June 23, 2026

The Supply Chain Bottleneck That Has Held Nuclear Back for Decades

For most of the past forty years, the economics of large-scale nuclear construction in the United States have been trapped in a self-reinforcing cycle of inaction. Manufacturers refused to invest in specialised production capacity without guaranteed order volumes. Utilities declined to commit to firm orders without confidence in a functioning domestic supply chain. The result was a near-complete hollowing out of the industrial base that once made the US the global leader in commercial reactor deployment.

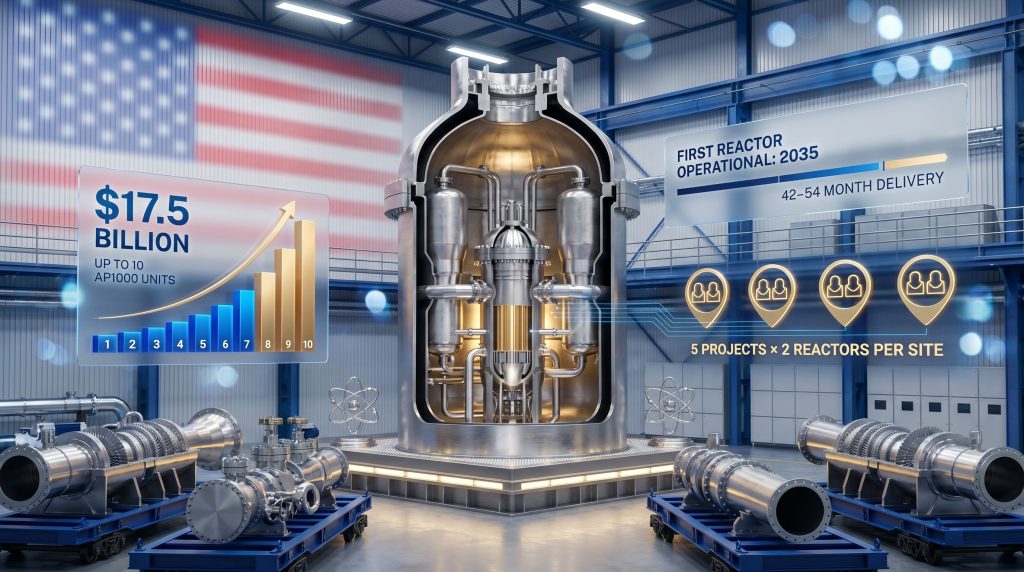

That structural paralysis is now being directly targeted by a conditional loan commitment of up to $17.5 billion from the US Department of Energy's Office of Energy Dominance Financing, designed to finance the advance procurement of long-lead time components for up to ten Westinghouse AP1000 nuclear reactors across five two-reactor project sites in the United States. This initiative is central to the broader US nuclear reactor supply chain loan for Westinghouse AP1000 reactors programme and carries significant implications for uranium market dynamics over the coming decade.

When big ASX news breaks, our subscribers know first

Understanding Long-Lead Time Items: The Hidden Driver of Nuclear Cost Overruns

What Makes Certain Components So Difficult to Source?

The phrase "long-lead time items" (LLI) refers to a category of highly specialised, precision-engineered components that cannot be ordered and received within a standard industrial procurement cycle. For nuclear applications, the most critical of these include:

- Reactor pressure vessels

- Containment vessels and liner systems

- Steam generators

- Large reactor coolant pumps

- Specialised turbine and generator systems

Manufacturing timeframes for these components typically range from 42 to 54 months, meaning that a reactor project which secures financing today cannot receive its most critical hardware for three and a half to four and a half years, regardless of how quickly all other planning, licensing, and civil works proceed.

This single procurement constraint has historically been the most underappreciated driver of nuclear construction delays. When components arrive late, the entire construction sequence is disrupted, skilled workforces sit idle, and cost overruns compound.

The DoE loan programme directly attacks this bottleneck by financing the advance procurement of LLI inventory before individual project funding vehicles have reached their final investment decisions. By acquiring these components at the programme level across all ten reactors simultaneously, the initiative creates the realistic potential to compress total construction timelines by up to three years per project compared to conventional sequential procurement approaches.

How the $17.5 Billion Financing Structure Actually Works

The Capital Architecture at a Glance

| Structural Element | Detail |

|---|---|

| Total Conditional Loan Commitment | Up to $17.5 billion |

| Reactors Targeted | Up to 10 AP1000 units |

| Project Configuration | 5 projects x 2 reactors per site |

| Partner Equity Required Per Project | $500 million (utility partner) + $500 million (Westinghouse SPV) |

| Total Upfront Equity Across Programme | Up to $5 billion |

| LLI Manufacturing Window | 42 to 54 months |

| Construction Acceleration Potential | Up to 3 years |

| Target First Reactor Operations | From approximately 2035 |

The Special Purpose Vehicle Model and Why It Matters

The financing will be administered through a dedicated Westinghouse special purpose vehicle (SPV), which will in turn oversee up to five individual project funding vehicles (PFVs). Each PFV will be jointly owned by Westinghouse and the relevant approved utility partner for a specific two-reactor project.

This SPV architecture serves several important financial engineering purposes:

- It isolates the financial risk of each project from Westinghouse's broader corporate balance sheet

- It creates a clean legal boundary between the DoE loan obligation and the equity commitments of individual partners

- It establishes a transparent repayment mechanism tied directly to the delivery and sale of long-lead items to end users

The repayment logic is straightforward and important to understand correctly. This is not a government grant, subsidy, or permanent fiscal commitment. The loan is designed to be self-liquidating, with repayment sourced from the proceeds generated when pre-procured LLI inventory is sold through to individual project funding vehicles upon delivery.

Step-by-step loan cycle:

- The Westinghouse SPV procures long-lead items using DoE loan funds at the programme level

- Individual project funding vehicles are established per two-reactor project

- Each approved utility partner commits $500 million in equity upfront, matched by $500 million from the Westinghouse SPV, totalling $1 billion per project before any DoE funds are accessed

- Pre-procured LLI components are delivered to project sites as construction schedules require

- Upon delivery, the sale proceeds from LLI transfer to project funding vehicles repay the DoE loan

- The financing cycle closes without ongoing fiscal dependency on government appropriations

Furthermore, as outlined by the DoE's loan programme office, this structure is specifically designed to mobilise private capital alongside public financing rather than replace it.

Critical Distinction: The $17.5 billion figure represents a conditional commitment, not a binding funding obligation. Westinghouse, its owners, and all project partners must independently satisfy specific technical, legal, environmental, and financial conditions before the DoE executes definitive financing documents and transfers any funds.

The AP1000: Why This Reactor Design Was Chosen as the Technology Platform

Technical Profile and Operational Credentials

The Westinghouse AP1000 holds a status no other large reactor design in the United States can claim: it is the only Generation III+ pressurised water reactor with full design certification from the Nuclear Regulatory Commission. That certification is not a minor administrative distinction. It represents the completion of a rigorous, multi-year technical review process and substantially reduces the licensing timeline uncertainty that has plagued other advanced reactor concepts.

Key technical characteristics of the AP1000 include:

- Rated electrical output: approximately 1,110 MWe per unit

- Two-unit site capacity: over 2,200 MWe of firm, dispatchable baseload generation

- Passive safety systems: gravity and natural circulation-driven cooling that removes the need for active mechanical intervention in emergency scenarios

- Modular construction: factory-fabricated module assemblies that reduce on-site labour hours and tighten quality control tolerances

The AP1000's operational track record in China, where units at the Sanmen and Haiyang sites have been generating electricity commercially, provides an important proof of concept that this is a deployed technology rather than a design in development. That distinction carries significant weight when assessing the risk profile of a loan-backed programme of this scale.

AP1000 vs. Small Modular Reactors: Different Time Horizons

A common question in nuclear investment discussions involves the relationship between large conventional reactor programmes and the emerging small modular reactor (SMR) sector. These are not competing approaches but rather technologies occupying different deployment windows.

| Technology | Status | Near-Term Deployability | Regulatory Pathway |

|---|---|---|---|

| AP1000 | NRC-certified, commercially operational | High (2030s) | Completed |

| SMRs (various designs) | Mostly pre-licensing or early certification | Lower (2030s-2040s) | In progress |

| Advanced Reactors (Gen IV) | Largely conceptual or early development | Low (2040s+) | Nascent |

The DoE loan programme's focus on the AP1000 reflects a deliberate prioritisation of near-term deployable technology over longer-dated innovation bets, which is consistent with the urgency of electricity demand growth being driven by artificial intelligence infrastructure, data centre proliferation, and industrial electrification across the United States.

Cameco and Brookfield: The Ownership Structure Behind Westinghouse

A Strategic Acquisition With Dual Exposure

Brookfield Renewable Partners and Cameco Corporation completed their joint acquisition of Westinghouse Electric Company in November 2023, combining two distinct but complementary strategic capabilities. Cameco brought deep expertise in the nuclear fuel supply chain, from uranium mining through to fuel fabrication. Brookfield contributed institutional-grade capital deployment experience across large-scale energy infrastructure assets globally.

Cameco CEO Tim Gitzel described the DoE loan commitment as an additional step in creating the right conditions for rapid AP1000 deployment in the US, noting the expected uplift to Westinghouse's energy systems segment during both the procurement phase and the subsequent construction phase. However, as highlighted by Westinghouse's own strategic partnership communications, realising these benefits depends on all conditional requirements being satisfied before binding agreements are executed.

For Cameco specifically, the strategic exposure runs on two distinct tracks. As a Westinghouse co-owner, Cameco benefits directly from increased reactor construction activity feeding into Westinghouse's energy systems revenue. But the second dimension is arguably more significant over a longer time horizon: as a uranium producer with operational assets including McArthur River, Cigar Lake, and the Inkai joint venture in Kazakhstan, Cameco is positioned to benefit from the structural increase in uranium fuel demand that ten new AP1000 reactors would generate.

Uranium Demand Implications: Quantifying the Fuel Cycle Effect

Ten AP1000 reactors operating at full capacity would require approximately 1,500 to 2,000 tonnes of uranium per year in steady-state operations. This is not a one-time procurement event but a multi-decade recurring demand commitment that cascades through the entire nuclear fuel cycle:

- Mining: increased uranium concentrate (U3O8) offtake requirements

- Conversion: uranium hexafluoride (UF6) conversion capacity demand

- Enrichment: separative work unit (SWU) demand for enriched uranium product

- Fuel fabrication: finished fuel assembly manufacturing for AP1000 fuel geometry

The current US vulnerability in this chain is significant. Heavy dependence on foreign conversion and enrichment capacity, particularly from Russian state entities, represents a supply security risk that domestic nuclear expansion programmes must address in parallel with reactor deployment. Consequently, the Russian uranium import ban has reinforced the urgency of building a self-sufficient domestic nuclear fuel cycle. This dynamic also strengthens the investment case for domestic enrichment infrastructure, including programmes like Centrus Energy's low-enriched uranium (LEU) and high-assay low-enriched uranium (HALEU) production capabilities.

Lessons From Vogtle: What the New Programme Does Differently

The Cautionary Benchmark

No serious analysis of US nuclear financing can bypass the experience of the Vogtle Units 3 and 4 project in Georgia, which ultimately reached completion but at a final cost exceeding $35 billion against an original estimate of approximately $14 billion, with construction delays stretching years beyond initial projections.

The root causes were multiple and interconnected:

- First-of-a-kind AP1000 construction in the US, with no established domestic workforce or supply chain

- Component manufacturing delays, in part due to the absence of pre-positioned LLI inventory

- Design change orders arising mid-construction from first-mover learning effects

- Workforce experience gaps at both the craft and engineering supervision levels

The new DoE-backed programme directly addresses the most structurally tractable of these failure modes. Bulk procurement across five standardised two-reactor projects creates the manufacturing volume certainty needed for fabricators to invest in dedicated production lines. Standardised reactor designs across multiple sites builds workforce experience progressively across the construction sequence, meaning that later projects benefit from the learning curve established on earlier ones. In addition, uranium supply challenges on the fuel side underscore why a comprehensive, coordinated approach to nuclear revival is essential rather than optional.

The next major ASX story will hit our subscribers first

Global Benchmarking: How the US Model Compares

State-Backed Nuclear Finance Across Major Programmes

| Country | Financing Mechanism | Approximate Scale | Technology |

|---|---|---|---|

| United States | DoE Conditional Loan (LLI procurement) | Up to $17.5 billion | AP1000 (10 units) |

| United Kingdom | Regulated Asset Base model | £20 billion+ (Sizewell C) | EPR |

| France | State equity injection via EDF | €50 billion+ (14 new EPRs) | EPR |

| South Korea | KEPCO state financing | Multiple export projects | APR-1400 |

| China | State policy bank financing | Multi-decade rolling programme | CAP1000 / HPR1000 |

The US approach is structurally distinct from most of these comparators. Rather than direct equity injection, guaranteed revenue mechanisms, or state ownership of the generating asset, the DoE model uses a loan-and-repayment architecture that is designed to be self-liquidating. This preserves private sector ownership of the eventual generating assets while removing the specific procurement risk barrier that has historically prevented project commitments from being made.

The Seven Utility Partners and What Their Interest Signals

Oversubscription as a Market Signal

Approximately seven utility companies have signed Letters of Intent to participate as approved project partners under the programme, against only five available project slots in the current programme structure. This oversubscription is analytically meaningful. It indicates that the combination of the DoE financing structure, the AP1000's NRC-certified status, and the LLI pre-procurement model has generated genuine commercial interest from utilities seeking firm baseload capacity, not merely exploratory conversations.

The identities of these utilities have not been publicly disclosed at this stage, which is consistent with standard practice during the conditional commitment phase. Protecting commercial negotiations whilst competitive partner selection is underway is a normal feature of large infrastructure financing processes.

Each approved partner must satisfy all required conditions before accessing programme financing, including equity commitment verification and creditworthiness assessment. These are not nominal requirements.

Workforce and Manufacturing Readiness: The Overlooked Constraint

Rebuilding a Hollowed-Out Industrial Base

The financing programme addresses the capital and procurement dimensions of the nuclear revival challenge. However, the workforce and manufacturing readiness dimension represents an equally significant constraint that no loan commitment can resolve on its own.

The 2026 to 2035 construction window implied by this programme is estimated to require tens of thousands of skilled nuclear construction workers, including welders qualified to nuclear code standards, structural ironworkers, instrumentation and control specialists, and civil engineers with large-scale containment structure experience. This workforce largely does not exist at the required scale in the United States today following decades of sector inactivity.

Key domestic manufacturing chokepoints that must be addressed in parallel include:

- Large forgings for reactor pressure vessels, which require specialised press capacity unavailable in most commercial steel facilities

- Reactor coolant pump systems with nuclear-grade quality assurance requirements

- Specialised valve and instrumentation systems compliant with NRC Class 1 seismic and pressure standards

- Containment vessel steel fabrication at scale

Bulk procurement across five standardised projects creates the volume certainty that manufacturers require to justify capital investment in new production capacity. This is the industrial policy logic embedded in the programme design, and it represents a meaningful structural departure from the one-at-a-time project approach that has characterised the post-1970s US nuclear experience. Furthermore, US uranium production rebound to a six-year high signals that the upstream fuel sector is also beginning to respond to these structural incentives.

Frequently Asked Questions: US Nuclear Reactor Supply Chain Loan for Westinghouse AP1000 Reactors

What Exactly Is the $17.5 Billion DoE Loan Designed to Fund?

The conditional loan commitment finances the advance purchase of long-lead time components with manufacturing timelines of 42 to 54 months, covering up to ten Westinghouse AP1000 reactors across five two-reactor project sites. Procuring these items at the programme level before individual projects reach final investment decision compresses overall construction timelines by up to three years per project.

Is This Financing a Government Grant?

No. This is a conditional loan commitment structured to be repaid from the proceeds of long-lead item sales to end-user project vehicles upon component delivery. All parties must satisfy independent technical, legal, environmental, and financial conditions before any binding financing documents are executed or funds disbursed.

When Are the First Reactors Expected to Begin Commercial Operations?

Reactors supported by this programme are expected to commence commercial operations from approximately 2035 onward, with the advance procurement strategy designed to bring that date forward by up to three years relative to conventional sequential procurement timelines.

Who Owns Westinghouse Electric Company?

Westinghouse Electric Company is jointly owned by Cameco Corporation and Brookfield Renewable Partners, following the completion of their acquisition in November 2023.

How Many Utilities Have Expressed Interest, and How Competitive Is the Selection Process?

Approximately seven utility companies have signed Letters of Intent to participate, competing for five available project slots within the current programme structure.

What Equity Commitment Is Required From Each Project Partner?

Each approved utility partner must commit $500 million in project equity upfront, matched by an equivalent $500 million from the Westinghouse SPV, creating a combined $1 billion per project equity foundation before any DoE loan funds are accessed.

Strategic Outlook: What This Signals for the Broader Energy Landscape

The US nuclear reactor supply chain loan for Westinghouse AP1000 reactors represents more than a single financing transaction. If all five projects proceed through final investment decision, this programme would constitute the largest coordinated nuclear construction initiative in the United States in more than four decades, with cascading implications across uranium markets, nuclear fuel cycle infrastructure, reactor manufacturing capacity, and the broader clean energy capital stack.

The programme also establishes a potentially replicable financing template. Should the LLI pre-procurement model demonstrate its ability to compress timelines and reduce unit costs across the initial tranche of projects, the same structure could be extended to additional reactor deployments beyond the initial ten-unit programme. For investors monitoring uranium investment growth opportunities, the scale and ambition of this initiative underscores why the nuclear fuel cycle warrants close attention across both equity and commodity markets.

Investor Note: This article contains forward-looking statements and projections based on publicly available information. Nothing in this article constitutes financial advice. Readers should conduct independent due diligence and consult qualified financial advisers before making investment decisions related to any companies or sectors discussed herein.

Readers seeking further context on US nuclear energy policy and the Westinghouse AP1000 technology platform may find additional reporting at miningweekly.com.

Want to Stay Ahead of the Next Major Uranium Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries hit the ASX, translating complex data across 30+ commodities into clear, actionable insights — including uranium opportunities driven by the structural demand shifts reshaping the nuclear fuel cycle. Explore historic discoveries and the returns they generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.