June 9, 2026

When Supply Becomes the Binding Constraint in Uranium Markets

Commodity markets have a well-documented tendency to punish the risk nobody is watching. For uranium, the uranium supply shortage that preoccupied investors for the better part of three decades was demand: would nuclear power survive politically, economically, and culturally in a world shaped by Chernobyl, Fukushima, and the relentless cost decline of renewable energy? That question consumed capital allocation decisions, suppressed exploration budgets, and kept a generation of development projects in indefinite suspension.

The answer has now arrived with enough clarity to reframe the entire investment thesis. Governments across the United States, Europe, and Asia are not retreating from nuclear power. They are expanding it. The risk that defined uranium's bear case for decades has been largely resolved, and in its place a structurally more complex problem has emerged: whether the ground can physically deliver enough uranium to feed the reactors the world is now committed to building.

This is not a marginal adjustment to the supply-demand balance. It represents a fundamental regime change in where risk sits within the uranium market, and it has direct consequences for how capital should be positioned across the investment spectrum. Understanding uranium supply-demand volatility is, consequently, more critical than ever for informed investors.

When big ASX news breaks, our subscribers know first

The Uranium Supply Shortage in Numbers

The scale of the uranium supply shortage becomes clearer when the underlying data is examined without the noise of short-term price movements. Primary mine production has not covered global reactor requirements since 1991. For more than three decades, the gap between what mines produce and what reactors consume has been bridged by secondary sources: commercial inventories, reprocessed material, and disarmament-derived supply from Cold War-era stockpiles.

Those secondary buffers are diminishing. Commercial inventories peaked in 2021 and have been in accelerating decline since. The World Nuclear Association projects that output from mines currently in operation could fall by roughly half between 2030 and 2040 as existing ore bodies are progressively depleted, even as reactor demand continues its upward trajectory driven by new build programmes in China, the United States, and across Europe.

| Metric | Data Point |

|---|---|

| Primary mine supply vs. reactor demand | Below requirements since 1991 |

| 2024 mine supply coverage of global demand | ~89% |

| Commercial inventory trend | Peaked 2021; declining since |

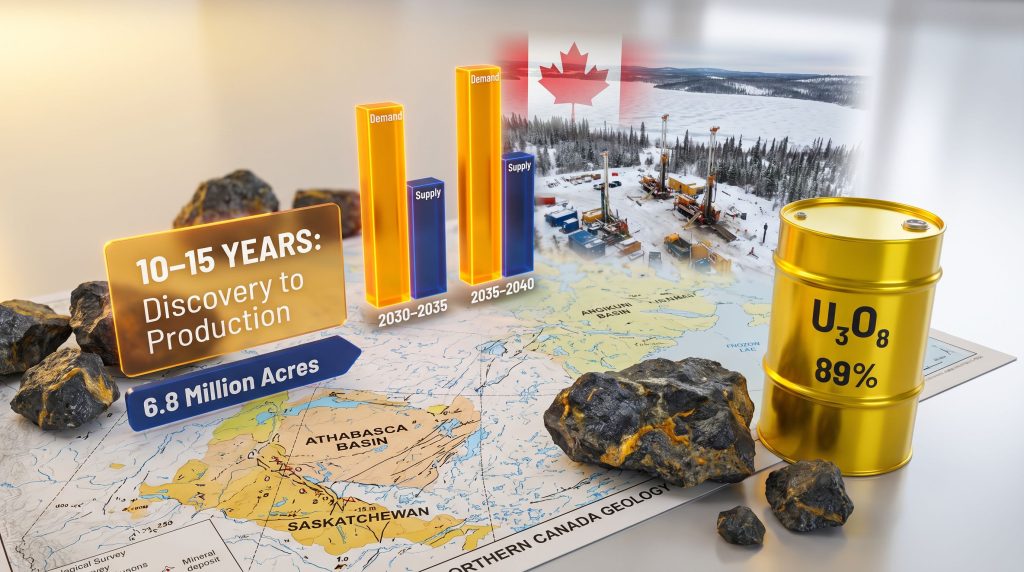

| Average mine development timeline | 10-15 years from investment to production |

| Projected output decline (existing mines) | Could halve between 2030 and 2040 |

| Cameco combined annual output | 15-18 million pounds U₃O₈ per year |

The arithmetic is unforgiving. In 2024, primary mines covered approximately 89% of global reactor demand. The remaining 11% came from secondary supply sources whose reliability diminishes with each passing year as inventories thin. New mines require 10 to 15 years from the point of investment to first production. That means any discovery made today will not contribute meaningfully to global supply until the mid-2030s at the earliest.

Furthermore, the growing uranium market deficit underscores precisely why the World Nuclear Association has warned that a nuclear renaissance could create a critical shortage of supply.

Critical insight: The uranium supply shortage is not a future event to be avoided. It is a structural condition already in progress, with secondary inventory drawdowns masking the true scale of the primary production deficit. When those buffers are exhausted, the market will be exposed to the full extent of the imbalance that has been building since 1991.

How Concentrated Supply Amplifies Operational Risk

One feature of the uranium market that is poorly understood outside specialist circles is the degree to which global production is concentrated in a small number of operating assets. Kazakhstan accounts for roughly 40 to 45% of world mine output. Canada and Australia together contribute a substantial further share, but within those jurisdictions, production is dominated by a handful of world-class operations.

This concentration has historically been framed as a positive: high-grade, tier-1 assets in stable jurisdictions are precisely what producers and utilities want. However, concentration is a double-edged characteristic. When a small number of assets underpin a significant portion of global supply, even localised operational disruptions carry outsized market consequences.

The practical implications of this dynamic were demonstrated when Cameco temporarily halted operations at the Key Lake mill and reduced activity at McArthur River in Saskatchewan following flooding and ice buildup on the Modstone River Bridge. A seasonal weather event, the kind that would be absorbed without consequence in a more distributed supply base, was sufficient to threaten output from one of the world's largest uranium production complexes. McArthur River and Key Lake together, alongside Cigar Lake, produce between 15 and 18 million pounds of U₃O₈ annually, representing a meaningful proportion of global primary supply.

The episode illustrates a broader vulnerability that extends well beyond Saskatchewan:

- Geopolitical friction affecting Russian uranium supply chains has already introduced meaningful uncertainty into global conversion and enrichment markets

- Production underperformance at Kazakh operations, which account for the single largest share of world output, has occurred in multiple recent years due to sulphuric acid supply constraints affecting in-situ recovery operations

- Logistical and political challenges in Namibia and Niger have periodically disrupted output from those producing jurisdictions

In addition, the Russian uranium import ban has further complicated the supply picture for Western utilities already navigating tightening inventory conditions.

Scenario: If two or more of the world's top five uranium-producing operations experienced simultaneous disruptions, whether from weather, regulatory action, geopolitical friction, or technical failures, secondary inventory drawdowns would accelerate sharply. The result could be rapid repricing of long-term supply contracts at a time when utilities are already competing to secure forward coverage.

The Policy Reversal Driving Demand

Understanding the uranium supply shortage requires understanding why demand certainty has increased so dramatically in a relatively compressed timeframe. The nuclear policy reversal across major economies has been both broad and durable.

In the United States, legislative and executive support for domestic nuclear development has extended to funding mechanisms for advanced reactor technologies, life extensions for existing plants, and, critically, measures targeting domestic uranium production and enrichment capacity to reduce dependence on Russian supply chains. China's nuclear buildout is proceeding at a pace that, considered in isolation, commands significant attention: the country is deploying new reactor capacity faster than any other nation and has dozens of units either under construction or in advanced planning stages.

Beyond these two anchors, the broader shift is notable for its geographic breadth:

- Japan has been progressively restarting reactors idled after Fukushima and has outlined plans to extend operating lifetimes and potentially build new capacity

- France, historically the world's most nuclear-intensive electricity system by share of generation, has committed to a new build programme after years of ambiguity

- Several Eastern European nations are advancing new reactor projects as part of energy security diversification strategies

- South Korea reversed course on its nuclear phase-out under new political direction

The combined effect of these policy commitments is a structural floor under long-term uranium demand that did not exist five years ago. Utilities are responding by shifting their contracting behaviour, locking in longer-term supply agreements that remove uncommitted pounds from the spot market and compound the tightening effect on available inventory.

Why the Development Pipeline Cannot Respond Quickly

The instinctive market response to supply tightness is investment in new production. In uranium, that mechanism faces a structural complication that distinguishes it from most other commodity sectors: the development timeline is extraordinarily long.

The lean years following Fukushima did not just suppress uranium prices. They effectively halted the exploration and project development activity that populates the mine development funnel. Companies that survived the downturn did so through capital preservation, maintaining ownership of existing assets rather than advancing them toward production. The result is a sector where resource-stage and development-stage projects are genuinely scarce relative to the scale of supply that will eventually be required.

The full mine development sequence for a uranium project:

- Grassroots exploration – Regional geophysical surveys, structural mapping, and initial drilling: 2-4 years

- Resource delineation – Infill drilling, geological modelling, and resource estimation to NI 43-101 or JORC standard: 3-5 years

- Feasibility and permitting – Environmental impact assessments, feasibility studies, and regulatory approval processes: 3-5 years

- Construction and commissioning – Mine development, processing infrastructure, and site establishment: 2-4 years

- Ramp-up to nameplate capacity – Achieving full permitted production rates: 1-2 years

Total elapsed time from discovery to first meaningful production: a minimum of 10 to 15 years.

This timeline has a direct and sobering implication for the uranium supply shortage. Discoveries made during the 2025 and 2026 field seasons, even if they represent genuine world-class deposits, will not contribute to global supply until the late 2030s. That is precisely the period when the World Nuclear Association projects the steepest decline in output from currently operating mines. For a broader perspective on uranium market dynamics, this pipeline constraint is perhaps the most consequential structural feature investors must account for.

| Time Horizon | Supply Outlook | Demand Trajectory |

|---|---|---|

| 2024-2026 | Partially supported by secondary inventories | Stable, growing moderately |

| 2027-2030 | Inventory buffer thinning; very limited new mines | Accelerating with new reactor startups |

| 2030-2035 | Existing mine depletion accelerating | Peak growth phase globally |

| 2035-2040 | Potential halving of current mine output | Sustained high demand |

Canada's Northern Basins and the Geological Case for Frontier Exploration

Canada hosts two of the most significant uranium geological settings on the planet. The Athabasca Basin in Saskatchewan is the world's highest-grade uranium district, with unconformity-hosted deposits that have been the subject of intensive exploration and development for decades. Less appreciated, but geologically compelling, are the underexplored basins further north in Nunavut: the Thelon Basin and the Angikuni Basin.

Unconformity-related uranium deposits, the deposit type responsible for the Athabasca Basin's exceptional grades, form at or near the contact between ancient basement rocks and overlying sedimentary sequences. The structural and lithological conditions that give rise to these deposits are not unique to the Athabasca. The Thelon and Angikuni Basins share key geological characteristics with the Athabasca: similar Proterozoic sedimentary sequences, comparable basement rock compositions, and analogous structural architecture. The difference is the level of modern systematic exploration each has received.

According to the World Nuclear Association, unconformity-type deposits represent some of the highest-grade uranium resources on the planet, making Canada's northern basins strategically significant in any credible long-term supply outlook.

ATHA Energy (TSX.V: SASK) has assembled a land position totalling 6.8 million cumulative prospective exploration acres across Canada's principal uranium basins, including 100% control of the Angikuni Basin in Nunavut. The company's Angilak Uranium Project sits in a geological corridor between the Athabasca and Thelon Basins that exploration work has now confirmed shares structural characteristics with producing Athabasca deposits.

What the 2024-2025 Drilling Results Demonstrated

The exploration logic behind large-scale land consolidation in frontier uranium basins is straightforward: if future supply must come from new discoveries, controlling prospective ground in tier-1 jurisdictions becomes a primary value driver. The 2024 and 2025 field seasons at Angilak tested that logic empirically.

Approximately 22,000 metres of drilling was completed across widely spaced regional targets, with no drilling directed into the existing Lac 50 deposit. The results were notable for their consistency: every single target tested returned uranium mineralisation, a 100% mineralisation success rate across a geographically dispersed programme.

Key metrics from the Angikuni Basin exploration programme:

| Exploration Parameter | Detail |

|---|---|

| Total prospective acreage controlled | 6.8 million cumulative acres |

| 2024-2025 drilling programme | ~22,000 metres across widely spaced targets |

| Mineralisation success rate | 100% of targets tested |

| New regional discoveries (2025) | 5 new discoveries within Angikuni Basin |

| Maiden hole at RIB North | 34.7 metres composite mineralisation; up to 8.16% U₃O₈ over 0.5 metres |

| Lac 50 exploration target | 61-98 million pounds U₃O₈ |

| Lac 50 structural strike length (3D modelling) | 21 kilometres identified; only deposit area drilled |

| 2026 drilling programme | ~20,000 metres across 3 mineralised corridors |

| 2026 programme funding | C$63 million financing closed February 2026 |

The grade intercept at RIB North deserves particular attention. A result of 8.16% U₃O₈ over 0.5 metres within a composite 34.7-metre mineralised interval is consistent with the high-grade characteristics of unconformity-style mineralisation in the Athabasca Basin. For context, average uranium mine grades globally sit well below 1% U₃O₈. High-grade unconformity deposits in the Athabasca Basin typically range from 1% to above 20% U₃O₈ in their richest intervals, making them profoundly different in economic character from the low-grade sandstone deposits that dominate production in the United States and parts of Africa.

Investors keen on interpreting drill results will recognise that these grade intercepts at RIB North represent a materially significant discovery threshold for unconformity-style mineralisation.

The next major ASX story will hit our subscribers first

The 2026 Angilak Programme: Building the Delineation Case

The 2026 Angilak Exploration Programme commenced diamond drilling on 1 May 2026, representing the largest single-season exploration effort undertaken on the project. Three drill rigs are scheduled to complete approximately 20,000 metres through to the end of September, targeting three defined mineralised corridors.

The three-corridor drilling strategy:

- Mineralised RIB Corridor – Expanding the 2025 discovery footprint and testing additional targets along the structural strike, building directly on the 34.7-metre maiden hole result at RIB North

- Lac 50 Deposit Corridor – Testing strike extensions identified through updated 3D inversion modelling along a 21-kilometre structural trend, the vast majority of which has not yet been subjected to drilling

- KU-Nine Iron Corridor – Targeting vectors that extend from uranium intersections recorded during the 2025 campaign, testing whether those results define the edge of a larger mineralised system

Complementing the drilling, an aerial Magnetotelluric (MMT) electromagnetic survey is scheduled across the full Angikuni Basin from late June, with 3D inversion modelling targeted for completion by the fourth quarter of 2026. MMT surveying is a geophysical technique particularly suited to mapping the conductive graphitic structures and fault zones associated with unconformity uranium mineralisation at depth, providing the subsurface imaging needed to guide systematic delineation drilling.

The programme is fully funded following the C$63 million financing closed in February 2026, positioning ATHA among the best-capitalised junior uranium exploration companies globally at a time when exploration capital constraints are forcing most peers to operate at reduced pace and scale.

Why capitalisation matters in uranium exploration: The exploration-to-production timeline for uranium spans a decade or more. Companies that can sustain continuous, uninterrupted drilling programmes accumulate a compounding advantage in resource definition over peers who must halt programmes to raise capital. A fully funded multi-year exploration programme is not merely a financial convenience; it is a structural competitive differentiator.

Investment Implications of a Structurally Tight Uranium Market

When supply is the binding constraint in a commodity market rather than demand, the distribution of value across the investment spectrum shifts in a predictable direction: upstream, toward the assets that control future production potential.

Tier-1 producers operating at or near capacity benefit from higher realised prices but face limited ability to grow output rapidly. Their existing ore bodies are being depleted, expansion options are constrained by geology and permitting timelines, and new development within their existing footprints requires years of additional investment before contributing incremental production.

The exploration and early-stage development segment occupies a different position. Companies whose discoveries represent the only credible source of new supply over the coming decade carry a strategic significance that is not yet fully reflected in market valuations for the sector's less visible participants. Indeed, as money management analysts have noted, uranium supply is approaching a tipping point that warrants serious consideration from institutional investors.

Key risk factors that could alter the supply outlook:

| Risk Category | Potential Impact | Probability Assessment |

|---|---|---|

| Geopolitical disruption (Russian supply chains) | Accelerates Western supply deficit | Moderate-High |

| Kazakhstan production underperformance | Removes largest single supply source | Moderate |

| Permitting delays on advanced projects | Extends supply response timeline | High |

| Secondary inventory exhaustion ahead of schedule | Triggers earlier price escalation | Moderate |

| Exploration capital constraints in junior sector | Slows discovery pipeline | High |

| Accelerated reactor buildout (China, US, EU) | Widens demand-supply gap | Moderate-High |

One underappreciated dynamic in the junior uranium sector is that permitting delays consistently rank among the highest-probability risk factors. Environmental assessment processes in Canada, while operating within a well-established regulatory framework, can extend project timelines significantly when triggered by comprehensive review requirements in sensitive northern jurisdictions. This makes early-stage exploration in Nunavut a longer-dated investment proposition than comparable work in Saskatchewan, but it does not diminish the geological prospectivity of the terrain.

Three Scenarios for the Supply Balance Through 2035

Scenario 1: Orderly Transition (Base Case)

Advanced development projects proceed broadly on schedule. Secondary inventories are managed carefully by utilities, and exploration programmes in Canada's northern basins advance toward resource delineation within the decade. The uranium supply shortage persists but remains manageable, supporting elevated prices without triggering acute fuel availability crises.

Scenario 2: Delayed Pipeline (Bear Case for Supply)

Permitting delays, capital constraints across the junior sector, and continued production underperformance at major operations combine to push the supply response timeline out by three to five years. Secondary inventories are exhausted ahead of projections. Utilities scramble to secure long-term contracts, and uranium prices escalate sharply as the market prices in a genuine supply emergency.

Scenario 3: Accelerated Discovery (Bull Case for Exploration)

Systematic exploration in underexplored northern basins generates multiple large-scale discoveries that advance rapidly through delineation. Well-capitalised companies with substantial land positions in tier-1 jurisdictions translate exploration success into resource estimates ahead of schedule, partially offsetting the structural supply deficit and attracting institutional capital into the sector at scale.

The three scenarios are not equally probable, and investors should be cautious about extrapolating any single pathway. However, what is common to all three scenarios is the conclusion that the uranium supply shortage will remain the defining structural feature of the market through the 2030s. The variable is not whether the deficit exists, but how severe it becomes and how quickly credible supply solutions emerge.

Frequently Asked Questions: Uranium Supply Shortage

What is causing the current uranium supply shortage?

The shortage reflects a structural imbalance between primary mine output and reactor fuel requirements that has persisted since the early 1990s. Secondary inventories accumulated during periods of oversupply historically bridged this gap, but those buffers peaked in 2021 and have been declining since. With new mine development requiring 10 to 15 years from investment to first production, the supply response to rising demand cannot occur quickly enough to prevent a widening deficit through the 2030s.

How much of global uranium demand is currently covered by mine production?

Primary mine supply covered approximately 89% of global reactor demand in 2024. The remaining 11% was sourced from secondary supplies including commercial inventories, reprocessed material, and other non-primary sources. As inventories decline, this secondary contribution becomes progressively less reliable as a buffer against primary supply shortfalls.

Which countries produce the most uranium?

Kazakhstan is the world's largest uranium producer, accounting for roughly 40 to 45% of global mine output. Canada and Australia are the next largest producers, followed by Namibia, Uzbekistan, Russia, and Niger. The concentration of supply in a small number of jurisdictions creates systemic exposure to geopolitical and operational disruptions.

Why can't existing mines simply increase production to meet demand?

Most tier-1 uranium operations are already producing at or near their permitted and operational capacity. Expanding output at existing mines requires additional capital investment, regulatory approvals, and in some cases access to deeper or lower-grade ore, all of which take time. New mines face the full 10 to 15 year development timeline regardless of uranium price conditions.

Where are the most prospective regions for new uranium discoveries?

Canada's Athabasca Basin remains the world's highest-grade uranium district. Northern Canadian basins, including the Thelon and Angikuni Basins in Nunavut, are increasingly recognised as prospective for Athabasca-style unconformity deposits and are in the early stages of systematic modern exploration. Australia's Gawler Craton and parts of Africa also host significant undeveloped uranium resources, though the grade profiles of most undeveloped deposits outside the Athabasca-style category are considerably lower.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forecasts, projections, and scenario analyses referenced in this article involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Investors should conduct their own due diligence and seek independent financial advice before making investment decisions. Past performance of commodity prices and exploration programmes is not indicative of future results.

Want To Be First When the Next Major Uranium Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, cutting through complex data to surface actionable opportunities before the broader market reacts — explore historic discoveries and their returns to understand what early positioning in a major find can mean, then begin your 14-day free trial to secure your market-leading edge.