July 11, 2026

The Nuclear Fuel Market's Hidden Architecture: Why Jurisdiction Now Outranks Price

Most commodity markets reset daily. Traders respond to inventory data, shipping rates, and macroeconomic signals, adjusting positions accordingly. Uranium operates on an entirely different clock. Once a nuclear reactor is commissioned, its operator enters a procurement cycle measured in decades, not quarters. Fuel must be secured years in advance, processed through multiple conversion and enrichment stages, and delivered on schedules that cannot flex without enormous operational consequence. This structural rigidity transforms the concept of supply reliability from a preference into an operational imperative, and in 2026, that imperative is reshaping how uranium supply constraints and stable-jurisdiction supply are valued across global nuclear fuel markets.

When big ASX news breaks, our subscribers know first

Two Prices, One Market Signal

Uranium pricing operates through two parallel benchmarks that most investors outside the sector rarely distinguish. The spot price reflects prompt-delivery transactions in a notoriously thin market where even modest trade volumes can produce significant price swings. The long-term contract price, reported by independent consultancies UxC and TradeTech, reflects the multi-year utility agreements that actually govern most of the world's nuclear fuel procurement.

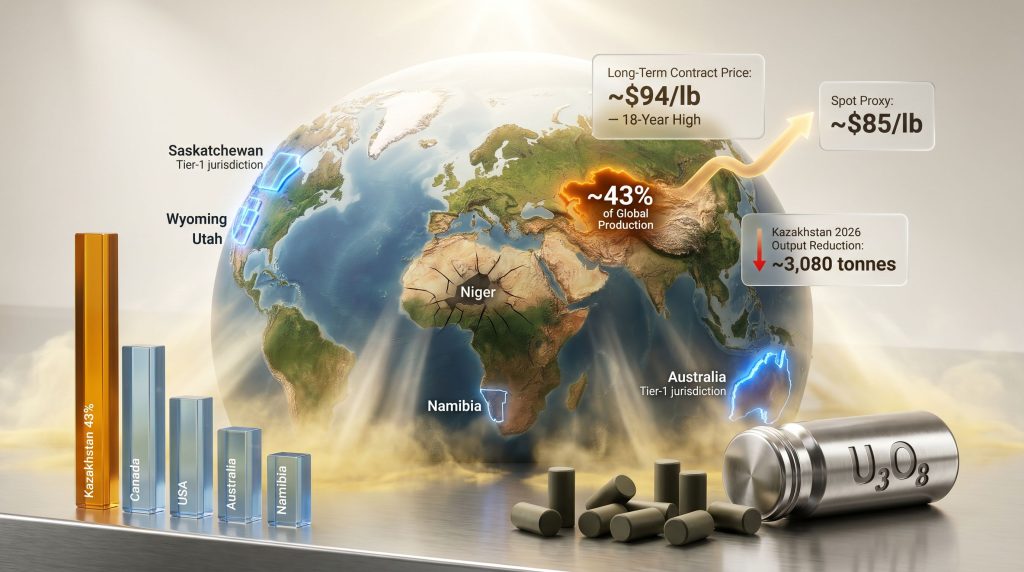

In the first quarter of 2026, these two benchmarks told a diverging story. TradeTech's long-term uranium indicator reached $93.00 per pound at the end of March 2026, up $6.50 from December 2025 and the highest reading in more than 18 years. UxC reported a comparable figure near $94 per pound. The spot proxy, by contrast, remained range-bound near $85 per pound.

| Benchmark | Price (Q1 2026) | Reporting Source | Market Function |

|---|---|---|---|

| Spot Proxy | ~$85/lb | UxC / TradeTech | Prompt delivery reference |

| Long-Term Contract Price | ~$94/lb | UxC / TradeTech | Multi-year utility contracts |

| New Mine Incentive Floor | $60–$70/lb | Industry consensus | Minimum to justify construction |

| Next-Wave Capacity Threshold | ~$100+/lb | Analyst estimates | Level needed to fund new mines |

The approximately $9 premium between term and spot pricing is not a market anomaly. It is a signal that utilities are paying a structural scarcity premium to lock in future delivery certainty rather than depending on a thin spot market that cannot guarantee volume. Philip Williams, Chief Executive Officer of IsoEnergy, has noted that long-term contracts are in practice being executed at prices that even the reported $94 figure does not fully capture, and that uranium equities are not yet reflecting this underlying pricing reality. According to Williams, a term price at that level represents a compelling market signal that the fundamental backdrop has materially improved.

Kazakhstan: The World's Largest Producer and Its Growing Constraints

No analysis of uranium supply constraints can avoid the central role of Kazakhstan. The country accounts for approximately 43% of global primary uranium production, making it the single largest and lowest-cost source in the world. It is also, increasingly, the single largest point of concentration risk for Western utilities. Understanding the broader uranium supply and demand picture makes this concentration risk all the more striking.

In 2026, Kazakhstan's state producer revised its nominal output target downward from 32,777 tonnes to 29,697 tonnes, a reduction of roughly 3,080 tonnes or approximately 5% of global primary production. This was not a demand-driven adjustment. It reflected a deliberate reallocation toward higher-value sales channels and state-controlled distribution.

The ownership dimension compounds the supply picture further. Amendments to Kazakhstan's subsoil code now require that its state producer hold at least 75% ownership in any production-right transfer and at least 90% in exploration rights at producing deposits. This effectively narrows the access that Western joint-venture partners previously held to some of the world's most cost-efficient uranium resources. The Budenovskoye joint venture's output, meanwhile, is committed entirely to the Russian civil nuclear industry, placing it entirely outside the supply pool available to Western utilities.

The Sulfuric Acid Dependency: Kazakhstan's Overlooked Operational Vulnerability

A lesser-known but critically important dimension of Kazakhstan's supply risk involves the chemistry of how its uranium is actually extracted. Virtually all of Kazakhstan's output is produced through in-situ recovery (ISR), a technique that injects acidified solution into uranium-bearing sandstone formations to dissolve the mineral underground before pumping it to the surface. These in-situ recovery methods, however, carry a significant and often overlooked logistical vulnerability.

The acid of choice is sulfuric acid, and Kazakhstan requires enormous volumes of it to sustain production. Approximately one-fifth of global sulfur shipments transit the Strait of Hormuz. When renewed disruption affected the Strait in early July 2026, it highlighted an operational fragility embedded deep in the supply chain of the world's most dominant uranium producer. A sustained disruption lasting even 60 to 90 days could meaningfully constrain acid deliveries, compress Kazakhstani output, and accelerate the term price premium for supply originating from stable, acid-independent jurisdictions.

Scenario Risk: The dependence of Kazakhstan's ISR operations on sulfuric acid routed through geopolitically exposed shipping lanes represents one of the most underappreciated supply-chain vulnerabilities in the global uranium market. It is not reflected in most supply-deficit models.

Niger's Stranded Supply and the ICSID Complication

While Kazakhstan represents an active constraint, Niger represents a supply source that has been effectively removed from the Western market entirely. The SOMAIR mine, formerly operated by Orano, produced zero uranium in 2025 following nationalisation by the country's military-led government.

The situation is further complicated by a September 2025 ruling from the World Bank's International Centre for Settlement of Investment Disputes (ICSID), which placed a legal block on the sale or transfer of a disputed stockpile estimated at between 1,150 and 1,500 tonnes of uranium. This material, previously accessible to Western buyers, now sits in regulatory limbo, neither available to the market nor formally resolved. That volume represents a meaningful reduction in accessible supply for utilities that previously relied on Francophone African sources.

| Supply Disruption | Volume Affected | Status |

|---|---|---|

| Kazakhstan 2026 output reduction | ~3,080 tonnes | Confirmed |

| Niger SOMAIR 2025 production | 0 tonnes | Stranded |

| Niger SOMAIR stockpile (ICSID blocked) | 1,150–1,500 tonnes | Legally frozen |

| Budenovskoye JV output (Russia-committed) | Undisclosed | Outside Western market |

Geopolitical Competition and the Rising Value of Stable-Jurisdiction Supply

The tightening of supply from Kazakhstan and Niger is not happening in a vacuum. A parallel competition is intensifying among major nuclear powers to secure long-term uranium supply through bilateral agreements and strategic relationships. Furthermore, the Russian uranium import ban has added another layer of complexity, further narrowing the pool of accessible supply for Western utilities.

Phil Hoskins, Chief Executive Officer of Atomic Eagle, has observed that uranium is increasingly becoming a geopolitical contest, with the United States producing only around 2% of its own uranium requirements while India and China are actively locking up long-term supply through dedicated agreements with the world's largest producers. China, in particular, has been constructing approximately 10 new reactors per year over recent years, creating a sustained forward demand that progressively absorbs available supply.

This dynamic is creating a tiered valuation structure for uranium assets based on jurisdiction:

| Jurisdiction Tier | Examples | Risk Profile | Utility Preference |

|---|---|---|---|

| Tier 1 – Stable | Canada, USA, Australia, Namibia | Low | High and rising |

| Tier 2 – Moderate | Zambia, Tanzania, Uzbekistan | Medium | Selectively increasing |

| Tier 3 – Restricted / Volatile | Kazakhstan (state-controlled), Niger (nationalized) | High | Actively diversifying away |

Hoskins has articulated the competitive logic clearly: credible near-term production pounds located in genuinely stable jurisdictions are becoming scarce precisely because the jurisdictions that previously supplied most of the world's uranium are either tightening access or exiting the Western supply chain altogether.

Demand: Beyond the Traditional Utility Procurement Cycle

While supply constraints tighten, demand is expanding across multiple vectors simultaneously.

Four privately built reactors reached criticality by the July 4, 2026 target established under a US executive order, converting previously announced nuclear projects into operating facilities with active long-term fuel procurement requirements. Utilities that deferred contracting in earlier years now carry uncovered fuel positions, meaning uranium required for future reactor operations remains uncontracted and must eventually be purchased at whatever market price prevails.

The AI-driven demand vector adds a structurally new layer to this picture. AI data centres require high-density, uninterrupted electricity supply that intermittent renewable sources cannot consistently provide. Hyperscalers securing long-term nuclear power agreements embed decades-worth of uranium fuel requirements into those contracts, extending procurement horizons well beyond traditional utility cycles. This demand is additive to existing utility contracting, not a substitute for it.

| Demand Driver | Near-Term Impact | Long-Term Impact |

|---|---|---|

| Existing reactor fleet (uncovered positions) | High | Moderate |

| New conventional reactor builds | Moderate | High |

| AI-driven hyperscaler nuclear agreements | Low-Moderate | High |

| Small modular reactors (SMRs) | Low | High |

| Reactor restarts (Japan, Europe) | Moderate | Moderate |

The next major ASX story will hit our subscribers first

Producer Economics: Capturing Value From Higher Contract Prices

Producers already operating under multi-year utility contracts are the first segment of the value chain to capture the financial benefit of rising long-term pricing.

Energy Fuels operates the only conventional uranium mill in the United States and has reported processing costs of $9 to $12 per pound and mining costs of $23 to $30 per pound at its Pinyon Plain mine, against a 2025 realised sales price of $74.20 per pound. Chief Executive Officer Mark Chalmers has described the business as generating cash at low cost with a genuinely unique competitive position, noting that the supply-demand deficit story is expected to drive uranium prices materially higher in the near term.

enCore Energy increased first-quarter 2026 uranium extraction by 22% year over year to 90,000 pounds, realising an average sales price of $67.78 per pound. Executive Chairman William Sheriff has pointed to scale as the critical dividing line within the ISR producer segment, arguing that operations producing less than one million pounds per year face structural disadvantages in credit markets and contract negotiations. In his view, scale reduces the cost of capital and strengthens the commercial position of producers in long-term utility discussions.

| Producer | Key Asset | Processing Cost | Mining Cost | 2025/Q1 2026 Realised Price |

|---|---|---|---|---|

| Energy Fuels | Pinyon Plain, USA | $9–$12/lb | $23–$30/lb | $74.20/lb (2025) |

| enCore Energy | South Texas ISR | Variable (ISR) | Variable (ISR) | $67.78/lb (Q1 2026) |

Development Assets: Where Future Uranium Supply Will Come From

The deficit through 2040 cannot be closed by existing mines alone. The next tranche of global uranium supply must originate from development-stage projects currently advancing through feasibility studies, environmental approvals, and permitting processes. Consequently, understanding the distribution of global uranium reserves has become a critical input for utilities and investors alike when evaluating which projects are most likely to close the looming supply gap.

IsoEnergy's Hurricane deposit in Saskatchewan contains an indicated resource of 48.6 million pounds grading 34.5% U₃O₈, placing it among the highest-grade indicated uranium deposits anywhere in the world. The company holds approximately C$130.5 million in cash to fund studies across assets in three jurisdictions. Philip Williams has highlighted the disconnect between the current term pricing environment and equity market valuations, suggesting that the market has not yet priced the full implications of contracts being executed above even the reported $94 per pound headline figure.

Atomic Eagle's Muntanga project in Zambia presents a different but complementary development geometry. The project holds a 58.8-million-pound resource grading 309 parts per million U₃O₈. While the grade is substantially lower than Saskatchewan-style high-grade unconformity deposits, the shallow geometry of the mineralisation supports a relatively straightforward heap-leach extraction method, which reduces capital intensity and simplifies the permitting pathway compared to underground mining operations. The project advanced toward formal permitting after securing environmental and resettlement approvals in mid-2026.

At the earliest stage of the supply pipeline, ATHA Energy controls more than 7 million acres across Canada's uranium basins and funded a roughly 20,000-metre drill program in 2026 through a C$63 million financing. Radiometric readings in counts per second identify exploration targets but are not equivalent to assayed mineral resources. ATHA's Chief Executive Officer Troy Boisjoli has described the current uranium market as the most constructive environment he has encountered across two decades of operating in the sector.

| Development Stage | Example | Resource Defined | Key Risk | Upside Potential |

|---|---|---|---|---|

| Producer | Energy Fuels, enCore Energy | Yes | Execution, cost overruns | Moderate |

| Developer (high-grade) | IsoEnergy (Hurricane) | Yes, 48.6Mlb @ 34.5% | Permitting, financing | High |

| Developer (bulk-tonnage) | Atomic Eagle (Muntanga) | Yes, 58.8Mlb @ 309ppm | Permitting, heap-leach execution | High |

| Explorer | ATHA Energy | No (radiometric targets) | Geological, financing, dilution | Very High |

The Valuation Gap: Why Uranium Equities Are Lagging an 18-Year-High Contract Price

One of the more unusual features of the current uranium market is the persistent gap between what long-term contracts are being executed at and what uranium equities are implying about the value of underlying assets. According to analysts at Crux Investor, this disconnect is actively spotlighting exploration companies as potential beneficiaries should equities eventually catch up with contract pricing. Several overlapping forces explain this disconnect:

- Interest rate headwinds: The US Federal Reserve's policy rate of 3.50% to 3.75% compresses the present value of future cash flows, disproportionately affecting pre-revenue developers whose entire investment case rests on projected production years in the future.

- Execution skepticism: Uranium mine restarts over the past two to three years have repeatedly missed announced production targets, leaving equity markets cautious about timelines even when pricing is supportive.

- Secondary supply uncertainty: Inventory drawdowns and material reclassification can extend secondary supply availability, potentially moderating the term premium without an improvement in primary mine output.

- Contract reporting opacity: A known feature of long-term uranium contracting is that actual transaction prices are frequently not publicly disclosed. Reported benchmarks like the UxC and TradeTech indicators are composite estimates, not exchange-cleared prices, which makes it difficult for equity markets to anchor valuations precisely.

Investor Caution: Uranium equities remain among the most volatile instruments in the resources sector. Developers and explorers carry dilution risk, permitting uncertainty, and execution risk. Even in a structurally supportive market environment, contract prices, project timelines, and equity valuations are unlikely to move in a straight line. Individual positions can still result in capital loss regardless of the commodity price backdrop.

Principal Risks to the Supply Constraint Thesis

A structurally bullish market narrative should always be stress-tested against scenarios where the thesis does not play out as anticipated.

Risk 1: Utility contracting delays. If large utilities continue deferring long-term purchases and lean on secondary supply sources longer than expected, the term price premium could compress without any fundamental improvement in primary mine output.

Risk 2: Interest rate persistence. A higher-for-longer rate environment mechanically reduces valuations for pre-revenue companies whose investment thesis depends entirely on future cash flows. This risk is most acute for exploration and early-stage development companies.

Risk 3: Mine execution failures. Higher prices do not automatically produce additional supply. Permitting timelines, workforce availability, reagent supply chains, and geological surprises all introduce execution risk that the equity market has already penalised repeatedly.

Risk 4: Geopolitical resolution. Disruptions in Kazakhstan and Niger have tightened the accessible supply pool. However, an unexpected policy reversal — such as a restoration of the SOMAIR operating licence or a modification to Kazakhstan's joint-venture ownership rules — could return supply to the market faster than current models anticipate. The uranium market dynamics driving today's premiums could therefore shift more quickly than investors expect.

The uranium market in 2026 presents a genuinely unusual configuration: an 18-year-high long-term contract price sitting alongside equity valuations that have not yet reflected the underlying pricing environment, a supply chain increasingly concentrated in jurisdictions that are either restricting Western access or producing zero output, and a demand profile expanding from multiple directions simultaneously. The World Nuclear Association has consistently noted that primary supply alone is unlikely to meet projected demand growth through the coming decade without significant new mine development. The most durable competitive advantage in this environment is not the lowest production cost. It is the combination of a defined resource, a realistic development path, and an address in a jurisdiction where the rules of investment do not change overnight. That is precisely what uranium supply constraints and stable-jurisdiction supply have elevated to the top of utility procurement priorities, and it is unlikely to reverse quickly regardless of how spot markets behave in the near term.

Want to Capitalise on Uranium's Tightening Supply Landscape Before the Market Catches Up?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex resource data into actionable investment insights for both short-term traders and long-term investors. Explore how historic mineral discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the broader market.