June 6, 2026

The Metal That Moves Armies: Why Tungsten Supply Chains Are Being Rebuilt From the Ground Up

Every major shift in global manufacturing power leaves a trail of overlooked commodities in its wake. Cobalt reshaped battery supply chains. Rare earths restructured electronics procurement. Now tungsten, a metal most people could not name on a periodic table, is forcing Western defence planners and industrial manufacturers to confront an uncomfortable reality: when a single country controls roughly 80% of global production and processing capacity for an irreplaceable material, the entire downstream supply chain operates at that country's discretion. Tungsten's strategic importance has never been more apparent.

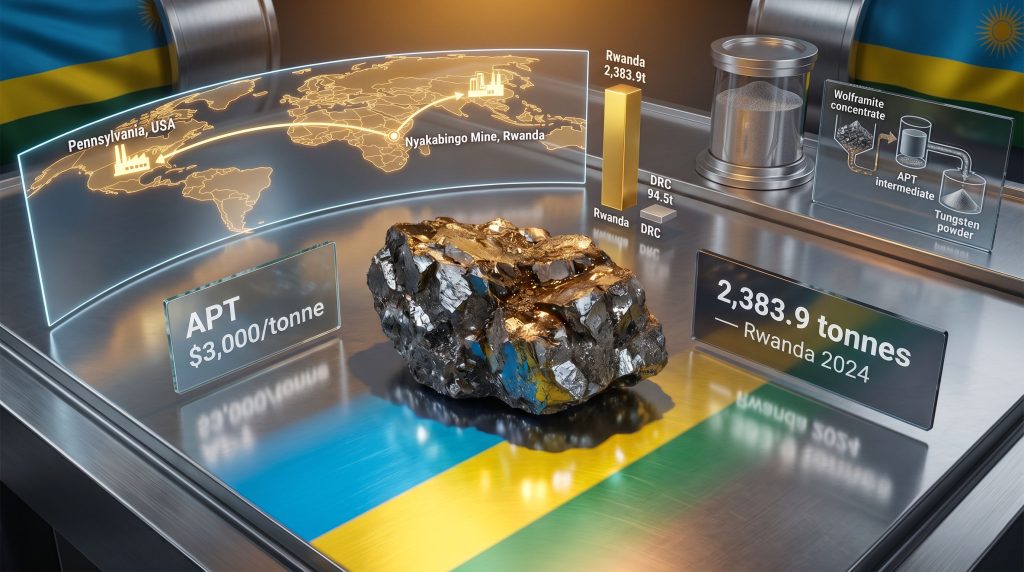

That dynamic is now playing out in real time, with ammonium paratungstate (APT), the benchmark intermediate product in tungsten processing, surpassing $3,000 per tonne in late April 2026, a sharp acceleration from pricing at the start of the year. The ripple effects of this price movement are being felt from defence contractor procurement desks in Virginia to aerospace manufacturing floors in Toulouse. And in an unlikely corner of Central Africa, Rwanda tungsten exports to the US are emerging as one of the only structurally positioned solutions to fill the gap.

When big ASX news breaks, our subscribers know first

Why Tungsten Cannot Be Substituted Away

The Physical Properties That Create Strategic Dependency

Tungsten holds a distinction no other element can claim: it has the highest melting point of any metal, reaching approximately 3,422 degrees Celsius. Combined with exceptional density and thermal resistance, this makes it functionally irreplaceable in applications where extreme conditions are non-negotiable.

The industrial applications span several critical sectors:

- Defence hardware: Armor-piercing kinetic energy penetrators, where tungsten's density and hardness are essential for penetrating hardened targets

- Aerospace components: High-temperature alloys, turbine counterweights, and vibration dampening in aircraft structures; furthermore, tungsten in defence and aerospace continues to grow in importance

- Electronics: Electrical contacts, semiconductor interconnects, and filaments where thermal stability is critical

- Industrial tooling: Tungsten carbide cutting tools that represent the backbone of precision manufacturing

Beyond its physical properties, tungsten carries formal strategic weight. Both the United States and European Union have classified it as a critical mineral, a designation that carries direct procurement consequences. Critical mineral classification elevates tungsten from a routine commodity purchasing decision to a supply chain resilience and national security consideration, triggering strategic reserve assessments and formal diversification mandates across government procurement frameworks.

Tungsten also sits within the "3Ts" classification alongside tin and coltan as Central Africa's three most strategically significant mineral exports, a grouping that reflects the region's disproportionate importance to global industrial supply chains.

Demand Architecture: Who Consumes Tungsten and Where Growth Is Accelerating

Understanding where tungsten demand originates helps explain why supply disruptions create cascading consequences across multiple industries simultaneously.

| Sector | Current Demand Share | Projected Share (2027–2028) | Primary Driver |

|---|---|---|---|

| Automotive | 25–30% | Stable | Cutting tools, wear-resistant components |

| Military & Defence | ~12% | ~15% | Stockpile replenishment, kinetic munitions |

| Electronics & Aerospace | Remainder | Growing | Precision components, thermal management |

Source: Project Blue (defence demand projections); Argus (automotive consumption data)

The automotive sector's structural demand provides a stable baseline, but it is the defence sector where near-term demand acceleration is most significant. According to Project Blue forecasts, military consumption is projected to reach 15% of global tungsten demand between 2027 and 2028, driven by NATO and allied nation stockpile replenishment cycles that have been accelerated by geopolitical instability across multiple regions.

This creates a critical dynamic for pricing: the automotive sector absorbs demand predictably, but defence procurement operates in concentrated purchasing cycles that generate price volatility spikes when multiple nations replenish simultaneously. In addition, the broader critical minerals demand surge is compounding pressure across the entire sector.

China's 2025 Export Restrictions: Anatomy of a Supply Chain Shock

How Beijing Compressed the Western Tungsten Supply Funnel

China's dominance over global tungsten is not merely a matter of mining output. The country controls approximately 80% of both production and downstream processing capacity, meaning that even tungsten sourced from other jurisdictions frequently passes through Chinese processing infrastructure before reaching Western manufacturers.

The 2025 policy changes introduced two simultaneous mechanisms of supply restriction:

- Mining quota reductions: Beijing reduced authorised extraction levels, limiting the volume of material available for export

- Export licence compression: By December 2025, the Chinese government had authorised only 15 companies to export tungsten for the 2026–2027 period, a dramatic reduction from previous licensing baselines

The dual-mechanism approach is significant. A quota reduction alone would tighten supply. An export licence compression alone would restrict market access. Applied simultaneously, the combination creates a structural bottleneck that Western manufacturers cannot negotiate around through pricing or volume commitments alone.

When a government simultaneously reduces mining quotas and compresses export licences, the resulting price signal is not cyclical. It reflects a deliberate policy decision to prioritise domestic consumption and strategic leverage over export revenue. Western manufacturers without pre-negotiated offtake agreements face structural cost exposure that spot market pricing cannot resolve.

APT as the Canary in the Supply Chain

Ammonium paratungstate (APT) functions as the global price benchmark for the tungsten supply chain. It is the intermediate product formed when wolframite or scheelite ore concentrates are chemically processed, and it serves as the feedstock for tungsten powders, wire, rod, and carbide products used across defence and industrial applications.

When APT prices crossed $3,000 per tonne in late April 2026, the movement reflected cumulative market shock from the 2025 policy implementation. This benchmark price cascades downstream: elevated APT costs translate directly into higher prices for tungsten powders, finished components, and ultimately the defence and aerospace systems that incorporate them.

For US manufacturers locked into spot market procurement, the $3,000/tonne APT environment represents a compounding cost exposure with no short-term resolution pathway, because the supply gap created by Chinese export restrictions cannot be filled quickly by alternative producers without existing operational infrastructure and established logistics chains.

Rwanda's Position in the Global Tungsten Supply Structure

Africa's Industrial-Scale Tungsten Producer

Rwanda exported 2,383.9 tonnes of tungsten in 2024, valued at $35.76 million, according to official data reported by Ecofin Agency. This positions the country among the top six tungsten producers globally, behind China, Russia, and North Korea, and establishes it as Africa's undisputed tungsten export leader by a substantial margin.

The engine behind this output is the Nyakabingo mine in northern Rwanda, operated by Trinity Metals and described by the company as the largest tungsten project on the African continent. Key operational metrics include:

- Monthly production capacity: 100–110 tonnes of wolframite concentrate

- Annualised output: Exceeding 1,200 tonnes of concentrate per year

- Estimated recoverable resources: More than 115,000 tonnes, indicating a multi-decade production horizon

- Mining method: Fully mechanised and industrial-scale operations

The 115,000-tonne resource base is particularly significant from a long-term supply security perspective. At current extraction rates, Nyakabingo supports decades of continued production with meaningful expansion potential, giving downstream partners confidence in multi-year offtake commitments without supply exhaustion risk.

Rwanda vs. DRC: A Tale of Two Tungsten Sectors

The contrast between Rwanda's tungsten sector and that of the Democratic Republic of Congo illustrates why industrial-scale operations command different strategic interest from Western buyers than artisanal output.

| Metric | Rwanda | DRC |

|---|---|---|

| Export Volume (most recent annual) | 2,383.9 tonnes (2024) | 94.5 tonnes (2025) |

| Export Value | $35.76 million | $1.3 million |

| Total Wolframite Output | Industrial-scale | 213 tonnes (artisanal, 2025) |

| Mining Method | Fully mechanised | Entirely artisanal |

| Primary Operation | Nyakabingo (Trinity Metals) | Multiple small-scale artisanal sites |

| US Trade Agreement | Signed August 2025 | Not yet established |

| DFC-Backed Institutional Investment | Yes, via TechMet | Exploratory stage only |

Source: Ecofin Agency, May 2, 2026

The DRC's wolframite output is entirely artisanal, which creates structural barriers to integration into formal Western supply chains. Artisanal mining produces inconsistent concentrate grades, lacks systematic supply chain documentation, and cannot reliably guarantee conflict-free provenance certifications, all of which are increasingly non-negotiable prerequisites for US defence and aerospace procurement.

It is also worth noting that tungsten represents a marginal component of the DRC's broader mineral export portfolio. The country exported 46,251 tonnes of cassiterite (tin ore) in 2025, valued at $652 million, demonstrating that tin, not tungsten, dominates its "3Ts" minerals economy. This disproportion reflects where DRC infrastructure investment and artisanal network development has historically been concentrated.

How the Rwanda-US Tungsten Supply Chain Was Constructed

The Commercial Framework: GTP, Trinity Metals, and Traxys

The operational architecture connecting Rwandan tungsten production to US industrial consumption was formalised in August 2025 through a multi-year offtake agreement between Trinity Metals and Global Tungsten & Powders (GTP), the largest tungsten manufacturer in the United States, headquartered in Towanda, Pennsylvania. Traxys functions as the offtake trading partner facilitating logistics and commercial flow between the two parties. Consequently, tungsten offtake agreements of this nature are becoming increasingly central to Western supply chain strategy.

Key commercial parameters of the agreement include:

- Contracted volume: 4 to 7 containers per quarter

- Initial term: Two years, with structural optionality for extension

- First delivery: Late 2025 or early 2026, marking the first tungsten shipment from Africa's Great Lakes region into the US industrial supply chain

This agreement is not merely a bilateral commercial arrangement. It represents the first formalised supply chain link between an African Great Lakes tungsten producer and the US defence-industrial base, creating a logistics and compliance framework that future volume expansions can be layered onto without rebuilding foundational infrastructure.

From Wolframite to Defence-Grade Powder: The Processing Architecture

Understanding the processing chain from mine to end-use application clarifies why GTP's Pennsylvania facility is such a strategically valuable node in the supply chain.

Wolframite concentrate from Nyakabingo undergoes chemical processing at GTP's Towanda facility to produce APT, which is then further refined into tungsten powders with varying particle size distributions optimised for specific applications. These include:

- Armour-piercing projectile cores for defence applications

- Aerospace alloy components requiring thermal stability

- High-precision electronic contacts

- Tungsten carbide cutting tool substrates for industrial manufacturing

The geographic proximity of GTP's processing facility to US defence contractors and aerospace original equipment manufacturers along the Eastern Seaboard provides practical advantages for compliance verification, classified procurement integration, and rapid delivery to end-users operating under national security procurement frameworks.

Institutional Architecture: TechMet and the DFC Signal

TechMet's equity stake in Trinity Metals adds a layer of institutional significance that transforms the commercial arrangement. The US International Development Finance Corporation (DFC) has provided backing to TechMet, the investment firm holding the Trinity Metals stake, which represents a clear signal of Washington's long-term commitment to securing alternative tungsten supply sources outside China's sphere.

This institutional backing changes the risk calculus for downstream US manufacturers considering long-term African supply agreements. A DFC-backed investment structure provides implicit sovereign-level reassurance around political risk, governance standards, and supply continuity, considerations that are weighed heavily in defence sector procurement decisions.

The Bilateral Policy Layer

The Rwanda-US trade agreement signed in August 2025 provides the enabling policy framework for mineral exports, reducing tariff and regulatory friction for tungsten concentrate shipments. This bilateral framework reflects Rwanda's deliberate positioning to strengthen diplomatic and commercial ties with Washington as a strategic hedge against the consolidation of Chinese supply chain leverage over Western manufacturers.

Scenario Analysis: Rwanda's Tungsten Export Growth Pathways Through 2028

Scenario 1: Sustained Chinese Restrictions Accelerate African Diversification

If Beijing maintains or further tightens export quotas through 2027–2028, Western buyers face a structural deficit with no short-term resolution. In this scenario, Nyakabingo transitions from an alternative supplier to a tier-one strategic source for US and European manufacturers.

At $3,000 per tonne APT-equivalent pricing applied to Rwanda's 2024 export baseline of 2,383.9 tonnes, the directional revenue impact is substantial relative to the $35.76 million recorded when exports were priced at earlier, lower rates. Expansion of GTP offtake volumes beyond the initial 4 to 7 containers per quarter commitment becomes commercially viable and operationally logical given Nyakabingo's production capacity headroom.

Scenario 2: Defence Procurement Formalises Rwanda as a Preferred Source Nation

With military tungsten consumption projected to reach 15% of global demand by 2027–2028, a dedicated defence procurement channel for Rwanda's output becomes increasingly plausible. Rwanda's compliance infrastructure, covering conflict mineral traceability, OECD Due Diligence Guidance for Responsible Supply Chains, and regional mineral certification schemes, creates a competitive advantage that artisanal producers structurally cannot match.

DFC-backed investment signals the potential for US government-aligned offtake frameworks or strategic reserve purchasing that would lock in volume commitments beyond the current commercial agreement. However, defence metal supply risks remain a broader concern that policymakers must address in parallel.

Scenario 3: DRC Enters the Formal Supply Chain

Kinshasa's growing engagement with US investors across critical mineral sectors introduces the possibility of DRC tungsten becoming a medium-term supplementary source. However, industrialising an entirely artisanal sector requires capital investment in mining infrastructure, processing facilities, traceability systems, and governance frameworks that collectively represent a 5 to 8 year development horizon at minimum.

This timeline constraint means DRC tungsten formalisation is not a near-term competitive threat to Rwanda's position. A complementarity scenario is more likely: Rwanda meets near-term US supply needs while DRC develops supplementary capacity over a longer horizon, expanding the overall African contribution to Western supply chains.

The next major ASX story will hit our subscribers first

Investor and Procurement Implications

What US Manufacturers Should Be Assessing Now

Industries most exposed to Chinese supply disruptions include defence contractors, aerospace original equipment manufacturers, electronics manufacturers, and industrial tooling producers. The Trinity Metals-GTP framework creates a template for establishing African supply agreements, but the window for securing favourable long-term offtake commitments narrows as the structural supply deficit becomes more widely recognised and competitive demand for available capacity increases.

Key procurement strategy considerations in a $3,000/tonne APT environment:

- Spot market exposure assessment: Quantify the cost impact of current APT pricing on input costs and project how sustained elevated prices affect margin structures

- Long-term offtake evaluation: Assess the trade-off between spot flexibility and contractual price certainty from African producers

- Compliance infrastructure audit: Verify that African supply chain partners meet OECD due diligence and conflict mineral traceability standards required for defence procurement compliance

- Logistics chain mapping: Establish processing proximity considerations to minimise supply chain vulnerability at the APT refining stage

Governance as a Non-Negotiable Procurement Prerequisite

Rwanda's participation in regional mineral certification schemes and its adherence to OECD Due Diligence Guidance for Responsible Supply Chains is increasingly a procurement prerequisite rather than an optional compliance consideration. US defence and aerospace buyers operate under tightening supply chain transparency requirements, and Rwanda's governance infrastructure positions it favourably relative to alternative African or developing-world suppliers.

This article is for informational purposes only and does not constitute financial, investment, or procurement advice. Commodity price projections, demand forecasts, and scenario analyses involve assumptions and uncertainties that may not reflect actual outcomes. Readers should conduct independent due diligence before making investment or procurement decisions based on information contained herein.

Rwanda's Larger Significance in Africa's Critical Mineral Repositioning

From Peripheral Supplier to Embedded Supply Chain Participant

Rwanda tungsten exports to the US represent something more consequential than a single commodity success story. The country's pre-2025 tungsten exports were primarily directed toward European processors, with the US market representing a comparatively negligible baseline. The formalisation of the Trinity Metals-GTP supply chain, underpinned by institutional capital and a bilateral trade agreement, elevates Rwanda from a peripheral commodity exporter to an embedded participant in the US defence-industrial supply base.

The architecture required to achieve this repositioning, specifically industrial-scale mining infrastructure, functioning governance and traceability systems, institutional investment capital, and bilateral diplomatic alignment, provides a replicable model for other African nations with critical mineral endowments seeking to capture strategic value rather than simply export raw commodities.

The Broader Pattern: Africa's Critical Mineral Leverage Is Growing

Rising tungsten prices and Chinese export restrictions are demonstrating a pattern that has already played out across cobalt, lithium, and rare earth elements: Africa's critical mineral endowment is becoming a structural lever in great-power supply chain competition. Countries with industrial-scale operations, governance credibility, and established Western diplomatic relationships are capturing disproportionate value from this dynamic.

Rwanda's tungsten position reflects the convergence of all three factors. Whether that convergence can be sustained through 2028 and beyond depends partly on Nyakabingo's operational performance, partly on how aggressively Beijing maintains export restrictions, and partly on whether the institutional frameworks constructed around the Trinity Metals-GTP partnership are expanded and deepened as supply chain competition intensifies.

What is already clear is that Rwanda tungsten exports to the US have moved beyond the realm of exploratory trade and into the architecture of strategic supply security. That transition, from commodity trade to sovereign supply instrument, is the defining shift that separates Rwanda's tungsten sector from almost every other African mineral export story currently in circulation.

For ongoing coverage of African critical mineral supply chains and trade developments, Ecofin Agency at ecofinagency.com provides sector-focused reporting across mining and energy industries throughout the continent.

Want to Spot the Next Major Critical Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying actionable opportunities across tungsten, rare earths, and more than 30 other commodities — converting complex geological data into clear, decisive investment insights. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.