July 7, 2026

When Quota Constraints Become a Strategic Liability

For decades, OPEC's market influence rested on a deceptively simple premise: collective restraint creates collective pricing power. Member nations accepted output ceilings in exchange for elevated revenues per barrel. The system worked reasonably well when installed production capacity and assigned quotas remained roughly aligned. However, when a country's infrastructure outpaces its permitted output by a margin measured in millions of barrels per day, the arithmetic of membership turns decisively negative.

That structural tension explains far more about the UAE's OPEC departure than any single political dispute. After 59 years of membership, the UAE formally withdrew from both OPEC and the broader OPEC+ framework on May 1, 2026, following an April 28 announcement by Energy Minister Suhail al-Mazrouei. The stated rationale was straightforward: years of upstream capital investment had built production infrastructure that the cartel's quota system was actively preventing from being used.

Al-Mazrouei framed the exit as an obligation to investors, arguing the UAE needed the freedom to supply global markets without output restrictions constraining what its capacity could physically deliver.

The numbers make that argument concrete. At the time of exit, the UAE's OPEC-assigned quota sat between 3.1 and 3.4 million barrels per day (bpd), while installed production capacity had already reached somewhere between 4.2 and 4.85 million bpd. That gap, representing over a million barrels of daily stranded output potential, was the real cost of continued membership.

When big ASX news breaks, our subscribers know first

UAE Oil Output After Leaving OPEC: The June 2026 Data Tells the Story

Near-Record Production in the First Full Quarter of Independence

The production data emerging from June 2026 offers the clearest early validation of the UAE's decision. Crude output climbed above 3.8 million bpd, its highest level since April 2020, according to Reuters source estimates. Bloomberg export tracking pushed that figure even higher, placing UAE export flows at approximately 3.94 million bpd, approaching the all-time record set in late 2025.

Critically, June's output not only exceeded the UAE's pre-war production baseline, it surpassed it entirely, making the UAE the fastest-recovering major Gulf producer and the only one to reach quota-free levels above its February 2026 benchmark. Furthermore, crude oil price trends in this period reflected the dramatic shift in supply dynamics following the exit.

The Reporting Discrepancy That Markets Should Not Ignore

One of the more technically significant details embedded in the June 2026 production data involves the divergence between UAE self-reported figures submitted to OPEC and independent assessments from the International Energy Agency (IEA). This gap deserves careful attention from analysts and traders who rely on OPEC's monthly production surveys.

| Reporting Source | May 2026 Output (bpd) | February 2026 Output (bpd) |

|---|---|---|

| UAE Self-Reported to OPEC | 2.11 million | ~3.40 million |

| IEA Independent Assessment | 2.80 million | 3.64 million |

| Bloomberg Export Tracking (June) | ~3.94 million | N/A |

| Reuters Source Estimates (June) | >3.80 million | N/A |

The divergence between self-reported and independently assessed figures is not a minor rounding difference. In May 2026, at the height of conflict-related disruptions, the UAE reported 2.11 million bpd to OPEC while the IEA independently estimated 2.80 million bpd, a gap of nearly 700,000 bpd.

In February, the IEA's figure of 3.64 million bpd exceeded the UAE's own OPEC submission by approximately 240,000 bpd. This pattern raises broader questions about the reliability of self-reported OPEC production data and why market participants should weight independent cargo tracking and IEA secondary source estimates more heavily when building supply models.

Gulf-Wide Recovery: How the UAE Compares to Its Neighbours

A Region Rebounding at Very Different Speeds

The June 2026 Gulf export recovery was significant in aggregate terms. Combined crude and condensate exports from Saudi Arabia, the UAE, Kuwait, Iraq, and Iran rose by more than 3.5 million bpd from May to June, reaching 10.07 million bpd according to Kpler data. Vortexa independently placed June Gulf flows at 10.2 million bpd, up sharply from 7.0 million bpd in May.

However, context is essential. June's combined Gulf output remains dramatically below the 16.5 million bpd recorded a year earlier, underscoring that the region's aggregate production recovery is still in early stages. In addition, geopolitical trade tensions continue to shape how quickly individual producers can restore and expand output capacity.

Country-by-Country Recovery Scorecard

| Producer | June 2026 Output/Exports | Pre-Conflict Baseline | Recovery Status |

|---|---|---|---|

| UAE | >3.80 million bpd | ~3.40-3.64 million bpd | Exceeded pre-conflict levels |

| Saudi Arabia | 4.32 million bpd | ~7.3 million bpd | ~59% recovery |

| Kuwait | 1.65 million bpd | ~2.6 million bpd | ~63% recovery |

| Iraq | 780,000 bpd | ~3.9 million bpd | ~20% recovery |

The UAE stands as the clear outlier in Gulf recovery speed. It is the only major producer to not only restore but exceed pre-conflict production levels, a direct consequence of its quota-free operational status and ADNOC's pre-positioned export infrastructure.

Iraq's position is particularly striking. As OPEC's second-largest producer, Iraqi exports of approximately 780,000 bpd in June represent roughly one-fifth of volumes shipped before the conflict, according to Vortexa data. The asymmetry between Iraq's recovery trajectory and the UAE's underscores how differently positioned Gulf producers are when it comes to rebuilding output capacity.

The Infrastructure Edge: Why ADCOP Changed Everything

Bypassing the Strait of Hormuz When It Mattered Most

A crucial but underappreciated element of the UAE oil output after leaving OPEC involves the Abu Dhabi Crude Oil Pipeline (ADCOP). When the Strait of Hormuz became operationally constrained during the conflict period, the UAE redirected export flows through ADCOP to the Port of Fujairah on the Gulf of Oman, bypassing the Strait entirely.

This infrastructure decision, made years before the current crisis, gave the UAE a structural first-mover advantage that no other major Gulf producer could replicate. Saudi Arabia, Kuwait, and Iraq all depend on Hormuz routing to varying degrees. Consequently, the UAE's ability to continue exporting during the disruption period while competitors were effectively locked out materially strengthened Abu Dhabi's market share position and geopolitical leverage in ways that will persist well beyond the immediate conflict aftermath.

ADNOC's Tender Strategy: Volume Over Premium

ADNOC's approach to crude sales since the OPEC exit reflects a deliberate prioritisation of market share capture over short-term price optimisation. Traders have reported that ADNOC has been selling crude through competitive tender processes at discounted prices, with the fifth tender covering approximately 18 million barrels for loading through August. Upper Zakum was the primary grade sold, with Das crude also changing hands in smaller volumes.

The pricing logic is straightforward but strategically significant. By discounting to levels that compete directly with Iranian and Russian crude alternatives on a landed-cost basis, ADNOC is actively pulling new buyer categories into its tender process.

New Buyers: Chinese Teapots and California Refineries

One of the more notable developments in ADNOC's recent tender activity involves the emergence of Chinese independent refineries, commonly known as teapot refiners, as active participants. According to market analysts at Sparta, these buyers were entirely absent from previous ADNOC tender rounds. Their appearance signals that current ADNOC discount levels have crossed a threshold where UAE crude competes economically with sanctioned Russian and Iranian grades on a delivered-cost basis into Chinese ports.

The teapot refiner category is particularly significant in oil market analysis because these independent Chinese processors typically have lower capital costs and more flexible crude procurement strategies than China's major state-owned refiners. When teapots begin bidding on Middle Eastern grades, it often signals a meaningful shift in price relationships between competing crude supply sources.

Separately, California refineries have emerged as new buyers of UAE crude, with ADNOC grades moving to US West Coast destinations through private negotiations. This geographic diversification of ADNOC's buyer base reflects a longer-term market positioning strategy that extends well beyond the immediate post-conflict supply window.

The Price Collapse: From War Premium to Surplus Anxiety

How Brent Fell More Than 40% in Under Three Months

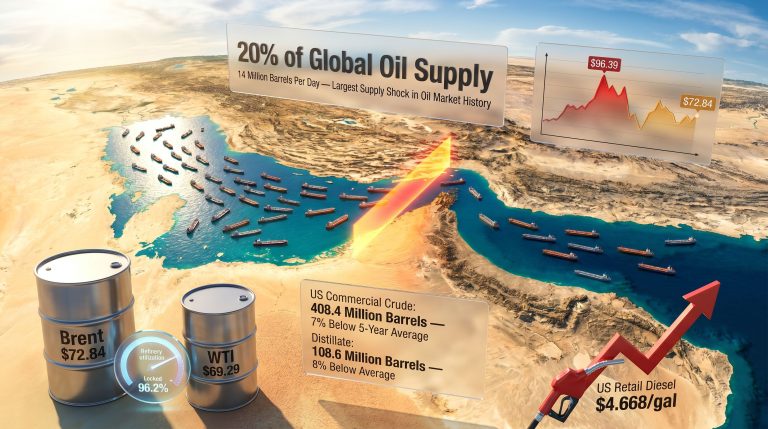

The oil market's narrative arc over the first half of 2026 represents one of the most dramatic pricing cycles in recent years. Brent crude peaked above $126 per barrel in late April 2026, driven by peak supply disruption anxiety during the Iran conflict and Hormuz uncertainty. By early July 2026, Brent had retreated to approximately $72 per barrel, roughly in line with pre-conflict pricing.

| Market Scenario | Brent Price Range |

|---|---|

| Peak Iran War Disruption (Late April 2026) | >$126/bbl |

| Post-Ceasefire Recovery (July 2026) | ~$72/bbl |

| Full Hormuz Normalization (Citi Forecast) | ~$60/bbl |

| UAE + Gulf Full Recovery Scenario | Potential further downside |

Analysts at Citi have published forecasts projecting a further decline toward $60 per barrel if Hormuz traffic fully normalises and Gulf supply continues recovering. Furthermore, this potential oil price crash scenario reflects how completely market sentiment has rotated from severe supply-disruption pricing into emerging surplus territory within the span of a single quarter.

The 'Mini-Glut' Mechanics: Prompt Supply vs. Forward Trading Windows

Understanding the Structural Mismatch

A technically important insight from current market analysis involves what analysts at Sparta have described as a structural mismatch between prompt crude availability and the standard Middle East trading window. Under normal market conditions, Gulf barrels are priced approximately two months ahead, meaning active trade in July should be pricing September loading cargoes. Instead, the post-Hormuz reopening has flooded the prompt market with barrels that should have loaded weeks earlier.

As of mid-June 2026, approximately 23 million barrels were still awaiting transit through the Strait of Hormuz, according to Kpler analyst Johannes Rauball. This backlog, clearing rapidly following the June 17, 2026 US-Iran ceasefire agreement, has created a temporary but significant overhang of prompt supply. The broader oil market effects of this supply normalisation are already reshaping how traders price forward curves.

The critical variable determining how long this mini-glut persists is Asian buyer behaviour. Two distinct scenarios exist:

-

Active SPR restocking: If Asian buyers, particularly Chinese state refiners and independent teapots, aggressively refill strategic petroleum reserves depleted during the conflict period, excess barrels will be absorbed relatively quickly and the glut resolves without major structural price damage.

-

Passive demand response: If SPR restocking appetite is limited or delayed, surplus barrels will first fill commercial storage, then relieve pressure through arbitrage trades into northwest European markets.

On the Atlantic Basin arbitrage question, market analysts note that declining crude differentials are currently doing more price discovery work than spread widening in the Brent-Dubai Exchange of Futures for Swaps (EFS). This means the arbitrage economics keeping Middle Eastern crude competitive into northwest Europe are being sustained by differential compression rather than outright spread movement, a technically subtle distinction with real implications for how traders should position around Middle Eastern crude grades versus Atlantic Basin benchmarks.

The next major ASX story will hit our subscribers first

UAE Production Outlook Through 2027: The IEA's Projection

From 3.8 Million to 5.2 Million Barrels Per Day

Looking beyond the immediate post-conflict supply surge, the IEA projects UAE total oil output reaching 5.2 million bpd by 2027, representing a potential increase of approximately 1.4 million bpd from current production levels. The UAE has been reclassified by the IEA as a major contributor to non-OPEC+ supply growth, a designation with meaningful implications for how analysts model global balances over the next 18 to 24 months.

| Timeframe | Estimated Output | Status |

|---|---|---|

| Pre-Exit Quota (2025) | ~3.1-3.4 million bpd | Quota-constrained |

| Post-Exit Actual (June 2026) | >3.8 million bpd | Quota-free, ramping |

| IEA Projection (2027) | 5.2 million bpd | Full capacity deployment |

| Theoretical Maximum | Up to 6.0 million bpd | Subject to market conditions |

The theoretical ceiling of 6.0 million bpd reflects energy officials' stated capacity ambitions under optimal market conditions, though this is not a formal production target and should be treated as an aspirational upper bound rather than a base case.

OPEC's Structural Weakening: Precedent and Fragmentation Risk

The Exit That Changes the Cartel's Internal Calculus

The UAE's departure removes one of OPEC's highest-capacity members from quota compliance discipline, creating a precedent with implications extending well beyond Abu Dhabi. Several other OPEC members carry installed production capacity that meaningfully exceeds their current quota allocations, and the UAE's successful exit model is now a visible, functioning alternative to continued cartel membership.

Three strategic scenarios frame the medium-term outlook:

-

Scenario 1 – Accelerated Capacity Deployment: The UAE reaches 5.2 million bpd by mid-2027, capturing significant Asian market share from recovering Iranian and Russian supply and cementing Abu Dhabi as a top-three global crude exporter.

-

Scenario 2 – Managed Ramp with Price Floor Defence: The UAE moderates production growth to avoid Brent declining below approximately $65 per barrel, using ADNOC's tender discount mechanism to balance volume growth against revenue optimisation.

-

Scenario 3 – OPEC Fragmentation Accelerates: The UAE's exit triggers similar capacity-liberation decisions from Kuwait or Iraq, further eroding collective output discipline and accelerating a structural transition toward volume-over-price market dynamics globally.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial, investment, or trading advice. Forecasts and projections referenced are those of third-party analysts and institutions and involve inherent uncertainty. Readers should conduct their own due diligence before making any investment decisions related to commodity markets or energy sector equities.

Frequently Asked Questions: UAE Oil Output After Leaving OPEC

Why did the UAE leave OPEC?

The UAE exited OPEC on May 1, 2026, to align production with its installed capacity and honour commitments to investors who funded years of upstream infrastructure expansion. The country's production capacity had grown well beyond OPEC-assigned quota limits, making continued compliance economically indefensible.

How much oil is the UAE producing after leaving OPEC?

UAE crude output exceeded 3.8 million bpd in June 2026, with export tracking data suggesting flows as high as 3.94 million bpd. The IEA projects UAE oil output after leaving OPEC will reach 5.2 million bpd by 2027.

What is ADNOC's pricing strategy post-OPEC?

ADNOC has been selling crude through competitive tender processes at discounted prices to attract new buyer categories, including Chinese independent refiners and US West Coast refineries, prioritising market share capture over short-term premium pricing.

How does UAE oil production compare to Saudi Arabia after the Iran conflict?

As of June 2026, Saudi Arabia's exports averaged approximately 4.32 million bpd, roughly 3 million bpd below its pre-conflict baseline. The UAE has already exceeded its pre-conflict production level, making it the fastest-recovering major Gulf producer.

Will the UAE's increased output cause global oil prices to fall further?

The market has already shifted from supply-shock pricing above $126 per barrel to approximately $72 per barrel. Analysts at Citi have projected a potential further decline toward $60 per barrel if Gulf supply normalisation continues and Asian demand absorption remains modest.

Want to Track the Next Major Commodity Shift Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, turning complex commodity and resource data into actionable alerts — so investors positioned in energy, mining, and resource equities can act decisively as global supply dynamics reshape market opportunities. Explore Discovery Alert's discoveries page to see how historic mineral discoveries have delivered substantial returns, and begin your 14-day free trial today to stay ahead of the market.