June 14, 2026

The Quiet Architecture of Monetary Collapse

History rarely announces its turning points in advance. The most consequential monetary shifts of the twentieth century, from the Weimar Republic's inflationary spiral to the Bretton Woods collapse of 1971, unfolded gradually before arriving suddenly. Today, a convergence of structural pressures is prompting serious analysts, institutional investors, and sovereign wealth managers to revisit questions that once seemed purely academic: what does a US currency reset and gold confiscation actually look like, and could it happen again?

These are no longer fringe concerns. They are increasingly the subject of institutional positioning, legislative action at the state level, and quiet policy debate within multilateral financial bodies.

When big ASX news breaks, our subscribers know first

Why Monetary Stress Signals Are Flashing in 2025

The most reliable leading indicators of monetary distress are rarely found in official government statements. They show up in institutional behaviour, particularly in how central banks allocate reserves.

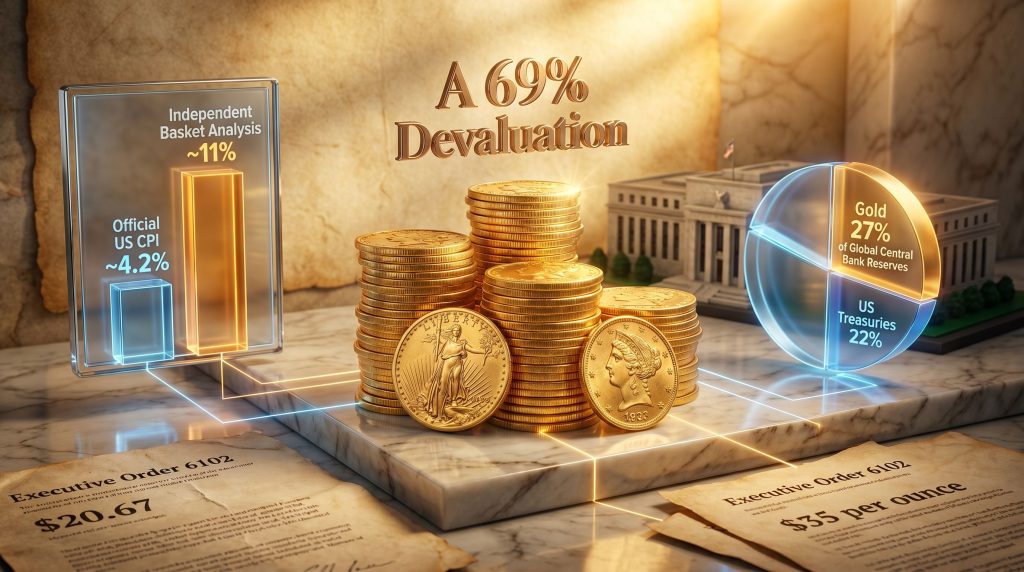

Recent IMF data confirms a striking shift in global reserve composition. Gold now constitutes 27% of global central bank reserves, having overtaken US Treasury holdings, which have declined to approximately 22% from a previous weighting of around 25%. This is not a marginal adjustment. It represents a broad institutional rotation away from the world's primary reserve instrument and toward physical metal. Furthermore, central bank gold buying at this scale only makes strategic sense if the institutions managing those reserves have material concerns about the long-term integrity of dollar-denominated assets.

Simultaneously, Bloomberg data indicates that global sovereign bond issuance in 2026 has surpassed the levels recorded during the 2020 pandemic period. The volume of new debt being taken on globally at a time of ostensible economic normalcy is, by historical standards, anomalous. Every major debt expansion in history has required either growth-driven repayment or monetary debasement to resolve. When growth is insufficient, debasement follows.

The Real Inflation Problem: What Official Numbers Miss

Official US CPI data has reported inflation at approximately 4.2%, described as the highest reading in three years, with authorities attributing much of the pressure to energy and supply disruptions. However, CPI methodology permits the substitution of cheaper goods when prices rise, excludes volatile food and energy components from core readings, and adjusts for quality improvements in ways that structurally compress the reported figure.

An independent longitudinal study tracking an identical basket of real consumer goods over a decade found that average annual inflation, measured against fixed purchasing patterns, has run closer to 11% per year. This divergence between official measurement and lived economic experience helps explain why US consumer sentiment has reached its lowest point in approximately 50 years. When people's wallets tell them one thing and official statistics tell them another, trust in the broader monetary narrative erodes.

The practical implication is stark. An investment portfolio generating an 11% annual return, widely considered an exceptional outcome, would merely maintain purchasing power under this real-world inflation framework, not build wealth.

| Inflation Measure | Reported Rate | Methodology |

|---|---|---|

| Official US CPI | ~4.2% | Substitution-adjusted, excludes food/energy core |

| Independent basket analysis | ~11% annual average | Fixed goods basket tracked over 10 years |

| Stock return needed to break even | ~11% annually | Required just to preserve purchasing power |

Further compounding the outlook, the partial closure of the Strait of Hormuz has concentrated approximately 50% of global fertiliser supply at a single geographic choke point. With reduced agricultural inputs, analysts project that food price inflation alone could add up to 20% to global food costs over the next one to two years as reduced planting cycles translate into lower crop yields. This is a supply-side shock layered on top of an already inflated monetary base, a compounding dynamic that historically precedes accelerated inflationary spirals.

Defining a Currency Reset With Historical Precision

The term currency reset is frequently used loosely in financial commentary. Used precisely, it refers to a deliberate governmental revaluation or structural overhaul of the national monetary unit, typically executed during or immediately following a period of hyperinflationary breakdown. It is categorically distinct from gradual inflation and represents a formal acknowledgement that the existing currency unit has lost functional utility either as a store of value or as a reliable medium of exchange.

Historical examples span the twentieth century across multiple continents:

- Post-WWI Germany, where the Papiermark was replaced by the Rentenmark at a ratio of one trillion to one

- Zimbabwe's 2009 currency abandonment following hyperinflation that rendered its currency functionally worthless

- Argentina's 2002 peso devaluation following the collapse of its dollar peg

- Mexico's 1993 redenomination, which replaced the old peso with the new peso at a 1,000:1 ratio

In each case, holders of physical gold and silver retained relative purchasing power through the transition. Holders of fiat currency savings faced direct wealth destruction through the conversion ratio.

The 1933 Precedent: What Actually Happened

The most directly relevant historical precedent for US audiences is the 1933 to 1934 monetary restructuring under the Roosevelt administration. Understanding this sequence precisely matters, because it is frequently mischaracterised in popular commentary.

In 1933, Executive Order 6102 required private citizens to surrender gold coins, bullion, and certificates to the Federal Reserve at the then-prevailing statutory rate of $20.67 per troy ounce. Holders received paper dollars in exchange, so it was not a zero-compensation seizure. However, the Gold Reserve Act of 1934 subsequently reset the official gold price to $35 per ounce, a 69% increase in the statutory gold value. Those who had been forced to surrender gold before this revaluation were effectively dispossessed of the upside.

The 1933 action was framed publicly as a national emergency measure to prevent gold hoarding from constraining monetary policy. Its practical effect was to transfer the benefit of gold's subsequent revaluation from private holders to the US Treasury.

The legal mechanism was the Trading with the Enemy Act of 1917, which granted the executive broad economic emergency powers. The modern equivalent, the International Emergency Economic Powers Act (IEEPA) of 1977, carries similarly expansive authority and has been interpreted broadly during declared national emergencies.

Why a Modern Reset Would Look Different

A twenty-first century US currency reset and gold confiscation scenario would operate in a fundamentally different structural context. The dollar is no longer anchored to gold, so there is no fixed conversion ratio to sever. A modern reset would more likely involve currency redenomination (such as a 10:1 conversion), sovereign debt restructuring, or the introduction of a new monetary instrument, potentially a Central Bank Digital Currency.

Critically, a US currency reset would not be contained within American borders. Because the dollar functions as the world's primary reserve currency, any formal restructuring would cascade through every nation holding dollar-denominated assets. This systemic dimension is precisely why central bank gold reserves at the sovereign level carry such analytical weight. These institutions are not buying gold for speculative reasons. They are positioning for a scenario where the instrument underpinning global trade and reserve management undergoes structural change.

Could the US Government Confiscate Gold Again?

This question requires separating legal possibility from operational probability.

Legal possibility: The IEEPA grants executive authority to regulate or prohibit financial transactions, including those involving precious metals, during a declared national emergency. Emergency powers legislation has historically been interpreted expansively during genuine crises. The legal architecture for a confiscation order exists.

Operational probability: Because the dollar is no longer on a gold standard, seizing privately held gold would not mechanically enable a currency revaluation in the way it did in 1934. The immediate operational rationale is weaker. Most mainstream monetary analysts classify a direct 1933-style confiscation as improbable under normal conditions.

| Factor | 1933 Context | 2025 Context |

|---|---|---|

| Dollar backed by gold | Yes | No |

| Confiscation mechanically enables revaluation | Yes | No direct mechanism |

| Public gold ownership prevalence | Moderate | Relatively low as a share of population |

| Digital surveillance infrastructure | None | Highly developed |

| Alternative monetary instruments | Limited | CBDCs, cryptocurrency, digital assets |

| Legal authority for emergency action | Trading with Enemy Act | IEEPA (broad scope) |

The CBDC Variable: Why the Calculus Changes

The confiscation risk calculus shifts materially when Central Bank Digital Currencies enter the analysis. CBDCs are programmable monetary instruments that allow issuing authorities to impose spending restrictions, transaction monitoring, expiry dates on holdings, and, critically, negative interest rates at the individual account level.

The IMF has publicly advocated for cashless monetary systems on the basis that they enable more precise interest rate transmission, including the capacity to implement negative rates that are structurally impossible in a cash-based economy where people can simply withdraw and hold physical currency.

The logical problem for any CBDC regime seeking comprehensive monetary control is this: if gold, silver, or cryptocurrency represent accessible exit pathways, then individuals retain the ability to opt out of the programmatic constraints. A CBDC system that cannot capture a meaningful portion of the monetary base cannot function as intended.

If a government introduces a mandatory CBDC framework and simultaneously restricts conversion into physical gold or silver, the functional effect is equivalent to confiscation, even without a formal seizure order. Regulatory elimination of exits achieves the same outcome as direct seizure.

This is not a mainstream policy prediction. It is a scenario analysis of the logical implications of full-spectrum monetary control implementation. The probability increases proportionally with the ambition of any CBDC design.

The Pre-1933 Coin Exemption: Historical Protection or Legal Illusion?

Executive Order 6102 included explicit language exempting gold coins with recognised special value to collectors of rare and unusual coins from the surrender requirement. This created a legal distinction between monetary gold, subject to the order, and numismatic gold, treated as collectible property.

Pre-1933 US gold coins fall into the numismatic category by definition, having been minted before the confiscation order. This historical carve-out is the primary legal argument cited by investors who prioritise pre-1933 coins over standard bullion products.

The reasoning extends beyond historical precedent. Dynastic wealth preservation strategies across cultures have long relied on assets that occupy legal categories adjacent to, but distinct from, pure monetary instruments. High-value collectibles, rare art, and numismatic coins have historically occupied grey zones that formal confiscation orders have tended to leave undisturbed, partly because the administrative complexity of valuation and seizure makes them operationally unattractive targets.

However, one critical caveat applies:

No legal guarantee exists that a future emergency order would replicate the 1933 exemption language. The collector carve-out is a historical precedent, not a legal certainty. Investors treating pre-1933 coin status as absolute protection are relying on a precedent, not a statute.

Numismatic coins also carry premiums above their melt value, which reduces pure gold-price leverage while potentially increasing legal defensibility. Whether that trade-off is appropriate depends entirely on an individual investor's threat assessment and time horizon.

Scenario Modelling: What a Reset Sequence Could Look Like

Phase 1: The Pre-Reset Environment

Based on historical patterns, the pre-reset period is characterised by:

- Persistent above-CPI real inflation steadily eroding household purchasing power

- Accelerating sovereign debt issuance beyond pandemic-era levels

- Central bank rotation from Treasuries into gold at institutional scale

- Declining consumer sentiment and rising financial stress indicators

- Early-stage food price inflation driven by agricultural supply disruption

Many analysts argue this description closely matches the current environment.

Phase 2: Hyperinflationary Acceleration

Inflation becomes self-reinforcing as currency holders accelerate spending to avoid holding depreciating assets. Commodity prices denominated in the domestic currency rise faster than wage growth. Savings in fixed-income instruments and cash holdings lose real value rapidly, including retirement accounts and pension funds.

Gold and silver, denominated in the inflating currency, rise sharply in nominal terms. Holders of physical metal retain relative purchasing power. The critical distinction is between nominal wealth, which appears to grow in inflating currency terms, and real wealth, which is measured in purchasing power.

Phase 3: The Reset Event

A formal currency redenomination or new monetary instrument is announced. Conversion ratios are set. Holders of physical gold can convert into the new currency at prevailing gold prices, which by this point reflect the full accumulated inflationary premium. Those without hard asset holdings face direct wealth destruction through the conversion ratio.

As one long-standing historical observation holds: throughout every hyperinflationary episode and currency reset on record, the only assets that reliably preserved wealth through the transition were physical gold and silver. Paper savings, fixed-income holdings, and cash were decimated regardless of the holder's prior wealth level.

Phase 4: Post-Reset Reconstruction

A new monetary framework is established. Gold may be formally revalued on government balance sheets, and the role of gold in the monetary system becomes a central policy question. Property rights over alternative monetary assets become a central policy battleground. The post-reset period is historically when the terms of the new monetary contract are set, often under conditions where the population has limited negotiating power.

The State-Level Resistance Dimension

An underappreciated variable in the US-specific scenario is the growing legislative movement at the state level to recognise gold and silver as legal tender. Florida's formal recognition of precious metals as legal tender, effective July 2025, represents one of several state-level actions pushing back against federal monetary monopoly.

Article I of the US Constitution explicitly identifies gold and silver as lawful tender, providing a constitutional grounding for state-level legal tender legislation that federal monetary authorities cannot easily override through ordinary legislative means.

Several states have simultaneously moved to restrict or prohibit the implementation of CBDCs within their jurisdictions. If a federal CBDC rollout were to coincide with a monetary crisis, the intersection of state legal tender laws, anti-CBDC legislation, and federalism doctrine could create genuinely complex jurisdictional conflict.

Whether state-level gold legal tender laws would provide practical protection against a federal emergency order remains constitutionally untested. However, the political mobilisation they represent is historically significant. Comparable state-versus-federal monetary conflict has precedent in the Free Silver movement of the 1890s and the various gold standard debates of the early twentieth century. In addition, the end of the gold standard in 1971 remains a pivotal reference point for understanding how quickly federal monetary policy can shift direction.

The next major ASX story will hit our subscribers first

Frequently Asked Questions

What is a US currency reset and has it happened before?

A US currency reset refers to a formal government-initiated revaluation or structural restructuring of the dollar. The closest historical precedent is the 1933 to 1934 period, when the Roosevelt administration required gold surrender under Executive Order 6102 and subsequently revalued gold from $20.67 to $35 per ounce under the Gold Reserve Act, effectively devaluing the dollar by approximately 69% in gold terms.

Could the US government legally confiscate gold today?

Broad emergency powers legislation such as the IEEPA grants the executive significant authority over financial assets during declared national emergencies. Because the dollar is no longer on a gold standard, the operational rationale for a 1933-style seizure is weaker than it was in 1934. Most analysts consider direct confiscation improbable under normal conditions, but acknowledge that a severe monetary crisis combined with a CBDC implementation agenda could alter the policy calculus materially.

What is the difference between gold confiscation and gold price revaluation?

A confiscation involves compulsory transfer of privately held gold to the government. A revaluation changes the official price at which the government values its own gold reserves without automatically affecting privately held metal. In the 1933 to 1934 sequence, the Executive Order was the confiscation mechanism and the Gold Reserve Act was the revaluation instrument. They served different functions in the same policy operation.

Why are central banks buying gold instead of US Treasuries?

IMF data confirms gold now constitutes 27% of global central bank reserves, exceeding the 22% held in US Treasuries. This institutional rotation reflects concern about US fiscal sustainability, dollar debasement risk, and the long-term reliability of Treasury instruments as reserve assets, particularly as sovereign debt issuance accelerates globally beyond pandemic-era levels. Furthermore, the Basel III gold impact on regulatory frameworks has reinforced gold's attractiveness as a reserve asset for financial institutions worldwide.

Are pre-1933 gold coins protected from confiscation?

The 1933 Executive Order exempted coins with recognised special value to collectors of rare and unusual coins. Pre-1933 US gold coins fall into this numismatic category by definition. However, this exemption was specific to that order. There is no legal guarantee that future emergency legislation would replicate the same language or classification.

What is the relationship between CBDCs and gold confiscation risk?

CBDCs are designed to give monetary authorities comprehensive control over currency circulation, including the capacity to impose negative interest rates and restrict certain transactions. If gold and silver represent viable exit pathways from a CBDC system, the policy logic of full monetary control implies that those exits would need to be restricted or eliminated, consequently achieving a functional confiscation outcome through regulatory means rather than direct seizure.

Key Takeaways for Investors and Informed Citizens

The following points represent the analytical core of this framework, each grounded in historical precedent, institutional data, or documented policy logic:

- Real inflation is structurally understated by official metrics. Independent fixed-basket analysis suggests average annual consumer inflation closer to 11% over the past decade, not the officially reported figures

- Central bank reserve composition is the most credible institutional signal available. The rotation from US Treasuries to gold at the sovereign level reflects sophisticated risk assessment, not speculative sentiment

- A US currency reset and gold confiscation scenario would be globally systemic in a way that no previous national reset has been, given the dollar's role as the world's primary reserve currency

- Direct gold confiscation is improbable but not impossible. The legal architecture exists, historical precedent exists, and the policy logic becomes coherent within a CBDC transition scenario

- Pre-1933 numismatic coins carry a historical legal distinction based on the 1933 exemption language, but this should be understood as a risk-reduction approach grounded in precedent, not guaranteed legal protection

- State-level gold legal tender legislation represents an emerging constitutional counterweight to federal monetary control that could gain practical significance during a crisis

This article is for informational and educational purposes only. It does not constitute financial, legal, or investment advice. Forward-looking scenarios and risk assessments involve uncertainty and speculation. Readers should conduct independent research and consult qualified professional advisers before making any financial decisions.

Want to Know When the Next Major Gold Discovery Hits the ASX?

While understanding the macro case for gold is essential, acting on it requires knowing precisely when significant discoveries are made — Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on high-potential mineral discoveries so investors can position themselves ahead of the broader market, just as early investors did with historic finds like De Grey Mining and WA1 Resources. Explore Discovery Alert's discoveries page to see the kind of returns major mineral discoveries have historically generated, and begin your 14-day free trial today to secure a genuine market-leading advantage.