May 15, 2026

The Structural Paradox at the Heart of North Africa's Phosphate Heartland

Across global agricultural systems, one mineral sits at the foundation of nearly every crop yield calculation: phosphate. Unlike nitrogen, which can be synthesised from atmospheric sources, phosphorus has no industrial substitute. It cannot be manufactured, replicated, or replaced. Every tonne of food produced at scale traces a direct dependency back to phosphate rock extraction, and that reality shapes the strategic importance of every producing nation, including those whose output has fallen dramatically from historical highs.

Tunisia's phosphate sector sits within this dependency framework in a position that is simultaneously privileged and precarious. The country holds an estimated 2.2% of global phosphate reserves, concentrated in the Gafsa basin in the country's interior. Those reserves are not the issue. The issue is whether the Tunisia phosphate industry revival can translate geological endowment into sustained, scalable production, given a set of institutional, social, and infrastructural constraints that have defined the sector's trajectory for more than a decade.

When big ASX news breaks, our subscribers know first

Why the Tunisia Phosphate Industry Revival Matters Well Beyond Its Own Borders

Phosphate's strategic significance has expanded beyond its traditional role in fertiliser supply chains. The mineral is now a key input in lithium iron phosphate (LFP) battery chemistry, a technology gaining rapid adoption across electric vehicle manufacturing and grid-scale energy storage. LFP batteries offer cost, safety, and longevity advantages over other lithium-ion chemistries, and their adoption trajectory means phosphate demand is no longer anchored solely to agricultural cycles.

Furthermore, the battery storage expansion driving LFP adoption has fundamentally altered the investment case for phosphate producers. Two converging demand forces are now reshaping that case worldwide:

- Fertiliser demand: Global population growth continues to drive sustained consumption of phosphate-based agricultural inputs, with no viable synthetic alternative at commercial scale.

- Energy transition demand: LFP battery technology is accelerating phosphate consumption in sectors entirely disconnected from agriculture, adding a new demand floor that did not exist a decade ago.

For Tunisia, these converging forces create both urgency and opportunity. The country's proximity to European agricultural markets, its relatively high-grade ore deposits, and its position along established Mediterranean trade routes represent genuine competitive advantages. However, those advantages are currently negated by a production base operating at less than half its historical peak capacity.

Where Tunisia Currently Stands

| Metric | Tunisia (2010 Peak) | Tunisia (2024/2025) | Tunisia (2030 Target) |

|---|---|---|---|

| Annual Output | ~8.2 million tonnes | ~3.04–3.9 million tonnes | 13.6–14 million tonnes |

| Global Ranking | 5th largest producer | ~10th globally | Top 5 (projected) |

| GDP Contribution | ~2%+ | Declining real value | Projected increase |

The government's 2030 production target would represent a 259% increase from 2024 output levels, exceeding the sector's pre-revolution peak by approximately 70%. This is not incremental recovery. It is transformational ambition.

From Peak to Trough: Understanding the Depth of Tunisia's Phosphate Decline

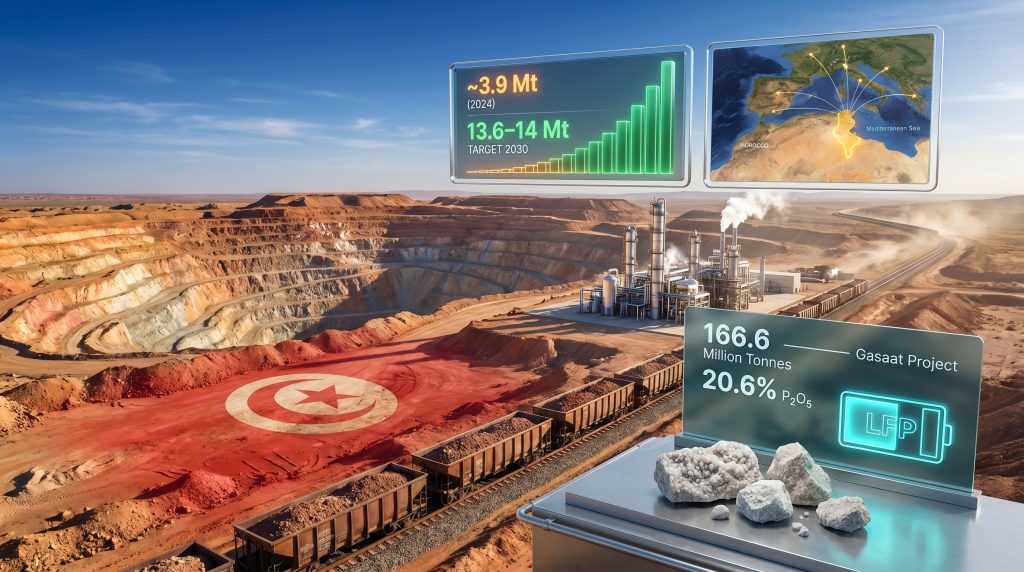

Tunisia's phosphate output reached 8.2 million tonnes in 2010, positioning the country among the world's top five producers. By 2024, output had fallen to approximately 3.04 million tonnes, a decline exceeding 63% across fourteen years. Understanding why this happened is essential for assessing whether the recovery trajectory initiated since 2023 can be sustained.

The collapse was not caused by resource depletion. The Gafsa basin's ore bodies remain largely intact. Instead, the decline reflects a compounding set of institutional and social failures:

- Chronic underinvestment in extraction and processing equipment, particularly from 2014 onward

- Recurring labour disruptions across the Mdhilla, Métlaoui, Redeyef, and Moularès mining districts

- An ageing rail wagon fleet that constrained ore transport capacity even during periods of stable extraction

- The absence of a coherent capital renewal programme within the state-owned operator, the Compagnie des Phosphates de Gafsa (CPG)

A partial recovery has been underway since 2023. CPG's director general, Abdelkader Amidi, confirmed that output reached 3.9 million tonnes in 2025, up from 3.04 million tonnes in 2024. That improvement is meaningful but modest relative to the scale of the 2030 ambition.

The Gafsa Basin: A Geography of Unresolved Grievance

The mining communities surrounding Gafsa carry a political history that cannot be separated from the sector's operational present. A major social uprising in the Gafsa basin in 2008 centred on demands for employment equity, local revenue sharing, and regional economic justice. The movement was suppressed by the government of President Zine El Abidine Ben Ali, but the underlying conditions it expressed remained unresolved.

Many analysts regard the 2008 Gafsa uprising as a direct precursor to Tunisia's 2011 revolution, occurring three years before the broader Arab Spring movement took hold. The significance of this history for investors and policymakers lies in its structural persistence. The grievances that animated the 2008 uprising were not addressed through reform. They were deferred through suppression, and deferred grievances in resource-dependent communities do not disappear. They resurface, repeatedly, as the Tunisian phosphate sector has demonstrated across every subsequent year of attempted recovery.

The Architecture of Tunisia's Five-Year Phosphate Recovery Plan

Tunisia's government has approved a comprehensive modernisation framework targeting near-quadrupled national phosphate output by 2030. The strategy operates across four interconnected pillars that must advance simultaneously to achieve the stated targets.

1. Extraction Expansion

- New production authorisation at Meknassy, targeting 600,000 tonnes per year

- Development of Oum Lakhecheb with potential output of 2.4 million tonnes per year

- Long-term advancement of Sra Ouertane targeting 4 million tonnes per year

- Progression of Tozeur-Nefta and M'dhilla facilities

2. Processing Infrastructure Upgrades

- Modernisation of the Gabès Chemical Complex, focused on fine phosphate and diammonium phosphate (DAP) production

- Expansion of phosphoric acid output capacity to support downstream fertiliser manufacturing

- Environmental upgrades at processing facilities, including emission controls at coastal industrial zones

3. Transport Network Rehabilitation

- Railway corridor modernisation connecting Gafsa basin mining districts to processing and export hubs

- A parliamentary-approved loan of 16 million Kuwaiti dinars (approximately $52 million USD) from the Arab Fund for Economic and Social Development, ratified in April 2026

- Rail wagon fleet renewal, explicitly identified by CPG's director general as a critical bottleneck constraining production even when extraction activity is stable

4. Water and Environmental Compliance

- Water infrastructure upgrades to support expanded extraction operations

- Emission reduction programmes at Gabès, where community opposition to industrial pollution has created recurring operational risks

Who Is Financing the Recovery?

| Funding Source | Commitment Period | Estimated Contribution | Designated Purpose |

|---|---|---|---|

| Saudi Fund for Development | 2024 | Portion of ~$171M total | Modernisation programme |

| Kuwait Fund for Arab Economic Development | 2025 | Portion of ~$171M total | Modernisation programme |

| Arab Fund for Economic & Social Development | April 2026 | ~$52M (16M KD) | Railway rehabilitation |

| Total Renovation Programme | 2024–2026 | Infrastructure and equipment |

A critical caveat applies to this financing picture. Speaking before Tunisia's parliament, CPG's director general acknowledged that loan tranches mobilised in recent years did not generate the operational improvements that had been anticipated. This is not simply a capital availability problem. It points to a capital deployment and governance challenge within the state enterprise, where financing has been secured but not translated into proportional operational gains.

Private Capital Entering Tunisia's Phosphate Basin

Alongside the state-led recovery framework, private investors are advancing into phosphate exploration across the Gafsa region and beyond. This mirrors broader trends in phosphate project development seen globally, where private capital is increasingly willing to enter markets once dominated by state operators. CPG has issued a three-year exploration licence in the Gafsa region, signalling a measured openness to expanded prospecting activity from non-state actors.

The most advanced foreign entrant is Australian company PhosCo, whose Gasaat phosphate project has emerged as a significant discovery. In May 2026, PhosCo announced two new deposits at Gasaat, elevating the project's total estimated resources to 166.6 million tonnes at an average grade of 20.6% phosphorus pentoxide (P₂O₅). The project parameters are substantial:

- Proposed production rate: 1.5 million tonnes per year

- Projected mine life: 46 years

- Capital expenditure estimate: $169.5 million USD

- Capital raising underway: A$5 million to fund a bankable feasibility study

A grade of 20.6% P₂O₅ is worth examining in technical context. Phosphate ore is typically processed and valued based on its P₂O₅ content, which represents the usable phosphorus compound extracted from the rock. Grades above 20% are considered commercially attractive for direct processing into phosphoric acid and downstream fertiliser products, reducing beneficiation costs and improving project economics. The Gasaat grade sits comfortably within the range that supports viable commercial development, particularly given the project's proximity to established Tunisian processing infrastructure.

Disclaimer: PhosCo's resource estimates and project economics are based on the company's own exploration results and feasibility assessments. These figures are subject to revision as additional drilling and engineering studies are completed. Resource estimates do not guarantee future production, and investors should treat project development timelines as indicative rather than confirmed.

Scenario Analysis: Private Sector Contribution to 2030 Targets

| Scenario | Private Sector Output by 2030 | Total Industry Output | Gap to 14Mt Target |

|---|---|---|---|

| Base Case | ~2–3 Mt/yr | ~11–12 Mt/yr | 2–3 Mt shortfall |

| Optimistic Case | ~4–5 Mt/yr | ~13–14 Mt/yr | Near target achieved |

| Downside Case | Under 1 Mt/yr | ~7–8 Mt/yr | 6–7 Mt shortfall |

Three Structural Fault Lines Threatening the Recovery Trajectory

The Tunisia phosphate industry revival faces obstacles that financing alone cannot resolve. Three fault lines sit beneath the surface of every recovery projection, and understanding them is essential for any serious assessment of the sector's trajectory.

Fault Line One: The Unresolved Social Contract in Gafsa

Labour unrest at CPG is not episodic in character. It is structurally embedded in the political economy of the Gafsa region. A strike launched on May 12, 2026 across the Mdhilla and Métlaoui districts, subsequently spreading to Redeyef and Moularès, was triggered by a dispute over the bonus payment associated with the Muslim feast of Eid al-Adha. The immediate trigger was routine. The structural conditions enabling it are not.

Former Industry and Energy Minister Slim Feriani stated in 2019 that protest-related disruptions were costing CPG approximately $1 billion per year in lost production value. That figure reflects the true operational cost of the social contract deficit in Gafsa, where unemployment rates and per-capita public investment levels rank among Tunisia's worst, and where the practice of absorbing surplus workers into CPG's payroll as a social stabilisation mechanism has created a financially unsustainable employment model.

The same workforce that CPG depends on for production recovery is also the constituency most likely to resist the efficiency-focused restructuring that financial sustainability demands. This tension is not resolvable through capital investment alone.

Fault Line Two: Institutional Fragility at CPG

CPG's governance and financial management challenges represent a distinct obstacle layer. The acknowledgment before parliament that previous loan disbursements had not generated expected operational improvements is a significant admission. It suggests that the barrier to recovery at CPG is not primarily a lack of funding. It is a capital absorption and deployment problem rooted in institutional capacity constraints.

Equipment ageing across extraction, processing, and transport functions has proceeded without systematic remediation. The rail wagon fleet, repeatedly cited as a critical logistics bottleneck, exemplifies an infrastructure problem that requires not just procurement but sustained maintenance regimes and operational governance that CPG has historically struggled to sustain. Consequently, the mining industry consolidation pressures visible globally may ultimately accelerate the structural reforms CPG requires.

Fault Line Three: Environmental Pressure at Gabès

The Gabès Chemical Complex occupies a central role in Tunisia's phosphate processing and export capacity, but it operates in a coastal environment where community opposition to industrial pollution has periodically disrupted operations. Phosphogypsum waste management and atmospheric emission controls represent both operational compliance requirements and community relations challenges. The recovery plan's environmental upgrade commitments are necessary, but implementation timelines remain uncertain and community tolerance for continued pollution during a transition period is not guaranteed.

The next major ASX story will hit our subscribers first

Benchmarking Tunisia Against Global Phosphate Producers

| Country | 2023 Output (Mt) | Key Competitive Advantage | Primary Risk Factor |

|---|---|---|---|

| Morocco | ~40 Mt | OCP Group's vertically integrated model | Export concentration |

| China | ~85 Mt | Domestic demand absorption | Environmental regulation tightening |

| Egypt | ~5–6 Mt | Mediterranean market proximity | Infrastructure constraints |

| Tunisia | ~3.9 Mt | High-grade deposits, EU market proximity | Social instability, ageing infrastructure |

| Jordan | ~9 Mt | Established export relationships | Water scarcity |

Tunisia's competitive positioning within this peer group reveals a clear pattern: the country possesses genuine natural advantages that peer producers in the region cannot easily replicate. However, those advantages are currently undermined by production unreliability and institutional constraints that Morocco, China, and Jordan do not face at comparable severity. The gap between Tunisia's resource endowment and its production performance is fundamentally a governance gap, not a geology gap.

In addition, the emerging battery raw materials market dynamics mean that closing this governance gap carries even greater long-term value than historical fertiliser pricing alone would suggest.

Three Trajectories for Tunisia's Phosphate Sector by 2030

Scenario A: Managed Transition (Most Probable)

CPG reaches 6–8 million tonnes by 2030 through incremental infrastructure improvements. Private sector entrants including PhosCo add 1.5–2.5 million tonnes. Social unrest is managed through targeted community investment but not structurally resolved. Export revenues increase substantially but fall short of fiscal transformation targets.

Scenario B: Accelerated Transformation (Optimistic)

Full deployment of committed financing generates rapid infrastructure upgrades. CPG achieves 10–11 million tonnes through operational restructuring and new site development. PhosCo and additional foreign entrants contribute 3–4 million tonnes collectively. Social compact reforms reduce strike frequency materially. Total output approaches 13–14 million tonnes by 2030–2031.

Scenario C: Structural Stagnation (Downside)

Escalating labour disputes and financing deployment failures constrain CPG output below 5 million tonnes. Private sector investment stalls amid permitting uncertainty and social risk. Total output plateaus at 5–6 million tonnes. Tunisia's fiscal position deteriorates further, reducing capacity for corrective investment and deepening the reform deficit.

Disclaimer: The scenario projections presented above are analytical frameworks based on publicly available data and structural assessments. They do not constitute investment advice or production forecasts. Outcomes will depend on political, social, operational, and macroeconomic variables that cannot be predicted with precision.

What a Genuine Recovery Requires: Conditions That Cannot Be Negotiated Away

For the Tunisia phosphate industry revival to transition from policy ambition to operational reality, several conditions must be met concurrently rather than sequentially:

- Governance reform at CPG: Improving capital deployment efficiency and financial management so that loan proceeds translate into proportional operational improvements

- Social compact development: Moving beyond workforce absorption as a stability mechanism toward genuine community investment and revenue-sharing frameworks in Gafsa

- Infrastructure execution: Completing railway rehabilitation and Gabès processing upgrades within committed timelines

- Private sector integration: Creating a regulatory environment that enables foreign and domestic explorers to advance toward production

- Environmental compliance: Resolving the Gabès pollution challenge in a manner that maintains community support for continued operations

Tunisia's phosphate challenge mirrors a broader pattern visible across resource-dependent economies throughout Africa: extraction wealth has not consistently translated into equitable regional development, and the communities bearing the environmental and social costs of extraction are frequently the same communities least rewarded by its proceeds. Resolving that asymmetry in the Gafsa context is not peripheral to the recovery plan. It is the recovery plan's most fundamental prerequisite.

Tunisia possesses the resource base, the geographic positioning, and increasingly the financing architecture to reclaim a meaningful position in global phosphate supply. What the sector currently lacks is not capital or ore. It is the institutional coherence and social legitimacy to deploy both at the scale that the 2030 targets demand.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across phosphate, battery materials, and over 30 other commodities — instantly translating complex geological data into actionable investment insights. Explore how historic mineral discoveries have generated exceptional returns and begin your 14-day free trial today to position yourself ahead of the broader market.