May 22, 2026

The global tungsten supply chain has reached a critical inflection point, with the development of a new tungsten mine in South Korea marking a significant shift in strategic mineral sourcing. This development comes as industries worldwide grapple with supply chain vulnerabilities and the need for reliable access to critical materials that enable advanced manufacturing processes.

Modern industrial infrastructure relies heavily on materials that can withstand extreme conditions while maintaining precision and reliability. Among these critical materials, tungsten stands out as an irreplaceable component in sectors ranging from aerospace to semiconductor manufacturing, creating supply chain dependencies that have become increasingly apparent in recent years. Furthermore, the mining industry evolution has highlighted the urgent need for supply diversification.

The strategic importance of tungsten stems from its unique physical properties that cannot be replicated by alternative materials. With the highest melting point of any pure metal at 3,695°C (6,683°F) and a density of 19.25 g/cm³, tungsten enables manufacturing processes and applications that would be impossible with conventional materials. This combination of extreme temperature resistance and exceptional density makes tungsten indispensable for cutting-edge industrial applications.

Industrial Applications Driving Tungsten Demand

The global tungsten market demonstrates remarkable diversity in its end-use applications, with hardmetals and cemented carbide tools representing approximately 50% of global consumption. These tungsten carbide tools maintain their cutting efficiency and hardness even at temperatures exceeding 1,000°C, enabling the machining of advanced materials including titanium alloys and carbon fiber composites used in aerospace manufacturing.

Steel and alloy production accounts for roughly 20% of tungsten consumption, where the metal serves as an alloying agent that significantly enhances strength, hardness, and high-temperature performance. The aerospace sector particularly benefits from tungsten-rhenium superalloys in high-pressure turbine blades, where operating temperatures can reach 1,500°C or higher during normal flight operations.

Chemical and catalyst applications represent 13% of global tungsten demand, while lighting and electronics consume approximately 8% of production. Despite the decline in incandescent lighting due to LED adoption, tungsten's role in electronics has expanded significantly. In semiconductor manufacturing, tungsten serves as interconnects and vias in integrated circuits with feature sizes below 5 nanometers, where its low resistivity and thermal stability prove critical for device performance.

The remaining 9% of tungsten consumption includes specialised applications such as radiation shielding, where tungsten's high density provides superior protection compared to traditional lead shielding while requiring significantly less volume. Military and defence applications utilise tungsten alloys in armour-piercing projectiles, taking advantage of the metal's exceptional density and hardness characteristics.

When big ASX news breaks, our subscribers know first

China's Dominance and Global Supply Vulnerabilities

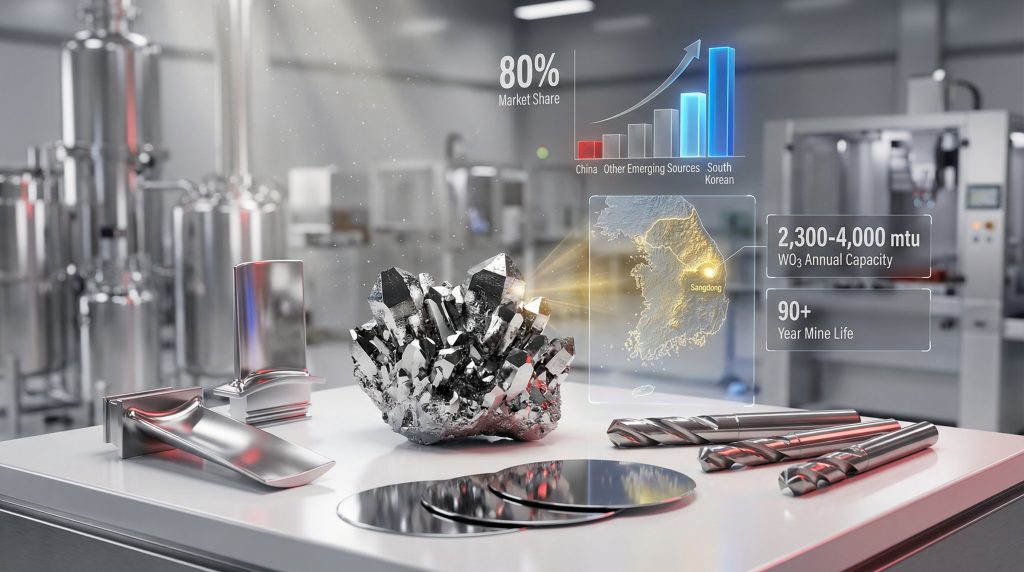

The global tungsten supply chain exhibits one of the highest concentration levels among critical minerals, with China controlling approximately 80-85% of refined tungsten production. This dominance extends far beyond raw material extraction to encompass the entire value chain, from mining through chemical processing, carbide tool manufacturing, and downstream applications.

Production Statistics and Market Control

China's tungsten production reached approximately 33,000-35,000 tonnes of tungsten metal equivalent in 2023, compared to total global production of roughly 41,000-42,000 tonnes. This production concentration is supported by China's control of approximately 60% of global identified tungsten reserves, estimated at 2.8-3.0 million tonnes of tungsten metal equivalent, primarily located in Hunan, Guangdong, and Jiangxi provinces.

The Shizhuyuan, Hehuachang, and Xihuashan mines in southern China represent the world's largest tungsten production concentration, with established transportation corridors, processing infrastructure, and export capabilities that create structural advantages over emerging suppliers. China exported approximately 18,000-20,000 tonnes of tungsten concentrate and refined products in 2023, representing roughly 50-60% of globally traded tungsten supply. This concentration raises significant concerns about critical minerals & energy security for Western nations.

Processing Infrastructure and Technical Advantages

China's market dominance becomes even more pronounced when examining processing capabilities. The country operates approximately 75% of global tungsten refining capacity, measured by APT (ammonium paratungstate) production capability. This represents processing capacity of approximately 30,000-32,000 tonnes annually, concentrated in Hunan, Jiangxi, and Guangdong provinces.

Chinese refineries have established proprietary processes for converting tungsten concentrate (WO₃) into technical-grade tungsten oxide and APT, which serves as the feedstock for downstream carbide production. These processes achieve 95-99% recovery rates with processing costs approximately 15-20% lower than Western refineries, creating significant competitive advantages beyond raw material access.

This processing dominance creates a strategic bottleneck where even non-Chinese tungsten concentrates frequently require shipment to China for refining into usable forms. Western hardmetal tool manufacturers, including those in Germany, Japan, and the United States, source 60-75% of refined tungsten from China, creating supply chain vulnerability to Chinese export policy changes or production disruptions.

South Korea's Strategic Mining Renaissance

The emergence of South Korea as a significant tungsten producer represents a fundamental shift in global supply chain dynamics. This development builds upon the country's historical mining capabilities while addressing contemporary strategic objectives related to supply chain resilience and critical mineral security.

Historical Context and Mining Legacy

South Korea operated significant tungsten mining operations through the 1990s, with the Sangdong mine and operations in the Taebaek Mountains region achieving peak production of approximately 4,000-5,000 tonnes annually during the 1970s-1980s. The Sangdong mine specifically achieved annual processing rates of approximately 2,000-2,500 tonnes WO₃ equivalent before ceasing primary operations in the mid-1990s.

The closure of Korean tungsten operations resulted from multiple factors including declining ore grades in easily accessible areas, depletion of high-grade surface deposits, and intense competition from lower-cost Chinese production. However, the underlying geological resources remained intact, setting the stage for renewed development under different economic and strategic conditions.

Geological Advantages and Resource Characteristics

The Sangdong deposit represents a metamorphic scheelite-type tungsten ore body with historical average grades of 0.45-0.50% WO₃. Scheelite deposits (calcium tungstate) offer significant technical advantages for underground mining compared to wolframite deposits (iron-manganese tungstate) common in China, as scheelite responds more effectively to flotation concentration methods and produces higher-purity concentrates.

The deposit's location at moderate depth (200-600 meters below surface) makes it suitable for conventional underground mining methods rather than open-pit extraction. Underground operations provide environmental footprint advantages relevant to South Korean regulatory frameworks, operational flexibility for managing geological variability, and longer mine life potential through multi-level extraction techniques. These characteristics provide valuable mineral deposit insights for understanding optimal extraction strategies.

Technical Specifications of the New Tungsten Mine in South Korea

The development of modern tungsten operations in South Korea incorporates advanced mining and processing technologies adapted to local geological and regulatory conditions. Almonty Industries (NASDAQ: ALM; ASX: AII), with a current market capitalisation of AUD $2.566 billion, has undertaken development of the Sangdong tungsten mine in Gangwon Province.

Production Capacity and Operational Specifications

The Sangdong operation targets annual production capacity of 2,300-4,000 metric tonnes of WO₃ equivalent, positioning it to capture 10-20% of non-Chinese tungsten supply once fully operational. The operation is designed around ore reserves grading 0.45-0.50% WO₃, with an estimated mine life exceeding 90 years based on current resource delineation.

| Operational Parameter | Specification | Strategic Significance |

|---|---|---|

| Annual Production Target | 2,300-4,000 mtu WO₃ | Meaningful supply diversification |

| Reserve Grade | 0.45-0.50% WO₃ | Above-average for global standards |

| Mine Life Estimate | 90+ years | Long-term supply security |

| Market Share Potential | 10-20% non-Chinese supply | Strategic alternative sourcing |

Underground Mining Methodology and Processing Systems

The Sangdong mine employs sublevel and longhole stoping methods, representing industry best practices for moderately deep vein deposits. These methodologies involve systematic drill and blast extraction of ore from sublevels, gravity-driven ore movement to lower collection points, and transport via conveyor or haulage systems to surface processing facilities.

The processing plant incorporates modern tungsten beneficiation technology including:

- Crushing and grinding circuits utilising jaw crushers, cone crushers, and ball mills to reduce ore to less than 200 mesh

- Flotation circuits employing sodium oleate or sodium fluoride collectors for scheelite separation

- Recovery systems designed to achieve 95-98% tungsten recovery rates on ore grades exceeding 0.3% WO₃

- Concentration stages producing tungsten concentrates at 65-75% WO₃ assay suitable for downstream refining

Quality control systems include X-ray fluorescence (XRF) analysis for real-time WO₃ assay verification, grade control sampling on 25-50 meter intervals within the mine, concentrate stockpile management ensuring consistent chemistry, and ISO 9001 and ISO 14001 certification frameworks for quality and environmental management compliance.

Market Impact and Supply Chain Implications

The introduction of significant Korean tungsten production creates multiple ripple effects throughout global supply chains, offering industrial consumers strategic alternatives to Chinese-dependent sourcing while potentially influencing pricing dynamics and market stability.

Supply Diversification Benefits

The new tungsten mine in South Korea addresses a critical vulnerability in Western industrial supply chains by providing a geographically and politically stable alternative to Chinese sources. This diversification becomes particularly valuable for industries with national security implications, including aerospace, defence, and advanced manufacturing sectors that require uninterrupted access to tungsten-based materials.

Risk reduction for industrial consumers extends beyond simple supply source multiplication. Korean tungsten production operates under established trade relationships with Western nations, transparent regulatory frameworks, and reliable logistics infrastructure. These factors reduce the types of supply disruption risks associated with geopolitically sensitive regions or countries with unpredictable export policies. In addition, almonty's tungsten supply chain leadership positions the company as a key player in this transformation.

Economic and Strategic Considerations

Regional economic impact from the new tungsten mine in South Korea includes direct employment creation in mining and processing operations, indirect employment through supporting services and infrastructure development, and export revenue generation for the Korean economy. The mining region benefits from infrastructure improvements including transportation, power, and communication systems that support broader economic development.

For South Korea specifically, domestic tungsten production aligns with broader strategic objectives related to critical mineral security and reduced dependence on Chinese supply chains. This represents part of a coordinated approach among OECD nations to establish reliable access to materials essential for advanced manufacturing and national defence applications. However, US-China trade impacts continue to influence global supply chain strategies.

Competitive Landscape and Global Context

The development of Korean tungsten production occurs within a broader context of efforts to establish non-Chinese sources of critical minerals. Understanding how the new tungsten mine in South Korea compares to other global projects provides insight into competitive positioning and strategic significance.

Alternative Non-Chinese Projects

Several other tungsten development projects are advancing globally, though most remain in earlier development stages compared to the Korean operations. Canada's Mactung project in Yukon Territory represents another significant non-Chinese tungsten initiative, though it faces challenges related to remote location, harsh climate conditions, and complex logistics requirements.

Australian tungsten projects, including various exploration and development initiatives, offer additional diversification potential but generally involve smaller-scale operations or face technical challenges that limit near-term production potential. European tungsten projects, particularly in Portugal and the United Kingdom, provide regional supply options but typically operate at scales significantly smaller than major Chinese producers.

Cost Competitiveness and Market Positioning

The new tungsten mine in South Korea benefits from several competitive advantages including:

- Established infrastructure reducing capital requirements for transportation and utilities

- Skilled workforce availability from Korea's industrial and mining experience

- Regulatory predictability providing clarity for long-term investment planning

- Geographic proximity to major Asian industrial consumers

Processing technology at Korean operations incorporates modern efficiency improvements that can achieve competitive production costs despite higher labour costs compared to Chinese operations. The focus on product quality and consistency may command premium pricing from industrial consumers valuing supply chain reliability over lowest-cost sourcing.

The next major ASX story will hit our subscribers first

Risk Factors and Development Challenges

Despite favourable geological and strategic positioning, the new tungsten mine in South Korea faces various operational, market, and financial challenges that could influence development timelines and ultimate success.

Technical and Operational Considerations

Underground mining complexity requires sophisticated ventilation systems, ground support methodologies, and safety protocols that increase operational complexity compared to surface mining alternatives. The Sangdong operation must achieve consistent ore grade control to maintain processing efficiency and concentrate quality standards required by downstream customers.

Processing efficiency optimisation represents an ongoing challenge, particularly in achieving target recovery rates while managing varying ore characteristics and maintaining environmental compliance standards. Korean environmental regulations require comprehensive waste rock management, mine water treatment to discharge standards, and post-closure land remediation planning that adds operational complexity and cost.

Market and Financial Risk Exposure

Tungsten price volatility exposes mining operations to significant revenue fluctuations that can impact project economics and investment returns. Historical tungsten pricing has demonstrated substantial volatility, with price swings of 50-100% occurring over relatively short timeframes based on Chinese production decisions, export policies, or global demand changes.

Capital intensity requirements for underground mining operations create exposure to construction cost inflation, equipment delays, and financing market conditions. The timeline from initial capital investment to full production typically spans multiple years, during which commodity price changes, cost inflation, or technical challenges can significantly impact project returns.

Competition from established Chinese suppliers remains a persistent challenge, particularly if Chinese producers respond to non-Chinese supply additions through pricing strategies or production adjustments designed to maintain market share.

Investment Implications and Strategic Opportunities

The development of the new tungsten mine in South Korea creates various investment themes and strategic opportunities for market participants, ranging from direct equity exposure to supply chain optimisation initiatives.

Portfolio Diversification and Critical Materials Exposure

Tungsten mining operations offer exposure to critical materials demand growth driven by advanced manufacturing, aerospace, and defence applications. Unlike many commodity sectors, tungsten demand demonstrates relatively stable long-term growth trends supported by technological advancement rather than cyclical economic patterns.

Investment in non-Chinese tungsten production provides geographic and political diversification benefits that may command valuation premiums as institutional investors increasingly focus on supply chain resilience and ESG considerations. Korean tungsten operations specifically offer exposure to stable regulatory environments and established trade relationships with Western markets.

Strategic Planning for Industrial Consumers

Long-term contracting opportunities with Korean tungsten producers enable industrial consumers to establish supply chain security while potentially capturing pricing advantages through advance commitments. These arrangements provide mutual benefits through revenue visibility for producers and supply certainty for consumers.

Technology partnership opportunities may emerge between Korean tungsten operations and downstream manufacturers seeking to optimise product specifications, develop new applications, or establish integrated supply chain relationships. Such partnerships can create competitive advantages through customised product development and preferential access to supply.

Future Outlook for Critical Materials Supply

The successful development of the new tungsten mine in South Korea establishes important precedents for critical mineral supply chain diversification and provides insights into broader strategies for managing resource security challenges.

Implications for Resource Security Strategy

The Korean tungsten development demonstrates that dormant mining projects can be successfully revived when strategic objectives align with favourable market conditions and adequate capital availability. This model may apply to other critical minerals where Western nations seek alternatives to concentrated supply sources.

Government policy support, including strategic mineral designations, tax incentives, and regulatory streamlining, proves essential for enabling economically viable development of non-Chinese critical mineral sources. The Korean example provides a template for public-private collaboration in establishing supply chain resilience.

Technology and Innovation Drivers

Research and development priorities in tungsten applications continue expanding, particularly in additive manufacturing, advanced composites, and next-generation semiconductor devices. These emerging applications may drive demand growth that supports multiple global production centres rather than continued concentration in Chinese facilities.

Recycling and circular economy opportunities in tungsten applications offer complementary approaches to supply diversification. Tungsten's high value and recyclability make recovery from end-of-life products economically attractive, particularly for countries with established manufacturing bases but limited primary production capabilities.

The new tungsten mine in South Korea represents more than a single mining project development. It symbolises a strategic shift toward supply chain resilience, demonstrates the viability of reviving dormant critical mineral operations, and provides a foundation for broader efforts to establish secure access to materials essential for advanced manufacturing and national security applications.

Please note: This analysis includes forward-looking statements and projections that involve uncertainties and risks. Commodity markets, mining operations, and geopolitical factors can significantly impact outcomes. Readers should conduct independent research and consult qualified financial advisors before making investment decisions related to critical materials or mining sector investments.

Ready to Capitalise on Critical Minerals Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant tungsten and critical minerals discoveries across the ASX, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 30-day free trial today and secure your market-leading advantage in the evolving critical materials sector.