May 18, 2026

When Civilian Nuclear Infrastructure Becomes a Battlefield: What It Means for Oil Markets

Energy markets have historically absorbed geopolitical shocks through a familiar sequence: a supply disruption event, a rapid repricing of risk, followed by gradual normalisation as diplomatic channels reopen or alternative supply routes emerge. That pattern has been the dominant framework for understanding crude oil price trends for decades. However, the events unfolding in the Gulf region in 2026 are challenging whether that framework still holds.

This is particularly evident after a drone strike targeted the UAE's Barakah nuclear power plant on May 18, pushing both Brent and WTI crude to their highest levels in years and raising questions that go well beyond conventional oil supply analysis.

The intersection of the UAE nuclear plant attack and oil prices is not simply a matter of supply disruption arithmetic. It represents a convergence of escalation vectors that energy markets have never encountered in this precise combination: an active 80-day restriction on the world's most critical energy transit corridor, ongoing proxy warfare targeting Gulf infrastructure, direct military engagement between major powers, and now, the targeting of civilian nuclear facilities.

Understanding why this matters requires looking past the daily price ticker and examining the structural dynamics underneath.

When big ASX news breaks, our subscribers know first

The Risk Premium Has Changed in Character, Not Just in Magnitude

Oil market risk premiums are a well-understood concept. Traders embed a layer of additional cost into crude prices whenever geopolitical instability threatens supply availability. During the 2022 Russia-Ukraine conflict, risk premiums pushed Brent above $130 per barrel briefly before retracing as alternative supply pathways emerged.

During the 2019 Abqaiq attack on Saudi Aramco's infrastructure, Brent spiked roughly 15% intraday before markets recalibrated once the scale of actual production damage became clear.

What Makes This Cycle Different?

What distinguishes the current environment is not the size of the risk premium but its persistence and its expanding scope. Furthermore, oil market disruption of this kind has pushed crude prices from approximately $70 per barrel in late February 2026 to above $100 per barrel within weeks of the initial US-Israeli joint military strikes against Iran on February 28.

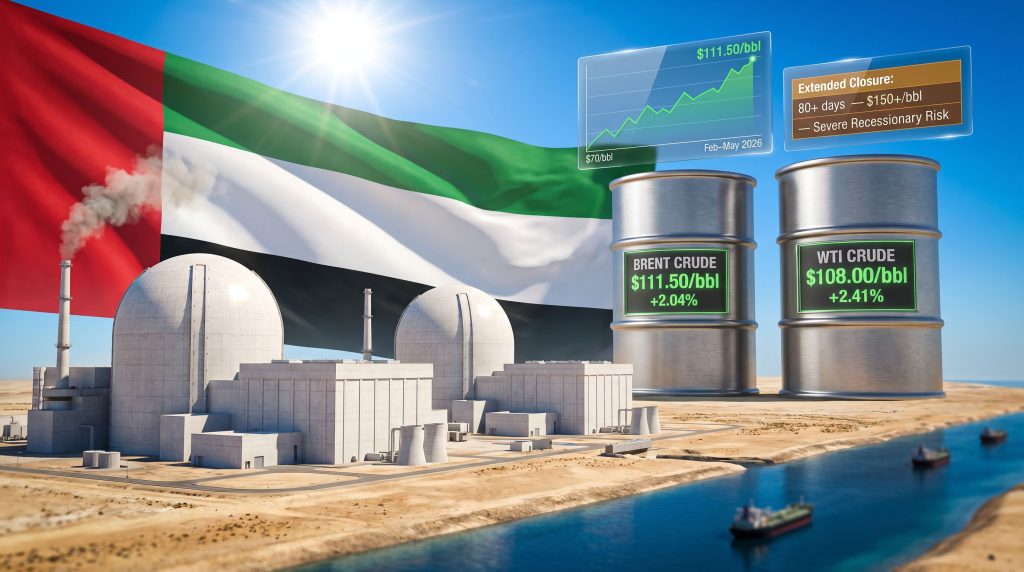

Prices have continued rising rather than mean-reverting. Brent crude reached $111.50 per barrel on May 18, representing a gain of $2.23 or 2.04% in a single session, while WTI traded at $108.00 per barrel, up $2.54 or 2.41%. Both benchmarks had already added more than 7% in the preceding week alone.

The critical insight here is that previous geopolitical oil spikes were largely self-limiting. This cycle does not yet have a visible ceiling because the supply disruption is structural rather than episodic.

The risk premium in current prices is therefore qualitatively different from prior geopolitical spikes. It reflects a sustained interruption of physical supply flow, not merely the fear of one. Iran's restriction of shipping through the Strait of Hormuz following the February strikes converted what might have been a temporary market anxiety event into a real and ongoing supply constraint.

Why the Barakah Strike Matters Beyond the Nuclear Question

The Barakah nuclear power plant, located in Abu Dhabi emirate, is the UAE's flagship energy diversification project. Built by the Korea Electric Power Corporation using APR-1400 reactor technology, the facility spans four reactor units with a combined capacity of 5,600 megawatts, making it one of the largest single-site nuclear installations in the world.

Its first unit began commercial operations in 2020, with the fourth unit coming online in early 2024. The plant was designed explicitly to reduce the UAE's dependence on natural gas for domestic power generation, freeing up hydrocarbon resources for export.

Why Targeting Barakah Sends a Powerful Signal

The significance of targeting this facility is layered. According to recent reporting on the Barakah drone strike, oil rose more than 1% immediately following news of the attack:

- From an energy security perspective, Barakah represents the UAE's long-term strategic hedge against hydrocarbon price volatility

- From a psychological warfare perspective, targeting a nuclear facility introduces radiological risk considerations that amplify public anxiety far beyond what conventional infrastructure strikes produce

- From a diplomatic perspective, the UAE's formal characterisation of the strike as a terrorist attack signals the likelihood of escalatory responses that markets will need to price in

- From a precedent perspective, attacking civilian nuclear infrastructure normalises a class of targets that has historically been considered off-limits under international norms

Emirati officials confirmed an investigation was underway following the incident, and the International Atomic Energy Agency stated it was actively monitoring the situation. The UAE's stated reservation of the right to respond created immediate uncertainty about what form that response might take and how it could further affect regional stability.

Critically, the oil market's reaction to the Barakah strike was not primarily driven by concerns about nuclear power generation capacity. The market reaction was driven by what the attack signals: a willingness by hostile actors to escalate beyond previously observed thresholds, and by the political pressure it creates on UAE and allied governments to respond in ways that could further inflame the broader conflict.

The Strait of Hormuz: 20% of Global Energy and Zero Redundancy

No analysis of the current UAE nuclear plant attack and oil prices environment is complete without understanding the Strait of Hormuz as a physical and strategic reality. The strait is a narrow maritime passage roughly 33 kilometres wide at its narrowest navigable point, positioned between Iran and Oman at the mouth of the Persian Gulf.

It functions as the sole maritime exit route for crude oil exports from Saudi Arabia, Iraq, Kuwait, the UAE, Bahrain, and Qatar, in addition to significant volumes of liquefied natural gas from Qatar.

Approximately 20% of global energy supplies transit this corridor daily, including an estimated 17 to 21 million barrels of crude oil depending on the season and production levels. There is no adequate alternative. The East-West Pipeline across Saudi Arabia can handle partial volumes, but its capacity is significantly lower than Hormuz throughput.

The scenarios facing energy markets break down as follows:

| Scenario | Duration | Estimated Brent Impact | Broader Economic Effect |

|---|---|---|---|

| Partial flow restriction (current) | Ongoing | $100 to $115 per barrel | GDP reduction of 0.2 to 0.4% |

| Full closure, short term | 30 to 60 days | $120 to $140 per barrel | GDP reduction of 0.5 to 0.8% |

| Extended closure | 80-plus days | Above $150 per barrel (modelled) | Severe recessionary risk |

Iran's decision to restrict shipping flow following the February 28 strikes created the foundational supply anxiety underpinning current prices. Moody's Ratings, in its geopolitical risk assessment, identified little evidence of a near-term or durable settlement between the US and Iran, effectively capping the probability of a Hormuz normalisation event in the near term.

The Strait of Hormuz is not simply a chokepoint in the logistical sense. It is a leverage mechanism that Iran has now demonstrated it will activate under sufficient pressure. Markets are pricing that leverage into every barrel traded.

The 80-day duration of the current disruption already places this event in historically unprecedented territory. The 1980s Tanker War produced periodic disruptions but never a sustained corridor restriction of this duration. Markets are navigating genuinely uncharted waters in terms of the sustained physical supply constraint.

How the Escalation Cycle Reached This Point

Understanding the sequence of events that produced the current oil price environment requires tracking a compressed but consequential timeline:

- February 28, 2026: US and Israeli forces conduct joint military strikes against Iran, representing the pivotal escalation trigger for the current price rally

- Post-strike, late February to March: Iran retaliates by restricting shipping flows through the Strait of Hormuz, converting geopolitical anxiety into a physical supply constraint

- March to April 2026: Drone incidents multiply across the Gulf, with proxy forces targeting energy and civilian infrastructure across multiple Gulf states

- May 2026: Saudi Arabia reports intercepting three drones entering its airspace from Iraqi territory and issues formal warnings about sovereignty protection measures

- May 18, 2026: A drone strike is reported at the Barakah nuclear power plant in the UAE; US President Donald Trump is reported to be scheduled to meet senior national security advisers to evaluate potential military options against Iran

The Role of Proxy Forces

What makes this escalation cycle particularly difficult for markets to price is the role of proxy forces. Iran's regional network, operating across Yemen, Iraq, and Lebanon, provides Tehran with asymmetric tools that complicate the attribution of any individual attack. An analyst at IG Markets described the drone strikes against Gulf infrastructure as a pointed warning that further direct strikes on Iran could activate more intensive proxy responses targeting Gulf energy assets.

In addition, escalating geopolitical tensions of this nature create non-linear risk environments that are extremely difficult for energy markets to price with any precision. Reports that US President Trump was scheduled to meet national security advisers to discuss potential military options against Iran added a further layer of uncertainty to already elevated market anxiety.

The Macroeconomic Consequences of Sustained Triple-Digit Oil

Moody's Ratings has revised its Brent crude price forecast to a range of $90 to $110 per barrel for much of 2026, explicitly acknowledging that significant volatility and periodic spikes beyond this band are expected in response to new geopolitical developments. This is not a narrow forecast range. A $20 per barrel band reflects genuine uncertainty about the trajectory of the conflict and the Strait of Hormuz situation.

The economic consequences of sustained prices within this band are material. Moody's assessment indicates that prices in the $90 to $110 per barrel range could reduce real GDP growth by 0.2 to 0.8 percentage points across several major economies.

| Economy Type | Exposure Level | Primary Vulnerability |

|---|---|---|

| Oil-importing emerging markets | Very High | Currency depreciation combined with import cost surge |

| European manufacturing economies | High | Energy-intensive industrial base facing margin compression |

| South and Southeast Asian economies | High | Structural dependence on Gulf crude imports |

| Oil-exporting Gulf states | Mixed | Revenue windfall offset by infrastructure risk and conflict costs |

| US economy | Moderate | Domestic production buffer, but significant inflation risk |

Moody's also noted that oil-importing nations are pursuing bilateral supply arrangements to reduce exposure to Hormuz-dependent crude flows. This represents a longer-term structural consequence of the conflict, consistent with the broader emergence of a multi-polar world economy in which nations actively diversify away from single-point dependencies in energy supply chains.

The next major ASX story will hit our subscribers first

What the Current Rally Tells Us About Energy Market Psychology

One of the less-discussed dimensions of the current price environment is what it reveals about how energy markets process non-linear risk. Standard oil market models are built around supply and demand fundamentals, OPEC market influence, inventory levels, and seasonal consumption patterns. They are not well-equipped to price the probability of an extended Strait of Hormuz closure or proxy attacks on nuclear infrastructure.

When models break down, markets default to risk aversion and price discovery through momentum. The more than 60% increase in Brent crude from approximately $70 per barrel in late February to above $110 per barrel by mid-May reflects not just the supply constraint but the market's recognition that its standard forecasting tools have limited applicability.

This creates specific dynamics worth understanding:

- Long positioning becomes self-reinforcing: Each new escalation event validates existing long positions, encouraging further accumulation rather than profit-taking

- Short sellers face asymmetric risk: The downside scenario is more immediately visible than the upside scenario, creating reluctance to build short positions even at elevated levels

- Volatility premiums expand in options markets: As the range of plausible outcomes widens, the cost of hedging exposure through options increases, which itself affects physical market pricing

- Speculative positioning diverges from fundamental analysis: Markets increasingly price scenarios rather than inventory levels, making traditional fundamental analysis less predictive of near-term price moves

Key Variables That Will Determine Oil's Next Direction

Four developments warrant the closest attention for anyone tracking where crude prices go from current levels:

- US military decision-making regarding Iran: Any confirmed expansion of direct military action against Iranian territory would likely push Brent above $120 per barrel within hours, given the established proxy escalation dynamic

- Strait of Hormuz shipping restoration: A credible and verified peace framework that reopens normal transit operations would represent the single most powerful downward price catalyst, potentially retracing Brent toward $85 to $90 per barrel

- Proxy attack frequency and targeting scope: If the Barakah strike represents the beginning of a broader shift toward nuclear and critical civilian infrastructure targeting, markets will embed a substantially higher risk floor into prices regardless of Hormuz developments

- IAEA findings on Barakah: If the investigation confirms significant structural damage or any radiological release, the political pressure on UAE and allied governments to respond militarily will intensify sharply

The interaction between these variables is non-linear. A diplomatic development that appears to reduce Hormuz risk could be simultaneously offset by a new proxy attack on infrastructure, keeping the net risk premium elevated even as one component declines. This is precisely why the current environment is structurally different from previous geopolitical oil spikes.

Is This a Structural Repricing or a Temporary Spike?

The question of whether the current UAE nuclear plant attack and oil prices environment represents temporary geopolitical noise or a structural repricing of Gulf energy risk is the most consequential question for energy markets and energy businesses planning capital allocation over a multi-year horizon.

Previous geopolitical oil spikes, including those associated with the Gulf War, the Arab Spring, and the initial Russia-Ukraine escalation, shared a common characteristic: resolution pathways were visible relatively early in the cycle, even if they took time to execute. The current situation lacks that feature.

Furthermore, analysis of how oil prices climbed after the Barakah attack to a two-week high underscores just how sensitive markets have become to each new development in the conflict. Moody's assessment that there is little evidence of a near-term or durable settlement between the US and Iran is not a minor qualification. It is a statement that the single most important prerequisite for oil price normalisation has no credible near-term catalyst.

A credible ceasefire with verified Hormuz restoration could theoretically return Brent toward $80 to $90 per barrel within weeks. However, the Barakah attack suggests that even a Hormuz ceasefire would leave active threat vectors against Gulf energy infrastructure in place, preventing a return to the pre-conflict risk premium baseline.

Energy markets appear to be pricing in a persistent risk floor rather than a temporary event premium. Whether that assessment proves correct depends entirely on developments that remain, at this point, genuinely uncertain. What is not uncertain is that the convergence of Strait of Hormuz disruption, proxy warfare against critical infrastructure, and now attacks on civilian nuclear facilities has created an energy market environment with no modern precedent.

This article is intended for informational purposes only and does not constitute financial advice. Oil price forecasts and economic impact assessments referenced herein, including those from Moody's Ratings, represent current analytical assessments subject to change as geopolitical conditions evolve. Readers should conduct independent research before making investment decisions related to energy markets or commodity-linked instruments.

Want to Stay Ahead of the Next Major Market-Moving Discovery?

While geopolitical shocks reshape energy markets and create ripple effects across commodities, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data into actionable opportunities for both short-term traders and long-term investors. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.