July 31, 2026

When Production Ambition Outgrows Institutional Loyalty

For most of the twentieth century, the architecture of global oil markets rested on a simple premise: producers benefit more from collective price discipline than from unconstrained volume competition. That logic held together an alliance of nations with often competing interests, diverse fiscal requirements, and wildly different production costs. It held, that is, until the gap between what a member could produce and what the cartel permitted it to produce became too wide to ignore.

The UAE's exit from OPEC and OPEC+ is best understood through this lens. It is not a diplomatic rupture or an ideological break. It is the outcome of a sovereign calculus that quietly shifted over many years, then crystallised under the pressure of regional conflict, infrastructure investment, and long-range demand forecasting. The UAE exit from OPEC represents one of the most consequential structural changes to global oil governance in decades, and its implications stretch well beyond Abu Dhabi's production targets.

When big ASX news breaks, our subscribers know first

Nearly Six Decades of Membership, Then a Clean Break

The UAE became an OPEC member in 1967, embedding itself within a collective bargaining framework that would come to define Middle Eastern energy geopolitics for generations. For most of that period, membership delivered real benefits: coordinated price floors, quota systems that stabilised revenue forecasting, and multilateral credibility in dealings with consuming nations and international energy institutions.

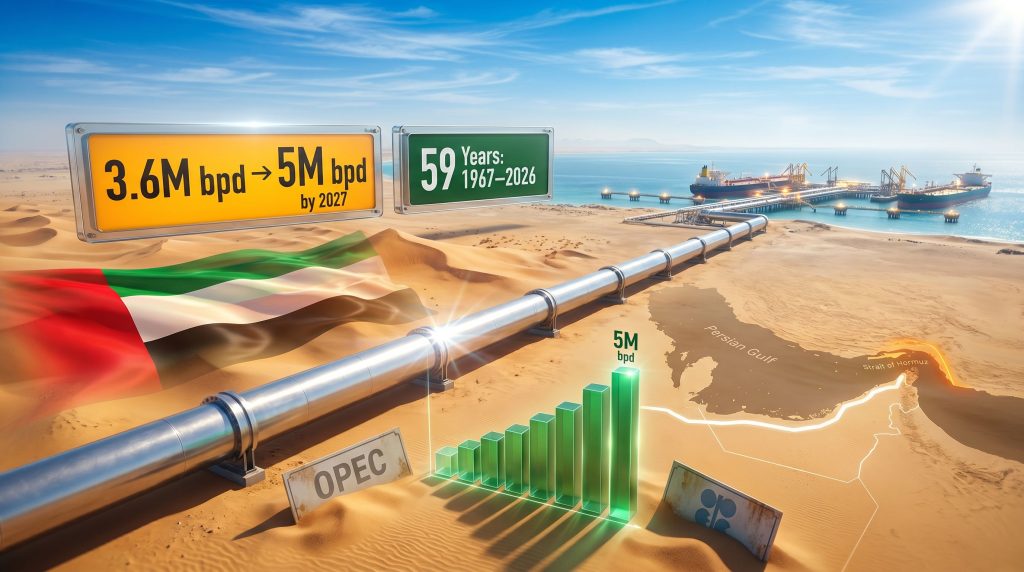

The exit from both OPEC and OPEC+, effective May 1, 2026, ended that 59-year institutional relationship. What makes this departure categorically different from previous member exits is the scale of what the UAE brings to global supply calculations. As OPEC's third-largest producer behind Saudi Arabia and Iraq, Abu Dhabi is not a peripheral voice leaving the room. It is one of the primary anchors of the cartel's collective output weight, and its absence changes the fundamental mathematics of how OPEC can credibly claim to manage global supply.

Reuters reports that the UAE's departure is not comparable to Qatar's 2019 exit, which involved a comparatively modest oil production base. The UAE's removal from OPEC's official membership base strips the cartel of a producer with both the capacity and the infrastructure to act independently at scale.

Four Structural Forces Behind the Decision

Quota Architecture Versus Upstream Capacity

The UAE has invested heavily in expanding its upstream oil infrastructure over the past decade. That investment created a structural contradiction: production capacity that had been built and paid for, but which quota obligations prevented Abu Dhabi from fully deploying to market. For a national energy strategy oriented around maximising the value of proven reserves before global demand peaks, this constraint represented a growing opportunity cost.

Exiting OPEC removes the ceiling. With a stated production ambition of reaching up to 5 million barrels per day by 2027 from a pre-conflict baseline of approximately 3.6 million barrels per day, the scale of Abu Dhabi's intended output expansion becomes clear. That represents a targeted increase of roughly 39% above pre-conflict production levels, a trajectory that is simply incompatible with cartel quota discipline. Furthermore, crude oil price trends in recent years have reinforced Abu Dhabi's conviction that acting independently offers greater long-term fiscal returns.

Regional Conflict and Collective Security Disillusionment

The February 2026 military conflict involving the US, Israel, and Iran introduced a new variable into Abu Dhabi's strategic calculus. OPEC's architecture was never designed as a collective security framework, but the conflict exposed a related question: whether remaining inside an institution led in part by a regional power whose interests do not perfectly align with your own still makes sense when geopolitical stress arrives.

Reports of friction between the UAE and Saudi Arabia over the handling of the conflict period added a political dimension to what had previously been primarily an economic disagreement over quota allocation. Strategic divergence at the bilateral level inevitably weakens the logic of institutional alignment. In addition, concerns over regional energy security have become increasingly prominent across the broader Indo-Pacific energy landscape, adding further context to how nations are repositioning their energy strategies.

The Hormuz Bypass as a Strategic Liberation Asset

Perhaps the most underappreciated element of the UAE's post-OPEC strategy is its physical infrastructure independence from the Strait of Hormuz. The Abu Dhabi Crude Oil Pipeline, stretching approximately 249 miles from Abu Dhabi's oil fields to the Gulf of Oman, allows the UAE to export oil entirely outside the Hormuz chokepoint.

This matters enormously in the current environment. During periods of Hormuz disruption, most Persian Gulf producers face direct exposure to supply route interruption. The UAE does not. Its export capability remains intact regardless of what happens in the strait, reducing both its physical vulnerability and its dependence on collective negotiating positions around Persian Gulf access rights.

- Key advantage: Hormuz-independent export capability at scale

- Pipeline length: ~249 miles, connecting Abu Dhabi fields to the Gulf of Oman

- Strategic outcome: Export continuity during regional conflict, regardless of OPEC collective posture

The Long-Duration Demand Bet

Underlying all of this is a conviction that global oil demand, particularly from emerging markets across Asia and Africa, will remain robust for longer than Western energy transition narratives suggest. If that assessment proves correct, the producer with the lowest extraction costs, the highest spare capacity, and the most flexible export infrastructure wins a volume competition. That competition is best pursued outside a quota framework designed to restrict volume in the interest of price.

How OPEC Has Responded

UAE Energy Minister Suhail Al Mazrouei confirmed at the Make It In The Emirates conference on May 4, 2026, that OPEC's institutional response to the UAE's departure had been measured and constructive, with the organisation broadly accepting the decision without antagonism. He further indicated that the UAE intends to maintain active working relationships with individual member states within both OPEC and OPEC+, framing the exit as a commercial reorientation rather than a hostile departure.

ADNOC's leadership has similarly characterised the decision as one directed at Abu Dhabi's own strategic interests rather than against any specific member or the organisation itself. This diplomatic framing matters because it preserves the bilateral relationships that underpin long-term supply agreements, technical cooperation, and shared market intelligence across the GCC.

OPEC+ has continued its own output trajectory in parallel, agreeing to a third consecutive production quota increase following the disruption to Hormuz shipping routes. The organisation's operational continuity in the near term is not in doubt. However, OPEC's global influence faces a more complex test over the medium term as the deeper question of credibility and cohesion emerges on a longer horizon.

| OPEC Response Interpretation | Structural Implication |

|---|---|

| Anticipated departure, pre-adjusted models | Internal quota recalibration already underway |

| Strategic de-escalation to prevent contagion | Concern that other members may follow |

| Reduced enforcement leverage | Inability to penalise a producer of this scale |

Oil Price Dynamics: What the Market Is Pricing In

The immediate crude market response to the confluence of the Hormuz disruption and the UAE exit reflected the inherent complexity of the situation. Brent crude spiked approximately 4% above $15 per barrel on the initial conflict-driven supply disruption fears, before retreating to approximately $14 per barrel following confirmation of the UAE's departure. Monitoring Brent and WTI futures remains essential for understanding how traders are positioning around this structural shift.

Disclaimer: Oil price figures referenced above reflect reported market data from the conflict and announcement period. Price levels in this range indicate an extraordinarily distressed market environment and should not be interpreted as representative of normalised crude pricing. Investors and analysts should not base forward projections solely on these figures.

Looking beyond immediate price action, three forward scenarios illustrate the range of plausible outcomes:

Scenario A: UAE Volume Growth Within a Disciplined OPEC+ Framework

The UAE scales toward 5 million bpd while remaining OPEC+ members hold their quota commitments. Net supply addition is gradual, absorbed by demand growth from Asian import markets. Price pressure is modest and manageable for Saudi Arabia's fiscal requirements.

Scenario B: UAE Exit Encourages Further Defections

Producers including Iraq and Kazakhstan, both of which have histories of quota non-compliance, interpret the UAE's exit as legitimising unilateral production expansion. Cartel discipline erodes progressively. The 2020 Saudi-Russia price war serves as a historical reference for how rapidly cooperative frameworks can collapse under this kind of pressure. Consequently, oil market volatility could intensify significantly if multiple producers pursue unconstrained volume strategies simultaneously.

Scenario C: Sustained Geopolitical Disruption Offsets Production Gains

Continued instability in and around the Strait of Hormuz constrains tanker availability, elevates insurance costs, and limits the net market impact of UAE production growth. Price volatility remains elevated independent of volume changes.

OPEC's Internal Power Balance After the UAE's Departure

The Saudi Arabia Asymmetry

The relationship between Saudi Arabia and the UAE within OPEC had historically been one of the cartel's most important bilateral anchors. Both nations shared broadly aligned interests in price stability, carried low production costs relative to other members, and cooperated on quota strategy in ways that gave the alliance credibility. That alignment is now fractured at the institutional level.

Saudi Arabia's fiscal breakeven oil price, historically estimated in the range of $70 to $90 per barrel, creates a structural tension with any scenario in which UAE volume growth contributes to sustained price weakness. Riyadh now manages OPEC without its most capable Gulf production partner, while facing a supply competitor in Abu Dhabi that operates with similar cost advantages but none of the quota obligations.

What Remains of OPEC's Collective Weight

The removal of approximately 3.6 million barrels per day of UAE production from OPEC's official membership base is not merely symbolic. It reduces the organisation's total representational output and, more critically, skews the remaining membership toward higher-cost, more fiscally vulnerable producers. These are precisely the members most likely to cheat on quotas when prices are low, further undermining the disciplinary architecture OPEC depends upon.

HSBC analysis has noted limited near-term market impact from the UAE's departure, a perspective that focuses on the immediate supply picture rather than medium-term structural dynamics. The more significant question is whether OPEC retains the credibility to function as a genuine market management body when its third-largest producer is now competing freely on volume.

The next major ASX story will hit our subscribers first

The UAE's Post-OPEC Production and Export Strategy

Scaling the Output Roadmap

| Metric | Figure |

|---|---|

| UAE OPEC membership duration | 59 years (1967 to 2026) |

| OPEC rank by production | Third largest |

| Pre-conflict production baseline | ~3.6 million barrels per day |

| 2027 production target | Up to 5 million barrels per day |

| Targeted production increase | ~39% above pre-conflict baseline |

| Hormuz bypass pipeline length | ~249 miles |

| Exit effective date | May 1, 2026 |

Priority Export Markets

Freedom from quota constraints opens the door to bilateral long-term supply agreements that OPEC membership would have complicated through volume limitations. The markets most relevant to Abu Dhabi's volume growth strategy are those demonstrating sustained import demand growth:

- India: Rapidly expanding refining capacity and sustained demand growth trajectory

- China: The world's largest crude importer, with ongoing appetite for long-term supply security agreements

- Southeast Asia: Emerging refining hubs across Vietnam, Indonesia, and the Philippines with increasing import requirements

The UAE's competitive positioning in these markets benefits from low production costs, established tanker logistics, and the Hormuz-independent export route that provides supply reliability others cannot guarantee during periods of regional stress.

Sovereign Wealth Implications

A production trajectory toward 5 million bpd at scale materially expands the revenue base available to Abu Dhabi's sovereign wealth vehicles. That additional capital can simultaneously fund continued upstream investment, accelerate domestic economic diversification initiatives aligned with UAE Vision 2031, and support the UAE's growing role as a global capital allocator. The UAE exit from OPEC is therefore not a retreat from energy ambition; it is a structural expansion of the terms on which that ambition is pursued.

Is This the Beginning of a Broader OPEC Fragmentation?

Historical Precedents and Their Limits

Previous member exits offer limited analytical guidance for the current situation. Ecuador departed in 1992 and again in 2019. Qatar left in 2019, citing a strategic pivot towards liquefied natural gas. Indonesia has suspended membership at various points. None of these exits involved a producer of the UAE's production scale or geopolitical significance within the GCC architecture.

The critical distinction is not simply production volume. It is the signal that the UAE's departure sends to other members who have long harboured ambitions to expand output beyond their quota allocations. As DW analysis highlights, if Abu Dhabi can exit cleanly, maintain bilateral relationships, and pursue a 5 million bpd target without institutional consequence, the internal logic of continued cartel compliance weakens for every producer that has built spare capacity it cannot currently use.

What OPEC Still Offers, and What It Is Losing

OPEC was founded in 1960 to counterbalance the pricing power of Western international oil companies over producing nations. That founding rationale has been substantially transformed by decades of nationalisation, the rise of state-owned producers, and the globalisation of energy trading. What the organisation offers today is more narrowly defined:

- Coordinated output management to support price floors

- A multilateral diplomatic forum for energy policy dialogue

- Market signalling capacity that influences futures pricing curves

- A framework for managing quota disputes between members

These functions retain real value for financially constrained producers with limited options outside collective action. They offer progressively less value to a producer like the UAE, which has the infrastructure, the cost structure, and the export route independence to act effectively on its own terms.

The question that now hangs over global oil markets is not whether OPEC survives the UAE exit from OPEC in the near term. It almost certainly does. However, the deeper question is whether the cartel's remaining architecture can sustain credibility and compliance discipline without one of its most consequential members, at a time when multiple other participants are already testing its boundaries.

This article is intended for informational purposes only and does not constitute financial or investment advice. Forward-looking scenarios, production targets, and price projections involve significant uncertainty and should not be relied upon as predictions of future market outcomes. Readers should conduct independent research and consult qualified advisers before making any investment decisions related to energy markets or commodities.

Want to Track the Next Major Commodity Market Shift Before the Crowd?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex commodity data into actionable investment insights — explore historic discovery returns to understand the scale of opportunity, and begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.