July 27, 2026

Understanding Critical Metal Economics in Advanced Manufacturing

Strategic minerals operate under fundamentally different economic principles compared to traditional commodity markets. When materials become irreplaceable in critical applications, price elasticity of demand diminishes dramatically, creating unique market dynamics that defy conventional economic theory.

The tungsten price surge exemplifies this phenomenon perfectly. Unlike cyclical commodity rallies driven by speculation or temporary supply disruptions, tungsten's current market trajectory reflects structural transformation in how economies value strategic resources. Furthermore, the metal's unique properties create technological lock-in effects across multiple industries, making substitution economically unfeasible even at elevated price levels.

Physical Properties That Define Market Behavior

Tungsten possesses the highest melting point of any metallic element at 3,422 degrees Celsius, combined with exceptional thermal conductivity and hardness characteristics exceeding 9 on the Mohs scale. These properties make tungsten functionally irreplaceable in precision manufacturing applications where temperature stability and material performance represent non-negotiable requirements.

This technical irreplaceability fundamentally alters traditional supply-demand relationships. For instance, in semiconductor manufacturing, tungsten serves as both interconnect material and barrier layer in nanometer-scale circuit structures, with manufacturers unable to substitute alternative materials without complete redesign of interconnect architectures.

Current Market Metrics and Price Performance

The tungsten price surge has demonstrated extraordinary momentum across all product categories, as reported by tungsten market analysts:

| Product Category | 2024 Low | 2025 Average | March 2026 Peak | Total Increase |

|---|---|---|---|---|

| Tungsten Concentrates (62.5% WO₃) | $9,000/MTU | $16,000/MTU | $23,500/MTU | 161% |

| Ammonium Paratungstate (88.5% WO₃) | $220/kg | $320/kg | $450/kg | 105% |

| Tungsten Powder (99%+ purity) | $28,000/MT | $42,000/MT | $55,000/MT | 96% |

These price increases exceed typical commodity rally magnitudes, reflecting the intersection of supply constraints with technologically-driven demand growth that exhibits minimal price sensitivity.

When big ASX news breaks, our subscribers know first

How Supply Concentration Creates Market Vulnerabilities

China's Strategic Resource Control Mechanisms

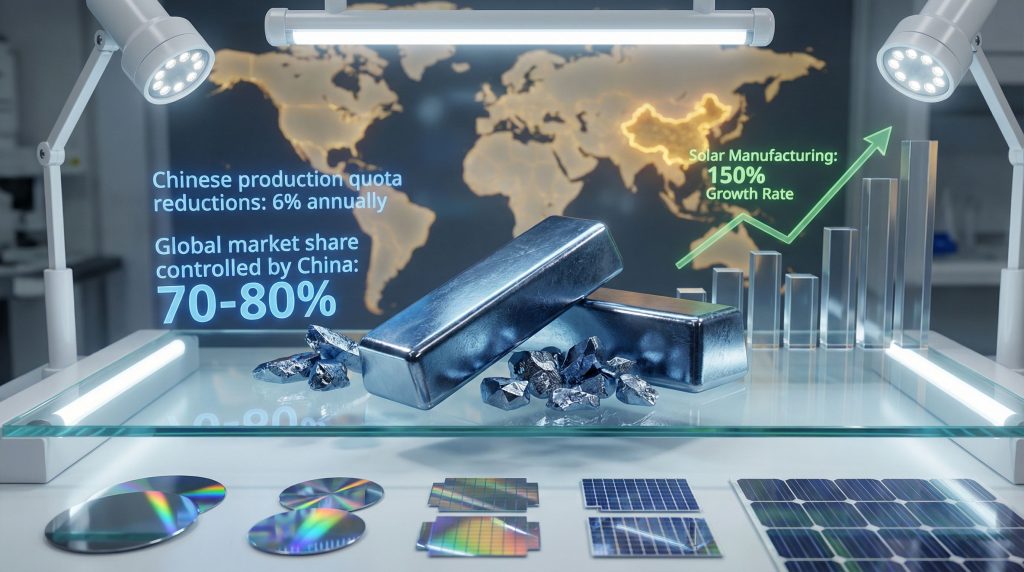

China's dominance in tungsten production represents one of the most concentrated supply chains in global commodity markets. With approximately 70-80% of global primary production capacity, China exercises unprecedented control over tungsten availability, implementing sophisticated policy tools that extend beyond traditional export quotas.

The Chinese government has systematically implemented:

• Production quota reductions of approximately 6.5% annually for multiple consecutive years

• Enhanced export licensing requirements creating administrative barriers independent of quota constraints

• Mandatory recycling quotas diverting material from export markets into domestic recycling streams

• State enterprise allocation preferences favouring domestic strategic industries

Export Control Mechanics and Market Impact

China's export control system operates through a multi-layered licensing framework administered by the Ministry of Commerce. Each tungsten export transaction requires separate licensing approval, creating administrative capacity constraints that limit actual exports below theoretical quota levels.

This system effectively functions as an export tax mechanism, allowing Chinese authorities to capture monopoly rents while constraining global supply availability. Consequently, the approach differs fundamentally from traditional commodity export policies that maximise volume; instead, China employs controlled scarcity to maintain elevated pricing whilst ensuring domestic industries receive priority allocation.

Inventory Depletion and Supply Chain Stress

Global tungsten inventory levels have declined to multi-year lows, with inventory-to-consumption ratios dropping below historical averages throughout 2025. This inventory depletion creates amplified price sensitivity to any supply disruptions, as industrial consumers maintain minimal buffer stocks.

The China International Capital Corporation projects a global market deficit of 20,000 metric ton units by 2028, representing approximately 15-18% of anticipated total supply availability. This structural deficit reflects sustained Chinese export constraints combined with limited new production capacity outside China.

Which Technological Sectors Drive Unprecedented Demand Growth

Semiconductor Industry Transformation

The semiconductor sector's evolution toward advanced manufacturing nodes has dramatically increased tungsten consumption per unit of production. Advanced chip fabrication requires tungsten for:

• Interconnect layers in 3-nanometre and 1-nanometre process technologies

• Barrier layers preventing metal diffusion in complex circuit architectures

• Contact plugs enabling electrical connections in three-dimensional chip designs

• Gate electrodes in advanced transistor structures

Taiwan Semiconductor Manufacturing Company, Samsung Semiconductor, and Intel have all indicated that tungsten supply security represents a critical constraint on production expansion planning. However, procurement teams implementing strategic stockpiling programs demonstrates the broader critical minerals energy security implications.

Clean Energy Infrastructure Demands

Solar panel manufacturing has emerged as a major tungsten consumption driver, with wire usage in silicon wafer production expanding rapidly:

Solar Industry Tungsten Consumption:

• 2023: 15% market penetration for tungsten wire cutting

• 2025: 60% market penetration achieved

• Efficiency gains justify premium material costs

• Production capacity expansion requires sustained tungsten availability

This adoption reflects efficiency improvements that justify higher material costs, creating relatively price-inelastic demand in a rapidly expanding market sector.

Defense and Aerospace Acceleration

Geopolitical tensions have accelerated defence spending globally, with tungsten-intensive applications experiencing sustained demand growth:

• Armour-piercing ammunition requiring 5-12 kilograms of tungsten per projectile

• Aircraft engine components utilising tungsten-heavy alloys for high-temperature performance

• Satellite systems incorporating tungsten for radiation shielding and thermal management

• Naval applications including submarine components and advanced weapons systems

U.S. Department of Defense procurement documentation indicates significant increases in weapons system production over the 2025-2026 period. Furthermore, tungsten availability constraints affecting production scheduling for multiple high-priority programmes highlights how the US mineral production order directly impacts strategic manufacturing.

What Economic Scenarios Could Reshape Tungsten Markets

Scenario Analysis Framework

Market participants must navigate multiple potential futures for tungsten pricing and availability, each driven by different combinations of geopolitical, technological, and economic factors.

High Price Scenario ($2,500-3,000/MTU by 2027):

• Continued or intensified Chinese export restrictions

• Sustained geopolitical tensions driving defence demand

• Limited new production capacity additions outside China

• Technology sector growth maintaining consumption expansion

Moderate Price Scenario ($1,800-2,200/MTU by 2027):

• Successful development of Western production projects

• Moderate easing of Chinese export policies

• Advanced recycling technology deployment

• Balanced supply-demand conditions

Supply Breakthrough Scenario ($1,200-1,600/MTU by 2027):

• Major new deposits entering production rapidly

• Breakthrough recycling technologies recovering 40-50% of industrial waste

• Significant substitution material development

• Economic slowdown reducing industrial demand

Critical Variables Influencing Outcomes

The trajectory of tungsten markets depends heavily on several key variables that market participants must monitor:

Production Capacity Timeline:

Development-stage projects outside China typically require 2-3 years from construction commencement to commercial production. Projects like Almonty's Sangdong operation in South Korea represent significant supply additions, but timing remains critical for market impact.

Recycling Technology Advancement:

Current tungsten recycling rates remain below 30% of consumption, with significant technical challenges in recovering tungsten from complex alloys and finished products. However, breakthrough technologies could fundamentally alter supply-demand balances, as demonstrated by advances in waste management solutions.

Substitution Research Progress:

Research into alternative materials focuses on developing composites that can replicate tungsten's unique combination of density, hardness, and thermal properties. Nevertheless, such development typically requires years to achieve commercial viability.

How Geopolitical Factors Reshape Strategic Mineral Markets

National Security Classification Evolution

Western governments have systematically elevated tungsten's strategic importance through formal classification systems:

• United States: Defense Production Act classification as "critical defence material"

• European Union: Critical Raw Materials list inclusion with "high-risk" designation

• Canada: National Security Memorandum strategic mineral classification

• Australia: Department of Resources critical mineral guidance inclusion

These classifications trigger cascading policy implications including domestic production subsidies, research and development funding for substitution technologies, strategic stockpile building requirements, and enhanced trade negotiation leverage.

Strategic Stockpiling Programs

Government and industrial stockpiling creates additional demand layers beyond traditional consumption patterns:

U.S. National Defense Stockpile:

Congressional testimony from defence procurement officials indicates current tungsten holdings remain insufficient to meet defence production requirements. Additionally, procurement deficiencies extending production timelines for high-priority weapons systems demonstrates the critical minerals strategy importance.

Allied Nation Coordination:

South Korea has implemented mandatory tungsten stockpiling requirements for defence contractors, with documented minimum inventory ratios of 6-12 months of consumption at specified production rates.

Trade Policy Integration

Tungsten increasingly features in bilateral trade negotiations and strategic partnership agreements. Countries recognise that tungsten supply security represents a national security issue requiring diplomatic solutions beyond market mechanisms.

Potential policy tools include preferential trade agreements for tungsten access, joint strategic reserve programs among allied nations, and coordinated responses to supply disruptions.

Which Investment Opportunities Emerge from Market Disruption

Primary Production Project Evaluation

Development-stage tungsten projects outside China offer direct exposure to structural supply deficits, but require sophisticated evaluation frameworks:

Resource Quality Assessment:

• Ore grade and tungsten content consistency

• Processing complexity and recovery rates

• Infrastructure requirements and development costs

• Permitting timelines and regulatory risks

Market Access Considerations:

• Product specification requirements for target markets

• Customer relationship development and off-take agreements

• Transportation and logistics optimisation

• Quality control and certification capabilities

Technology Sector Opportunities

Companies developing advanced tungsten processing, recycling, or substitution technologies may capture significant value as traditional supply chains face disruption:

Recycling Technology Development:

Advanced tungsten recovery from industrial waste streams could address 40-50% of consumption growth, creating substantial value for technology developers and operators. This aligns with broader trends in the mining industry evolution towards sustainability.

Processing Innovation:

Improvements in tungsten refining and powder production can enhance yield rates and reduce processing costs, creating competitive advantages in constrained supply environments.

Strategic Positioning Approaches

Investment strategies must account for tungsten's unique market characteristics:

Direct Exposure Vehicles:

• Development-stage mining companies with advanced tungsten projects

• Integrated producers with processing capabilities

• Technology companies developing tungsten applications

Indirect Exposure Considerations:

• Downstream manufacturers with tungsten-dependent operations

• Defence contractors with tungsten-intensive product lines

• Technology companies requiring tungsten for advanced applications

The next major ASX story will hit our subscribers first

What Risks Could Disrupt the Current Price Trajectory

Demand Destruction Mechanisms

Extremely elevated tungsten prices could trigger several demand reduction mechanisms:

Substitution Acceleration:

• Research funding for alternative materials may increase substantially

• Industrial applications may accept performance trade-offs to reduce costs

• Design modifications could reduce tungsten content in existing applications

Project Deferral Effects:

• Capital-intensive projects may postpone implementation

• Discretionary applications may face budget constraints

• Industrial consumers may optimise inventory management to reduce consumption

Supply Response Potential

High prices create incentives for supply responses that could moderate market conditions, as evidenced by recent supply chain developments:

Exploration Acceleration:

Elevated prices make previously marginal tungsten deposits economically viable, potentially increasing resource development activity in regions outside China.

Recycling Economics:

Higher primary material costs improve recycling project economics, potentially accelerating technology development and capacity deployment.

Economic Recession Scenarios

Broader economic downturns could affect tungsten demand through multiple channels:

• Industrial production reductions affecting manufacturing demand

• Capital expenditure deferrals impacting technology sector consumption

• Defence budget pressures potentially moderating military procurement

• Construction activity declines reducing infrastructure-related tungsten usage

However, strategic applications in defence and critical technology sectors would likely maintain consumption levels even during economic contractions.

How Market Participants Should Position for Extended Volatility

Supply Chain Diversification Strategies

Companies dependent on tungsten must develop comprehensive sourcing strategies that account for continued supply uncertainty:

Multi-Source Procurement:

• Direct relationships with non-Chinese producers

• Participation in development-stage project financing

• Strategic partnerships with recycling operations

• Alternative material research and qualification programs

Inventory Management Optimisation:

• Strategic stock-building during supply availability

• Just-in-case inventory policies replacing just-in-time approaches

• Collaborative inventory management with supply chain partners

• Financial hedging instruments for price risk management

Investment Strategy Framework

The tungsten price surge offers exposure to structural supply deficits, but requires sophisticated risk management:

Project Evaluation Criteria:

• Development timeline alignment with market deficit projections

• Regulatory and permitting risk assessment across jurisdictions

• Management team experience in resource development and operations

• Financial capacity for sustained development through market cycles

Portfolio Construction Considerations:

• Geographic diversification across tungsten projects

• Development stage diversification balancing risk and timeline

• Technology exposure including processing and recycling innovations

• Market concentration limits given tungsten's specialised nature

Long-Term Strategic Positioning

The tungsten price surge is transitioning from commodity-driven to strategically-managed resource allocation, with implications extending well beyond current price cycles:

Structural Market Evolution:

• Government intervention in supply chain management

• Strategic alliance formation among consuming nations

• Technology development prioritisation for supply security

• Integration of tungsten access into broader geopolitical strategy

This transformation suggests that traditional commodity market analysis may prove insufficient for understanding tungsten market dynamics. Consequently, frameworks incorporating geopolitical risk assessment, technology development timelines, and strategic resource management principles become essential.

Risk Management Protocols:

Market participants must develop robust frameworks for managing tungsten exposure that account for the metal's unique characteristics, including concentrated supply chains, technological irreplaceability, and strategic importance across multiple critical industries.

Ready to Capitalise on Critical Mineral Market Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in critical minerals before the broader market recognises their strategic value. Begin your 14-day free trial today and secure your market-leading advantage whilst positioning yourself ahead of the tungsten supply transformation and broader critical minerals strategy developments.