June 7, 2026

Ukraine's mineral sector has emerged as a strategic focal point in 2026, with the woman behind Ukraine's minerals push driving unprecedented international cooperation to unlock the country's vast geological resources. This transformation reflects broader shifts in critical minerals energy security priorities, as Western allies seek alternatives to concentrated supply chains that have created systemic vulnerabilities.

Strategic Mineral Dependencies: The Global Chess Game Reshaping Security

Critical mineral supply chains have become the invisible foundation upon which modern economic security rests. As nations grapple with technological sovereignty and green energy transitions, the geographic concentration of essential resources has transformed from a commercial concern into a strategic vulnerability. The concentration of rare earth processing in single regions, lithium extraction in politically unstable zones, and titanium production in conflict-affected areas has created systemic risks that policymakers are only beginning to understand.

This strategic reality has prompted a fundamental reassessment of resource diplomacy, forcing Western allies to confront uncomfortable dependencies that decades of globalisation have embedded deep within their industrial ecosystems. The search for alternative supply sources has intensified dramatically as geopolitical tensions expose the fragility of just-in-time mineral procurement strategies.

When big ASX news breaks, our subscribers know first

What Makes Ukraine's Mineral Resources Strategically Valuable in 2026?

Quantifying Ukraine's Untapped Critical Mineral Reserves

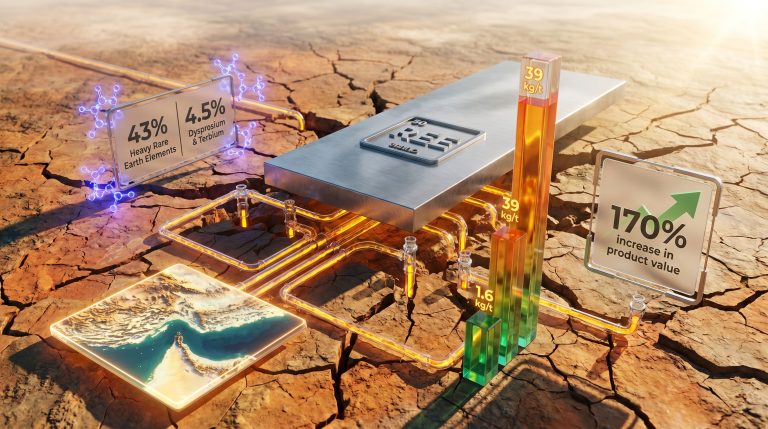

Ukraine's geological endowment represents one of Europe's most significant underdeveloped mineral provinces, with extensive Soviet-era surveys indicating substantial deposits across multiple critical mineral categories. The country holds approximately 5% of global rare earth element reserves, concentrated primarily in the Azov Sea coastal regions and central Ukrainian shield formations.

| Mineral Type | Ukraine Reserves | Global Ranking | Key Deposits |

|---|---|---|---|

| Titanium | 20% of world reserves | #1 globally | Irshansk, Volnogorsk |

| Lithium | 500,000 tonnes estimated | Top 10 globally | Kryvyi Rih basin |

| Rare Earth Elements | 5% of global reserves | #6 globally | Azov coastal zone |

| Uranium | 44,000 tonnes | #8 globally | Central shield region |

The Kryvyi Rih basin contains lithium concentrations averaging 0.8% lithium oxide, comparable to major Australian deposits but requiring different extraction methodologies due to the hardrock geological environment. These formations extend across approximately 1,200 square kilometres of accessible territory, representing potential lithium carbonate equivalent production of 50,000 tonnes annually at full development.

Titanium resources present the most immediate commercial opportunity, with the Irshansk deposit containing rutile concentrations exceeding 4% in proven zones. Historical Soviet extraction focused on lower-grade areas, leaving higher-concentration zones undeveloped due to technological limitations that modern processing methods have since overcome.

Geopolitical Supply Chain Dependencies

Current global critical mineral supply chains exhibit dangerous concentration risks that Ukraine's development could help mitigate. China controls 87% of rare earth processing capacity globally, while Chile and Australia dominate lithium production with combined market shares exceeding 70%. This concentration creates vulnerability points that strategic planners increasingly view as unacceptable.

Ukraine's geographic position offers direct rail and shipping access to European markets within 48-72 hours, compared to 4-6 week shipping times from major Asian producers. This proximity advantage becomes strategically valuable when considering supply chain resilience requirements for defence applications and renewable energy infrastructure.

The European Green Deal objectives require 30 times more lithium and 5 times more rare earth elements by 2030 compared to current consumption levels. Ukrainian production could supply up to 15% of European lithium demand and 8% of rare earth requirements if deposits reach projected development scales.

Furthermore, NATO allies face particular strategic exposure in titanium markets, where Russian and Ukrainian production historically supplied 40% of aerospace-grade titanium to Western manufacturers. Restoring Ukrainian production capacity would restore critical supply redundancy for defence contractors and commercial aerospace companies.

How Will the US-Ukraine Minerals Partnership Transform Exploration?

Financial Structure and Investment Framework

The $150 million joint reconstruction fund operates through a sophisticated risk-sharing mechanism designed to accelerate exploration while protecting investor interests. The fund structure allocates 60% for direct geological surveys, 25% for infrastructure development, and 15% for regulatory framework establishment.

Revenue-sharing arrangements follow a 50-50 split model for new discoveries, excluding existing Soviet-era deposits that remain under Ukrainian state control. This structure incentivises exploration of previously unmapped areas while respecting Ukrainian sovereignty over historically developed resources.

Risk-adjusted return calculations for international investors suggest internal rates of return between 18-25% for successfully developed projects, assuming 5-7 year development timelines and current critical mineral pricing. These projections incorporate 20% risk premiums for ongoing security concerns and regulatory uncertainties.

Private equity participation requirements include minimum 10-year investment commitments and technology transfer obligations to Ukrainian partners. This structure ensures knowledge transfer beyond simple capital injection, building long-term domestic capabilities in modern mining techniques.

Technical Modernisation of Soviet-Era Data

Historical geological surveys from the 1970s-1980s provide extensive baseline data but require significant updating to meet modern exploration standards. Soviet methodologies emphasised broad regional assessments over detailed deposit characterisation, creating information gaps that contemporary exploration must address.

| Survey Aspect | Soviet Era (1980s) | Modern Requirements |

|---|---|---|

| Grid Spacing | 500m-1km intervals | 25m-100m precision |

| Depth Analysis | Surface to 200m | 500m+ penetration |

| Geochemical Analysis | 12 elements standard | 45+ elements required |

| Data Processing | Manual interpretation | AI-assisted modelling |

Partnership countries contribute specialised technologies: US geological survey methods focus on deep penetration techniques, German partners provide advanced geochemical analysis, Canadian expertise emphasises resource calculation standards, while UK contributions centre on environmental impact assessment.

The drilling-focused approach prioritises confirmation of historical estimates over entirely new discovery, reducing exploration risk while upgrading resource classifications to international standards. Modern drilling programmes target 150-200 metre depths compared to typical 50-75 metre Soviet surveys.

However, advanced technologies including LiDAR mapping, hyperspectral imaging, and AI-assisted geological modelling provide capabilities unavailable during Soviet exploration periods. These tools enable identification of structural patterns that suggest additional mineral occurrences beyond historically mapped zones.

Which Regions Offer the Highest Development Potential?

Territory-Based Risk Assessment Matrix

Security considerations fundamentally shape development priorities, with accessible territories receiving priority attention regardless of absolute resource quality. The risk assessment framework evaluates proximity to conflict zones, infrastructure integrity, and workforce availability as primary factors.

Central Ukrainian regions including Kirovohrad and Cherkasy oblasts offer the highest security ratings combined with significant lithium potential. These areas remain 150+ kilometres from active conflict zones while maintaining functional rail connections to western Ukraine and European markets.

Western Ukraine's mineral zones provide maximum security but contain lower-grade deposits primarily focused on construction materials and industrial minerals. Development in these regions serves proof-of-concept purposes while building operational experience for higher-value eastern deposits.

| Region | Security Rating | Infrastructure Status | Primary Minerals | Development Priority |

|---|---|---|---|---|

| Kirovohrad | High | 85% functional | Lithium, Uranium | 1st Phase |

| Cherkasy | High | 90% functional | Rare Earths | 1st Phase |

| Dnipro | Medium | 70% functional | Titanium | 2nd Phase |

| Zaporizhzhia | Low | 30% functional | Iron, Titanium | 3rd Phase |

Infrastructure readiness varies significantly across potential development zones. Power grid stability remains problematic in eastern regions, requiring distributed generation solutions or grid reconstruction before large-scale mining operations become feasible.

Priority Mineral Targets for 2026 Exploration

Rare earth element deposits in the Azov coastal zones contain monazite concentrations suitable for commercial extraction, though security constraints limit immediate access. Geological modelling suggests 150,000 tonnes of rare earth oxides in proven reserves within 20 kilometres of current access points.

In addition, titanium resources offer the most immediate development potential due to established Soviet-era processing infrastructure that requires modernisation rather than complete reconstruction. The Irshansk deposit alone could support 100,000 tonnes annual production of titanium concentrate within 3-4 years of development commencement.

Lithium extraction feasibility depends on technology selection between traditional hardrock processing and experimental direct extraction techniques. Hardrock methods require significant water resources but utilise proven technology, while direct extraction reduces environmental impact but remains commercially unproven at scale.

Market demand projections for 2027-2030 suggest European lithium requirements of 400,000 tonnes lithium carbonate equivalent annually, creating substantial market opportunity for Ukrainian production. Current global production capacity will fall 200,000 tonnes short of projected demand by 2029.

What Are the Investment Scenarios for Ukraine's Mineral Sector?

Reconstruction-Linked Development Models

Mining revenue integration with post-war reconstruction programmes creates unique investment structures linking resource extraction profits to infrastructure rebuilding projects. This model ensures mineral development contributes directly to economic recovery rather than extractive colonial patterns.

According to the Atlantic Council analysis, timeline projections anticipate exploration completion by late 2026, development decisions through 2027, with initial production beginning 2028-2029 for priority deposits. Full-scale production across multiple deposits reaches projected levels 2030-2032, assuming continued security improvements.

Economic multiplier effects from mineral sector development could contribute 2-3% to Ukrainian GDP by 2030, with indirect employment supporting 50,000-70,000 jobs across processing, transportation, and support services. These projections assume successful integration with European supply chains and stable security conditions.

Revenue allocation mechanisms direct 40% of mining profits toward reconstruction bonds, 35% to private investors, and 25% to Ukrainian state budgets. This structure ensures reconstruction funding while maintaining commercial viability for international partners.

International Partnership Risk-Reward Analysis

Western allies' strategic benefits include reduced Chinese dependence for critical minerals, enhanced supply chain resilience, and geopolitical influence in Eastern European energy security. These strategic advantages justify higher risk tolerance than purely commercial investments might warrant.

Ukrainian economic sovereignty considerations require technology transfer obligations and domestic capacity building to prevent extractive colonialism. Partnership agreements include mandatory training programmes, equipment manufacturing partnerships, and processing facility development within Ukraine.

Consequently, comparative analysis with post-conflict resource development in Kosovo, Bosnia, and Iraq suggests 5-8 year timelines for stable commercial production, with security improvements being the critical path variable. Successful cases demonstrate annual returns of 15-25% for patient capital willing to absorb initial political risk.

Risk mitigation strategies include political risk insurance, multilateral development bank participation, staged investment tranches, and exit clause provisions tied to security deterioration metrics. These protections enable private capital participation despite ongoing uncertainties.

How Could This Strategy Impact Global Critical Mineral Markets?

Supply Chain Diversification Scenarios

Market share redistribution modelling indicates Ukrainian production at full capacity could supply 8-12% of European critical mineral demand by 2032, reducing Chinese market dominance from 87% to 75% in rare earth processing for European consumers.

Price impact analysis suggests moderate downward pressure on critical mineral prices as Ukrainian supply increases global production capacity by 3-5% across target minerals. However, growing demand from renewable energy expansion likely offsets supply increases, maintaining price stability rather than dramatic reductions.

Timeline for meaningful global supply contribution requires 8-10 years from exploration initiation to significant market impact. Initial production by 2028-2029 provides regional supply diversification for European markets before global market effects become measurable.

For instance, supply security improvements for NATO allies become immediately valuable regardless of absolute production volumes, as alternative sourcing options reduce strategic vulnerability even at relatively modest scales.

Competitive Response from Existing Producers

China's potential strategic reactions include accelerated African mining investments, increased stockpiling, technology export restrictions, and pricing strategies designed to undercut Ukrainian production economics. These responses could intensify competition for global mineral markets.

Australia's complementary opportunities emerge through processing partnerships with Ukrainian raw materials, leveraging established refining capacity to add value to Ukrainian concentrates before final market delivery.

Furthermore, long-term implications for critical mineral diplomacy include enhanced Western negotiating positions, reduced coercive leverage for resource-controlling states, and increased importance of technological capabilities over raw material access as competitive advantages.

Market structure evolution trends toward regional supply chains rather than globally optimised systems, prioritising security and resilience over pure cost efficiency in strategic mineral sourcing.

The next major ASX story will hit our subscribers first

What Challenges Could Derail Ukraine's Mineral Ambitions?

Security and Infrastructure Constraints

Ongoing conflict impacts on exploration activities include restricted access to prime geological zones, workforce safety concerns, equipment security risks, and insurance cost premiums that increase project economics by 15-25% compared to stable jurisdictions.

Energy grid stability requirements for mining operations demand reliable power supply for processing equipment, ventilation systems, and materials handling. Current grid reliability in target regions averages 60-70%, requiring backup generation or grid improvements before commercial operations.

Transportation corridor security affects mineral export logistics, with rail lines to western Ukraine experiencing periodic disruptions requiring flexible routing and increased inventory management. Sea access through Romanian and Polish ports adds transportation costs but provides export security.

However, insurance and financing costs reflect political risk premiums of 8-12% above normal commercial rates, significantly impacting project economics and requiring careful financial structuring to maintain commercial viability.

Technical and Regulatory Hurdles

Environmental compliance frameworks must balance wartime pragmatism with international mining standards, creating regulatory uncertainty that complicates permitting timelines and operational planning. Expedited approval processes risk future compliance challenges.

International mining standards implementation requires regulatory harmonisation with EU directives, NATO requirements, and partner country standards while maintaining Ukrainian sovereignty over domestic resource policy.

Workforce development needs include training programmes for modern mining techniques, safety protocols, environmental management, and equipment operation. Soviet-era mining experience provides basic foundations but requires substantial updating for contemporary operations.

Technology transfer obligations create intellectual property challenges as international partners balance competitive advantages with partnership requirements for knowledge sharing and domestic capability building.

Global Strategic Implications and Market Outlook

Policy Alignment with Strategic Minerals Framework

The woman behind Ukraine's minerals push has successfully aligned these initiatives with broader Western critical minerals policy analysis, creating synergies across multiple jurisdictions. This coordination reflects growing recognition that resource security requires multilateral approaches rather than unilateral strategies.

Resource security partnerships increasingly mirror defence alliances, with mineral access agreements becoming as strategically important as traditional security arrangements. The Ukrainian model demonstrates how resource diplomacy can advance multiple strategic objectives simultaneously.

European Union alignment with Ukrainian mineral development supports broader strategic autonomy objectives while reducing dependence on authoritarian regimes for critical inputs. This alignment strengthens both Ukrainian sovereignty and European resource security.

Comparative Regional Development Models

Australian parallels in lithium industry innovations provide proven frameworks for scaling mineral production while maintaining environmental standards. These experiences offer valuable lessons for Ukrainian development planning and regulatory framework design.

Similarly, uranium market dynamics demonstrate how geopolitical factors can rapidly reshape commodity markets, validating the strategic importance of diversified supply sources for nuclear fuel cycles.

The strategic antimony outlook reveals similar patterns where strategic minerals become geopolitical tools, reinforcing the importance of securing alternative sources before supply disruptions materialise.

Long-Term Market Evolution Scenarios

Supply chain regionalisation trends suggest Ukrainian mineral development occurs within broader restructuring of global commodity flows away from concentrated Asian production toward distributed regional networks emphasising security over efficiency.

The Deutsche Welle report indicates that this strategic shift represents a fundamental change in how democratic nations approach resource security, moving from purely commercial considerations to strategic planning frameworks.

Technology integration with mineral development creates opportunities for Ukrainian expertise in digital mining technologies, automated processing systems, and environmental monitoring that could generate intellectual property value beyond raw material exports.

Frequently Asked Questions About Ukraine's Mineral Strategy

When Will Ukraine's Mineral Production Begin?

Exploration phases continue through late 2026, with development decisions expected 2027. Initial production from priority deposits could commence 2028-2029, reaching commercial scales by 2030-2031. Timeline achievement depends critically on security improvements and infrastructure restoration.

Phased development approaches prioritise lower-risk, higher-value deposits in secure territories before expanding to higher-potential zones in currently contested regions. This strategy enables early revenue generation while building operational experience.

How Will Revenue Sharing Work with International Partners?

Revenue distribution follows 50-50 partnerships for new discoveries, with Ukrainian partners retaining majority stakes in existing Soviet-era deposits. International investors receive operational management rights and technology licensing arrangements as value creation mechanisms.

Profit reinvestment requirements direct minimum percentages toward infrastructure improvements, workforce development, and environmental compliance, ensuring sustainable development rather than extractive exploitation.

Which Minerals Offer the Greatest Export Potential?

Titanium concentrates provide immediate export opportunities due to established processing infrastructure and strong European demand from aerospace and chemical industries. Export potential reaches 100,000 tonnes annually within 5 years.

Lithium production offers highest long-term value due to battery industry growth, but requires significant processing investment and longer development timelines. European market demand could absorb entire Ukrainian production capacity at projected development scales.

Rare earth elements present strategic value exceeding commercial returns, as supply diversification benefits justify development support even at marginal economic returns compared to Chinese production costs.

This analysis is provided for informational purposes and does not constitute investment advice. Critical mineral markets involve significant political, economic, and operational risks that investors should carefully evaluate. Projections regarding Ukrainian mineral development depend on security improvements and regulatory developments that remain uncertain.

Looking to Capitalise on Critical Minerals Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Explore why major mineral discoveries can generate substantial returns and begin your 14-day free trial today to position yourself ahead of the market.