June 29, 2026

The Hidden Architecture of Western Mineral Dependency

Long before policymakers began describing lithium and cobalt as matters of national security, the global mining industry had quietly reorganised itself around a single, dominant processing ecosystem. Decades of underinvestment in Western refining infrastructure, combined with China's deliberate and sustained expansion into mineral processing, created a structural asymmetry that now sits at the centre of some of the most consequential economic negotiations of the 2020s.

The April 2026 U.S. EU critical minerals partnership is not a reaction to a sudden crisis. It is the formal acknowledgment of a vulnerability that has been building for a generation. Understanding why that vulnerability matters, and what the new transatlantic framework can realistically achieve, requires looking beyond the diplomatic ceremony in Washington and examining the industrial, geological, and geopolitical forces shaping the global minerals landscape.

When big ASX news breaks, our subscribers know first

What Actually Makes a Mineral "Critical"?

The word "critical" carries specific technical weight in both U.S. and EU policy frameworks, and it is worth unpacking before examining the partnership itself. A mineral earns critical classification not simply because it is rare or valuable, but because it meets two simultaneous conditions: it is essential to high-priority industrial or defence applications, and its supply is concentrated in ways that create meaningful disruption risk.

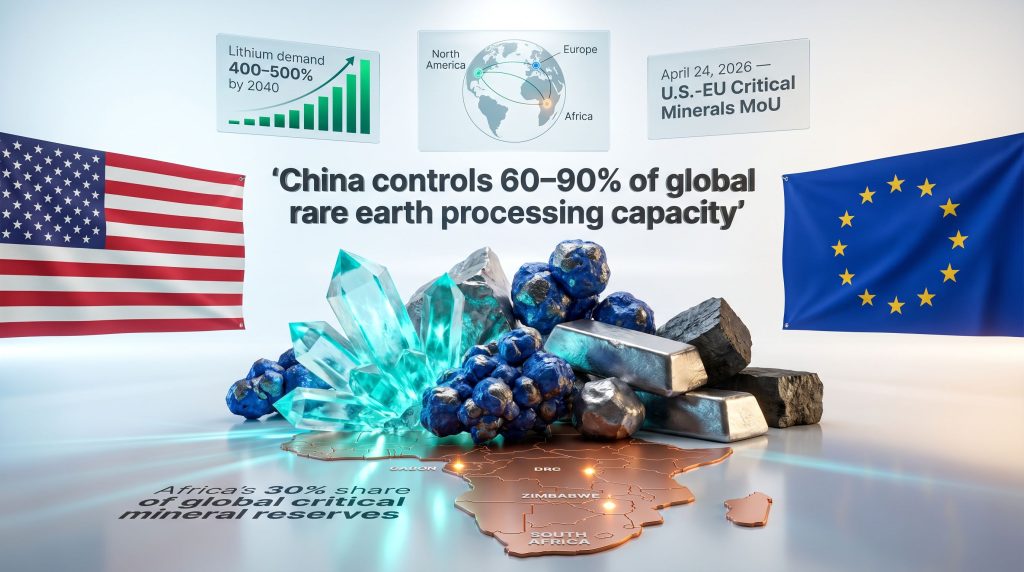

Under this framework, minerals such as lithium, cobalt, nickel, manganese, graphite, and rare earth elements occupy the top tier of strategic concern. The EU's Critical Raw Materials Act, adopted in 2023, formally identifies 34 strategic raw materials and sets ambitious internal targets: at least 10% of annual EU consumption to be met through domestic production, and 40% of strategic mineral processing to be conducted within the bloc by 2030. Furthermore, the critical raw materials transition agenda has given these targets substantial political weight across member states.

The U.S. framework, shaped significantly by the Inflation Reduction Act (IRA) and preceding Department of Energy policy, operates similarly but with a stronger emphasis on subsidy-linked incentives to reshape private sector investment decisions. The critical insight here is that both frameworks distinguish sharply between raw extraction and downstream processing capacity, and it is the processing gap, not the mining gap, that represents the deepest structural vulnerability for Western supply chains.

Why Processing Capacity Is the Real Battleground

A nation can host significant mineral deposits while remaining strategically dependent if it cannot process those minerals into battery-grade or industrial-grade materials. This distinction is frequently underappreciated outside specialist circles. Mining a lithium-bearing ore body is a fundamentally different industrial capability from converting that ore into battery-grade lithium hydroxide, which requires sophisticated hydrometallurgical facilities, precise chemistry management, and substantial capital investment.

China's strategic advantage lies overwhelmingly in this processing layer rather than purely in upstream mining. China accounts for an estimated 60 to 90% of global rare earth element processing capacity, a concentration that took decades to construct through sustained state-backed industrial policy. Moreover, China's rare earth export restrictions have demonstrated precisely how that dominance can be weaponised. This is not a gap that can be closed through diplomacy alone, as mineral processing facilities require years to permit, construct, commission, and optimise.

The April 2026 MoU: What Was Actually Signed

On April 24, 2026, U.S. Secretary of State Marco Rubio and EU Trade Commissioner Maroš Šefčovič convened in Washington, D.C., to sign a Memorandum of Understanding formalising transatlantic cooperation on critical minerals. The event represented the most substantive formal step in U.S.-EU critical minerals partnership negotiations to date, though its immediate operational significance should be assessed carefully.

Secretary Rubio publicly stated that the agreement would lead to concrete actions, and emphasised that the combined purchasing power and economic productivity of the United States and European Union constituted a significant global force. Critically, Rubio stressed that both sides must work to ensure access to raw materials is not subject to monopoly or excessive concentration in any single country's hands — a formulation that, while not naming China directly, is unmistakably directed at Beijing's current market position.

The following table illustrates the distinction between what the MoU formally establishes and what remains under negotiation:

| Dimension | MoU Provisions | What Remains Pending |

|---|---|---|

| Supply chain coordination | Joint investment frameworks | Binding procurement obligations |

| Trade facilitation | EU mineral access to IRA-linked U.S. subsidies | Full Critical Minerals Agreement (CMA) |

| Environmental standards | Alignment on sustainable sourcing criteria | Harmonised certification systems |

| Stockpiling | Exploratory joint reserve mechanisms | Operational stockpile agreements |

| Technical standards | Coordination on processing benchmarks | Unified regulatory frameworks |

Importantly, no timeline was announced for concluding a binding Critical Minerals Agreement, and details of the specific discussions were not publicly disclosed. Bloomberg had reported in early April 2026 that the deal was imminent and expected to encompass investment coordination mechanisms and joint project development, but the precise architecture remains to be defined. For further context on the EU and US partnership announcement, reporting from Euronews outlines the strategic motivations driving both parties.

Why Choose an MoU Over a Binding Treaty?

The selection of a non-binding memorandum as the diplomatic instrument reflects practical realities as much as strategic intent. Binding treaties require legislative ratification processes on both sides of the Atlantic, introducing significant delay and political risk. Memoranda of Understanding allow both parties to signal strategic alignment and establish working frameworks without triggering those processes.

This approach mirrors similar instruments the U.S. has deployed with Japan, South Korea, Mexico, and Chile as part of a sequenced bilateral strategy to build a network of mineral-secure allied supply chains. The EU's inclusion within this architecture is significant, given that the EU and U.S. together constitute the world's largest bilateral trade and investment relationship.

The "Friend-Shoring" Architecture and Where the EU Fits

The concept of "friend-shoring" — reorganising supply chains to run through politically allied nations rather than geopolitical competitors — has become the organising principle of U.S. minerals diplomacy across multiple administrations. The IRA's domestic content requirements and free trade agreement eligibility criteria are the primary commercial mechanisms driving this reorganisation.

For European mining and processing companies, the critical commercial question raised by the MoU is whether EU-sourced minerals will qualify for IRA subsidy eligibility. The EU exported approximately €8.3 billion in relevant materials to the United States, establishing a substantial existing trade relationship. However, the precise qualifying conditions for IRA subsidy access will only be determined through a subsequent binding Critical Minerals Agreement, leaving European industry in a state of commercial uncertainty in the near term.

Europe's critical minerals supply chain provides an important negotiating foundation here. The Critical Raw Materials Act's domestic production and processing targets give Brussels a clear mandate and measurable benchmarks, reducing the internal political complexity of the EU's negotiating position compared to earlier attempts at transatlantic coordination.

A History of Near Misses: Why the 2023 Effort Failed

This is not the first time Washington and Brussels have attempted to formalise mineral cooperation. Discussions were initiated in 2023 following joint statements between the Biden administration and the European Commission, progressing through the EU-U.S. Trade and Technology Council framework. Those negotiations ultimately did not produce a formal agreement, stalling over several structural disagreements:

- Divergent positions on IRA subsidy eligibility criteria for EU companies

- Differences in environmental and labour standard benchmarks

- Disagreements on the scope of reciprocal market access commitments

- Political complexity created by the IRA's implicit preference for U.S. domestic industry

Between 2023 and 2026, two developments materially shifted the strategic calculus. First, China escalated its use of export controls on critical minerals, including restrictions on gallium, germanium, and graphite, demonstrating in concrete terms its willingness to weaponise mineral supply chains in trade disputes. Second, the EU completed its Critical Raw Materials Act legislative framework, giving Brussels a clearer and more unified domestic policy baseline from which to negotiate.

China's Processing Dominance: The Structural Problem Neither Side Can Ignore

The convergence of energy transition demand growth and geopolitical supply concentration creates a compounding risk that neither the U.S. nor EU can address unilaterally, making transatlantic coordination structurally rational rather than merely politically convenient.

Beijing has spent decades constructing a vertically integrated position in the global critical minerals ecosystem. This spans upstream mining investments, particularly in cobalt-rich jurisdictions such as the Democratic Republic of Congo, through to downstream processing and materials manufacturing. This position did not emerge by accident. It reflects deliberate industrial policy choices, tolerance for processing-related environmental costs that Western regulators would not countenance, and sustained state financing of infrastructure in resource-holding nations.

The strategic exposure this creates for Western economies is compounded by the demand trajectory of the energy transition. Global lithium demand is projected by the International Energy Agency to increase by 400% or more through 2040 relative to 2020 levels. Consequently, DRC cobalt supply risks have moved to the centre of Western supply chain planning, given that the DRC supplies an estimated 70% of global cobalt mine output, much of which flows through Chinese-controlled processing channels.

Furthermore, critical minerals and energy security concerns have become increasingly intertwined as China's demonstrated willingness to deploy mineral export restrictions as a trade lever means that Western supply chain exposure is not merely theoretical. It has been tested, and the vulnerabilities have been exposed in real time.

Africa's Strategic Position: 30% of Global Reserves, 100% Contested

For any realistic assessment of where Western mineral supply chain diversification can actually be achieved at scale, Africa is the unavoidable variable. The continent holds an estimated 30% of global critical mineral reserves, encompassing cobalt in the DRC, lithium in Zimbabwe and the DRC, manganese in South Africa and Gabon, and rare earth deposits distributed across multiple jurisdictions.

Both the U.S. and EU have independently developed economic engagement mechanisms to expand their presence in African mining sectors. The April 2026 MoU creates potential for these previously separate approaches to become coordinated, though the transition from parallel to joint strategy involves significant institutional complexity.

The following table summarises the key Western engagement frameworks targeting African mineral sectors:

| Initiative | Led By | Key African Focus Areas | Primary Mechanism |

|---|---|---|---|

| Lobito Corridor | U.S. + EU + Partners | DRC, Zambia, Angola | Infrastructure and rail investment |

| Global Gateway | EU | Multiple African nations | Development finance for mining infrastructure |

| Partnership for Global Infrastructure and Investment (PGII) | U.S. | Sub-Saharan Africa | Private sector mobilisation |

| Mineral Security Partnership (MSP) | U.S. + Allies incl. EU | Africa-wide | Investment coordination and due diligence |

The Sovereignty Dimension: Africa's Conditions Are Changing

A dimension of the African mining landscape that receives insufficient attention in Western policy discussions is the rapidly evolving position of African governments themselves. The era of raw ore exports with minimal domestic value addition is facing increasing political and legislative resistance across the continent. Zimbabwe, Namibia, and other jurisdictions have introduced or are actively considering export restrictions on unprocessed minerals, specifically to force downstream processing investment within their borders.

The African Union's Agenda 2063 and the Africa Mining Vision both explicitly prioritise domestic beneficiation as a condition for sustainable mineral development. These are not simply aspirational statements. They represent a structural shift in the terms on which African governments are willing to engage with foreign mining investors, whether Western or Chinese.

For the U.S. EU critical minerals partnership, this creates a specific strategic requirement: offers made to African mineral-holding nations must include credible processing investment, technology transfer, and trade access commitments — not simply capital for extraction. China's first-mover advantage in African mineral investment spans decades of infrastructure financing, offtake agreements, and processing partnerships. Reversing or competing with that embedded position through diplomacy and development finance alone is an enormously complex undertaking. For a deeper examination of G7 trade talks and mineral strategy, Mining.com provides useful analysis of where allied tensions persist even within cooperative frameworks.

The next major ASX story will hit our subscribers first

Implementation Pathway: From MoU to Market Reality

The gap between diplomatic intent and industrial transformation is where critical minerals partnerships have historically underdelivered. The following elements will determine whether the April 2026 MoU generates meaningful supply chain change or becomes another framework that produces limited operational outcomes:

-

Speed of binding agreement negotiations — A full Critical Minerals Agreement must define precise IRA subsidy eligibility conditions for EU-sourced materials. The longer this remains unresolved, the greater the commercial uncertainty facing European mining and processing companies.

-

Joint investment coordination — Meaningful co-financing arrangements between the U.S. Development Finance Corporation and the EU's European Fund for Sustainable Development (EFSD+) require shared due diligence standards and aligned project pipelines.

-

Sustainability standard harmonisation — Both parties have committed to high environmental protection and labour rights standards as conditions for qualifying supply chains. Joint standard-setting reduces the risk of regulatory arbitrage but requires significant technical alignment work.

-

African partnership terms — The credibility of the entire architecture depends on whether resource-holding nations, particularly in Africa, find Western partnership terms genuinely competitive with available Chinese alternatives.

-

Circular economy integration — Battery recycling and material recovery frameworks are incorporated as long-term supply augmentation strategies, but their commercial scale remains years away.

Critical Risks: What Could Undermine the Partnership

The MoU is best understood not as a solution to Western supply chain vulnerability, but as the formalisation of a shared diagnosis and the beginning of a structural response that will play out across African mining sectors, allied industrial policy, and global commodity markets over the next decade.

Several structural risks deserve clear-eyed assessment:

-

Non-binding instruments have a weak track record — The history of transatlantic economic diplomacy includes numerous frameworks that generated extensive process but limited industrial outcomes. The 2023 precedent illustrates this risk concretely.

-

Internal EU tensions — EU member states have divergent exposures to critical mineral supply disruptions. Germany's automotive sector dependency on battery materials differs substantially from southern European industrial profiles, creating internal negotiating complexity.

-

IRA competitive tensions — The IRA's domestic content requirements structurally favour U.S.-based supply chains, creating friction with EU industrial interests even within an ostensibly cooperative framework.

-

Political cycle misalignment — Industrial supply chain transformation operates on decade-long timescales. Political administrations and diplomatic priorities shift every two to four years, creating persistent risk of framework discontinuity.

-

Geopolitical volatility in resource regions — The DRC, which holds critical cobalt and lithium reserves, operates in a politically complex environment where supply security assumptions can be rapidly disrupted.

Frequently Asked Questions

What minerals are covered by the U.S.-EU critical minerals MoU?

The agreement encompasses minerals classified as critical by both U.S. and EU frameworks, including lithium, cobalt, nickel, manganese, graphite, and rare earth elements — all of which are essential inputs for electric vehicle batteries, renewable energy infrastructure, and advanced defence systems.

Is the April 2026 MoU legally binding?

No. The instrument is a non-binding memorandum of understanding that establishes intent and framework for future cooperation. A binding Critical Minerals Agreement remains under negotiation with no publicly announced timeline.

How does the MoU affect EU companies seeking IRA subsidy access?

The MoU creates a pathway toward subsidy eligibility for EU-sourced minerals under the U.S. Inflation Reduction Act, but the precise qualifying conditions will only be determined through a subsequent binding agreement. European mining and processing companies remain in a state of commercial uncertainty until those conditions are defined.

What role does Africa play in the partnership's long-term success?

Africa holds an estimated 30% of global critical mineral reserves and is a central strategic arena for both U.S. and EU mineral engagement. The partnership's long-term viability depends substantially on whether Western investment terms offered to African nations are credible alternatives to established Chinese engagement frameworks, particularly on the question of domestic processing and value-added industrialisation.

Why did the 2023 U.S.-EU mineral cooperation discussions fail?

The 2023 effort stalled over divergent positions on IRA subsidy eligibility criteria, environmental and labour standard benchmarks, and the scope of reciprocal market access. The acceleration of Chinese export controls on critical minerals between 2023 and 2026, combined with the EU's completion of its Critical Raw Materials Act legislative framework, provided the strategic and institutional conditions for the 2026 U.S. EU critical minerals partnership MoU to proceed.

Want To Position Yourself Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — turning complex mineral data into actionable investment insights the moment they hit the market. Explore historic discoveries and the substantial returns they generated, then begin your 14-day free trial at Discovery Alert to ensure you're positioned ahead of the broader market when the next major find is announced.