August 4, 2026

The modern energy landscape faces a critical bottleneck that threatens to derail decarbonisation efforts worldwide. While governments accelerate nuclear deployment targets and utilities plan massive capacity expansions, the uranium mining sector confronts fundamental constraints that cannot be resolved through traditional market mechanisms. This structural uranium supply gap represents far more than cyclical commodity volatility – it reflects structural limitations embedded within the nuclear fuel supply chain that will shape energy security for the next two decades.

Long-term contracting patterns reveal the severity of this emerging crisis. Major utilities, traditionally focused on cost optimisation, are now prioritising supply security over pricing considerations. This shift signals recognition that uranium availability, not affordability, has become the primary constraint facing nuclear power expansion. The implications extend beyond individual project economics to encompass national energy independence strategies and climate commitments that depend critically on nuclear baseload capacity.

Understanding the Fundamental Market Imbalance

The structural uranium supply gap manifests as a persistent shortfall where global production consistently operates 20-30% below consumption requirements. Current data indicates an annual deficit of approximately 55 million pounds U₃O₈, with global demand reaching 180 million pounds while primary mine production delivers only 125 million pounds.

This disparity differs fundamentally from cyclical commodity patterns in three critical ways:

• Duration persistence – Structural gaps extend across 10-15 year planning horizons rather than resolving within typical 2-5 year commodity cycles

• Root cause complexity – Capital intensity and geological constraints prevent rapid supply response, unlike temporary production disruptions

• Price mechanism failure – Higher uranium prices cannot resolve shortages within required timeframes due to 7-10 year minimum development cycles

According to the World Nuclear Association's 2025 World Nuclear Fuel Report, only 46% of projected 2040 uranium demand is covered by currently known supply sources. The WNA's central forecast projects 391 million pounds U₃O₈ annual demand by 2040, with higher scenarios reaching 532 million pounds. However, the uranium supply-demand volatility this creates represents a fundamental supply-demand disconnect that cannot be addressed through conventional market adjustments.

| Year | Demand (Million lbs U₃O₈) | Supply (Million lbs U₃O₈) | Gap (Million lbs) |

|---|---|---|---|

| 2024 | 180 | 125 | -55 |

| 2030 | 230 | 160 | -70 |

| 2040 | 391 | 210 | -181 |

The cumulative effect creates a projected deficit of 196 million pounds by 2040, equivalent to eleven years of Cigar Lake production capacity. This calculation assumes Cigar Lake's annual output of approximately 18 million pounds U₃O₈, making the scale of the shortage immediately comprehensible to industry participants familiar with major producing assets.

When big ASX news breaks, our subscribers know first

Nuclear Energy Renaissance Driving Unprecedented Demand Growth

Twenty-four countries have endorsed the Net Zero Nuclear Industry Pledge, committing to triple global nuclear capacity by 2050. This governmental backing represents a fundamental shift from nuclear power being viewed as an economic option to being classified as a strategic necessity for both decarbonisation and energy security objectives.

The post-2022 geopolitical landscape has accelerated this transition, particularly across European and Asia-Pacific markets where energy independence considerations now outweigh pure cost competitiveness. Nuclear power provides the only scalable, carbon-free baseload generation technology capable of supporting industrial electricity demand while maintaining grid stability during renewable energy intermittency periods.

Small Modular Reactors Creating Additional Demand Categories

Advanced reactor deployment introduces specialised fuel requirements that compound existing supply constraints. High-Assay Low-Enriched Uranium (HALEU) fuel, required for many SMR designs, contains 5-20% uranium-235 enrichment compared to 3-5% for conventional reactors. This higher enrichment level demands additional uranium feedstock and creates parallel supply bottlenecks in enrichment services.

Current global HALEU production capacity remains extremely limited, with the United States producing less than 1% of global enrichment services. Furthermore, these developments are aligned with advanced US ISR technology advances that will be necessary to bridge supply gaps. Russia controls 46% of worldwide enrichment capacity, while China operates 13%, creating strategic vulnerabilities for Western reactor deployment programmes. The U.S. Department of Energy has announced domestic HALEU production initiatives, but commercial-scale availability requires multi-year development timelines.

Geographic Demand Acceleration Patterns

Asia-Pacific regions lead the global reactor construction pipeline, with China, India, and Southeast Asian countries planning substantial nuclear capacity additions. European energy security imperatives, particularly following 2022 supply disruptions, have renewed nuclear investment across France, Poland, and the United Kingdom. North American utilities are extending existing reactor lifespans whilst evaluating new construction projects to meet net-zero compliance requirements.

"The structural supply deficit creates particularly favourable conditions for producers located in Western, allied jurisdictions with established regulatory frameworks and proven permitting pathways."

This demand concentration across politically stable markets places premium value on uranium production from jurisdictions aligned with major consuming regions, fundamentally altering procurement strategies from cost-focused to security-focused approaches.

Why Traditional Supply Responses Cannot Close This Gap

Uranium mining confronts unique development constraints that prevent rapid capacity expansion despite sustained price incentives. The minimum 7-10 year timeline from discovery to production represents the primary structural barrier preventing supply response to demand signals.

Development Timeline Constraints

Even advanced projects with existing permits require extensive lead times before production commencement. The Tony M mine in Utah, despite being a past-producing operation with permits in place, still requires 2026 bulk sampling and processing before restart decisions can be finalised. The Hurricane deposit in Canada, containing 48.6 million pounds U₃O₈ Indicated resources at extraordinary grades, remains in exploration phases despite advanced resource definition.

This timeline reality means that investment decisions made today determine uranium availability in the mid-2030s, creating an inevitable gap between current demand acceleration and future supply capacity. Traditional commodity markets resolve imbalances within months to years through production adjustments, but uranium's capital intensity and regulatory complexity extend these response times by nearly a decade.

Grade Deterioration and Operational Bottlenecks

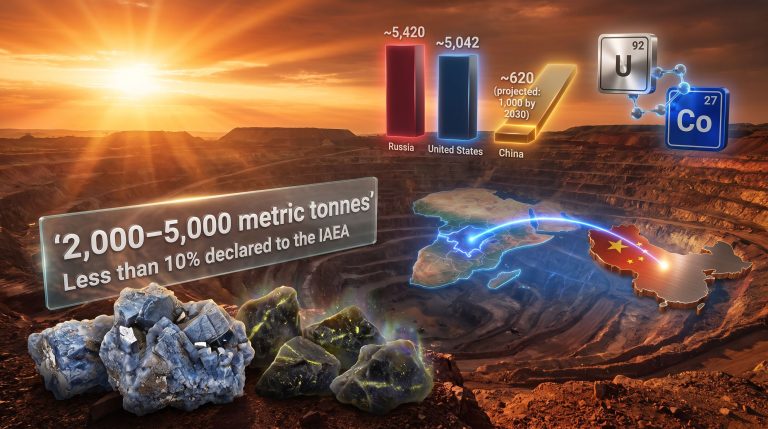

Existing uranium operations face declining ore grades as higher-grade zones become depleted, forcing operators to process larger volumes of lower-grade material at increased extraction costs. Kazakhstan, producing 43% of global uranium supply, has acknowledged infrastructure constraints limiting rapid expansion despite substantial resource bases.

In-Situ Recovery (ISR) limitations prevent easy capacity scaling beyond current levels due to:

• Geological constraints requiring specific host rock chemistry

• Water table management limitations in production basins

• Permitting restrictions in environmentally sensitive jurisdictions

• Infrastructure bottlenecks in specialised equipment manufacturing

Open-pit and underground mining operations can theoretically expand capacity but require 10-12 year development cycles versus 7-8 years for ISR projects, further extending supply response timelines. The technical complexity of high-grade underground operations, particularly in jurisdictions like Canada's Athabasca Basin, demands specialised expertise and equipment that cannot be rapidly deployed across multiple projects simultaneously.

Secondary Supply Depletion Accelerating

Secondary uranium sources, including military stockpile releases and utility inventory drawdowns, have historically provided 20-30% of global supply whilst masking structural primary production shortfalls. These sources are now depleting at accelerating rates, eliminating buffers that previously balanced supply-demand equations.

Reactor decommissioning programmes, once a reliable source of recycled uranium, face finite capacity as older reactor fleets reach end-of-life. The permanent nature of stockpile depletion means these supply sources cannot be regenerated, forcing increased reliance on primary mining production precisely when development timelines prevent rapid capacity additions.

Geopolitical Factors Intensifying the Supply Crisis

Five countries control 84% of global uranium production, creating unprecedented concentration risk for utilities seeking supply security. Kazakhstan leads with 43%, followed by Canada (13%), Australia (12%), Namibia (11%), and Niger (5%). This geographic concentration means approximately 28% of global supply comes from jurisdictions reliably accessible to Western markets, whilst the remainder originates from countries with varying degrees of geopolitical alignment.

Russian Supply Chain Vulnerabilities

Russia's dominance of uranium enrichment services, controlling 46% of global capacity, creates downstream vulnerabilities distinct from mining constraints. The US Senate uranium ban impact beginning in 2028, will force American utilities to secure alternative supply sources and enrichment services simultaneously. European diversification pressures following 2022 geopolitical tensions compound these procurement challenges.

The interconnected nature of enrichment and mining creates multiplicative supply risks. Even securing adequate uranium concentrate becomes insufficient without access to enrichment services, particularly for advanced reactor fuels requiring specialised processing capabilities. Western enrichment capacity remains severely limited, with the United States producing less than 1% of global services despite operating the world's largest commercial nuclear fleet.

Strategic Mineral Classifications Driving Policy Changes

Multiple jurisdictions have designated uranium as a critical mineral, triggering strategic stockpiling initiatives and export control considerations. This classification prioritises domestic supply security over export market optimisation, potentially restricting global uranium trade flows precisely when international demand reaches historic peaks.

Japan's partnership arrangements with Australian projects, including offtake agreements pre-dating current market tightness, demonstrate proactive supply chain diversification strategies. The Japan Australia Uranium and Itochu arrangement, securing rights to acquire 35% interest in Lake Maitland for US$39.6 million, provides independent validation of commercial project viability whilst ensuring Japanese utility access to geopolitically stable uranium sources.

What Could Kazakhstan's Expansion Limitations Mean?

Despite controlling the largest share of global production, Kazakhstan faces specific constraints limiting rapid expansion potential:

• Infrastructure bottlenecks in specialised mining equipment limit expansion pace

• Water management challenges in ISR operations require extensive aquifer monitoring

• Geopolitical alignment considerations create uncertainty for Western utility contracting

• Transportation logistics through Central Asian corridors face capacity constraints

"Kazakhstan's position as the world's dominant uranium producer paradoxically highlights supply concentration risks rather than providing supply security assurance."

These limitations mean that even the world's largest uranium producer cannot single-handedly resolve global supply shortfalls, emphasising the need for geographically diversified production capacity development.

The Enrichment Bottleneck Compounding Supply Problems

Uranium enrichment represents a critical chokepoint in the nuclear fuel cycle, with capacity constraints that compound mining supply limitations. The process of converting natural uranium into reactor-usable fuel concentrates global capacity among a small number of facilities, creating strategic vulnerabilities for nuclear power programmes worldwide.

Global Enrichment Capacity Distribution

Current enrichment capacity concentration creates multiple single points of failure:

• Russia: 46% of global capacity

• China: 13% of global capacity

• European Union: 25% of global capacity

• United States: Less than 1% of global capacity

This distribution means Western utilities depend heavily on foreign enrichment services, creating supply chain risks that extend beyond uranium mining constraints. The technical complexity and capital requirements of enrichment facilities prevent rapid capacity expansion, with new facilities requiring 5-8 year construction timelines and specialised centrifuge technology.

HALEU Supply Chain Gaps Creating Parallel Shortages

Advanced reactor deployment introduces High-Assay Low-Enriched Uranium (HALEU) requirements that existing commercial enrichment capacity cannot adequately supply. HALEU fuel, containing 5-20% uranium-235, requires significantly more enrichment work units per kilogram of final product compared to conventional 3-5% enriched fuel.

Current commercial HALEU production remains virtually non-existent in Western jurisdictions, with most advanced reactor developers relying on down-blended weapons-grade material for initial fuel supplies. This temporary solution cannot support commercial-scale SMR deployment, creating additional demand for both uranium feedstock and specialised enrichment services.

The parallel development of HALEU supply chains means that resolving uranium mining constraints represents only one component of the nuclear fuel supply challenge. Even adequate uranium concentrate availability becomes insufficient without corresponding enrichment capacity specifically configured for advanced reactor fuel requirements.

Mining Regions Holding the Key to Closing the Gap

Three tier-one uranium jurisdictions possess the geological resources, regulatory frameworks, and political stability necessary to meaningfully address global supply shortfalls: Canada, Australia, and the United States. These regions combine world-class uranium deposits with established mining industries and alignment with major consuming markets.

Canada: Athabasca Basin Advantages

Canada's Athabasca Basin hosts the world's highest-grade uranium deposits, with average grades significantly exceeding global benchmarks. The Hurricane deposit exemplifies this advantage, containing 48.6 million pounds U₃O₈ Indicated at extraordinary grades of 34.5% U₃O₈. For comparison, nearby deposits like Cameco's Tamarack average 4.42%, making Hurricane nearly eight times higher grade.

Key Canadian advantages include:

• Established regulatory framework with clear permitting pathways

• Proximity to processing infrastructure (McClean Lake mill within 40 kilometres)

• Existing transportation networks reducing development capital requirements

• Skilled workforce with decades of uranium mining experience

• Political stability ensuring long-term project viability

The exceptional grades found in Athabasca Basin deposits translate directly into lower operating costs, smaller environmental footprints, and projects capable of maintaining profitability across uranium price cycles. Hurricane's highest-grade core of 38,200 tonnes averages 52.1% U₃O₈, representing world-class mineralisation by any standard.

Australia: Scale and Political Stability

Australia controls the largest global uranium reserves at 28% of worldwide resources whilst maintaining geopolitical alignment with major consuming markets. The continent's uranium deposits, whilst typically lower grade than Athabasca Basin operations, offer large-scale, open-pit mining potential suitable for substantial production volumes.

The Wiluna Uranium Project in Western Australia demonstrates these characteristics, hosting 69.1 million pounds U₃O₈ Measured and Indicated across multiple shallow, near-surface deposits suited to conventional open-pit extraction and alkaline leach processing. This scale provides optionality for significant production capacity additions when uranium markets justify development investment.

Australian projects benefit from:

• Established mining infrastructure across multiple states

• Clear regulatory processes with defined environmental assessment procedures

• Strategic partnerships with Asian utilities seeking supply diversification

• Large-scale deposit potential enabling substantial production volumes

• Existing export facilities connecting to Pacific Rim markets

United States: Domestic Supply Security

American uranium mining offers strategic value through domestic supply security considerations, particularly as energy independence priorities influence utility procurement strategies. The Henry Mountains region in Utah exemplifies near-term production potential, with the Tony M mine leveraging past-producing status and existing permits to accelerate restart timelines.

| Region | Current Production (%) | Reserve Base (%) | Development Timeline |

|---|---|---|---|

| Kazakhstan | 43% | 12% | Limited expansion |

| Canada | 13% | 9% | 5-8 years |

| Australia | 12% | 28% | 7-10 years |

| United States | 0.3% | 5% | 3-5 years (restarts) |

U.S. uranium mining advantages include:

• In-Situ Recovery technology expertise developed in Wyoming and Texas basins

• Existing processing infrastructure (White Mesa Mill in Utah)

• Domestic utility preference for supply chain security

• Accelerated permitting potential for strategic mineral projects

• Past-producing mines offering shorter restart timelines

The Tony M operation demonstrates this potential, with existing state and federal permits representing 3-5 years of time savings and over US$1 million in avoided permitting costs compared to greenfield development projects. Furthermore, potential US uranium tariff disruptions could further emphasise the importance of domestic production capacity.

The next major ASX story will hit our subscribers first

Investment Implications of the Structural Supply Gap

The structural uranium supply gap creates investment dynamics fundamentally different from cyclical commodity opportunities. Traditional supply-demand balancing mechanisms cannot function effectively when development timelines exceed demand growth visibility, creating persistent pricing premiums for producers with near-term production capability.

Uranium Price Trajectory Analysis

Historical uranium price cycles reflected temporary supply-demand imbalances that resolved through production adjustments or demand destruction. Current market conditions indicate structural shortages that price mechanisms alone cannot correct within required timeframes. This distinction suggests sustained higher price levels rather than cyclical peaks followed by corrections.

Long-term contracting trends support this analysis, with utilities shifting from spot market reliance toward 8-15 year supply agreements at premium pricing. These contracts reflect utility recognition that uranium availability, not cost optimisation, represents the primary procurement constraint through the 2030s.

Mining Company Valuation Framework Evolution

Investment analysis must incorporate new variables reflecting structural supply constraints:

• Resource grade premiums become more significant as processing costs remain fixed

• Jurisdictional risk discounts increase due to supply chain security requirements

• Development timeline advantages create substantial net present value premiums

• Permitting status becomes a primary value driver regardless of resource scale

• Processing infrastructure access eliminates major capital expenditure requirements

Companies with advanced, permitted projects in tier-one jurisdictions command valuation multiples that reflect scarcity premiums rather than traditional mining economics. The Hurricane deposit's exceptional grade combined with proximity to existing processing infrastructure exemplifies this dynamic, where geological advantages compound logistical benefits.

Utility Procurement Strategy Transformation

Electric utilities are fundamentally altering uranium procurement approaches, prioritising supply security over historical cost minimisation strategies. This shift creates opportunities for producers offering:

• Long-term contract certainty with clear delivery timelines

• Geopolitical stability in producing jurisdictions

• Production capacity scalability beyond initial mine plans

• Supply chain transparency throughout the fuel cycle

• Strategic partnership potential for multi-decade relationships

Strategic inventory building has accelerated across major utilities, with many seeking to secure 3-5 years of forward fuel requirements rather than traditional 18-24 month coverage. This behaviour indicates recognition that spot market availability may become unreliable during periods of acute shortage.

Positioning for the Structural Shortage

Investors seeking exposure to the structural uranium supply gap must evaluate opportunities across multiple criteria that extend beyond traditional mining investment frameworks. The interplay between geological quality, jurisdictional advantages, and development timelines creates complex risk-reward profiles requiring specialised analysis.

Development-Stage Company Analysis

Companies advancing uranium projects toward production warrant evaluation across multiple dimensions:

Resource Quality Metrics:

• Grade comparison to regional benchmarks and global averages

• Resource category confidence (Measured, Indicated, Inferred classifications)

• Deposit geometry and mining method suitability

• Metallurgical characteristics and processing complexity

Jurisdictional Risk Assessment:

• Regulatory framework clarity and permitting timeline predictability

• Political stability and mining industry support

• Taxation regimes and royalty structures

• Infrastructure availability and development requirements

Management Team Evaluation:

• Track record in uranium project development and operations

• Experience navigating regulatory processes in relevant jurisdictions

• Capital markets access and funding capability

• Technical expertise across exploration, development, and production phases

Production Company Investment Considerations

Operating uranium producers offer different risk profiles reflecting current cash flow generation against future expansion optionality:

Cost Curve Positioning:

• All-in sustaining costs relative to long-term uranium price forecasts

• Operational flexibility during uranium price volatility periods

• Resource base longevity and reserve replacement capabilities

• Processing infrastructure ownership versus toll milling arrangements

Growth Optionality Assessment:

• Expansion potential at existing operations

• Development pipeline quality and advancement stage

• Capital requirements for production capacity increases

• Permitting status for expansion projects

Contract Book Analysis:

• Long-term contract coverage providing cash flow visibility

• Contract pricing mechanisms (fixed price versus market-linked)

• Customer diversification across utilities and geographic regions

• Contract renewal prospects and pricing renegotiation opportunities

Physical Uranium Investment Framework

Direct uranium ownership offers pure commodity exposure without operational or development risks, but requires consideration of unique characteristics:

Storage and Custody Requirements:

• Specialised facilities licensed for uranium storage

• Insurance coverage for radioactive materials

• Regulatory compliance across multiple jurisdictions

• Physical delivery logistics for potential sales

Liquidity Characteristics:

• Spot market depth and transaction volumes

• Conversion requirements between different uranium forms

• Market maker availability for large transactions

• Price discovery mechanisms during supply constraints

Regulatory Compliance Factors:

• Import/export licensing requirements

• Nuclear material accounting and reporting obligations

• Security protocols for radioactive material handling

• International safeguards compliance

Risk Analysis: Challenges to the Supply Gap Thesis

Whilst structural uranium supply constraints appear compelling, several factors could alter the projected supply-demand trajectory. Investors must consider scenarios where current assumptions prove incorrect or external developments change market fundamentals.

Demand-Side Variables and Potential Reversals

Nuclear reactor construction faces multiple risks that could reduce projected uranium consumption:

Construction Timeline Delays:

• Complex engineering requirements extending project schedules

• Regulatory approval processes taking longer than anticipated

• Capital cost overruns affecting project economics

• Supply chain constraints in specialised reactor components

Policy Reversals on Nuclear Energy:

• Political changes affecting long-term nuclear energy support

• Public opposition following potential nuclear incidents

• Alternative energy technology cost improvements

• Grid integration challenges with increased renewable penetration

Competition from Alternative Technologies:

• Battery storage cost reductions enabling renewable baseload alternatives

• Hydrogen production methods providing long-term energy storage

• Fusion power development accelerating beyond current projections

• Energy efficiency improvements reducing overall electricity demand

Supply-Side Upside Scenarios

Several developments could increase uranium availability beyond current projections:

Technological Breakthroughs in Extraction:

• Advanced ISR techniques accessing previously uneconomic deposits

• Seawater uranium extraction becoming commercially viable

• Ore processing innovations improving recovery rates from lower-grade material

• Automation reducing mining costs and accelerating development timelines

New Discovery Potential:

• Unexplored regions yielding significant uranium discoveries

• Advanced exploration techniques identifying overlooked deposits

• Geopolitical changes opening previously inaccessible uranium regions

• Unconventional uranium sources becoming economically extractable

Secondary Supply Source Extensions:

• Additional military stockpile releases from undisclosed inventories

• Reactor lifetime extensions reducing uranium demand per facility

• Recycling technology improvements extracting more uranium from waste

• International cooperation programmes mobilising strategic reserves

Market Structure Considerations

Uranium market dynamics could evolve in ways that alter current supply-demand projections:

Long-term Contract Versus Spot Market Evolution:

• Utilities shifting procurement strategies away from long-term contracting

• Spot market liquidity improving through financial instruments

• Price discovery mechanisms changing during extended supply constraints

• Market manipulation risks in highly concentrated supply chains

Utility Inventory Management Strategy Changes:

• Inventory optimisation reducing apparent demand growth

• Just-in-time procurement becoming more sophisticated

• Supply chain financing innovations reducing working capital requirements

• Coordinated utility procurement creating buyer market power

Geopolitical Stability Assumptions:

• Producer country relationships with consuming nations improving

• International trade agreements reducing supply chain restrictions

• Political risks in major producing regions being overestimated

• Emergency supply sharing agreements between allied nations

Strategic Positioning for Market Participants

The structural uranium supply gap creates opportunities across multiple participant categories, each requiring tailored approaches reflecting different risk tolerances and investment horizons. Success demands understanding how supply constraints translate into value creation across the nuclear fuel cycle.

Quality-Focused Asset Selection

Resource grade quality becomes increasingly important during periods of supply constraint, as higher-grade deposits maintain profitability across broader price ranges whilst offering superior economics during supply shortages. The Hurricane deposit's 34.5% U₃O₈ grade compared to global averages of 0.1-0.5% demonstrates this principle, where exceptional geology creates sustainable competitive advantages.

Jurisdictional quality deserves equal consideration, as regulatory certainty and political stability provide development timeline predictability. Canadian, Australian, and American projects offer established frameworks where permitting processes, whilst complex, follow predictable pathways compared to jurisdictions with evolving regulatory regimes.

Geographic Diversification Strategies

Supply chain security concerns encourage diversification across multiple producing regions rather than concentration in lowest-cost jurisdictions. The five-country production dominance creates systemic risks that utilities increasingly recognise, driving procurement strategies toward geographically distributed supply sources.

Investment portfolios should reflect this diversification imperative, balancing exposure across:

• High-grade, smaller-scale projects in established mining jurisdictions

• Large-scale, lower-grade deposits suitable for substantial production volumes

• Near-term production candidates offering shorter development timelines

• Long-term development projects positioned for future supply requirements

• Different mining methods (underground, open-pit, ISR) providing operational diversity

Timeline Alignment with Investment Horizons

The structural nature of uranium supply constraints means investment returns will likely manifest over extended periods rather than through rapid appreciation cycles. Successful positioning requires aligning investment timelines with development schedules and production ramp-up phases.

Near-term catalysts (2024-2027):

• Bulk sampling results and production restart decisions

• Regulatory approvals for advanced projects

• Long-term contract announcements with major utilities

• Resource estimate updates at exploration-stage projects

Medium-term value creation (2027-2032):

• First production from development-stage projects

• Production capacity expansions at existing operations

• Advanced reactor deployment creating HALEU demand

• Secondary supply depletion forcing primary market reliance

Long-term structural benefits (2032-2040):

• Full-scale advanced reactor deployment

• Complete secondary supply exhaustion

• Peak uranium demand from nuclear capacity tripling initiatives

• Market rebalancing through new mine development

Uranium investment strategies that incorporate these considerations are essential for navigating this complex market environment. Additionally, understanding the broader implications of a nuclear fuel supply chain is crucial for comprehensive investment planning.

Investment decisions in uranium markets require careful consideration of multiple risk factors, including regulatory changes, technological developments, and geopolitical events that could significantly impact returns. This analysis does not constitute financial advice and investors should conduct independent research and consult qualified professionals before making investment decisions. Past performance does not guarantee future results, and uranium investments carry substantial risks including commodity price volatility, regulatory uncertainty, and operational challenges specific to nuclear materials.

The structural uranium supply gap represents a fundamental shift in nuclear fuel market dynamics, where traditional supply-demand balancing mechanisms cannot function effectively due to extended development timelines and capital constraints. This creates unprecedented opportunities for investors positioned correctly across the supply chain, provided they understand the complex interplay between geological quality, jurisdictional advantages, and development execution capabilities that will determine long-term success in this evolving market landscape.

Moreover, analysts increasingly highlight that the uranium market is experiencing a structural deficit that could drive multi-year bull market conditions. Financial institutions are also recognising these dynamics, with some forecasting uranium prices could reach US$200 per pound as supply constraints tighten further.

Ready to Capitalise on the Next Uranium Discovery?

Discovery Alert's proprietary Discovery IQ model provides instant notifications when significant uranium discoveries are announced on the ASX, helping investors identify actionable opportunities before broader market awareness develops. Begin your 14-day free trial today and position yourself ahead of the structural supply gap that's reshaping the uranium investment landscape.