June 24, 2026

Global energy markets face an unprecedented transformation as traditional fossil fuel dependencies clash with climate imperatives and national security concerns. Power demand surges driven by artificial intelligence infrastructure and electrification trends force utilities worldwide to confront a stark reality: renewable intermittency cannot sustain baseload requirements without massive storage investments that remain economically prohibitive. This convergence has elevated nuclear power from a niche energy source to a strategic necessity, fundamentally altering uranium market dynamics and creating a sustained uranium supply deficit that extends far beyond typical commodity cycles.

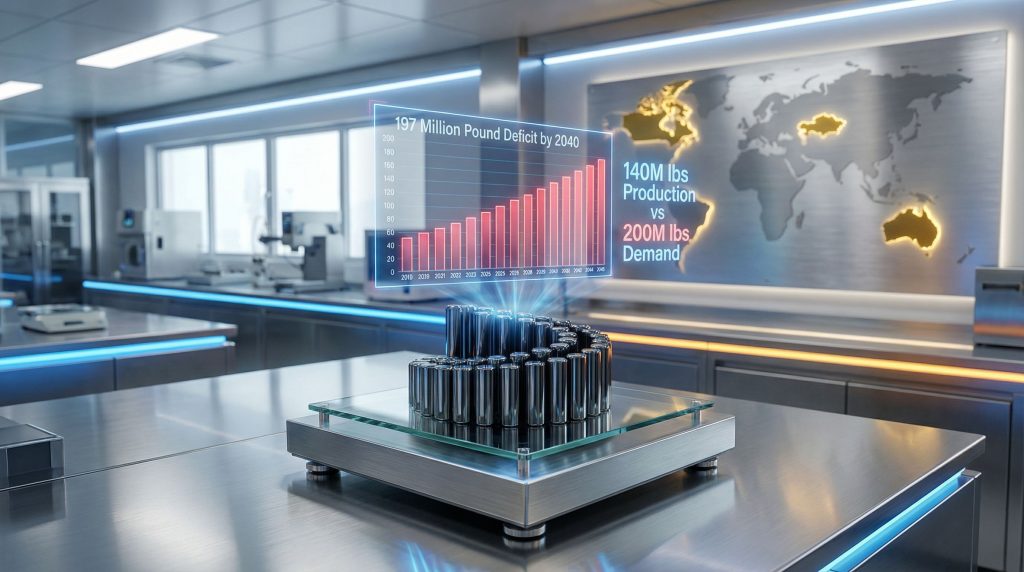

Understanding Uranium Market Fundamentals and Supply Constraints

The uranium supply deficit represents more than a temporary market imbalance. Current global production delivers approximately 140 million pounds annually while reactor fuel demand continues climbing toward 200 million pounds, creating a persistent 20-30% shortfall between mining output and consumption requirements. This gap has been temporarily masked by strategic inventory drawdowns accumulated during Japan's post-Fukushima reactor shutdowns, but these buffer stocks have reached critically low levels.

Japan's resumption of uranium procurement in 2024 after 11 years of relying on accumulated reserves provides concrete evidence of inventory depletion. The world's former third-largest nuclear power producer had suspended most reactor operations following the Fukushima Daiichi disaster in March 2011. This strategic reserve exhaustion forces utilities globally to return to primary supply markets, eliminating the pricing cushion that masked underlying production constraints.

Projected Supply Gap Expansion Through 2040

Industry analysis projects the uranium supply deficit will expand dramatically over the next 15 years as new reactor construction accelerates and advanced nuclear technologies require specialised fuel forms:

| Period | Supply Deficit | Primary Demand Drivers |

|---|---|---|

| 2026-2030 | 85-120 million lbs | Existing reactor fleet expansions and restarts |

| 2031-2035 | 140-170 million lbs | New reactor construction programmes in Asia and North America |

| 2036-2040 | 197+ million lbs | Small Modular Reactor deployment and HALEU requirements |

The 197 million pound deficit projection by 2040 assumes current production capacity with modest expansion from existing operations. Furthermore, this scenario excludes potential supply disruptions from geopolitical tensions, environmental challenges, or regulatory delays that historically impact uranium mining operations.

Energy Density Advantages Drive Nuclear Adoption

Nuclear fuel's energy density provides compelling economic advantages over fossil fuel alternatives. A single 7-gram uranium fuel pellet generates equivalent energy to 800 kilograms of coal while producing zero direct carbon emissions. This energy concentration enables utilities to maintain baseload generation without the sulphur dioxide, particulate matter, or carbon emissions associated with coal-fired power plants.

According to Geoscience Australia data, nuclear facilities achieve capacity factors often exceeding 90%, compared to 20-35% for solar and wind installations. This reliability advantage becomes critical as power grids require consistent baseload generation to support industrial operations and emerging technologies like artificial intelligence data centres that demand 24/7 electricity supply.

When big ASX news breaks, our subscribers know first

Development Timeline Constraints and Production Bottlenecks

New uranium mining projects require 5-7 years minimum from final investment decision to commercial production, with regulatory approval processes often extending timelines by 2-3 additional years. This development duration reflects the specialised nature of uranium mining operations, which must satisfy environmental permitting requirements, indigenous consultation processes, and nuclear regulatory oversight that exceeds standard mining project approval frameworks.

The complexity of uranium project development creates several interconnected bottlenecks:

- Exploration and Resource Definition (Years 1-2): Drilling programmes and geological modelling to establish resource estimates

- Feasibility Study Phase (Years 2-4): Engineering studies and environmental impact assessments

- Permitting and Approvals (Years 3-5): Regulatory approvals and community consultation processes

- Capital Construction (Years 5-7): Infrastructure development and processing facility construction

- Production Ramp-up (Years 7-9): Operational optimisation and workforce training

Operational Performance vs Design Capacity

Global uranium production consistently operates at approximately 70% of theoretical nameplate capacity, representing a 30% efficiency gap between engineered specifications and actual commercial output. This performance shortfall stems from three primary operational challenges:

In-Situ Recovery (ISR) Operations: Water management limitations reduce extraction efficiency below design parameters, particularly during seasonal variations or aquifer pressure changes that affect solution flow rates through uranium-bearing ore bodies.

Conventional Mining Operations: Ore grade variability creates processing inconsistencies that require continuous adjustment of milling and extraction parameters. Consequently, this reduces overall throughput compared to steady-state design assumptions.

Processing Facility Maintenance: Required maintenance windows for specialised uranium processing equipment reduce effective annual production rates, as facilities must periodically shut down for safety inspections and equipment replacement.

Capital Investment Threshold Requirements

The uranium sector experienced a prolonged bear market from 2011-2020 that severely limited capital investment in new projects and mine expansions. Current uranium prices, while elevated from historical lows, remain insufficient to incentivise the massive capital commitments required for new large-scale operations.

Development projects require sustained uranium prices above $80-90 per pound to achieve acceptable returns on investment, given the high upfront capital costs and extended payback periods associated with uranium mining operations. Most major development projects require multi-hundred million dollar capital expenditures with 7-10 year payback periods, making them sensitive to long-term price visibility rather than short-term price spikes.

Geopolitical Concentration and Supply Chain Vulnerabilities

Two-thirds of global uranium production concentrates in just three countries: Kazakhstan (43%), Canada (13%), and Australia (12%). This geographic clustering creates systemic supply chain risks that extend beyond typical commodity market dynamics, as uranium serves as critical infrastructure for nuclear power generation with no readily available short-term substitutes.

"Only approximately one-third of global uranium production remains accessible to Western utilities, as substantial volumes flow to China and other non-Western nuclear programmes through long-term supply agreements, effectively reducing available supply for Western markets by roughly 67%."

Russian Enrichment Capacity Dependencies

Russia controls approximately 46% of global uranium enrichment capacity through Rosatom's facilities, creating strategic vulnerabilities for Western nuclear fuel cycles. The United States has implemented progressive restrictions on Russian uranium imports, culminating in a Russian uranium import ban by 2028, which eliminates Western access to Russia's commercial high-assay low-enriched uranium (HALEU) production.

This enrichment capacity concentration creates a bottleneck beyond primary uranium mining. While Western countries can access uranium from Australia, Canada, and Namibia, the conversion of natural uranium into reactor fuel requires specialised enrichment facilities that remain concentrated in geopolitically sensitive regions.

Recent Production Disruptions and Market Impact

Supply chain vulnerabilities manifest through periodic production disruptions that create immediate price pressure:

| Disruption Source | Production Impact | Market Response |

|---|---|---|

| McArthur River operational delays | 5-8% reduction in Canadian output | +$4/lb spot price movement within 30 days |

| Kazatomprom production guidance cuts | 3-5% global production reduction | Long-term contract premium expansion |

| Namibian operational constraints | 2-3% African production impact | Increased utility contracting activity |

These disruptions demonstrate how concentrated production creates price volatility that extends beyond the immediate supply impact, as utilities compete for alternative sources in a market with limited excess capacity.

Policy-Driven Demand Growth and Energy Security Priorities

The United States has committed to quadrupling nuclear energy capacity by 2050, which would require doubling current global uranium production solely to meet American demand growth. This policy-backed demand differs fundamentally from previous speculative uranium cycles, as it reflects long-term energy security strategies rather than short-term market speculation.

Current U.S. nuclear capacity of approximately 95 gigawatts would expand to roughly 380 gigawatts under this policy framework, requiring an additional 285 gigawatts of new nuclear generation. This expansion timeline creates sustained uranium demand that utilities must secure through long-term contracts, reducing available supply for other global markets.

Small Modular Reactor Technology Deployment

Small Modular Reactors (SMRs) offer modular deployment options that can utilise existing power plant infrastructure while providing 90%+ capacity factors compared to 20-35% for renewable installations. These systems enable nuclear power deployment in smaller increments than traditional gigawatt-scale facilities, making them suitable for industrial applications requiring consistent power delivery.

SMR technology requires specialised fuel forms, particularly HALEU, that must be enriched to 5-20% uranium-235 compared to 3-5% for conventional reactor fuel. Current Western HALEU production capacity remains extremely limited outside of Russian facilities now subject to import restrictions, creating additional supply pressure for advanced reactor deployment programmes.

Energy Security vs Decarbonisation Balance

Nuclear power provides the only scalable, carbon-neutral baseload energy source capable of replacing coal-fired generation without requiring massive battery storage investments. This positioning becomes critical as governments balance energy security concerns with decarbonisation commitments that require eliminating fossil fuel dependence within increasingly compressed timelines.

Unlike renewable energy sources that require backup power systems or storage solutions for grid stability, nuclear facilities can provide consistent baseload generation that matches coal plant reliability whilst eliminating direct carbon emissions. This capability enables utilities to retire coal facilities without compromising grid stability or requiring substantial battery infrastructure investments.

Market Indicators and Investment Positioning

Long-term uranium contract prices increased from $80 to $86 per pound after 18 months of relative stability, with utilities dramatically expanding contracting activities throughout 2025. This represents a fundamental shift in utility procurement strategies, as operators now secure supplies 3-5 years in advance rather than relying on spot market purchases.

Approximately 70% of post-2027 uranium demand remains uncontracted—the highest level recorded in three decades. This unprecedented exposure indicates that utilities have not yet secured future fuel supplies for the majority of their operational requirements, creating potential supply competition as contracting deadlines approach.

Tier-1 Jurisdiction Investment Advantages

Australia controls approximately 30% of global uranium reserves whilst maintaining stable regulatory frameworks and established mining infrastructure. This combination of resource endowment and political stability creates superior investment opportunities for uranium exposure, particularly as Western utilities seek supply chain diversification away from geopolitically sensitive regions.

The designation of "Tier-1" jurisdiction status reflects multiple factors:

- Political Stability: Consistent regulatory frameworks and mining-friendly policies

- Infrastructure Access: Established transportation and processing facilities

- Environmental Standards: Rigorous environmental protection requirements that ensure sustainable operations

- Technical Expertise: Skilled workforce and established mining service industries

Production vs Development Company Risk Profiles

Existing uranium producers benefit immediately from rising prices and supply constraints, whilst development companies offer leveraged exposure to long-term supply deficit resolution. The optimal investment timing depends on uranium price trajectory expectations and individual risk tolerance for development execution risks.

Current Producers enjoy immediate cash flow generation from existing operations, providing downside protection during price volatility whilst maintaining exposure to price appreciation. These companies typically maintain established customer relationships and proven operational capabilities.

Development Companies offer amplified exposure to uranium price movements but carry execution risk related to project development, financing, and regulatory approval timelines. These investments require higher risk tolerance but provide potentially greater returns if projects achieve commercial production during sustained price elevation.

Technology-Driven Cost Positioning

In-situ recovery (ISR) mining technology offers significant cost advantages and reduced environmental impact compared to conventional mining methods. Companies utilising ISR technology can achieve first-quartile cost positioning, providing superior margins during uranium price cycles and enhanced resilience during market downturns. For instance, innovative extraction at Alta Mesa demonstrates how advanced techniques can improve operational efficiency.

ISR operations involve injecting solutions into underground uranium deposits and pumping the uranium-bearing solution to surface processing facilities, eliminating the need for traditional mining infrastructure and reducing environmental disturbance. This technology enables uranium extraction at production costs typically 20-30% below conventional mining operations.

The next major ASX story will hit our subscribers first

Long-Term Energy Security and Strategic Reserve Requirements

The emerging nuclear renaissance faces a fundamental mismatch between reactor construction timelines (8-12 years) and uranium supply development periods (5-7 years). This timing gap suggests that the uranium supply deficit may intensify before new production capacity becomes available, potentially creating sustained price pressure throughout the late 2020s and early 2030s.

Countries pursuing nuclear energy expansion may need to establish critical minerals strategic reserve programmes similar to oil stockpiles, given the concentrated nature of global production and long lead times for new supply development. Such reserve programmes would create additional demand pressure beyond operational reactor requirements, further tightening available supply for commercial utilities.

What Are HALEU Production Infrastructure Requirements?

Advanced reactor technologies requiring HALEU fuel face particular supply constraints, as global HALEU production capacity remains extremely limited outside of Russian facilities now subject to Western sanctions. Western investment in HALEU production infrastructure becomes critical for advanced reactor deployment programmes and energy security objectives.

The development of domestic HALEU production capability requires specialised enrichment facilities capable of producing uranium enriched to 5-20% uranium-235, compared to conventional reactor fuel enriched to 3-5%. These facilities require significant capital investment and regulatory approval processes that extend beyond standard uranium mining project timelines.

Technology Innovation and Supply Chain Evolution

Nuclear technology advancement continues driving uranium demand growth through improved reactor efficiency and expanded deployment scenarios. Next-generation reactor designs offer enhanced safety features and operational flexibility that make nuclear power suitable for applications previously limited to fossil fuel generation.

The evolution toward advanced reactor technologies creates opportunities for uranium companies positioned to serve specialised fuel requirements whilst providing exposure to broader nuclear industry growth trends. However, US uranium market disruption from trade tensions could affect supply chain development.

Investment considerations for the uranium supply deficit extend beyond traditional mining exposure into companies developing innovative extraction technologies and advanced fuel cycle capabilities. This positioning provides exposure to both immediate supply constraints and long-term technology evolution that continues reshaping nuclear energy markets globally.

Furthermore, the uranium supply deficit's broader implications suggest that higher prices alone may not resolve the fundamental mismatch between supply development timelines and accelerating demand growth.

Investment Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. Uranium investments carry significant risks including regulatory changes, operational challenges, and commodity price volatility. Investors should conduct independent research and consult qualified financial advisors before making investment decisions. Past performance does not guarantee future results, and all investments carry risk of loss.

Considering investing in uranium exposure before the supply deficit intensifies?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant uranium and mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial today to position yourself ahead of the market whilst accessing immediate insights into emerging uranium exploration and development opportunities.