July 21, 2026

The global landscape of critical mineral supply chains is undergoing a fundamental transformation, driven by emerging geopolitical tensions and national security imperatives. Countries worldwide are reassessing their dependencies on concentrated supply sources, particularly in the rare earth elements sector where single-nation dominance has created systemic vulnerabilities for defense contractors, automotive manufacturers, and clean energy infrastructure developers.

This strategic shift toward supply chain resilience has catalysed unprecedented investment flows into domestic mineral extraction, processing, and manufacturing capabilities. The U.S. mine-to-magnet supply chain development represents one of the most comprehensive industrial policy initiatives in recent decades, encompassing extraction facilities, separation technologies, and permanent magnet manufacturing across multiple states.

The convergence of policy incentives, private capital deployment, and technological innovation is creating new pathways for domestic rare earth value creation that could fundamentally alter global market dynamics by 2030.

National Security Imperatives Drive Supply Chain Transformation

Defence procurement regulations scheduled for implementation in January 2027 will prohibit the use of Chinese-origin rare earth magnets in U.S. weapons systems, creating an urgent timeline for domestic alternative development. This regulatory framework affects critical defence platforms including missile guidance systems, radar installations, and advanced propulsion technologies that rely on high-performance permanent magnets.

The strategic vulnerability stems from China's control of approximately 80-85% of global rare earth separation capacity as of 2024, according to U.S. Geological Survey assessments. This concentration creates single-point-of-failure risks in supply chains supporting national defence infrastructure.

Key defence applications requiring rare earth magnets include:

• Precision-guided munitions and smart weapon systems

• Electronic warfare and communications equipment

• Submarine propulsion and naval vessel systems

• Satellite technology and space-based defence platforms

The Department of Defence has identified rare earth permanent magnets as among the most critical materials for maintaining technological superiority in advanced weapons systems. Current military specifications (MIL-SPEC) require magnet performance standards that historically only established suppliers have been able to meet at scale.

When big ASX news breaks, our subscribers know first

Economic Competitiveness Through Trade Policy Coordination

Implementation of a 25% tariff on Chinese rare earth imports beginning in 2026 represents a significant shift in trade policy designed to level competitive dynamics between domestic and foreign suppliers. This tariff structure aims to offset the cost advantages Chinese manufacturers derive from government subsidies estimated at 20-30% of production costs for state-owned enterprises.

Furthermore, the mining permits policy supports streamlined approval processes for domestic facilities. The economic rationale extends beyond simple trade protection to encompass long-term industrial competitiveness.

Chinese rare earth processors benefit from several structural advantages:

• Three decades of accumulated processing expertise and operational knowledge

• Massive scale economies across integrated extraction and separation facilities

• Lower regulatory compliance costs compared to U.S. environmental and safety standards

• Coordinated supply chain integration spanning mining through finished magnet production

Federal coordination across multiple agencies has resulted in over $1.4 billion in committed funding through various programmes including the Defense Production Act, Inflation Reduction Act incentives, and specialised loan guarantee programmes. This represents the largest peacetime industrial mobilisation effort for critical minerals in U.S. history.

Domestic Extraction Capabilities Establish Supply Foundation

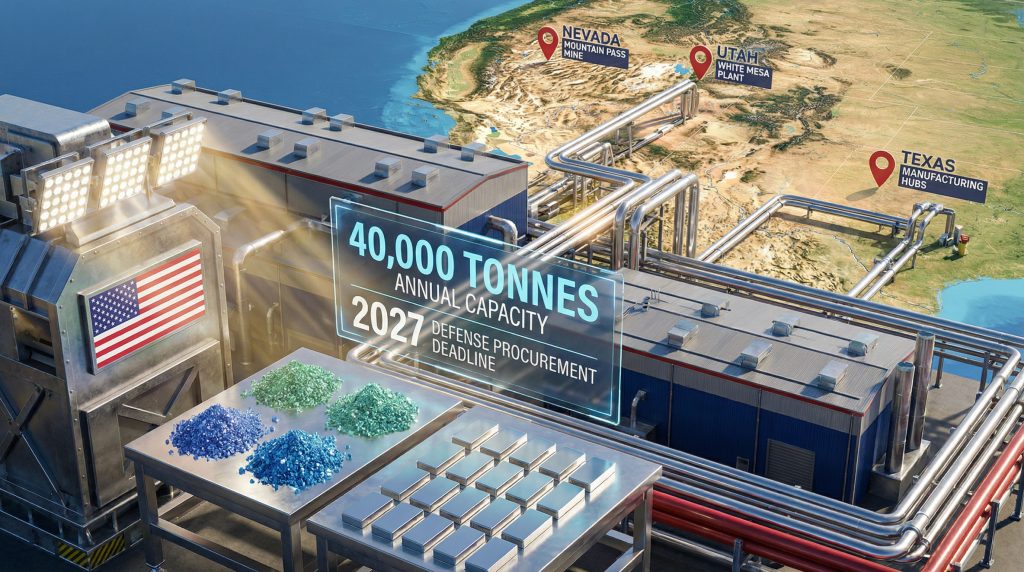

Mountain Pass Operations in Nevada serves as the cornerstone of domestic rare earth extraction, with annual production capacity exceeding 40,000 tonnes of rare earth concentrate. The facility, operated by MP Materials Corporation, represents the only large-scale rare earth mining operation currently operational in the United States.

The Mountain Pass deposit contains carbonatite ore with rare earth oxide concentrations significantly higher than typical global averages. Processing capabilities include:

• Acid leaching systems for ore dissolution and concentration

• Solvent extraction cascades for element separation

• Precipitation and calcination facilities for oxide production

• Planned expansion to integrated metal production capabilities

Energy Fuels' White Mesa facility in Utah provides complementary processing capabilities focused on heavy rare earth elements. The facility became operational in 2024 with capacity to process over 2,000 tonnes annually of dysprosium, terbium, and other critical materials essential for high-temperature magnet applications.

| Facility | Location | Annual Capacity | Primary Focus | Operational Status |

|---|---|---|---|---|

| Mountain Pass | Nevada | 40,000+ tonnes concentrate | Light rare earths (NdPr) | Operational since 2018 |

| White Mesa | Utah | 2,000+ tonnes separated oxides | Heavy rare earths | Operational 2024 |

| Planned Ohio facility | Ohio | 8,000+ tonnes metal production | Integrated processing | Development phase |

Advanced Processing Infrastructure Enables Value Creation

The separation and refining stage represents the most technically challenging and capital-intensive component of the U.S. mine-to-magnet supply chain. Unlike raw material extraction, separation requires specialised chemistry expertise, environmental management systems for acidic waste streams, and precision process control to achieve 99.9%+ purity requirements for magnet applications.

MP Materials' Texas operations focus on neodymium-praseodymium (NdPr) separation, the primary materials used in permanent magnet production. The facility utilises multi-stage solvent extraction processes that require precise control of:

• Extraction kinetics and selectivity parameters

• Temperature and pH management across processing stages

• Solvent recovery and recycling systems

• Quality assurance protocols for defence contractor specifications

Heavy rare earth processing at the White Mesa facility addresses a critical supply gap, as these materials provide high-temperature coercivity essential for military and aerospace applications. However, AI in mining operations is increasingly being explored to optimise these complex processes. The facility processes co-products including thorium and uranium that require specialised radioactive material handling capabilities.

Technical Challenge: Rare earth separation typically requires 5-7 stage extraction cascades with precise control of chemical parameters. Process optimisation through advanced instrumentation and control systems can reduce both operating costs and environmental waste generation.

Manufacturing Capabilities Scale Toward Market Requirements

Vulcan Elements' North Carolina facility represents one of the first large-scale permanent magnet manufacturing operations designed to utilise domestic rare earth feedstock. The facility targets 3,000+ tonnes annual production capacity with specific focus on automotive and defence applications.

Permanent magnet manufacturing involves complex metallurgical processes including:

-

Metal reduction from oxide feedstock using calcium or other reducing agents

-

Alloy preparation through controlled atmosphere melting (vacuum or inert gas)

-

Hydrogen decrepitation to create fine powder with optimal particle size distribution

-

Magnetic field alignment during powder pressing to maximise energy product

-

Sintering at 1,000-1,200°C for densification and grain structure development

-

Ageing heat treatment to develop coercivity and thermal stability

MP Materials' integrated Texas operations combine separation and magnet production capabilities, targeting 10,000+ tonnes annual capacity by 2027. This vertical integration eliminates intermediate transportation and handling steps whilst optimising material specifications for specific end-use requirements.

The facility's General Motors supply agreement demonstrates commercial validation for domestic magnet production in electric vehicle applications, where performance requirements include:

• Magnetic strength (remanence) of 1.3-1.4 Tesla for NdFeB compositions

• Coercivity resistance to demagnetisation at elevated temperatures

• Dimensional stability and corrosion resistance for automotive environments

Federal Investment Programmes Accelerate Development

Multiple federal funding mechanisms provide financial support for U.S. mine-to-magnet supply chain development, with coordination across defence, energy, and commerce departments to maximise strategic impact. In addition, the critical minerals strategy provides comprehensive policy direction for these initiatives.

| Programme | Funding Allocation | Focus Area | Implementation Timeline |

|---|---|---|---|

| Defense Production Act | $500+ million | Critical mineral processing and stockpiling | 2024-2027 |

| Inflation Reduction Act | $400+ million | Manufacturing tax credits and incentives | 2023-2030 |

| CHIPS Act Integration | $300+ million | Technology development and R&D | 2024-2028 |

| DOE Loan Programmes | $200+ million | Infrastructure and facility development | 2023-2026 |

Defense Production Act funding specifically targets supply chain bottlenecks through direct government investment in processing capabilities. This includes loan guarantees, purchase agreements, and cost-sharing arrangements that reduce private sector investment risk for strategic facilities.

The Inflation Reduction Act provides production tax credits equivalent to 30% of magnet material costs for qualifying electric vehicle manufacturers sourcing from domestic suppliers. This demand-side incentive creates market pull for domestic rare earth production whilst supporting clean energy infrastructure goals.

CHIPS Act provisions extend beyond semiconductor applications to include critical mineral processing technologies. Research and development funding supports advanced separation techniques, recycling technologies, and process automation that could provide competitive advantages over established foreign suppliers.

The next major ASX story will hit our subscribers first

Private Capital Deployment Validates Commercial Opportunity

Strategic equity investments exceeding $100 million per major project demonstrate private sector confidence in domestic rare earth market development. Institutional investors including pension funds, sovereign wealth funds, and specialised commodity investment vehicles are participating in facility development across multiple states.

Corporate partnership agreements provide demand certainty for domestic producers through long-term supply contracts. Major automotive manufacturers, defence contractors, and wind turbine producers are signing multi-year agreements that guarantee minimum purchase volumes in exchange for supply security.

Key investment characteristics include:

• 10-15 year contract terms providing revenue visibility for project financing

• Price escalation mechanisms tied to commodity indices and inflation adjustments

• Performance guarantees for magnet specifications and delivery schedules

• Force majeure protections for supply disruption scenarios

Public-private partnerships leverage government funding with private sector expertise and capital. This hybrid financing approach reduces development risk whilst accelerating facility construction timelines compared to purely private or government-funded approaches. Furthermore, mining investment strategies are evolving to support these strategic initiatives.

Regulatory Framework Evolution Supports Strategic Goals

Defence acquisition regulation changes taking effect in 2027 will require complete supply chain transparency for rare earth magnets used in weapons systems. Contractors must demonstrate domestic sourcing or approved allied nation supply for all permanent magnet components in defence platforms.

The regulatory framework includes:

• Supply chain verification protocols requiring documentation of material origin through the entire processing chain

• Performance certification requirements ensuring domestic magnets meet or exceed specifications for replaced foreign components

• Qualification testing procedures that may require 12-24 months for new supplier approval

• Stockpiling requirements for critical defence applications to ensure supply continuity

Export control coordination with allied nations creates preferential trade relationships for critical mineral supply chains. This includes expedited licensing procedures for rare earth exports between trusted partners and information sharing agreements on supply chain security.

Market Dynamics and Competitive Positioning

Cost competitiveness remains the primary challenge for domestic rare earth producers competing against established Chinese suppliers. Current production costs for U.S. facilities range from $15,000-$25,000 per tonne of separated oxides compared to $8,000-$12,000 per tonne for mature Chinese operations.

Several factors contribute to this cost differential:

• Scale economies: Chinese facilities operate at 10-50 times the capacity of initial U.S. operations

• Labour costs: Manufacturing labour costs in China remain 40-60% lower than U.S. levels

• Environmental compliance: U.S. environmental regulations add $2,000-$4,000 per tonne in compliance costs

• Learning curve effects: Chinese processors benefit from three decades of operational optimisation

Strategic Consideration: While cost competitiveness remains challenging, supply security premiums and policy support mechanisms can offset 15-25% cost differentials for strategic applications, particularly in defence and critical infrastructure sectors.

Quality consistency across large-scale production runs represents another critical challenge. Defence contractors require statistical process control demonstrating consistent magnet performance across thousands of units, necessitating sophisticated quality management systems throughout the supply chain.

How Do Cost Dynamics Affect Market Viability?

The cost competitiveness challenge is further complicated by U.S. economic policies that influence exchange rates and manufacturing costs. However, strategic considerations may justify premium pricing for supply security benefits.

Technology Innovation and Competitive Advantages

Advanced recycling capabilities offer potential cost advantages and supply security benefits for domestic producers. Rare earth magnet recycling can recover 85-95% of rare earth content from end-of-life electric vehicle motors, wind turbines, and electronic devices.

Current recycling economics show:

• Recovery costs of $12,000-$18,000 per tonne of rare earth oxides

• Material quality equivalent to primary production for most applications

• Supply security independent of mining operations and geopolitical risks

• Environmental benefits through reduced mining and processing waste

Process automation and artificial intelligence applications in rare earth processing remain in early development stages. Potential applications include:

• Real-time optimisation of solvent extraction parameters

• Predictive maintenance for complex chemical processing equipment

• Quality control automation reducing manual testing requirements

• Yield optimisation through machine learning algorithms

However, documented commercial-scale implementations of AI-driven cost reductions in rare earth processing are limited as of 2025. Additionally, critical supply chain analysis suggests that technological innovation will be crucial for long-term competitiveness.

Production Targets and Timeline Projections

Domestic U.S. mine-to-magnet supply chain capacity targets for 2030 reflect ambitious scaling goals across extraction, processing, and manufacturing stages:

Projected Annual Production Capacity:

• Rare earth concentrate: 60,000+ tonnes domestic extraction capacity

• Separated oxides: 25,000+ tonnes processing capability

• Finished permanent magnets: 15,000+ tonnes manufacturing capacity

• Recycled rare earth materials: 5,000+ tonnes from domestic recycling operations

These capacity targets would provide:

• Complete defence supply security for permanent magnet requirements

• 30%+ of U.S. automotive magnet demand for electric vehicle production

• Significant export capability to allied nations for supply chain diversification

Economic Impact and Regional Development

Facility construction and operation is projected to create over 10,000 direct jobs in rare earth extraction, processing, and manufacturing by 2030. These positions typically offer wages 25-40% above regional manufacturing averages due to specialised technical requirements.

Regional economic multiplier effects include:

• Construction employment during 3-5 year facility development phases

• Support services including maintenance, logistics, and professional services

• Supplier network development for specialised equipment and materials

• Tax revenue generation for local and state governments

States benefiting from rare earth industry development include Nevada, Utah, Texas, North Carolina, and Ohio, with additional exploration and development activity in Wyoming, Colorado, and Montana. Moreover, supply chain developments are creating new opportunities across multiple regions.

Investment Strategy and Risk Assessment

Vertical integration strategies offer the highest potential returns for investors capable of controlling multiple supply chain stages. Companies operating both processing and manufacturing facilities can optimise material specifications, reduce transportation costs, and capture greater value-added margins.

Key investment evaluation criteria:

• Government partnership strength through funding agreements and procurement contracts

• Technology differentiation in processing efficiency or product performance

• Customer contract portfolio providing revenue visibility and demand certainty

• Management execution capability for complex industrial project development

Principal investment risks include:

• Construction and commissioning delays affecting project timelines and costs

• Market demand fluctuations if EV adoption or defence spending patterns change

• Competition from established suppliers potentially reducing market prices

• Regulatory or policy changes affecting government support programmes

Investment Consideration: The domestic rare earth supply chain development represents a strategic transformation requiring patient capital and long-term investment horizons. Success depends on coordinated execution across multiple facility types and sustained government policy support.

Disclaimer: This analysis is for educational purposes only and should not be construed as investment advice. Rare earth supply chain development involves significant technical, market, and regulatory risks that require thorough due diligence and professional consultation before making investment decisions. Future projections are subject to change based on market conditions, policy developments, and technological advances.

Want to Discover the Next Major Mineral Investment Opportunity?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities in the critical minerals sector ahead of the broader market. Explore why major mineral discoveries can lead to substantial returns and begin your 30-day free trial today to position yourself at the forefront of Australia's mining investment landscape.