July 15, 2026

Why Tungsten Offtake Structures Are Reshaping Critical Mineral Finance

Few forces reshape commodity markets as quietly and profoundly as the structural decisions made before a single tonne of ore reaches a processing facility. Long-term offtake agreements sit at the intersection of project finance, geopolitics, and industrial procurement strategy, functioning as instruments that bind future supply to future demand across decade-long horizons.

In the tungsten sector specifically, these agreements have taken on an entirely new dimension. As Western governments and industrial manufacturers confront the reality of near-total dependence on Chinese-origin tungsten, the race to secure alternative, politically stable supply has fundamentally altered how tungsten offtake agreements are structured, priced, and valued by the market.

The Almonty Sangdong mine offtake agreement, recently amended with Global Tungsten & Powders, offers a rare window into how these dynamics play out at the highest levels of critical mineral project development.

When big ASX news breaks, our subscribers know first

How Offtake Agreements Actually Function in Critical Mineral Project Finance

Most discussions of offtake agreements treat them as simple sales contracts. In reality, their function within the project finance architecture is considerably more sophisticated. When a development-stage mining company approaches institutional lenders for project financing, the quality of its offtake book is often the single most determinative factor in whether debt is approved, at what leverage ratio, and on what terms.

Lenders run what is known as a debt service coverage ratio model, projecting whether contracted cash flows are sufficient to meet principal and interest obligations across the loan term. A contract with:

- A long duration (reducing refinancing risk)

- A creditworthy counterparty (reducing default risk)

- A hard floor price mechanism (reducing revenue volatility)

- No upside price cap (preserving commodity exposure)

…scores maximally across every dimension a project finance bank cares about.

Critical Framework: In project finance, a hard floor price is not simply a commercial protection mechanism. It functions as a synthetic revenue guarantee that lenders can incorporate directly into their base-case debt serviceability models. The absence of an upside cap ensures this protection does not come at the cost of equity upside.

This is precisely the structure embedded in the amended Almonty Sangdong mine offtake agreement with Global Tungsten & Powders, and it is what enabled the earlier securing of $75.1 million in project financing from KfW IPEX-Bank, the German institution specialising in export and project finance.

The Sangdong Mine: A Deposit With Deep Historical Roots

Why This Asset Is Fundamentally Different From a Greenfield Development

The Sangdong deposit in South Korea is not a newly discovered orebody. It is one of the most extensively studied and historically productive tungsten deposits in the world outside of China, with documented production history stretching back decades before the mine was placed on care and maintenance in the 1990s following a prolonged collapse in tungsten prices.

This historical production legacy carries significant technical and commercial implications that are not widely appreciated:

- Geological confidence: The deposit has been drilled, sampled, and mined extensively, meaning the resource estimation carries a level of geological confidence that most greenfield projects cannot achieve

- Infrastructure inheritance: Unlike greenfield developments, Sangdong benefits from existing underground development, access infrastructure, and site-level knowledge accumulated over decades of prior operation

- Processing pathway knowledge: The mineralogical characteristics of the ore are well understood, reducing the metallurgical uncertainty that frequently derails processing plant commissioning at newer projects

Tungsten mineralisation at Sangdong occurs primarily as scheelite, the calcium tungstate mineral that is the dominant ore form in most large-scale tungsten deposits globally. Scheelite responds well to conventional flotation and gravity separation circuits, and the deposit's relatively consistent grade profile supports predictable concentrate output. Furthermore, the mine also carries meaningful molybdenum credits, adding a secondary revenue stream that is fully contracted under a separate life-of-mine offtake agreement with SeAH M&S, a major South Korean industrial conglomerate.

Processing plant throughput operations commenced on July 1, 2026, with ramp-up progressively advancing toward full Phase 1 capacity.

Dissecting the Amended Offtake: What Changed and Why It Matters

The Commercial Architecture of the GTP Agreement Upgrade

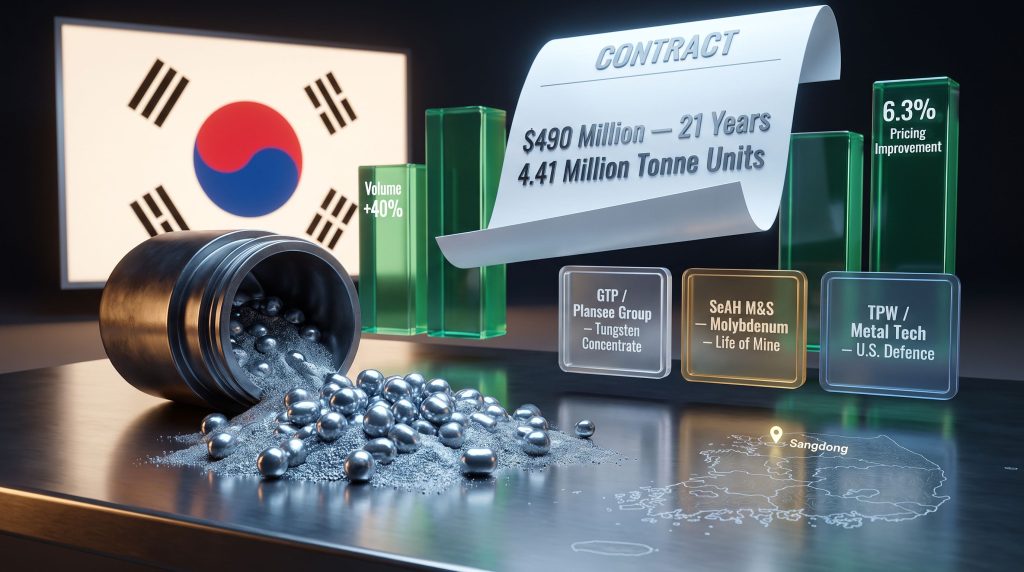

The amendment to the existing tungsten concentrate offtake agreement between Almonty and Global Tungsten & Powders represents one of the more substantive commercial upgrades seen in the critical mineral sector in recent years. Across every measurable parameter, the revised terms represent a meaningful improvement.

| Commercial Parameter | Previous Terms | Amended Terms |

|---|---|---|

| Contract Duration | 15 years from first delivery | 21 years from first delivery |

| Total Contracted Volume | 3.15 million tonne units | 4.41 million tonne units |

| Annual Minimum Volume | Post-ramp-up baseline | 210,000 tonne units per year |

| Pricing Improvement | Baseline | Approximately 6.3% uplift |

| Annual Revenue Uplift | Baseline | At least $30 million per year |

| Total Contract Revenue | Prior estimate | $490 million over contract life |

| Phase 1 Production Coverage | ~90% | ~90% (maintained) |

| Delivery Horizon | Mid-2040s | Late 2040s |

A 40% increase in contracted volume is not a routine commercial adjustment. It signals that Global Tungsten & Powders has conducted a forward-looking assessment of its feedstock requirements and concluded that securing a larger share of Western-aligned tungsten concentrate supply now, before Sangdong reaches full production, is strategically preferable to negotiating additional volumes later from a position of reduced leverage.

The floor price of $183 per metric tonne unit (MTU) operates without an upside price cap. At the confirmed annual minimum volume of 210,000 MTU, this translates to a revenue floor from the GTP agreement alone of approximately $38.43 million per year. The 6.3% pricing improvement then adds at least $30 million annually above previous contract terms, bringing the total contracted revenue across the 21-year agreement to $490 million.

Understanding Tonne Units: A Key Industry Metric

For readers unfamiliar with tungsten market conventions, a tonne unit (TU) is a unit of measure specific to tungsten concentrate trading. One tonne unit equals 10 kilograms of contained tungsten trioxide (WO3) within a tonne of concentrate. The standard benchmark for tungsten concentrate pricing is expressed in US dollars per metric tonne unit (MTU), which represents the per-kilogram price of contained WO3. This is distinct from how most base metals are quoted, and the distinction matters when interpreting revenue calculations tied to contracted volume figures.

Who Is Global Tungsten & Powders and What Does Their Commitment Signal?

The Plansee Group's Strategic Position in the Tungsten Value Chain

Global Tungsten & Powders is a core operating entity within the Plansee Group, an Austrian industrial group with deep expertise in refractory metals manufacturing. The Plansee Group's operations span tungsten, molybdenum, and tantalum-based materials, with GTP specifically focused on converting tungsten concentrate into advanced tungsten powders, carbides, and specialised materials for industrial cutting tools, electronics, and defence-grade components.

What makes GTP a particularly significant counterparty is its position as a genuine end-user and processor rather than a commodity trading intermediary. This distinction matters enormously in project finance:

- Trading intermediaries can be replaced or default more easily than industrial manufacturers with active processing infrastructure

- GTP's commitment to purchase is underpinned by its own downstream customer obligations, creating a natural incentive to honour the contract

- The Plansee Group's established European industrial footprint provides counterparty stability that a lender's credit committee can model with confidence

Structural Insight: When an offtake counterparty is itself embedded in a downstream manufacturing value chain, the probability of contract abandonment is materially lower than with a purely financial or trading counterparty. GTP's processing operations require consistent feedstock supply, making contract performance a commercial necessity rather than an optional commitment.

The Full Offtake Ecosystem: Three Agreements Across Two Commodities

Multi-Party Revenue Architecture at Sangdong

The Almonty Sangdong commercial structure extends well beyond the GTP tungsten agreement. Almonty has assembled a layered offtake framework spanning three distinct counterparties, two primary product forms, and two commodity streams.

| Offtake Agreement | Counterparty | Coverage | Duration | Floor Price | End Market |

|---|---|---|---|---|---|

| Tungsten Concentrate | Global Tungsten & Powders (Plansee Group) | ~90% Phase 1 concentrate | 21 years | $183/MTU (no upside cap) | European industrial processing |

| Molybdenum | SeAH M&S | 100% molybdenum output | Life of mine (~60 years) | $19.00/lb (no upside cap) | Korean steel manufacturing |

| Tungsten Oxide | Tungsten Parts Wyoming & Metal Tech | 100% Phase 1 oxide (min. 40 MT/month) | Binding (executed May 2025) | Structured pricing | U.S. defence procurement |

The molybdenum agreement deserves particular attention. A life-of-mine commitment spanning an estimated 60-year mine life is an exceptionally rare commercial structure, reflecting SeAH M&S's assessment of Sangdong as a generational source of molybdenum supply. Molybdenum at Sangdong is a genuine co-product rather than a trace byproduct, adding meaningful revenue diversification without incremental mining cost.

The tungsten oxide agreement with Tungsten Parts Wyoming and Metal Tech is architecturally distinct from the GTP concentrate agreement. Tungsten oxide is a further-processed product form, meaning Almonty is capturing additional value within the processing chain before delivery. The designation of this product stream for defence and aerospace supply aligns Sangdong with allied-nation supply chain requirements in an environment where defence procurement frameworks increasingly specify origin requirements for critical mineral inputs.

The next major ASX story will hit our subscribers first

Phase 2: The Uncommitted Optionality That Investors Should Understand

Why the Absence of Phase 2 Offtake Is Actually a Strategic Asset

A feature of the current offtake structure that warrants careful interpretation is the explicit exclusion of Phase 2 production from all existing agreements. Phase 2, which is anticipated to roughly double Sangdong's annual processing throughput, remains entirely uncontracted.

This is frequently misread as a commercial gap. However, a more analytically accurate interpretation is that it represents deliberate, value-preserving optionality.

| Dimension | Phase 1 | Phase 2 |

|---|---|---|

| Processing Capacity | Established baseline | Expected to double Phase 1 |

| Offtake Coverage | ~90% committed under GTP | No existing commitments |

| Revenue Certainty | $490M total contract revenue confirmed | Open to new negotiation |

| Operations Status | Commenced July 1, 2026 | Timeline not yet confirmed |

| Strategic Value | Revenue floor secured | Uncontracted upside optionality |

When Almonty negotiates Phase 2 offtake agreements, it will do so from a fundamentally different position than it occupied during Phase 1 negotiations. At that point, Sangdong will be a producing asset with demonstrable throughput, recovery rates, and concentrate quality metrics, rather than a development-stage project relying on technical studies and historical data. Demonstrated production performance is the single most powerful negotiating tool available to a mining company, and retaining Phase 2 volumes as uncommitted preserves the ability to extract maximum commercial value from that position.

Geopolitical Context: Why Western Tungsten Supply Security Has Reached Inflection Point

China's Dominance and the Structural Supply Risk It Creates

China currently accounts for the overwhelming majority of global tungsten mine production, estimated at over 80% of annual mined supply, with similarly dominant positions in processing and refined product output. This concentration has created a structural dependency that has no parallel in most other commodity markets. Consequently, tungsten's strategic importance to Western industrial and defence sectors has never been more acutely felt.

Unlike lithium or cobalt, where alternative supply development has progressed rapidly in response to battery demand growth, tungsten has received comparatively less investment attention despite its critical role in defence manufacturing. Tungsten's applications in armour-piercing projectiles, missile guidance systems, drone components, and precision cutting tools make it militarily irreplaceable. There is currently no commercially viable substitute for tungsten in its primary defence applications.

Several converging forces have elevated the urgency of Western-aligned supply development:

- China has progressively tightened export controls on tungsten and associated products, creating supply uncertainty for Western industrial and defence manufacturers

- The European Union has formally classified tungsten as a critical raw material under its Critical Raw Materials Act framework, identifying supply concentration as a systemic risk

- The United States and allied nations have increasingly embedded origin requirements into defence procurement frameworks, creating demand pull for non-Chinese tungsten sources

- NATO member nations face the uncomfortable reality that a sustained conflict scenario could sever access to Chinese tungsten supply precisely when defence manufacturing demand is highest

Furthermore, the broader critical minerals demand surge across allied Western nations has intensified scrutiny of single-source dependencies, placing projects like Sangdong at the centre of strategic supply planning. In addition, critical minerals for defence have become a central policy concern across NATO member states, underscoring why long-duration offtake structures at Sangdong carry significance well beyond conventional commodity finance.

Speculative Perspective: Some analysts within the refractory metals sector have begun to argue that tungsten could follow a trajectory similar to rare earth elements in the 2010s, where a period of Chinese export restriction prompted rapid and sustained price appreciation. If such a trajectory were to materialise, the no-upside-cap structure of Sangdong's offtake agreements would allow full participation in that price movement above the floor levels. This remains a speculative scenario, not a consensus forecast.

Key Takeaways for Investors and Industry Observers

The Almonty Sangdong mine offtake agreement amendment with Global Tungsten & Powders is not simply a news item about revised commercial terms. It is a structural data point about how critical mineral supply chains are being reorganised at an institutional level, with long-duration contracts, hard floor pricing, and creditworthy counterparties serving as the foundational instruments of that reorganisation.

Several implications are worth distilling:

- Revenue predictability at scale: $490 million in contracted revenue across 21 years, with a defined annual minimum floor, provides a level of cash flow visibility that is exceptional among junior and mid-tier mining companies

- Multi-commodity resilience: The combination of tungsten concentrate, tungsten oxide, and molybdenum offtakes across three counterparties creates revenue diversification that reduces single-commodity and single-counterparty concentration risk

- Phase 2 optionality value: Uncontracted Phase 2 volumes represent a genuine, material source of potential future value that is not currently reflected in existing revenue projections

- Counterparty quality as a signal: GTP's decision to expand volumes and extend duration is an informed commercial judgment by one of Europe's most established tungsten processors, carrying signal value about their expectations for Western tungsten supply tightness

- Project finance precedent: The KfW IPEX-Bank financing demonstrated that this offtake structure is of sufficient quality to satisfy the credit standards of an institutional development lender, setting a benchmark for future critical mineral project financing in the tungsten sector

This article contains forward-looking statements and speculative analysis regarding commodity price trajectories, supply chain dynamics, and project development outcomes. Such statements involve inherent uncertainty and should not be construed as financial advice or investment recommendations. Readers should conduct independent research and seek professional financial advice before making investment decisions.

Want to Track the Next Major Critical Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying high-potential mineral discoveries across tungsten, molybdenum, and more than 30 other commodities — translating complex data into clear, actionable insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have delivered exceptional returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.