk carriers offer cost advantages for large-scale movements between major ports.

The information presented in this analysis is based on current market conditions and publicly available data. Tungsten market dynamics involve significant uncertainties, and price forecasts should be considered speculative. Investors should conduct thorough due diligence and consult qualified professionals before making investment decisions related to tungsten mining companies or related securities.

Market participants interested in deeper analysis of critical metals supply chains and South Korean mining developments can explore specialised commodity research platforms and industry publications for additional perspectives on strategic materials markets.

Looking to Capitalise on Critical Metals Market Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market in critical metals and strategic materials. Visit Discovery Alert's dedicated discoveries page to understand how major mineral discoveries have historically generated substantial returns, then begin your 14-day free trial today to position yourself ahead of these volatile yet lucrative markets.