June 11, 2026

The global race for technological supremacy has transformed U.S.-China rare earth supply chain competition into one of the most consequential strategic contests of the modern era. While traditional trade disputes focus on tariffs and quotas, the U.S.-China rare earth supply chain competition represents a fundamentally different challenge, where control over processing infrastructure matters more than access to raw materials. This competition extends beyond conventional economic metrics into the realm of national security, industrial policy, and technological sovereignty.

Unlike previous commodity cycles driven by price volatility or demand shocks, the current rare earth dynamics reflect deeper questions about economic interdependence in an era of great power competition. The seventeen elements classified as rare earths have become proxy battlegrounds for broader strategic objectives, with implications that extend far beyond mining operations into the core of critical minerals energy transition, defence manufacturing, and semiconductor production.

Understanding the Strategic Foundation of Rare Earth Competition

The strategic importance of rare earth elements stems from their unique magnetic, catalytic, and optical properties that make them irreplaceable in high-performance applications. These seventeen elements, comprising the lanthanide series plus yttrium and scandium, serve as critical inputs across defence systems, electric vehicles, wind turbines, and advanced electronics.

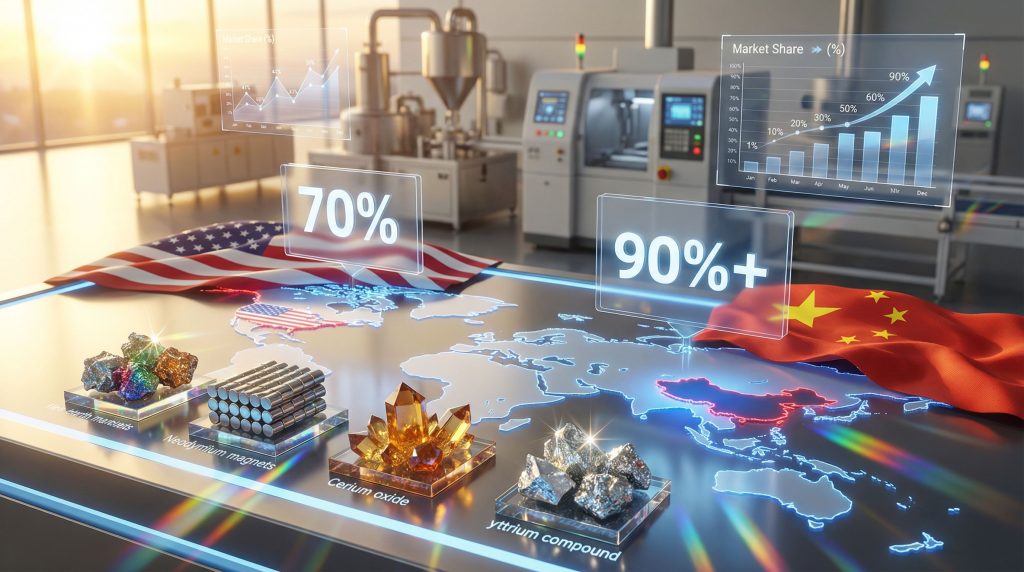

Global production reached approximately 890,000 tonnes of rare earth oxide equivalent (TREO) in 2023, with China accounting for roughly 70% of mining output. However, the real strategic chokepoint lies downstream in processing and manufacturing, where China controls over 90% of separation capacity and magnet production facilities.

Critical Applications Driving Strategic Value

Modern defence systems depend heavily on rare earth permanent magnets for guidance systems, radar arrays, and electronic warfare equipment. Each electric vehicle motor requires approximately 0.5-1.0 kg of rare earth permanent magnets, while wind turbines utilising permanent magnet generators need 150-600 kg of rare earth magnets per megawatt of capacity.

The semiconductor industry relies on rare earth elements for manufacturing equipment and precision optics, though specific demand projections remain classified due to national security considerations. This broad industrial dependency creates systemic vulnerabilities that extend beyond any single sector.

Supply Chain Concentration Risks

| Supply Chain Stage | China's Market Share | Key Vulnerabilities |

|---|---|---|

| Mining Operations | 70% | Alternative sources available |

| Processing/Separation | 90%+ | Critical bottleneck |

| Magnet Manufacturing | 85-90% | Strategic leverage point |

| Finished Applications | Variable | End-use integration |

The International Energy Agency projects global electric vehicle sales could reach 35-40 million units annually by 2030, requiring magnet demand to increase 3-4x from 2020 baseline levels. Similarly, global wind capacity targets of over 2,000 GW by 2030 represent significant additional rare earth demand across renewable energy infrastructure.

When big ASX news breaks, our subscribers know first

China's Integrated Control Architecture

China's rare earth dominance reflects decades of strategic industrial policy combining resource control, processing expertise, and manufacturing integration. This approach differs fundamentally from traditional commodity markets, where mining and processing often operate as separate industries across multiple countries.

Vertical Integration Strategy

Chinese rare earth operations integrate mining through finished magnet production under coordinated government oversight. Major state-linked producers including Baogang Rare Earth Group, China Northern Rare Earth Group, and Jinchang Rare Earths operate under production quotas set by the Ministry of Natural Resources and published quarterly.

China's annual processing capacity reaches 350,000-400,000 tonnes, concentrated primarily in Guangdong, Sichuan, and Inner Mongolia provinces. These facilities operate at 40-70% utilisation rates, with profitability heavily dependent on export licensing approval and downstream demand patterns.

Neodymium-iron-boron (NdFeB) magnet production capacity in China approaches 170,000-180,000 tonnes annually, representing approximately 85-90% of global production. Major manufacturers include Ningbo Yunsheng, Innuovo Materials, and various Lynas-linked facilities operating under joint venture structures.

Administrative Control Mechanisms

China employs a sophisticated licensing system rather than traditional export restrictions. This approach includes:

• Automatic approval for specified non-sensitive applications

• Case-by-case review for dual-use and sensitive technologies

• Denial procedures for military-related end-uses in restricted jurisdictions

The Ministry of Industry and Information Technology (MIIT) coordinates with the Ministry of Commerce on export licensing decisions, creating administrative flexibility that can respond rapidly to changing geopolitical conditions.

Processing Technology Advantages

China's processing dominance extends beyond simple capacity to include technical expertise in separation chemistry and quality control. Modern rare earth separation requires complex solvent extraction processes with precise pH control, temperature management, and waste handling protocols that took decades to optimise.

China's approach prioritises finished product exports over raw material access, creating immediate industry disruption while maintaining long-term leverage through processing bottlenecks.

Historical examples demonstrate this leverage potential. During 2010-2011, China restricted dysprosium oxide exports for high-temperature magnet applications, creating supply shocks that forced global magnet manufacturers to reformulate products and led to 200%+ price increases for dysprosium-heavy grades.

Beijing's Strategic Contradictions in 2026

China faces fundamental tensions between maintaining rare earth leverage and promoting broader economic growth objectives. The Asia Society Policy Institute's December 2025 analysis identifies this as a core strategic contradiction, where tools that enhance short-term control often suppress the commercial dynamism needed for long-term competitiveness.

Economic Structural Challenges

China's official GDP growth rate of 5.0% in 2024 masks underlying structural headwinds, with international economists estimating actual growth closer to 3.5-4.5%. Youth unemployment peaked at over 21% in mid-2023 before reporting suspension, while current estimates suggest 16-18% unemployment among urban youth aged 15-24.

Local government hidden debt reaches an estimated 25-40 trillion RMB ($3.5-5.5 trillion USD) across provincial and municipal levels, heavily concentrated in infrastructure projects with declining revenue potential. Rare earth mining and processing regions face particular fiscal pressures from environmental remediation liabilities accumulated over decades of extraction operations.

Demographic and Consumption Pressures

China's population declined by 850,000 in 2023 and an estimated 1.1 million in 2024, marking consecutive years of demographic contraction. The working-age population has contracted consistently since 2012, creating labour supply constraints in manufacturing-intensive sectors including rare earth processing.

Household consumption remains depressed at 52-54% of GDP, significantly below pre-COVID levels of 58-60% and OECD averages of 65-70%. This consumption weakness creates export dependency for rare earth producers, making them vulnerable to external demand shocks and trade disruptions.

Administrative Risk Aversion

Chinese industrial policy in sensitive sectors like rare earths operates through approval frameworks that prioritise stability over market efficiency. This creates delays in new capacity development and discourages private investment in dual-use technologies where regulatory uncertainty persists.

Risk-averse bureaucratic structures slow innovation and capacity expansion, potentially undermining China's technological competitiveness in advanced materials processing. Local officials facing debt service pressures may prioritise short-term export revenues over long-term industrial optimisation.

Export Controls as Strategic Leverage Tools

China has systematically expanded rare earth export restrictions since 2023, targeting downstream applications rather than raw materials. This approach maximises industrial disruption while maintaining commercial relationships in non-sensitive sectors, reflecting broader patterns observed in the US-China trade war impact across multiple industries.

Recent Control Escalation Timeline

April 2025: China implemented restrictions on seven rare earth elements, requiring special licensing for exports to designated countries and end-uses.

December 2025: New regulations banned rare earth exports to military-linked entities in the United States, Europe, and allied nations, with case-by-case review requirements for civilian applications.

October 2025: Advanced magnet manufacturing technology became subject to export licensing, effectively restricting knowledge transfer for high-performance applications.

Weaponised Interdependence Strategy

China's control strategy focuses on creating immediate supply disruptions while maintaining long-term processing advantages. This approach includes:

• Targeting finished products rather than raw ore exports

• Maintaining commercial access for non-sensitive applications

• Creating regulatory uncertainty that complicates long-term planning

• Preserving processing bottlenecks that ensure continued relevance

The effectiveness of this strategy depends on maintaining credible leverage without triggering complete supply chain diversification by importing countries. Excessive restrictions risk accelerating alternative source development and permanent market share loss.

U.S. Industrial Response and Vulnerability Reduction

The United States has shifted from viewing rare earths as primarily a mining challenge to recognising the need for complete supply chain integration. This systems-level approach acknowledges that processing and manufacturing capabilities matter more than raw material access for strategic independence, as outlined in recent critical minerals executive order directives.

Building Complete Magnet Production Capacity

Recent U.S. investments focus on integrated supply chains rather than isolated mining projects. MP Materials received a $150 million government loan for separation and magnet manufacturing facilities in California, while the Department of Defence committed $400 million in stock purchases to support domestic production scaling.

The Biden administration's $1 billion financing package for critical minerals partnerships targets allied coordination rather than purely domestic capacity, recognising cost and technical advantages of international collaboration.

Integration Timeline Challenges

Building complete rare earth supply chains requires coordination across multiple technical stages:

- Separation and purification (5-7 year development timeline)

- Metal and alloy production (3-4 year development timeline)

- Magnet manufacturing (2-3 year development timeline)

- Quality qualification (1-2 year testing and certification)

Current U.S. aspirations for 18-24 month vulnerability reduction appear optimistic given these technical requirements and the need for skilled workforce development across multiple specialities.

Allied Coordination Framework

The U.S. strategy emphasises multilateral partnerships rather than complete domestic integration. Key initiatives include:

• G7 working groups for supply chain diversification

• Bilateral agreements with Australia, Malaysia, Cambodia, and Japan

• Allied stockpiling programmes for strategic reserves

• Technology sharing arrangements for processing expertise

This approach recognises economic realities while building strategic flexibility through multiple supply sources and shared technological capabilities.

Mutual Vulnerability and Disruption Equilibrium

The current U.S.-China rare earth supply chain competition exists within a framework of mutual vulnerability, where both sides possess leverage but face constraints on its exercise. This creates a temporary equilibrium that could shift rapidly as vulnerabilities change.

Current Vulnerability Assessment

United States Dependencies:

- 90%+ reliance on Chinese processing for separated rare earth materials

- 85-90% dependence on Chinese magnet manufacturing

- Limited qualified alternatives for defence-grade applications

Chinese Vulnerabilities:

- Export revenue dependence from Western markets

- Technology gaps in advanced separation and purification

- Environmental compliance costs limiting expansion options

Global Production Capacity Outside China

| Component | Non-Chinese Capacity | Development Timeline | Key Bottlenecks |

|---|---|---|---|

| Raw Materials | ~250,000 tonnes TREO | 3-5 years expansion | Mine development, permits |

| Processing | ~50,000 tonnes capacity | 5-7 years buildout | Technical expertise |

| Magnets | ~50,000 tonnes annually | 2-3 years scaling | Manufacturing equipment |

Global magnet production capacity outside China totals approximately 50,000 tonnes annually, representing roughly 25-30% of total demand. This capacity concentration creates systemic vulnerabilities but also opportunities for rapid scaling under appropriate investment and policy support.

Escalation Risk Scenarios

Several factors could destabilise the current equilibrium:

• Accelerated U.S. capacity development reducing Chinese leverage

• Complete breakdown of predictable export licensing

• Broader trade war escalation affecting commercial relationships

• Allied supply chain coordination creating alternative options

The Asia Society Policy Institute warns that faster vulnerability reduction by either side could erode the mutual disruption balance currently stabilising relations between the world's two largest economies.

The next major ASX story will hit our subscribers first

Optimal Strategic Pathways for Sustainable Competition

Both China and the United States face strategic choices that will determine whether rare earth competition remains manageable or escalates into broader economic decoupling. Optimal approaches require balancing immediate leverage with long-term industrial competitiveness.

China's Sustainable Leverage Strategy

China's optimal approach involves maintaining credible but predictable export controls that preserve strategic influence without triggering complete supply chain exodus:

• Predictable licensing frameworks that enable commercial planning

• Stable commercial terms for non-sensitive applications

• Graduated restrictions targeting truly sensitive end-uses

• Technological upgrading to maintain processing advantages

This strategy requires resisting maximalist policies that could accelerate Western diversification efforts while preserving leverage for genuine security concerns.

U.S. Systems-Level Industrial Policy

The United States should treat rare earths as a comprehensive industrial challenge rather than simply a mining problem:

• Integrated supply chain development from ore to finished magnets

• Long-term procurement commitments providing investment certainty

• Allied coordination for shared capacity and risk reduction

• Defence qualification programmes ensuring performance standards

Success requires moving beyond announcement-focused mining projects toward operational processing and manufacturing capabilities with proven quality standards.

Investment and Procurement Integration

Effective vulnerability reduction requires pairing capital investment with demand certainty through defence procurement and civilian applications. The Department of Defence's 10-year buying agreements for domestic rare earth production provide the revenue visibility needed for private investment in processing infrastructure.

Allied stockpiling programmes can create additional demand buffers while building strategic reserves for crisis scenarios. Combined stockpiles across G7 nations could total several years of consumption, providing leverage during supply disruptions.

Global Market Adaptation and Alternative Development

International markets are developing alternative supply chains and risk management strategies in response to U.S.-China rare earth supply chain competition. These adaptations reflect broader trends toward supply chain diversification and strategic autonomy across critical industries, particularly affecting European critical minerals supply planning.

Regional Supply Chain Development

Australia's Lynas Corporation operates the world's largest rare earth processing facility outside China, with annual separation capacity reaching 22,000 tonnes TREO. Expansion plans target 50,000+ tonnes by 2027, supported by long-term contracts with Western manufacturers seeking supply diversification.

Malaysia's processing facilities provide separation services for Australian rare earth concentrates, creating integrated supply chains that bypass Chinese processing entirely for specific applications.

Cambodia and Vietnam are developing downstream processing capabilities focused on magnet manufacturing, supported by Japanese and South Korean technology transfer agreements.

Technology Transfer and Joint Ventures

International technology sharing arrangements accelerate non-Chinese capacity development:

• Japanese magnet manufacturers licensing technology to Western facilities

• European rare earth recycling programmes reducing primary material dependence

• Canadian processing initiatives supported by U.S. defence contracts

• Indian separation facilities targeting domestic electronics manufacturing

These arrangements create multiple supply options while distributing technical knowledge beyond Chinese control.

Market Structure Evolution

Premium pricing for non-Chinese rare earth sources reflects security considerations rather than pure economic factors. Industrial customers increasingly accept 15-25% price premiums for verified supply chain transparency and reduced geopolitical risk.

Long-term contract structures provide stability for both producers and consumers, with agreements typically spanning 5-10 years and including force majeure provisions for geopolitical disruptions.

Market participants are developing sophisticated risk management frameworks that treat supply chain security as a measurable cost factor rather than an external uncertainty.

Strategic reserve programmes across allied nations create additional demand sources while building crisis response capabilities. Combined reserves could potentially cover 6-12 months of consumption across critical applications.

Performance Metrics and Success Indicators

Measuring progress in U.S.-China rare earth supply chain competition requires moving beyond announcement-focused metrics toward operational capacity and qualified supply chain integration. Success indicators must reflect actual production capabilities rather than planned projects.

Quantitative Progress Indicators

Processing Capacity Development:

- Operational separation facilities outside China by annual capacity

- Qualified production rates meeting defence and civilian specifications

- Technology transfer success measured by yield rates and purity levels

Supply Chain Integration:

- End-to-end production from ore to finished magnets within allied nations

- Qualification timelines for new suppliers across defence applications

- Cost competitiveness relative to Chinese alternatives

Market Diversification:

- Source country distribution for rare earth imports by major economies

- Contract duration and pricing trends for non-Chinese suppliers

- Strategic reserve accumulation across allied stockpiling programmes

Qualitative Strategic Assessments

Technological Independence:

- Processing expertise development in allied nations

- Innovation capacity for next-generation applications

- Intellectual property control and technology sharing agreements

Geopolitical Stability:

- Predictability of Chinese export licensing decisions

- Allied coordination effectiveness for supply chain diversification

- Crisis response capabilities during supply disruptions

Long-Term Competitive Dynamics

Success ultimately depends on achieving sustainable competitive structures rather than temporary supply chain adjustments. China's long-term advantage relies on maintaining processing expertise and cost efficiency, while U.S. success requires building allied capacity with comparable performance standards.

Innovation incentives will determine whether competition drives technological advancement or simply creates parallel supply chains with higher costs. The clean energy transition provides demand growth that could support multiple efficient producers rather than zero-sum competition.

Regulatory frameworks that balance security concerns with commercial efficiency will prove critical for long-term market stability and continued investment in rare earth capacity development.

Strategic Competition Outlook and Market Evolution

The trajectory of U.S.-China rare earth supply chain competition will depend heavily on policy choices made during 2025-2026, as both sides race to reduce vulnerabilities while maintaining industrial competitiveness. Current trends suggest a prolonged period of managed competition rather than complete decoupling.

China's strategic challenge involves preserving rare earth leverage without triggering permanent market share loss to alternative suppliers. Excessive restrictions could accelerate the very diversification efforts that Beijing seeks to prevent.

U.S. strategic success requires moving beyond mining-focused solutions toward integrated supply chain development with proven operational capabilities. Announcement-focused policies must give way to sustained investment and procurement commitments.

Allied coordination provides the most promising pathway for reducing Chinese leverage while maintaining cost competitiveness. Distributed production across multiple countries could create resilient supply chains without sacrificing economic efficiency.

Market adaptation continues as industrial customers develop sophisticated risk management approaches that treat supply chain security as a quantifiable business factor. Premium pricing for diversified sources reflects genuine economic value rather than temporary political preferences.

The challenges facing global supply chains illustrate how critical mineral dependencies affect national security calculations across multiple industries. Furthermore, research on escaping China's rare earth dominance demonstrates the technical and economic challenges facing alternative supply development efforts.

The outcome of this strategic competition will influence not only rare earth markets but broader patterns of economic interdependence between major powers. Success in managing this competition constructively could provide models for addressing similar challenges across other critical industries and supply chains.

Disclaimer: This analysis contains forward-looking assessments based on current policy trends and market conditions. Actual developments may vary significantly due to policy changes, technological breakthroughs, or geopolitical events not anticipated at the time of publication. Investment and supply chain decisions should be based on comprehensive due diligence and professional advice appropriate to specific circumstances.

Looking to Invest in the Next Critical Minerals Opportunity?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, instantly transforming complex critical minerals data into actionable investment insights. With rare earth supply chains reshaping global markets, explore how major discoveries can generate substantial returns and start your 30-day free trial today to position yourself ahead of evolving market opportunities.