May 23, 2026

The Invisible Threshold: How the Uranium Market Mistakes Capacity for Reality

Most commodity markets fail spectacularly not because the underlying fundamentals were wrong, but because participants consistently misread the instruments they were using to measure them. The uranium supply deficit is a case study in exactly this dynamic. The data showing scarcity has been available for years, embedded in the same industry reports that market participants cite as evidence of adequacy. The problem is not the data itself; it is a fundamental misunderstanding of what those documents were designed to measure and for whom they were written.

Understanding this distinction is not a minor analytical footnote. It is the difference between identifying a structural uranium supply deficit that is already underway and concluding that supply concerns remain a future problem safely deferred to another cycle. Furthermore, the uranium supply challenges facing the market are compounding in ways that conventional analysis consistently underestimates.

When big ASX news breaks, our subscribers know first

Why the World's Most-Cited Uranium Reports Are Not What Investors Think They Are

The World Nuclear Association and comparable institutional bodies publish uranium supply and demand assessments that serve as the primary reference points for most market participants. These documents are extensively researched, methodologically rigorous, and genuinely valuable. They are also systematically misapplied by virtually every investment-oriented reader who picks them up.

The core issue lies in how supply figures are constructed. These reports present nameplate capacity rather than adjusted production output, and they count operable reactors alongside actively operating ones when calculating demand coverage. Nameplate capacity is the theoretical maximum a facility could produce under ideal, continuous operating conditions. It bears little resemblance to actual deliverable pounds in any given year.

When historical WNA projections are compared against actual production outcomes, the divergence is not random noise. It is a consistent, directional gap in which production capability underperforms published projections by approximately 16 to 30 percentage points across repeated measurement periods. This is not a data error. It reflects the methodological design of documents built for long-range infrastructure planning, not near-term market analysis.

Chris Frostad, CEO of Purepoint Uranium, has made the point with notable clarity: the numbers and predictions in these reports are well-documented and carefully researched. They simply were not produced for investors attempting to identify entry points or timing windows. Using a policy planning instrument as a supply forecast is, in analytical terms, the equivalent of reading a building's architectural drawings to predict when it will need repairs.

The Fabrication Lag That Almost Nobody Accounts For

Compounding the capacity-versus-output confusion is a processing gap that is rarely incorporated into market analysis despite being a well-established feature of the nuclear fuel cycle. From the point of uranium extraction as U₃O₈ (commonly called yellowcake) through conversion to uranium hexafluoride (UF₆), enrichment, and final fabrication into reactor fuel assemblies, the timeline runs approximately one to two years.

This lag has profound implications. Even if a new mine comes online precisely on schedule, its output cannot address reactor fuel requirements for the following year. Forecasts that match projected production against near-term consumption without incorporating this processing timeline produce materially earlier deficit onset dates than the same data analysed at face value. Adjusted supply modelling that accounts for fabrication timelines shifts the supply-demand crossover window meaningfully forward, reinforcing the case that the uranium supply deficit is closer than conventional analysis suggests.

Three Distinct Categories of Disappearing Uranium Pounds

The uranium supply deficit is not reducible to a single cause. Supply erosion is occurring simultaneously across three distinct channels, each with different drivers, different timelines, and different implications for how quickly the shortfall can be closed. In addition, uranium supply-demand volatility is amplifying the difficulty of accurately forecasting the pace of deterioration.

Category One: Project Delays and Pipeline Slippage

Development-stage uranium projects are characterised by a structural tendency toward timeline optimism at the announcement stage followed by systematic delay in execution. Most pipeline projects do not have firm commissioning timelines. Industry aggregators apply optimistic deployment assumptions to these projects when constructing supply forecasts, but the observed execution rate tells a different story.

Restart and greenfield developments across multiple jurisdictions are increasingly being pushed beyond 2027, a threshold that carries specific significance for the mid-decade supply outlook. Projects facing this delay remove the market's most credible near-term supply relief valve. Factors compounding this trend include:

- Funding challenges linked to uranium price uncertainty and equity market volatility

- Skilled labour shortages affecting technical and operational roles

- Permitting timelines extending beyond initial projections

- Management instability at key development-stage operators

- Institutional investors applying insufficient analytical rigour to development-stage assessments, often relying on recycled presentations rather than independent project evaluation

Category Two: Geopolitical Reorientation of Supply Flows

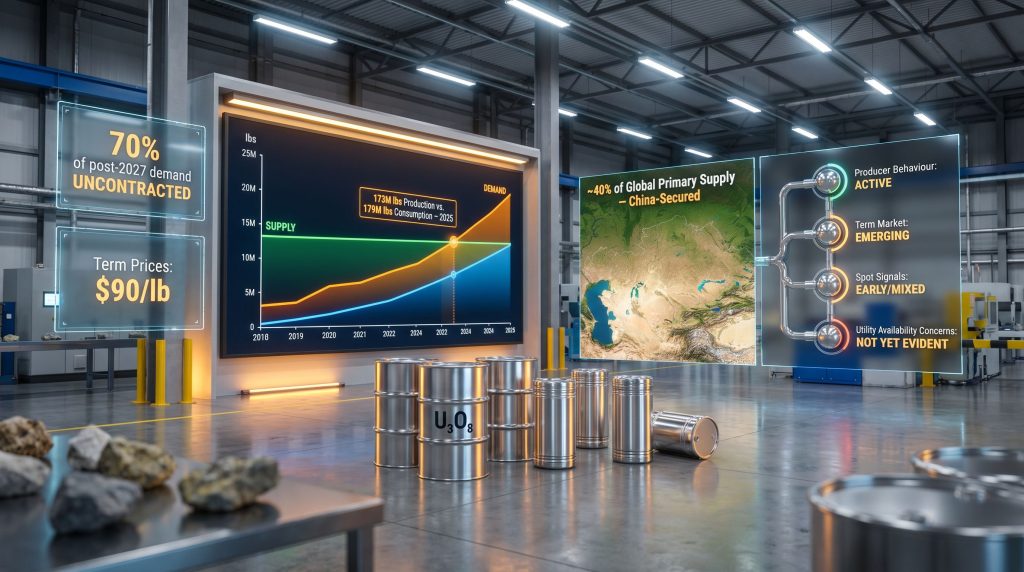

China has systematically built equity positions in uranium production assets across multiple jurisdictions, securing access to approximately 40% of global primary uranium production through a combination of direct imports and foreign mining investments. This is not a future risk. It represents a structural shift in how uranium pounds are allocated at the point of production.

Niger's 2023 nationalisation of uranium assets previously operated by French company Orano illustrates a separate dimension of geopolitical supply erosion: instability in African uranium-producing nations permanently removes volumes from Western fuel cycle access. These are not temporary disruptions subject to negotiated resolution. They represent irreversible reconfigurations of supply geography that leave Western utilities competing for a smaller pool of available material.

The outcome is effectively a bifurcated uranium market: state-backed buyers with captive supply arrangements operating in one tier, and open-market participants facing genuine scarcity in another. Consequently, uranium market dynamics are shifting in ways that disadvantage buyers without long-term supply security.

Category Three: Depletion of Secondary Supply Mechanisms

The post-Fukushima period generated a decade-long buffer of secondary uranium supply that masked the underlying production shortfall from most market observers. Enrichment plant underfeeding, a process by which enrichers extract more uranium value from a given volume of feed material than technically required, contributed meaningfully to secondary supply availability during this period. This mechanism is now approaching exhaustion as a significant market contributor.

Japan's re-entry into uranium procurement after more than a decade of inactivity serves as a directional signal that stockpiles accumulated during the post-2011 period are drawing toward levels that require active replenishment. When a major buyer that has been absent from the market for over a decade returns as a net purchaser, it confirms that inventory buffers accumulated during that absence are no longer adequate.

| Supply Erosion Category | Primary Driver | Western Market Impact | Reversibility |

|---|---|---|---|

| Project delays | Funding, labour, permitting | High | Partial, time-dependent |

| Geopolitical reorientation | China equity stakes, Niger nationalisation | High | Low to none |

| Secondary supply depletion | Underfeeding exhaustion, stockpile drawdown | Moderate to high | None |

| Operational underperformance | McArthur River constraints, Kazakhstan shortfalls | Moderate | Partial |

Kazakhstan and the Producer Behaviour Signal the Market Is Underweighting

When the world's dominant uranium producer changes how it thinks about production, the signal deserves careful attention. According to Cameco's supply-demand analysis, Kazakhstan, through state-owned Kazatomprom, has deliberately transitioned from a strategy centred on volume maximisation toward what the company describes as value-based production management. This is not a response to temporary logistical disruption. It reflects a long-term strategic calculation that price realisation, not output volume, is the primary value driver going forward.

Producers do not make this transition unless they are confident that supply scarcity will persist. Managing output for price rather than maximising tonnes is only rational when the seller believes their product will become harder to source over time. Kazakhstan's behaviour represents a first-order signal that the supply constraint thesis is being validated at the producer level, well before it is fully priced into financial markets.

Separately, operational challenges at McArthur River in Canada, one of the world's highest-grade uranium deposits operated by Cameco, produced an approximate 25% production shortfall against expectations. High-grade deposits carry a general assumption of reliable, cost-effective production. When even these assets encounter meaningful output constraints, it reinforces that the development and production environment for uranium is more complex than headline capacity figures suggest.

Demand: Structurally Growing, Incompletely Contracted, and Increasingly Origin-Conscious

Unlike the supply side, uranium demand modelling benefits from a degree of structural predictability. Nuclear reactors follow documented construction timelines. Fuel requirements can be calculated with reasonable precision once a reactor's design specifications are known. This predictability makes demand the more stable variable in the supply-demand equation.

The World Nuclear Association projects reactor consumption reaching approximately 330 million pounds annually by 2040, with upper-range scenarios extending to 530 million pounds, representing roughly a 90% to 196% increase from 2025 consumption levels of approximately 179 million pounds. Independent modelling from UxC anticipates material and sustained deficits from around 2030 extending through 2040, with the supply gap widening as the decade advances.

Perhaps more immediately relevant is the contracting position of the utility sector. An estimated 70% of post-2027 reactor fuel demand remains uncontracted, the highest proportion in approximately three decades. This is not utility complacency. It reflects the difficulty of securing long-term supply under acceptable terms when sellers increasingly understand the structural scarcity environment they operate within.

Utilities are undergoing a subtle but significant psychological transition: moving from a posture of price sensitivity toward one of availability concern. When this shift completes, contracting behaviour changes fundamentally. Buyers who once walked away from offers they considered overpriced begin accepting terms they previously rejected, not because they want to, but because securing physical supply becomes the priority.

On small modular reactors (SMRs): while these technologies generate substantial investor interest, their near-term demand contribution is modest. Multiple SMR units are required to match the annual fuel consumption of a single conventional large reactor, and most commercial deployments remain years from completion. Their demand contribution is best described as a meaningful long-run addition rather than a near-term market catalyst.

The Inventory Opacity Problem: Why the Deficit Is Already Here But Not Yet Priced

Uranium inventory data is, by the standards of major commodity markets, exceptionally opaque. Information on stockpile levels across the fuel cycle, from mine output through conversion, enrichment, and utility storage, is fragmented, inconsistently reported, and often commercially sensitive. The market cannot directly observe when production deficits translate into physical scarcity.

This opacity creates what might be called a recognition gap: the actual supply-demand imbalance may already exist in physical reality, but it will not become visible to financial markets until its effects propagate through observable behaviour changes. As industry participants have noted, the market is likely already in the midst of the deficit period, but without transparent inventory data, that reality remains invisible to most participants.

A UxC utility survey provided directional evidence that while buyers currently report adequate inventory positions, they broadly anticipate drawdown over the following one to two years. This alignment between what buyers expect to do and what the structural supply analysis predicts should be happening is meaningful corroboration, even if precise inventory levels remain unavailable.

The probability window for the supply-demand crossover to become physically undeniable sits in the range of mid-2026 to early 2027, based on adjusted analysis incorporating production realities and fabrication lags. This is a probability range, not a certainty, and inventory opacity prevents tighter precision. However, the spot-term price divergence already visible in the market provides an additional indicator that physical tightness is advancing.

Risk Framework: The primary uncertainty in the uranium supply deficit thesis is not whether the deficit will occur. The adjusted supply data makes that conclusion robust. The uncertainty is the lag between when physical scarcity materialises and when financial markets recognise and price it. Investors face an asymmetric information environment where the fundamental thesis is strong but the timing mechanism is obscured.

The next major ASX story will hit our subscribers first

The Four-Stage Sequence Through Which Market Recognition Unfolds

Because no single catalyst event is likely to define this uranium cycle, understanding the sequential stages through which the market will recognise the uranium supply deficit is essential for positioning and monitoring.

Stage 1: Producer Behaviour is already observable. Kazakhstan's value-based production strategy and operational constraints at major established producers represent the earliest and most reliable signals that the supply environment is tightening. These are rational responses to anticipated scarcity by parties with the most direct information about production economics.

Stage 2: Term Market Dynamics are actively emerging. Long-term uranium prices have reached and held above $90 per pound, surpassing the $85 threshold identified as a key transition signal. Additional evidence includes fewer competitive bids per utility tender, contract extensions being negotiated beyond 2035, and growing buyer preference for origin-specific supply agreements that prioritise geographic security over price optimisation.

Stage 3: Spot Market Signals remain early and mixed. Volatility has increased and the spot market has tested an $85 floor, but sustained directional movement has not yet materialised. The spot market historically lags term market signals in uranium because the majority of transactions occur under long-dated contracts. Spot price behaviour at this stage should be read as a directional indicator rather than a confirmation signal.

Stage 4: Utility Availability Concerns have not yet emerged publicly. When utilities begin stating difficulty securing adequate fuel supply, it marks full market recognition of the uranium supply deficit. It also marks the end of early entry opportunities.

| Stage | Key Indicator | Current Status |

|---|---|---|

| Producer behaviour | Value-based output management, operational constraints | Active and confirmed |

| Term market transition | Prices above $90/lb, fewer tender bids, extended contracts | Emerging and strengthening |

| Spot market signals | Increased volatility, floor testing | Early and mixed |

| Utility availability concerns | Public statements on supply security difficulties | Not yet evident |

What Sets This Cycle Apart From the 2000s Uranium Boom

Investors drawing direct comparisons between the current environment and the mid-2000s price surge risk misapplying a historical framework that does not map cleanly onto present conditions. The 2000s cycle was characterised by a single identifiable catalyst, the flooding of the Cigar Lake mine in Canada, which triggered a rapid, spike-like price response. The current cycle is structurally different across several dimensions:

- Secondary supply availability: The 2000s cycle still had substantial Cold War-era stockpiles to draw upon. Those buffers are now largely depleted.

- Geopolitical supply risk: The current cycle involves significant and permanent supply reorientation toward state-backed buyers, an element largely absent from the 2000s dynamic.

- Utility contracting posture: Buyers are increasingly prioritising supply security over price, a shift not seen in the previous cycle.

- Development pipeline responsiveness: The current development pipeline faces structural constraints that make it far less responsive to price signals than in the 2000s.

- Demand trajectory: Reactor construction globally is accelerating through the 2030s in a way that was not evident during the 2000s boom.

The current cycle's recognition will unfold through sequential stage transitions rather than a sudden event-driven spike. This makes timing-based investment strategies less reliable and reinforces the importance of fundamental company quality as the primary return driver. Furthermore, reviewing uranium market trends supports the view that this structural shift is deepening rather than moderating.

An Investment Framework Built on Structure Rather Than Catalysts

The consistent lesson from uranium market history is that investors who position for a specific catalyst event regularly find themselves either too early, too late, or reacting to events that turn out to be temporary disruptions rather than structural inflection points. Kazakhstan's periodic logistical issues with sulfuric acid supply are a useful example: market participants repeatedly interpreted these as permanent game-changing events, while the company itself worked actively to resolve them.

A more durable approach prioritises sector fundamentals over event speculation and focuses evaluation on company-specific attributes that perform across multiple price scenarios. Key attributes worth prioritising include:

- Production certainty: Operating assets or near-term production capability insulate companies from the project delay risk that afflicts the development pipeline.

- Jurisdictional security: Western-aligned supply sources command increasing premium as utilities seek origin-specific contracts, making political stability and regulatory predictability core value drivers.

- Balance sheet resilience: Companies capable of sustaining operations through price volatility without dilutive financing avoid the equity destruction that has historically afflicted leveraged uranium developers through cycle troughs.

- Contracting exposure: Long-term contract books priced above incentive thresholds lock in value regardless of spot market timing uncertainty.

- Management track record: In a sector where project execution consistently underperforms projections, management teams with demonstrated delivery capability represent a genuine differentiator.

However, as analysts at Crux Investor have noted, uranium forecasts routinely overstate supply and underestimate scarcity, making independent due diligence on individual companies especially important. The structural uranium supply deficit cannot be rapidly resolved through new supply. That characteristic provides a durable supportive environment for well-positioned operators across multiple price scenarios, reducing the dependence on precise timing that makes commodity investing so difficult for most participants.

Frequently Asked Questions: Uranium Supply Deficit

What is causing the uranium supply deficit?

The deficit emerges from converging pressures: a decade of underinvestment following the Fukushima accident, consistent overestimation of production capacity by industry forecasters, geopolitical reorientation of supply toward state-backed buyers, progressive depletion of secondary supply mechanisms, and a development pipeline that structurally underdelivers against published timelines. With global production of approximately 173 million pounds in 2025 falling short of reactor consumption of roughly 179 million pounds, and total fuel cycle demand adding further pressure, the gap is real and widening.

When will the uranium supply deficit become visible to the market?

Adjusted analysis incorporating fabrication lags and production realities points to a crossover window between mid-2026 and early 2027, with market recognition likely lagging the actual physical event due to inventory opacity. Recognition will unfold sequentially through producer behaviour changes, term market adjustments, spot price signals, and finally utility availability concerns.

Why do official uranium forecasts overestimate supply?

These publications report nameplate capacity rather than adjusted output, count operable reactors as operating, and apply optimistic project timeline assumptions. They are designed as policy planning instruments, not investment analysis tools. Historical comparison of WNA projections against actual outcomes shows production consistently underperforming published forecasts by 16 to 30 percentage points.

How much post-2027 uranium demand is currently uncontracted?

Approximately 70% of post-2027 reactor fuel demand remains uncontracted, the highest proportion in roughly three decades. This reflects both supply-side difficulty and a growing buyer awareness that availability, not price, will become the primary constraint.

What price signals a genuine structural market transition?

Sustained long-term contracting above $85 per pound has been identified as a key threshold. With term prices reaching $90 and holding, that threshold has been crossed. Supporting signals include fewer competitive bids per utility tender, contract extensions beyond 2035, and increasing demand for origin-specific supply agreements.

How does China's supply positioning affect Western buyers?

China has secured access to approximately 40% of global primary uranium production through imports and equity stakes in mining assets, systematically reducing the volume available to open-market buyers. This creates a genuine competitive disadvantage for Western utilities relying on spot and term market procurement.

Will small modular reactors materially increase uranium demand in the near term?

SMRs represent a meaningful long-run demand addition but are not a near-term catalyst. Multiple units are required to match the fuel consumption of a single conventional reactor, and most commercial deployments remain years from operation. Their demand contribution will be incremental rather than transformational over the next five years.

The Deficit Is Here: What Remains Uncertain Is Only the Timing of Recognition

The uranium supply deficit is not a speculative forecast awaiting confirmation. It is a measurable, ongoing condition whose full market impact is being temporarily absorbed by depleting inventory buffers and exhausting secondary supply mechanisms. Once those buffers are consumed, the gap between what the market produces and what reactors require becomes physically undeniable.

Three transition triggers are showing increasing evidence of activation: sustained term contracting above $85 per pound has been achieved; consecutive inventory drawdowns are accumulating directional confirmation; and development projects are systematically being pushed beyond 2027. None of these individually resolves the timing question. Together, they map the contours of an approaching supply-demand crossover whose direction is clear even where its precise moment is not.

For investors, the key insight is counterintuitive. In a market characterised by inventory opacity and delayed recognition, waiting for definitive confirmation means waiting until the opportunity has passed. The four-stage recognition sequence provides observable milestones for tracking market transition. By the time Stage 4 utility availability concerns become public statements, the entry window will have closed.

This article is intended for informational purposes only and does not constitute financial advice. Uranium market projections, supply and demand figures, and price references involve inherent uncertainty and may differ materially from actual outcomes. Past market cycles do not guarantee future performance. Readers should conduct independent research and consult qualified financial advisers before making investment decisions.

Want to Identify the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including uranium and other critical commodities — so subscribers can act on actionable opportunities ahead of the broader market. Explore historic discoveries and their exceptional returns, then begin your 14-day free trial at Discovery Alert to position yourself at the leading edge of the next major find.