June 27, 2026

When Inventory Signals Diverge From Price Reality: Understanding What EIA Data Actually Tells Us

Global oil markets are built on a paradox: the commodity most central to industrial civilization is also one of the most difficult to price with precision. US crude oil and gasoline inventories EIA data sits at the heart of that challenge. Traders, analysts, and portfolio managers dedicate enormous attention to weekly petroleum stock figures not because they tell a complete story, but because they offer one of the few objective, high-frequency snapshots of supply and demand equilibrium in real time.

The mid-2026 EIA Weekly Petroleum Status Report cycle has delivered some of the most striking inventory movements seen in recent years, with consecutive draws of historic magnitude reshaping how analysts view the balance between U.S. domestic production capacity and consumption. However, inventory numbers never exist in isolation. The data must be layered against seasonal benchmarks, refinery throughput rates, product-specific demand signals, and a geopolitical backdrop that has rarely been more complex.

Understanding these crude oil market dynamics is essential for separating informed market participants from those reacting purely to headlines.

When big ASX news breaks, our subscribers know first

What the EIA Weekly Petroleum Report Actually Measures

The U.S. Energy Information Administration publishes its Weekly Petroleum Status Report every Wednesday at 10:30 a.m. Eastern Time. The report quantifies changes in commercial crude oil stockpiles, refined product inventories including gasoline and distillates, refinery utilisation rates, and a proxy for domestic demand known as total products supplied. Each figure is expressed in millions of barrels and reflects activity for the week ending the prior Friday.

Three distinct categories of petroleum storage are tracked in U.S. data, and conflating them is a common source of analytical error:

- Commercial crude stockpiles are privately held inventories owned by oil companies, refiners, and traders. This is the headline figure that moves markets.

- The Strategic Petroleum Reserve (SPR) is a government-controlled emergency reserve stored in underground salt caverns along the Gulf Coast, managed separately from commercial stocks.

- Total petroleum inventories aggregate both commercial and SPR volumes, providing the broadest possible view of available supply.

The EIA release is preceded each Tuesday by a private-sector estimate from the American Petroleum Institute (API). Because the API surveys its member companies rather than conducting a comprehensive government census, its figures are considered directionally useful but carry more uncertainty than the EIA's verified release. When the two reports align closely, market confidence in the directional signal strengthens considerably.

"The EIA crude oil inventory figure functions as the definitive benchmark for U.S. petroleum supply conditions. A divergence between the API estimate and the EIA release of even a few hundred thousand barrels can trigger meaningful intraday price swings across WTI and Brent futures contracts."

How U.S. Crude Oil Inventories Trended in Mid-2026

Commercial Stockpile Data and Five-Year Benchmark Comparisons

The consecutive drawdown pattern that emerged across late May and mid-June 2026 was statistically unusual by any historical standard. Back-to-back weekly reductions exceeding 8 million barrels each are rare events that signal a meaningful imbalance between supply inputs and consumption outputs in the U.S. petroleum system.

| Reporting Week | Weekly Change (Crude) | Total Commercial Stockpile | Deviation from 5-Year Average |

|---|---|---|---|

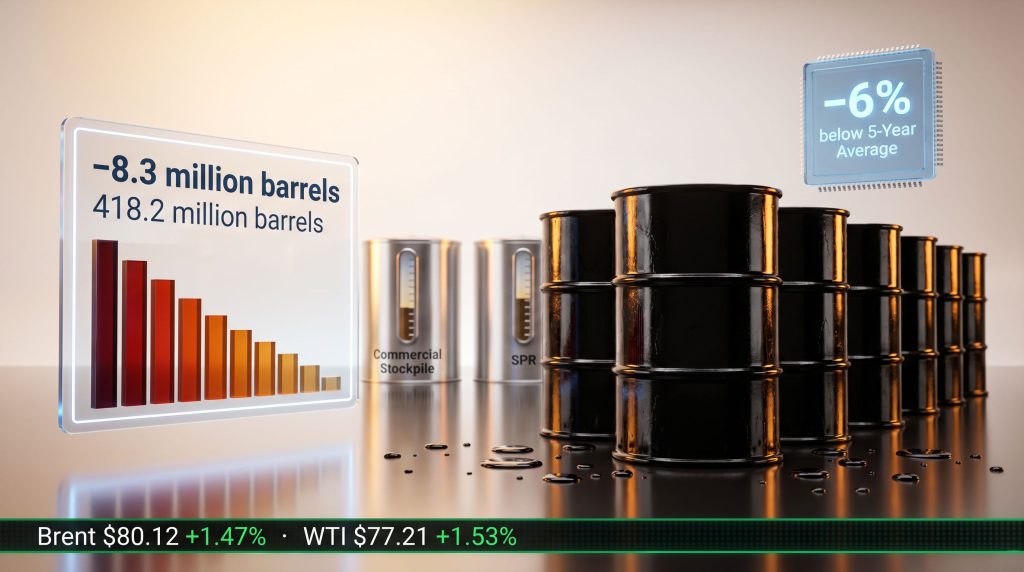

| Week ending May 29, 2026 | -8.0 million barrels | 433.7 million barrels | -3% below average |

| Week ending June 12, 2026 | -8.3 million barrels | 418.2 million barrels | -6% below average |

Furthermore, what makes these figures analytically significant extends beyond the single-week magnitude. Across a nine-week window, commercial crude storage declined by approximately 52 million barrels, a cumulative depletion rate that compresses the buffer available to absorb future supply disruptions. Each successive draw that pushes stocks further below the five-year seasonal average amplifies the bullish signal embedded in the data.

The U.S. crude oil inventories analysis during this period consequently highlights just how rapidly supply conditions can shift within a single quarter.

The Five-Year Average as a Market Anchor

Petroleum analysts rely on the five-year seasonal average as a reference point for assessing whether inventories are in a state of surplus, balance, or deficit relative to historical norms. The mechanics are straightforward: by comparing current stock levels to the average observed during the same calendar week across the prior five years, analysts can strip out seasonal fluctuations and identify genuine supply tightness.

A 6% deficit below the five-year average in commercial crude stockpiles is a meaningful tightness signal. More acute, however, is the situation across distillate products, where inventories sat 13% below the five-year seasonal average for the same period. That gap represents a more severe form of structural undercutting across the petroleum product spectrum.

What Gasoline and Distillate Inventory Movements Reveal About U.S. Demand

Motor Gasoline Inventory Dynamics: A Mixed Signal

Gasoline inventory movements during the period reflected the inherent volatility of consumer fuel demand heading into the U.S. summer driving season. Weekly swings between builds and draws are common during this transition window, making single-period gasoline figures less reliable as standalone demand indicators.

| Reporting Week | Gasoline Inventory Change | Daily Production Rate | Demand Signal |

|---|---|---|---|

| Week ending May 29, 2026 | +3.4 million barrels | 9.4 million barrels/day | Demand softening |

| Week ending June 12, 2026 | -0.9 million barrels | 10.1 million barrels/day | Demand firming |

| Week ending June 19, 2026 (est.) | +2.064 million barrels | – | Demand cooling again |

The rise in gasoline production to 10.1 million barrels per day during the June 12 reporting week is itself a noteworthy data point. Elevated production rates at that level imply high refinery utilisation, which speaks to the health of refinery throughput capacity. However, when production increases but inventory still draws down, it confirms that consumption absorbed the additional supply. The four-week rolling average for gasoline demand of 8.9 million barrels per day provides a more stable read on underlying consumption trends than any individual weekly figure.

Middle Distillate Inventories: The Overlooked Tightness Signal

While gasoline naturally captures public attention given its consumer visibility, the distillate market often tells a more economically significant story. Distillates encompass diesel fuel, heating oil, and jet fuel, all of which power freight transportation, agricultural machinery, aviation, and industrial operations.

"While headline attention gravitates toward crude oil draws, the distillate market's persistent 13% deficit below seasonal norms represents a structural tightness that could amplify price pressures in transportation and industrial sectors if production rates do not recover meaningfully."

Despite a 1.0 million barrel increase in distillate stocks during the June 12 reporting week, the cumulative deficit remains severe. Daily distillate production declining to 5.2 million barrels compounds the structural tightness by constraining the rate at which the deficit can be rebuilt. For traders focused on crack spreads and refiner economics, this dynamic warrants closer attention than the crude headline number alone.

How Total U.S. Petroleum Demand Compares Year-Over-Year

Total Products Supplied: The Broadest Demand Proxy

The single most comprehensive demand indicator within the EIA weekly data set is total products supplied, a figure that aggregates consumption-equivalent volumes across all petroleum product categories. For the four-week period ending June 12, 2026, this metric averaged 20.6 million barrels per day, representing a 3.3% increase compared to the same period one year earlier.

Breaking down the demand picture by product category reveals important structural patterns:

- Total products supplied: 20.6 million barrels per day (four-week average), up 3.3% year-over-year

- Distillate fuel demand: 3.7 million barrels per day (four-week average), up 5.5% year-over-year, the strongest growth rate across all major product categories

- Gasoline demand: 8.9 million barrels per day (four-week average), reflecting pre-July 4th seasonal consumption patterns

The distillate year-over-year growth rate of 5.5% deserves particular scrutiny. That level of demand expansion in freight and industrial fuels is broadly consistent with robust economic activity in manufacturing, logistics, and transportation. When placed against a production backdrop of declining daily output and stockpiles already running 13% below seasonal norms, the supply-demand arithmetic becomes increasingly unfavourable.

What Year-Over-Year Demand Growth Means for Inventory Trajectory

A 3.3% aggregate increase in petroleum consumption compounding against a multi-week drawdown in commercial stockpiles is not a benign combination. The directional implication is clear: if demand continues to outpace production and import volumes, the existing deficit below the five-year average will deepen rather than narrow.

In addition, the oil price volatility trends observed earlier in 2025 suggest that markets can reprice sharply when inventory deficits reach critical thresholds. Should this trajectory persist through the second half of summer, analysts have noted that stockpiles could approach multi-year lows before the traditional end-of-season inventory rebuild begins.

Why the API vs. EIA Inventory Divergence Matters to Traders

Comparing the Two Benchmark Reports

| Report | Week Ending June 12, 2026 | Crude Draw Reported |

|---|---|---|

| API (American Petroleum Institute) | June 12, 2026 | -8.33 million barrels |

| EIA (Energy Information Administration) | June 12, 2026 | -8.3 million barrels |

The near-identical alignment between the API and EIA figures for the June 12 reporting week strengthened the reliability of the directional signal. Contrast this with the May 29 reporting week, where the API estimated a draw of approximately 6.75 million barrels against the EIA's confirmed figure of 8.0 million barrels, a divergence large enough to require traders to reassess positioning after the official government data released.

Understanding why divergence occurs requires appreciating the methodological differences between the two reports. The API collects voluntary survey data from its member companies, providing a directional estimate. The EIA conducts a more comprehensive statistical survey with mandatory reporting requirements, resulting in a higher-confidence final figure. Neither is infallible, but the EIA release is generally treated as the authoritative number for market pricing purposes.

How Markets Responded to the June 12 Inventory Data

Following the June 12 EIA release, oil prices recovered from the prior session's decline. By mid-morning in New York, Brent crude was trading at $80.12 per barrel, a gain of $1.16 (+1.47%) on the day, while WTI crude reached $77.21 per barrel, up $1.16 (+1.53%). This moderate recovery reflects the general directional rule: a crude draw larger than consensus expectations is typically bullish for both WTI and Brent, while a gasoline inventory build beyond expectations can weigh on crack spreads and refiner margins.

According to recent EIA reporting on inventory movements, export volumes and shifting demand patterns continue to play a significant role in how weekly figures ultimately land relative to analyst expectations.

The next major ASX story will hit our subscribers first

What Is the Strategic Petroleum Reserve's Role When Commercial Stocks Fall?

SPR as a Buffer and Its Current Limitations

The SPR occupies a unique position in the U.S. petroleum supply framework. Unlike commercial inventories, which fluctuate continuously in response to market forces, the SPR is a policy instrument designed for deployment in genuine emergency scenarios such as major supply disruptions, natural disasters, or acute geopolitical shocks. It is not a routine balancing mechanism for commercial inventory shortfalls.

The challenge in mid-2026 is that the SPR's available buffer has been materially constrained by prior drawdowns, limiting the government's capacity to supplement commercial supply at a time when stockpiles are declining. This creates a structural vulnerability: if a geopolitical supply event materialises simultaneously with already-low commercial stocks and a depleted strategic reserve, the U.S. petroleum system has fewer layers of insulation than it has historically enjoyed.

Geopolitical Context Amplifying Inventory Concerns

The Strait of Hormuz remains one of the single most consequential chokepoints in the global petroleum supply chain. Approximately 20% of the world's traded oil transits the strait annually, according to EIA estimates. Any sustained disruption to Hormuz traffic would reduce the volume of feedstock available to global refiners, including those supplying U.S. markets through import channels.

Furthermore, OPEC's market influence on production strategy decisions interacts directly with U.S. commercial inventory dynamics. Saudi Arabia's crude pricing decisions and output quota management influence the global supply volumes available for import into the United States, affecting the rate at which domestic stockpiles draw down or rebuild. When domestic production fails to offset declining import availability, commercial inventories bear the burden.

The trade war impact on oil flows adds another layer of complexity, as tariff-related shifts in import and export patterns can distort the weekly inventory figures in ways that require careful contextual interpretation.

How to Read EIA Inventory Data: A Step-by-Step Analytical Framework

For those approaching the weekly EIA report without a structured methodology, the following framework provides a disciplined analytical pathway:

- Identify the headline crude number. Is it a build or a draw? How does the magnitude compare to consensus analyst expectations? A draw that exceeds expectations carries more bullish weight than one that falls short.

- Benchmark against the five-year seasonal average. A draw that pushes stocks further below the historical average intensifies the tightness signal compared to one that merely reduces an existing surplus.

- Assess gasoline and distillate movements separately. Each product category has distinct demand drivers and price implications. Refinery throughput and utilisation data contextualise the production side of the equation.

- Evaluate the four-week demand averages. Single-week demand figures contain substantial week-to-week noise. The rolling four-week average smooths seasonal volatility and surfaces underlying consumption trends more reliably.

- Cross-reference API and EIA for signal confidence. Close alignment between the two reports strengthens the reliability of the directional reading. Wide divergence warrants caution before repositioning.

- Contextualise within the macro and geopolitical environment. OPEC+ production decisions, refinery outage schedules, seasonal demand cycles, and geopolitical disruptions all modulate the ultimate price impact of any individual weekly inventory figure.

FAQ: U.S. Crude Oil and Gasoline Inventories Explained

What does the EIA crude oil inventory report measure?

The EIA Weekly Petroleum Status Report quantifies the net change in commercial crude oil stockpiles held by U.S. firms, expressed in millions of barrels, for the week ending the prior Friday.

How often is the EIA inventory report released?

The report is published every Wednesday at 10:30 a.m. Eastern Time by the U.S. Energy Information Administration.

What is considered a large weekly crude draw?

Draws exceeding 3 to 4 million barrels are generally considered significant by market participants. Draws above 8 million barrels, as seen in consecutive weeks during May and June 2026, are statistically uncommon and typically generate strong bullish price reactions.

What is the five-year average and why does it matter?

The five-year seasonal average represents the historical norm for inventory levels at a given point in the calendar year. Deviations above or below this benchmark help analysts assess whether current supply conditions are loose, balanced, or tight relative to historical precedent.

How does gasoline inventory data differ from crude inventory data?

Crude inventories reflect feedstock availability for refineries. Gasoline inventories reflect the refined product available for consumer consumption. Both are reported in the same EIA release but carry distinct price implications for different segments of the petroleum market. Monitoring both simultaneously provides a more complete picture of US crude oil and gasoline inventories EIA conditions.

What happens to oil prices when crude inventories fall more than expected?

A larger-than-expected crude draw typically signals stronger-than-anticipated demand or constrained supply, which is generally bullish for WTI and Brent crude prices. Historical crude oil stock data confirms this relationship holds consistently across multiple market cycles.

What is the Strategic Petroleum Reserve and how does it differ from commercial stocks?

The SPR is a U.S. government-controlled emergency reserve stored in underground salt caverns. Commercial stocks are privately held by oil companies, refiners, and traders. The EIA headline inventory figure refers to commercial stocks only.

Key Takeaways: What the Mid-2026 EIA Data Signals for Oil Markets

- Structural tightening underway: Back-to-back draws of more than 8 million barrels have pushed commercial crude stockpiles 6% below the five-year seasonal average, a meaningful supply tightness signal with compounding implications.

- Demand remains resilient: Total petroleum products supplied averaging 20.6 million barrels per day, up 3.3% year-over-year, confirms underlying consumption strength heading into summer.

- Distillate markets under pressure: A 13% deficit below the five-year average in distillate stocks represents the sharpest tightness signal across all petroleum product categories and carries direct implications for freight, industrial, and aviation fuel costs.

- Gasoline dynamics remain mixed: Weekly gasoline inventory oscillations between builds and draws reflect seasonal volatility rather than a clear directional trend, requiring four-week averaging for a reliable read.

- SPR buffer capacity constrained: The government reserve's reduced capacity to offset commercial drawdowns structurally elevates supply risk in a geopolitically uncertain environment.

- Price sensitivity elevated: With stockpiles running well below seasonal norms, US crude oil and gasoline inventories EIA readings indicate that crude oil prices remain more responsive to incremental demand surprises or supply disruptions than they would be in periods of inventory surplus.

This article is for informational and educational purposes only and does not constitute financial, investment, or trading advice. All statistics and figures referenced are sourced from publicly available EIA data and market reports. Past inventory trends and price relationships do not guarantee future market outcomes. Readers should conduct independent research and consult qualified financial professionals before making investment decisions.

Want to Stay Ahead of Major Resource Discoveries Driving the Next Market Move?

While oil market dynamics capture global attention, significant mineral discoveries on the ASX can deliver equally transformative investment opportunities — and Discovery Alert's proprietary Discovery IQ model ensures subscribers receive real-time alerts the moment those discoveries are announced. Explore Discovery Alert's dedicated discoveries page to see how historic finds have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the broader market.