July 10, 2026

Why Institutional Capital Is Starting to Take UK Geothermal Seriously

For most of the past two decades, geothermal energy in the United Kingdom existed largely as a geological curiosity rather than a commercial proposition. The country lacks the volcanic hotspots that power Iceland's grid or the hydrothermal systems that have made geothermal a mainstream contributor across parts of the United States and New Zealand. Yet beneath Cornwall's ancient granite moorlands, a combination of radioactive heat generation within deep rock formations and naturally occurring brine chemistry has created something the broader energy transition desperately needs: a resource that can simultaneously produce zero-carbon baseload electricity and battery-grade lithium from a single underground source.

That combination has now attracted the attention of ABN AMRO, the major European commercial bank, which has extended a GBP 10 million financing facility to Geothermal Engineering Limited (GEL) to support the company's geothermal energy and lithium extraction development plans across the UK. Reported by Renewables Now on 7 May 2026, the GEL ABN AMRO financing arrangement marks a meaningful step in the maturation of UK geothermal as a bankable asset class, and raises important questions about where this emerging sector is heading.

Disclaimer: This article contains forward-looking statements, production targets, and financial projections drawn from publicly available reporting and the project outline provided. These should not be construed as investment advice. All figures and timelines are subject to change and involve material risks. Readers should conduct independent due diligence before making any investment or commercial decisions.

When big ASX news breaks, our subscribers know first

Cornwall's Geological Advantage and the Dual-Resource Logic

Understanding why GEL's United Downs project in Cornwall is attracting structured debt financing requires a basic understanding of the geology that makes it unusual, even by global geothermal standards.

Cornwall sits atop the Cornubian batholith, a vast body of granite formed around 280 to 300 million years ago during the Variscan orogeny. Granite contains elevated concentrations of uranium, thorium, and potassium, all of which decay radioactively and generate heat over geological timescales. This means Cornwall's subsurface is significantly hotter than would be expected at equivalent depths elsewhere in England, with geothermal gradients considerably above the UK average.

Critically, the brine circulating through fractures within this granite is naturally enriched in lithium, reportedly carrying concentrations exceeding 340 parts per million (ppm). For context, many conventional lithium brine operations in South America's Lithium Triangle typically work with grades ranging from around 200 to over 1,000 ppm, depending on the basin, but those resources require large evaporation ponds, consume significant land, and operate in remote high-altitude environments with complex water rights issues. Cornwall's geothermal brine extraction is accessed through existing wellbores drilled for energy purposes, making the lithium a co-product of infrastructure already justified on energy economics alone.

This dual-resource logic is what distinguishes GEL's model from conventional approaches to either geothermal power or lithium mining:

- Geothermal electricity generation provides a continuous, dispatchable power source uncorrelated with weather conditions

- Heat from the same brine resource can be supplied directly to industrial or district heating applications

- Lithium ions are selectively extracted from the brine using Direct Lithium Extraction (DLE) technology before the brine is reinjected underground

- The entire system operates as a closed loop, producing no surface mining waste and leaving no evaporation pond footprint

Technical Note on DLE: Direct Lithium Extraction is a processing methodology that uses sorbent materials, ion exchange resins, or membrane-based systems to selectively capture lithium ions from brine without the multi-year evaporation cycle required by traditional methods. DLE enables faster processing cycles, higher lithium recovery rates, and greater suitability for environmentally sensitive or low-footprint settings. It is central to GEL's ability to produce battery-grade lithium carbonate equivalent (LCE) from geothermal brine at commercial scale.

Unlike solar or wind generation, geothermal power operates continuously regardless of time of day or seasonal conditions. This baseload characteristic is particularly valuable for anchoring mineral processing operations that require consistent power supply to maintain quality-controlled chemical processing environments.

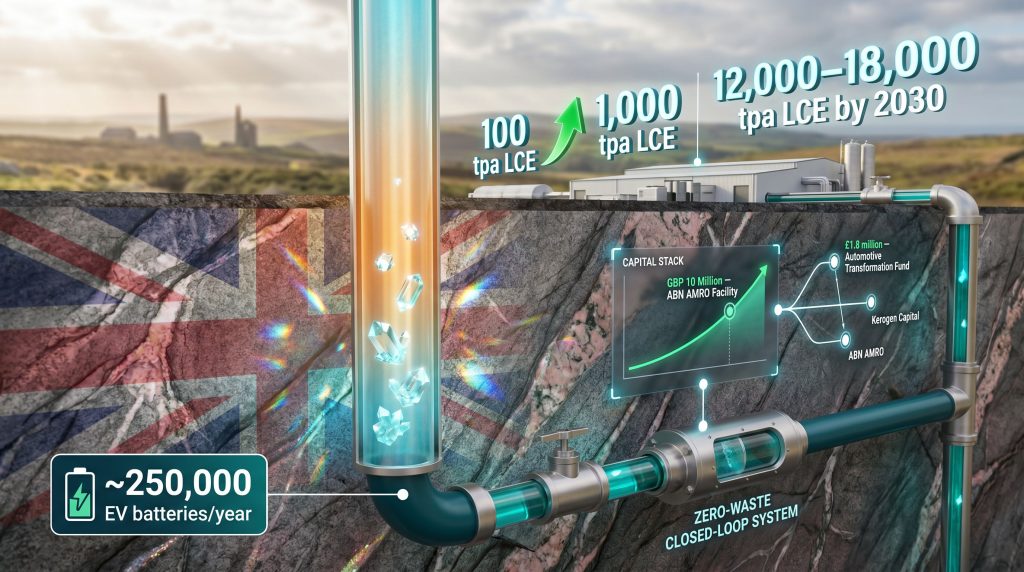

Breaking Down the GBP 10 Million ABN AMRO Facility

The GEL ABN AMRO financing arrangement sits within a broader blended capital structure that GEL has assembled across its development journey. Blended finance — the combination of concessional public funding with private equity and commercial debt — has become an increasingly standard architecture for early-commercial deep-technology energy projects where the risk profile is too novel for conventional project finance but the technology is sufficiently proven to attract institutional interest.

GEL's capital stack, as reflected in publicly available information, includes the following components:

| Capital Source | Type | Stated Purpose | Scale |

|---|---|---|---|

| Automotive Transformation Fund (ATF) | Government Grant | Scale-up readiness | £1.8 million |

| DRIVE35 Programme (APC UK / Innovate UK) | Government Grant | Scale-up feasibility study | Undisclosed |

| Kerogen Capital | Private Equity | Strategic equity backing | Undisclosed |

| ABN AMRO | Debt Financing | Geothermal and lithium expansion | GBP 10 million |

The ABN AMRO facility represents the commercial debt layer of this structure, a significant development because mainstream European commercial banks have historically been reluctant to extend credit to geothermal projects at early-commercial scale, where subsurface resource risk and technology scale-up risk combine to create a more complex risk profile than conventional renewables.

What makes the GBP 10 million facility strategically interesting is less its absolute size and more what it signals about ABN AMRO's appetite in this space. According to ABN AMRO's own announcement, a facility of this scale is best characterised as an early-commercial relationship transaction rather than a project finance commitment. It positions the bank to develop institutional knowledge of GEL's operations, build a credit relationship, and participate in substantially larger capital raises as the project scales toward its 2030 national targets. For GEL, it provides working capital and expansion financing while validating the project's creditworthiness to a wider market of potential debt providers.

United Downs: From Proof of Concept to Commercial Operation

GEL's United Downs facility near Redruth in Cornwall represents the operational foundation of its broader ambitions. Having commenced commercial-scale lithium production at approximately 100 tonnes per annum (tpa) of Lithium Carbonate Equivalent in early 2026, United Downs holds the distinction of being the first facility in the United Kingdom to simultaneously produce zero-carbon lithium and geothermal electricity from the same underground brine resource within a fully closed-loop system.

The near-term scaling trajectory is ambitious. GEL has set a target of reaching 1,000 tpa LCE by late 2026, representing a tenfold increase in production volume within a single operating year. Achieving this ramp-up requires meaningful expansion of DLE processing capacity, quality control systems capable of maintaining battery-grade purity specifications at higher throughput, and robust subsurface management to sustain consistent brine flow rates and lithium concentrations across the expanded operation.

What Battery-Grade Lithium Actually Requires

Not all lithium is equal from a battery manufacturer's perspective. Lithium carbonate destined for cathode active material production in lithium-ion batteries must typically meet purity thresholds of 99.5% or higher for battery-grade certification, with tightly controlled limits on impurities including sodium, potassium, calcium, magnesium, iron, and sulphate. Achieving and consistently maintaining these specifications at scale is one of the central technical challenges for any DLE-based operation.

Geothermal brine chemistry is inherently variable, and Cornwall's brines contain a complex mixture of dissolved minerals beyond lithium alone. The selectivity of DLE adsorbents for lithium over competing ions, and the downstream purification steps required to reach battery-grade purity, represent significant engineering and operational challenges that will only become more demanding as throughput scales from 100 tpa to 1,000 tpa and beyond. Furthermore, understanding how lithium mining works from brine sources provides essential context for appreciating the complexity of GEL's processing challenge.

The 2030 Vision: 18,000 Tonnes and 250,000 EV Batteries

GEL's long-term ambition extends well beyond United Downs. The company has articulated a national scaling target of 12,000 to 18,000 tpa LCE across multiple UK sites by 2030, a level of output that would, based on typical lithium content per battery pack for a mid-range electric vehicle, be sufficient to supply the equivalent of approximately 250,000 EV battery systems annually.

To contextualise that figure against the UK automotive market: the Society of Motor Manufacturers and Traders (SMMT) reported that battery electric vehicle registrations in the UK reached approximately 381,970 units in 2024, meaning GEL's 2030 target, if achieved, could theoretically supply lithium equivalent for roughly 65% of that volume from domestic zero-carbon production.

| Production Milestone | Volume (tpa LCE) | Target Date |

|---|---|---|

| Commercial production commenced | ~100 | Early 2026 |

| Near-term scaling target | ~1,000 | Late 2026 |

| National multi-site ambition | 12,000 to 18,000 | 2030 |

| EV battery equivalent (at 2030 target) | ~250,000 vehicles/year | 2030 |

Achieving this trajectory requires GEL to develop additional Cornwall-based sites, several of which reportedly hold existing planning permissions, reducing one of the major timeline risks in geothermal project development. Cornwall's granite geology extends across a substantial geographic area, and the Cornubian batholith provides a natural resource base that could theoretically support multiple geothermal wells across different locations while drawing on broadly consistent subsurface conditions.

The Supply Chain Rationale

The strategic importance of domestic lithium production to the UK battery supply chain is difficult to overstate. The UK currently has no meaningful domestic lithium production and is entirely dependent on imports from Australia (hard-rock spodumene concentrate), Chile and Argentina (brine-derived lithium), and processed materials from China. This creates multi-layered supply chain vulnerability at a time when the UK automotive sector is undergoing its most significant structural transformation in a century.

In addition, the global lithium market is increasingly shaped by geopolitical competition and trade policy, making domestically sourced supply even more strategically valuable.

For UK battery manufacturers and automotive original equipment manufacturers, domestically sourced zero-carbon lithium carries ESG compliance advantages that extend beyond raw material security. Supply chain due diligence regulations, Scope 3 emissions accounting frameworks, and downstream customer expectations around battery sustainability credentials are all creating commercial value for lithium that can demonstrate low-carbon provenance and traceable, environmentally responsible extraction.

Key Risks That Investors and Lenders Must Weigh

The GEL ABN AMRO financing story cannot be assessed without acknowledging the material risks that remain unresolved at this stage of GEL's development.

Subsurface and Resource Risk

Geothermal brine resources are not uniform. Lithium concentrations, brine temperature, flow rates, and brine chemistry can vary between drill sites even within the same geological formation. As GEL expands to additional Cornwall sites beyond United Downs, each new location will carry its own subsurface risk profile that must be characterised through drilling, testing, and extended production monitoring before it can be incorporated into production models with confidence.

Comparative experience from other geothermal-lithium projects provides instructive context:

- Upper Rhine Graben (Germany): Projects in this basin, pursued by developers including Vulcan Energy Resources, have encountered challenges relating to brine scaling, equipment corrosion from highly mineralised brines, and variability in lithium concentrations between wells. These operational learnings are directly applicable to Cornwall's operating environment.

- Salton Sea (California, USA): The Salton Sea geothermal field hosts some of the most lithium-rich brines identified globally, but decades of geothermal power operation there have demonstrated that brine management, scaling control, and mineral extraction at scale present persistent engineering challenges. Controlled Thermal Resources is among the developers attempting commercial lithium extraction from this resource.

Processing Scale-Up and Technology Risk

Moving from 100 tpa to 1,000 tpa within approximately 12 months is an aggressive target by any measure in extractive industries. DLE technology at pilot scale has been demonstrated by multiple operators globally, but commercial-scale deployments remain relatively limited in number, and each new scale-up introduces engineering challenges around throughput consistency, adsorbent regeneration cycles, reagent consumption, and product quality control.

Market and Offtake Risk

Lithium market pricing has experienced extreme volatility in recent years. Lithium carbonate spot prices peaked at extraordinarily elevated levels during 2022 before declining sharply through 2023 and into 2024, with some benchmarks falling by more than 80% from peak to trough. For early-commercial producers without long-term offtake agreements in place, this price volatility directly affects the economics underlying debt serviceability calculations. The absence of confirmed multi-year supply agreements with UK battery manufacturers or automotive OEMs represents a meaningful risk factor that lenders such as ABN AMRO will need to carefully assess.

The next major ASX story will hit our subscribers first

How GEL's Model Compares to Sector Peers

GEL does not operate in isolation. A small but growing cohort of developers globally is pursuing geothermal-lithium co-production, each with different geological settings, technology choices, and capital structures.

| Developer | Location | Primary Focus | Current Stage |

|---|---|---|---|

| Geothermal Engineering Limited (GEL) | Cornwall, UK | Power + Lithium co-production | Early commercial (2026) |

| Eden Geothermal | Cornwall, UK | Heat and power | Development |

| Vulcan Energy Resources | Upper Rhine, Germany | Lithium + geothermal power | Pilot to commercial |

| Controlled Thermal Resources | Salton Sea, USA | Geothermal power + lithium | Development |

GEL's first-mover status in UK commercial geothermal-lithium co-production, combined with its existing planning permissions for additional Cornwall sites, creates a degree of competitive positioning that is difficult for new entrants to replicate quickly. Planning consents in the UK for deep geothermal infrastructure involve complex regulatory processes spanning environmental impact assessments, hydraulic fracturing notifications, water abstraction licensing, and land access arrangements.

Having navigated these for United Downs and reportedly secured permissions for additional sites, GEL holds a procedural advantage that translates into time-to-production advantages over any future competitor. Moreover, the broader role of critical minerals in the energy transition underscores why first-mover producers with proven assets are attracting serious institutional attention.

What Comes Next: The Financing Catalysts to Watch

The GBP 10 million ABN AMRO facility is best understood as an early chapter in a financing story that will need to be retold at much larger scale if GEL's 2030 national targets are to be realised. Moving from early-commercial to full project finance scale — typically involving facilities of tens or hundreds of millions of pounds — will require GEL to demonstrate several additional capabilities to the institutional lending community:

- Consistent production performance at 1,000 tpa LCE, including sustained battery-grade purity and brine resource stability over multiple operating quarters

- Long-term offtake agreements with creditworthy counterparties such as UK battery manufacturers or Gigafactory operators, which provide the revenue certainty that underpins non-recourse project finance structures

- Independent resource certification of Cornwall's geothermal brine lithium reserves across multiple sites, using recognised standards comparable to those applied in conventional mining resource estimation

- Demonstrated DLE technology scalability through successful commissioning of expanded processing capacity at United Downs

The entry of ABN AMRO into this space, even at early-commercial scale, provides a meaningful signal to other institutional lenders that the asset class is worth monitoring. As GEL progressively de-risks its operations and builds a track record of consistent production, the financial architecture underpinning UK geothermal-lithium development is likely to become both more accessible and more substantial.

For a country seeking to secure its battery supply chain without compromising on carbon credentials, the combination of baseload renewable power and domestically produced zero-carbon lithium from a single Cornish brine source represents a genuinely distinctive proposition — one that is now, for the first time, attracting the structured attention of mainstream European banking capital.

Readers seeking additional context on UK geothermal energy financing and project developments can access ongoing coverage through Renewables Now, which provides industry reporting across European renewable energy sectors including geothermal.

Want to Catch the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across critical commodities like lithium — transforming complex geological data into clear, actionable investment insights for traders and long-term investors alike. Explore historic discoveries and the substantial returns they generated, then start your 14-day free trial to position yourself ahead of the broader market.