July 16, 2026

When Refinery Infrastructure Becomes a Battlefield: The New Logic of Energy Warfare

For most of modern history, energy infrastructure occupied a peculiar middle ground in armed conflict. Pipelines, refineries, and storage terminals were understood to be strategically sensitive, yet rarely became primary military targets at scale. That calculus has shifted fundamentally in 2026. Ukraine attacks on Russian refineries and global diesel markets have become inseparable subjects, representing something qualitatively different from conventional energy disruption tactics: a systematic, months-long effort to dismantle an adversary's downstream processing capacity plant by plant, unit by unit, until the cumulative damage exceeds the system's ability to self-repair.

The consequences are now rippling far beyond the front lines. Understanding why requires examining both the technical architecture of refinery operations and the structural role Russia played in supplying diesel to a wide range of global buyers. Furthermore, the geopolitical oil price factors at play here extend well beyond a single conflict zone.

When big ASX news breaks, our subscribers know first

The Architecture of Downstream Warfare

Why Crude Distillation Units Are the Strategic Chokepoint

To understand why Ukraine's targeting strategy has proven so effective, it helps to understand how refineries actually work at a mechanical level. At the foundation of every refinery sits the crude distillation unit, or CDU. This is the primary processing stage where raw crude oil is heated and separated into distinct product streams: naphtha, kerosene, diesel, fuel oil, and other fractions. Without a functioning CDU, a refinery cannot accept crude feedstock at all, regardless of how intact its secondary processing units remain.

This technical reality transforms CDU damage from a production inconvenience into a complete facility shutdown. Under normal planned maintenance schedules, a CDU overhaul can take weeks to months. Under wartime conditions where the same facility faces re-strikes before repairs are completed, restoration timelines become indefinite. Ukraine appears to have understood this chokepoint clearly, with multiple confirmed attacks specifically targeting primary distillation infrastructure at facilities including Norsi in Kstovo and the Omsk refinery.

Precision Strikes vs. Conventional Energy Disruption

Traditional energy disruption in wartime typically involved pipeline sabotage, storage facility destruction, or port blockades. These approaches share a common limitation: they are geographically constrained and often reversible within weeks. Refinery strikes occupy a different strategic tier. Processing infrastructure is expensive to repair, impossible to relocate, and serves as a node through which all upstream crude production must pass before it becomes usable fuel.

Disabling a refinery does not merely reduce export capacity; it severs the link between crude reserves and domestic consumption simultaneously. The compound effect of simultaneous strikes across geographically dispersed regions eliminated the standard industry fallback responses: redirecting product from unaffected facilities, drawing down inventories, or withholding export cargoes to cover domestic shortfalls. When Moscow, Nizhny Novgorod, Samara, Tatarstan, Bashkortostan, and southern Russia are all compromised at once, none of those options remain viable.

The Scale of Destruction: Russia's 21-Year Processing Low

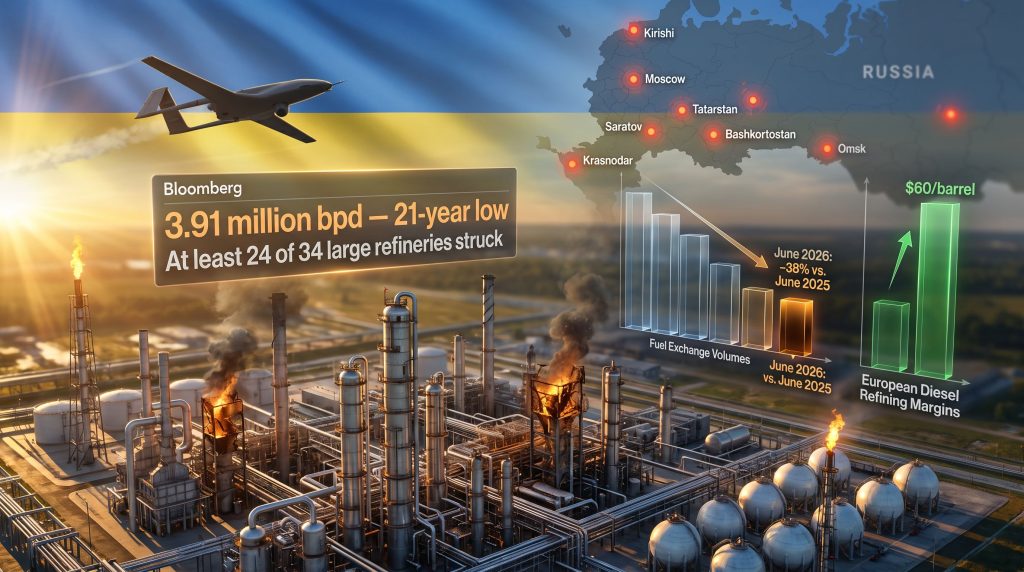

By early July 2026, Russian refineries were processing an average of just 3.91 million barrels of crude per day, according to Energy Aspects data cited by Bloomberg. That figure sat more than 1.4 million barrels per day below the prior year's average and represented the lowest national throughput rate recorded since March 2005. The breadth of the campaign makes the numbers comprehensible: Ukraine struck at least 24 of Russia's 34 large refineries across approximately 50 separate attacks over roughly 100 days.

The Refinery Damage Map

| Refinery / Region | Attack Status | Estimated Capacity Impact |

|---|---|---|

| Omsk (Siberia) | Struck July 6, 2026; primary distillation units damaged | ~22 million tonnes/year capacity at risk |

| Kirishi (European Russia) | Struck March and May 2026; significant capacity lost | Major northwest processing hub |

| Moscow Refinery | Multiple June 2026 strikes; potentially offline through year-end | Critical domestic supply node |

| Norsi, Kstovo | Repeated strikes including primary processing unit damage | 63% exchange sales decline reported |

| Saratov | Halted operations following March 2026 strike | Full operational shutdown |

| Taneco (Tatarstan) | Attacked; 56% exchange sales decline reported | Integrated complex |

| Samara Group | Attacked; ~65% exchange sales decline reported | Multi-plant regional cluster |

| Afipsky (Krasnodar) | Struck overnight July 14, 2026 | Black Sea refining hub |

| Gazprom Neftekhim Salavat (Bashkortostan) | Struck July 14, 2026 | Largest integrated refining-petrochemical complex |

The Omsk Strike: Eliminating the Final Safe Zone

The July 6 attack on the Omsk refinery carried particular strategic significance. Situated more than 2,000 kilometres from the front lines in western Siberia, Omsk had represented what many analysts considered an unreachable sanctuary within Russia's refining geography. At approximately 22 million tonnes of annual crude processing capacity, it is Russia's largest single refinery by throughput.

The strike reportedly damaged ELOU-AVT-11, a primary distillation unit rated at 8.4 million tonnes of crude and 1.2 million tonnes of gas condensate per year, according to Interfax Ukraine reporting. A second major unit, AVT-10, was also reportedly affected. The operational implication of reaching Omsk extended beyond the physical damage — it signalled that no Russian refining asset, regardless of its distance from Ukraine, could be considered beyond the campaign's reach.

The Repair Cycle Trap

Repeat strikes at already-damaged facilities have turned the restoration process into a losing race. Ukraine returned to the Moscow refinery, Norsi, and Syzran after initial attacks, striking again before operators could restore full output. This pattern is analytically important: a single strike creates a recovery timeline, but a second strike before that timeline completes resets the clock entirely, often with compounding damage to partially repaired infrastructure. Indeed, Ukrainian drone attacks on Russian refineries have demonstrably plunged the country into a sustained fuel crisis. The cumulative effect is a maintenance burden that Russian operators simply cannot outpace with available repair capacity.

Exchange Trading Data: The Mirror Russia Cannot Cover

Russia progressively restricted its refinery operational data as the attacks intensified, making independent assessment more difficult. However, fuel trading volumes on the St. Petersburg International Mercantile Exchange provided a transparent window into production reality that could not be easily concealed.

Fuel Sales Volume Collapse

| Period | Average Daily Fuel Sales (tonnes/day) | Year-on-Year Change |

|---|---|---|

| January to March 2026 | 118,000 to 150,000 | Baseline |

| April 2026 | 104,000 | Declining |

| May 2026 | 106,000 | Brief stabilisation |

| June 2026 | 80,300 | -38% vs. June 2025 |

The facility-level data was more severe still. Exchange deliveries from the Moscow refinery's distribution points averaged approximately 4,400 tonnes per day before the June 16–18 attack cluster. In the aftermath, that figure dropped to roughly 400 tonnes per day. Kirishi exchange sales fell approximately 80% following its May strike. The Samara refinery group lost around 65% of exchange volume, while Norsi and Taneco registered declines of 63% and 56% respectively.

Alongside the volume collapse, weighted average fuel prices on the exchange climbed 37% year-on-year by June 2026, reflecting the acute supply scarcity that physical traders were pricing into every transaction. Consequently, monitoring oil price movements has become essential for traders navigating this environment.

The Wholesale Rule Change That Deepened Independent Retailer Pain

Moscow's response to the supply crisis included a regulatory adjustment that amplified the damage flowing down to independent fuel retailers. From July 1, 2026, the mandatory exchange quota requiring large refiners to sell a fixed proportion of gasoline through the St. Petersburg exchange was reduced from 15% to 10%. This freed vertically integrated producers such as Rosneft, Gazprom Neft, and Lukoil to redirect a larger share of their diminished output into their own captive retail networks.

The consequence for independent operators was direct and severe. Independent retailers account for roughly 65% of Russia's 27,800 filling stations and serve an estimated 30–40% of the retail fuel market. With exchange volumes already compressed by refinery outages and the mandatory quota simultaneously reduced, these operators faced higher prices for smaller available volumes, with no alternative sourcing pathway.

A Sequential Export Ban Timeline

Russia's export restriction sequence serves as a precise chronological record of the crisis deepening:

| Date | Fuel Type Banned | Underlying Driver |

|---|---|---|

| April 2026 | Gasoline exports suspended | Domestic production surplus eliminated |

| June 1, 2026 | Jet fuel exports banned | Demand tightening amid refinery outages |

| July 8, 2026 | Diesel exports banned (including vertically integrated producers) | Domestic shortfall reached critical threshold |

The diesel ban was the most consequential step. Russia produced 81.6 million tonnes of diesel in 2024 against domestic consumption of approximately 51 million tonnes, a structural surplus of roughly 30 million tonnes annually that had made it one of the world's largest diesel exporters. By July 2026, that structural surplus had been consumed by cumulative refinery losses, and the ban extended even to vertically integrated oil companies that had previously held exemptions.

Russia's Emergency Response: From Exporter to Importer

The shift from diesel exporter to fuel importer within a single year represents one of the most striking energy market reversals of the conflict. Russia's emergency procurement efforts included:

- At least 60,000 tonnes of gasoline reportedly sourced from India in mid-2026, according to Reuters

- Belarusian gasoline imports reaching 141,000 tonnes during the first 25 days of June alone, which was 2.4 times the total volume imported during the entirety of May

- Reported procurement efforts targeting approximately 400,000 tonnes per month of gasoline from international suppliers

Simultaneously, the maritime dimension of the campaign compressed distribution options. Ukrainian forces claimed 11 vessel strikes in the Sea of Azov in a single overnight operation on July 14, 2026, extending a maritime campaign that had already disrupted tanker traffic through the Kerch Strait and the Volga-Don waterway. The combination of land and sea interdiction is compressing both production capacity and product distribution simultaneously — a pincer dynamic that Russia's logistics planners have no straightforward answer to.

The next major ASX story will hit our subscribers first

Global Diesel Market Consequences

Russia's Pre-Crisis Position in Global Diesel Architecture

| Metric | Figure |

|---|---|

| Russia's global diesel export rank | Second-largest exporter globally, behind the United States |

| 2024 diesel production | 81.6 million tonnes |

| 2024 domestic diesel consumption | ~51 million tonnes |

| Estimated pre-crisis export surplus | ~30 million tonnes annually |

| Refining capacity incapacitated (March to July 2026) | ~800,000 barrels per day offline |

The market reaction to the July 8 diesel export ban was immediate. European diesel refining margins surged above $60 per barrel, reaching record territory. U.S. diesel futures recorded their largest single-session gain in four years on the same day, according to Reuters. In addition, WTI and Brent futures reflected the broader volatility spreading across global energy benchmarks.

Regional Exposure to the Russian Diesel Withdrawal

| Region | Exposure Level | Alternative Supply Source |

|---|---|---|

| Turkey | High | United States, Middle East |

| North Africa | High | India, Middle East |

| Central Asia | Critical | Limited alternatives available |

| Brazil | Moderate | United States, Middle East |

| Europe | Indirect (already diversified post-2022) | United States, India |

Central Asia's position is particularly acute. Russian jet fuel deliveries to Central Asia and Afghanistan fell more than 92% between May and June 2026, according to Reuters. Gasoline shipments to the same region dropped 34% over the same period. These markets had historically relied on Russian refinery output as a near-exclusive supply source, with limited infrastructure to pivot rapidly toward alternative origins.

The Compounding Dual-Shock Environment

The timing of Russia's diesel withdrawal coincides with supply disruption signals emanating from the Middle East. Brent futures flipped into backwardation as buyers displaced from Russian supply began competing with importers already seeking alternatives to delayed Gulf product shipments. Furthermore, the broader trade war impact on oil has layered additional complexity onto an already fragile supply picture. When two independent supply shocks converge simultaneously, their combined market impact exceeds what either event would generate in isolation — a compounding dynamic that energy traders are now navigating in real time.

Domestic Consequences: Rationing, Queues, and Market Distortion

Inside Russia, the human and operational cost of the refinery crisis has become visible at the consumer level. Drivers in Chita reportedly waited as long as 39 hours in fuel queues. Filling stations in Krasnodar, Irkutsk, Pskov, and other regions closed or imposed purchase limits. Some stations reserved remaining fuel stocks exclusively for government and emergency service vehicles.

In a detail that illustrates the severity of local coordination breakdown, teachers in Krasnodar were reportedly assigned shifts at filling stations to help manage queue logistics, according to DW reporting. The paradox of a country producing millions of barrels of crude oil daily while its citizens queue for hours to purchase refined fuel encapsulates the structural vulnerability that Ukraine's campaign has exposed: crude in the ground is not the same as usable fuel at the pump, and the refining infrastructure connecting those two realities has been systematically degraded.

Can Russia's Refining Sector Recover?

Physical recovery of refinery infrastructure is theoretically possible. Russia has significant engineering capacity and financial motivation to restore processing throughput. However, several structural constraints complicate the recovery timeline:

- Active re-strikes prevent completion of repair cycles at already-damaged facilities, resetting restoration timelines repeatedly

- Sanctions restrictions on specialised refinery equipment and components create procurement bottlenecks that extend repair timelines beyond peacetime norms

- Market adaptation by export customers, who are now establishing alternative supply relationships with American, Indian, and Middle Eastern suppliers, may prove semi-permanent regardless of physical infrastructure restoration

- Simultaneous maritime pressure from tanker strikes constrains product distribution even where refining capacity remains functional

Even if Russia achieves full physical restoration of its refinery network, the commercial landscape it returns to will differ materially from the one that existed before the campaign began. Buyers who have successfully diversified supply chains rarely revert entirely to previous arrangements, particularly when the reliability of the original supplier has been demonstrated to be structurally vulnerable.

Three Scenarios for Global Diesel Markets Over the Next 12 Months

Scenario 1: Prolonged Disruption. Continued strikes prevent meaningful refinery restoration. Global diesel markets remain structurally tight through winter 2026–27, with elevated prices sustained and alternative supply chains becoming permanently embedded. European and Asian buyers accelerate long-term procurement contracts with non-Russian suppliers.

Scenario 2: Partial Recovery. A ceasefire or operational pause allows partial refinery restoration. Russian diesel exports resume at reduced volumes, providing modest market relief but insufficient to fully replace pre-conflict supply levels. Price normalisation is gradual and incomplete.

Scenario 3: Compounding Shock. Simultaneous escalation in Middle East supply disruptions deepens the Russian withdrawal's impact, creating a dual-shock environment that pushes diesel prices toward levels not recorded since the 2022 energy crisis. This scenario carries the highest probability of demand destruction in price-sensitive emerging markets. Tracking crude oil price trends will be essential for assessing which scenario materialises over coming months.

This article contains forward-looking analysis and scenario projections based on publicly available data as of mid-July 2026. Energy market conditions are subject to rapid change. Nothing in this article constitutes financial or investment advice.

Key Summary Statistics

| Indicator | Data Point |

|---|---|

| Russian crude processing rate (early July 2026) | 3.91 million bpd, a 21-year low |

| Decline vs. prior year average | -1.4 million bpd |

| Refineries struck | At least 24 of 34 large facilities |

| Total attacks conducted | ~50 over approximately 100 days |

| June 2026 fuel exchange volumes vs. June 2025 | -38% |

| June 2026 exchange prices vs. June 2025 | +37% |

| European diesel refining margins post-ban | Above $60 per barrel |

| Russian jet fuel deliveries to Central Asia (May to June 2026) | -92% |

| Gasoline imports from Belarus (first 25 days of June) | 141,000 tonnes, 2.4 times May total |

| Russian gasoline production vs. summer demand | ~65% coverage |

For ongoing coverage of global energy market dynamics and the Russia-Ukraine conflict's energy impact, detailed analysis across all major supply disruption themes continues to evolve. In addition, the broader consequences for global fuel supply chains remain a critical area of focus for energy market participants worldwide.

Want to Stay Ahead of the Next Major Commodity Market Shift?

When geopolitical shocks like Russia's refinery crisis ripple through global energy and commodity markets, the window for decisive investment action can close in hours — Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries so subscribers can act before the broader market catches up. Explore historic discovery returns that demonstrate what early positioning can mean for investors, and begin a 14-day free trial at Discovery Alert to secure your market-leading edge.