July 12, 2026

The Quiet Transformation Reshaping How Steel Gets Made

Across the United States, a structural revolution in steel production has been unfolding over several decades, one measured not in dramatic announcements but in the steady rise of electric arc furnace capacity and the corresponding elevation of ferrous scrap from industrial byproduct to strategically critical raw material. Understanding this shift is essential context for interpreting what US ferrous scrap prices in June 2026 are actually telling the market, because the numbers themselves only tell part of the story.

The other part involves sentiment, grade differentiation, and the psychology of a market caught between modestly constructive fundamentals and persistent macro uncertainty. June 2026 represents precisely the kind of inflection point where these forces collide. Furthermore, the global crude steel outlook for 2025 and beyond provides important context for understanding how these domestic scrap dynamics connect to broader international steel trends.

When big ASX news breaks, our subscribers know first

What US Ferrous Scrap Prices in June 2026 Actually Look Like

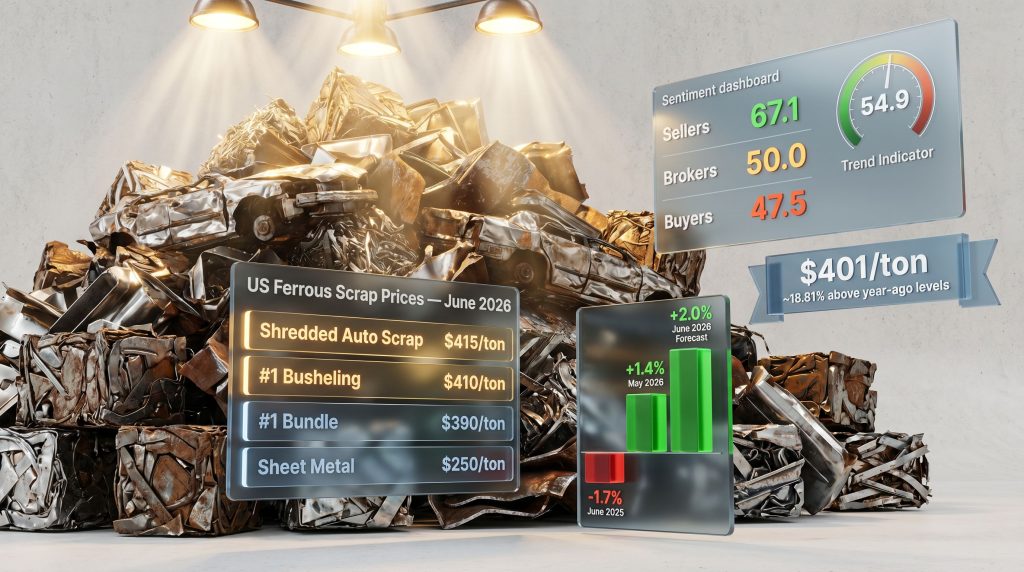

The current pricing landscape spans a wide spectrum depending on grade, with the most striking feature being the sheer distance between the strongest and weakest performing categories. The benchmark scrap steel index was trading at approximately $401 per ton as of late May 2026, according to Fastmarkets' US Scrap Trends Outlook for June 2025. That figure sits roughly 5.54% below where it was thirty days prior, yet remains elevated by approximately 18.81% compared to year-ago levels, a combination that captures the market's dual nature: short-term softness layered over a longer-term structural improvement.

June 2026 Ferrous Scrap Prices by Grade

The grade-specific breakdown paints a more granular picture of where strength is concentrated and where headwinds are most pronounced:

| Scrap Grade | June 2026 Price (USD/ton) | Month-on-Month Trend |

|---|---|---|

| Shredded Auto Scrap | $415 | Firm |

| #1 Busheling | $410 | Stable to Firm |

| #1 Bundle | $390 | Neutral |

| #1 HMS | $365 | Soft |

| Structural Steel | $365 | Soft |

| HMS 80/20 | $285 | Declining |

| Sheet Metal | $250 | Weakest Grade |

The $165 per ton spread between shredded auto scrap and sheet metal is one of the most telling features of the current market. That gap reflects not just differences in metallurgical cleanliness but a broader structural realignment in how domestic steel mills are sourcing their input material. As EAF steelmaking continues to account for a growing share of total US steel output, the premium on high-purity, low-residual scrap grades has become an entrenched feature of the pricing landscape rather than a cyclical anomaly.

Year-on-Year Sentiment Shift: June 2025 vs. June 2026

The contrast between where the market stood twelve months ago and where it sits today is instructive. In June 2025, the prevailing sentiment was decisively bearish, with the market forecasting an average monthly price decline of -1.7%. By the time June 2026 arrived, that same forward-looking indicator had swung to a forecasted average monthly increase of +2.0%, according to the Fastmarkets survey methodology. That 3.7 percentage point reversal in sentiment is not insignificant given the relatively compressed price movements typical of monthly scrap trading cycles.

The year-over-year sentiment reversal from -1.7% to +2.0% represents a meaningful psychological reset, suggesting market participants have reassessed fundamental conditions rather than simply extrapolating recent price trends.

How Market Participants Are Positioned Heading Into June Trades

Understanding the Trend Indicator Reading of 54.9

The Fastmarkets Trend Indicator, which aggregates directional expectations from buyers, sellers, and brokers into a single composite reading, posted 54.9 ahead of June trade. A reading above 50 indicates net bullish sentiment, while readings approaching or exceeding 65 have historically been associated with more forceful upward price moves. At 54.9, the market is leaning constructive but carrying significant hedges. This is the quantitative equivalent of a market that believes prices will rise but is not prepared to bet aggressively on that outcome.

The forecast model built on this reading outputs an average month-on-month price increase of +2.0%, following a +1.4% gain in May 2026, marking two consecutive months of positive momentum in a market that spent much of 2025 oscillating around flat or negative monthly changes.

The Buyer-Seller-Broker Divide

Perhaps the most strategically significant data point in the June 2026 outlook is the pronounced divergence in sentiment across different market participant categories:

| Market Participant | Trend Indicator Reading | Market Interpretation |

|---|---|---|

| Sellers | 67.1 | Strongly Bullish |

| Brokers | 50.0 | Perfectly Neutral |

| Buyers | 47.5 | Mildly Bearish |

This ~19.6-point spread between seller optimism and buyer caution creates a negotiating environment that is likely to be contentious through the June trading cycle. Sellers at 67.1 are positioned well above the neutral threshold and appear confident that market fundamentals support price gains. Buyers at 47.5 are sitting fractionally below neutral, signaling resistance to conceding on price without clearer evidence that demand conditions justify higher valuations.

Brokers, occupying the perfectly neutral midpoint at 50.0, effectively reflect genuine market balance. Their reading suggests they see merit in both the seller and buyer arguments, which historically tends to resolve in modest, below-expectation price outcomes when wide participant divergences like this exist. Wide buyer-seller spreads have a documented tendency to compress into smaller-than-anticipated price movements as the two sides negotiate toward a settlement price neither fully endorses.

What Is Actually Driving the Market in June 2026

The Dominant Signal: Nothing Is Dominant

One of the more revealing findings from the June 2026 survey is that the dominant market driver response among participants was "All Unchanged." This designation signals a market in approximate equilibrium, where no single supply disruption, demand surge, policy development, or macroeconomic catalyst is expected to meaningfully break prices in either direction. The consensus level around this view reached 67%, sitting slightly above the recent average range, which paradoxically indicates moderate agreement rather than overwhelming conviction, suggesting some participants do see specific catalysts at play even if the majority does not.

Geopolitical Uncertainty as a Price Suppressor

Geopolitical uncertainty is actively weighing on market sentiment, according to survey participants in the June 2026 outlook published by Fastmarkets. This factor functions as a soft ceiling on price enthusiasm rather than an acute downward driver, creating hesitation among buyers who might otherwise be willing to accept modest price increases. The ambiguity surrounding trade policy frameworks, export demand from key international markets, and the downstream implications of broader geopolitical tensions collectively limit the willingness of buyers to concede on price without clearer evidence of tightening supply.

This is a critical distinction: geopolitical uncertainty in the current context is not generating aggressive selling pressure. Instead, it is suppressing the magnitude of price gains that sellers might otherwise achieve given their elevated sentiment reading of 67.1. The US steel tariffs impact on downstream scrap markets remains a live variable, and the market is willing to move higher, but only cautiously.

Inventory Conditions: Balanced, Not Stressed

The Inventory Indicator reading of 50.7 is effectively at the midpoint of average stocking conditions, confirming that mills are neither meaningfully short of scrap units nor holding excess inventory that would create selling pressure. This balanced inventory state is an important stabilising factor, removing the urgency that typically drives more dramatic price swings. When mills are running lean on inventory, buying activity tends to intensify rapidly, compressing the time available for price negotiation. When mills are overstocked, the reverse dynamic unfolds. At 50.7, neither scenario is in play, reinforcing the "All Unchanged" equilibrium narrative.

Grade Performance: Where the Market Is Winning and Losing

Premium Grades Continue to Outperform

The structural case for premium grades like #1 Busheling and Shredded Auto Scrap rests on their compatibility with EAF steelmaking. Electric arc furnaces are sensitive to the residual content of their input material, particularly copper, tin, and nickel, which cannot be removed once incorporated into the steel melt. Grades that offer low residual levels command a consistent premium because they allow EAF operators to produce a wider range of steel specifications, including higher-value flat-rolled products, without expensive dilution strategies.

- #1 Busheling ($410/ton): Generated primarily from industrial stamping and manufacturing operations, this grade represents one of the cleanest available scrap streams and is considered a foundational input for EAF flat-rolled production

- Shredded Auto Scrap ($415/ton): Produced through the shredding of end-of-life vehicles, this grade benefits from advanced sorting technologies that have improved its metallurgical consistency considerably over the past decade

- Both grades are currently experiencing "stable to firm" conditions, supported by structural EAF demand

Mid-Tier and Lower Grades: Where Softness Is Most Visible

The contrast at the lower end of the grade spectrum tells a different story. HMS 80/20 at $285 per ton and Sheet Metal at $250 per ton represent the weakest segments of the market, facing headwinds from both reduced export appetite and increasing domestic mill selectivity. As mills have the ability to be more selective about their scrap diet in a balanced inventory environment, lower-grade materials face greater pricing pressure since they offer less metallurgical value and require mills to absorb higher processing costs or blend more aggressively with premium grades.

The price gap dynamics by category are worth examining:

| Grade Category | Price Range | Key Driver |

|---|---|---|

| Premium (EAF-optimised) | $410-$415/ton | Low residuals, high metallurgical purity |

| Mid-Tier | $365-$390/ton | Functional but less selective demand |

| Lower-Grade | $250-$285/ton | Export sensitivity, mill selectivity |

The Broader Steel Market Context

EAF Utilisation as the Underlying Demand Signal

US ferrous scrap prices in June cannot be understood in isolation from the steel mills that consume the material. EAF facilities, which use scrap as their primary or exclusive iron input, account for an increasingly dominant share of US steel production capacity. Fluctuations in EAF capacity utilisation rates function as leading indicators for scrap demand, with even modest changes in operating rates translating into meaningful shifts in scrap absorption across different grade categories.

Periods of reduced EAF utilisation create scrap accumulation dynamics that can accelerate price weakness, while high-utilisation environments create competitive buying conditions that support prices across the grade spectrum. In addition, innovations such as hydrogen iron ore reduction technologies are beginning to offer alternative iron unit sources that could, over the longer term, influence scrap's relative competitiveness.

Export Markets and the Global Price Floor

US ferrous scrap operates as a globally traded commodity, with export demand from key international buyers including Turkey, South Korea, and markets across Southeast Asia playing a significant role in establishing domestic price floors. When international demand is robust and export volumes are high, domestic scrap prices benefit from competition between domestic mills and international buyers for available material.

When export demand softens, as has been observed in periods of geopolitical uncertainty or when international buyers develop domestic scrap alternatives, the absence of this competitive pressure can amplify domestic price softness. The trade impacts on iron ore and related ferrous commodities provide useful parallel context for understanding these export dynamics.

Downstream Activity: Construction and Manufacturing as Demand Anchors

Construction and manufacturing activity represent the ultimate demand signal for ferrous scrap through their influence on finished steel consumption. Residential and commercial construction drives demand for rebar and structural steel products, which in turn sustains consumption of lower and mid-tier scrap grades used in long products mills. Automotive and capital goods manufacturing generates demand for flat-rolled steel products, supporting prime scrap grade consumption. Any meaningful softening in forward order books for either sector creates a sequential reduction in scrap purchasing activity that can take several weeks to manifest in benchmark pricing.

Furthermore, green steel pricing trends are beginning to intersect with scrap market dynamics, as producers increasingly look to lower-carbon production routes that place a premium on high-quality scrap inputs.

The next major ASX story will hit our subscribers first

Scenarios for H2 2026: Three Possible Trajectories

The June 2026 market data, when synthesised with the broader structural and cyclical context, points toward three plausible second-half trajectories:

| Scenario | Conditions Required | Likely Price Direction |

|---|---|---|

| Bull Case | EAF utilisation rises, export demand recovers, geopolitical clarity improves | Sustained gains above +3-5% MoM |

| Base Case | Balanced inventory, modest demand growth, stable trade conditions | Gradual +1-2% MoM gains, grade divergence persists |

| Bear Case | Demand softens, export markets contract, macro uncertainty deepens | Return to negative MoM territory, lower-grade prices under pressure |

The base case appears most consistent with current data, given the balanced inventory reading, modestly constructive Trend Indicator, and the absence of a dominant bullish or bearish catalyst. However, the proximity of the Trend Indicator to neutral at 54.9 means that relatively modest changes in any of the key variables could shift the balance toward either the bull or bear case without requiring dramatic underlying developments.

Disclaimer: Price forecasts and scenario projections discussed in this article are based on survey-derived sentiment data and should not be construed as financial or trading advice. Commodity markets are inherently uncertain, and actual outcomes may differ materially from forecasted expectations.

Frequently Asked Questions: US Ferrous Scrap Prices in June

What is the current price of ferrous scrap in the US?

As of early June 2026, US ferrous scrap prices range from approximately $250 per ton for sheet metal to $415 per ton for shredded auto scrap, with the benchmark index at roughly $401 per ton across all grades. For live benchmark data, the USGS iron and steel scrap statistics provide a useful historical reference point for contextualising current pricing.

Are ferrous scrap prices going up or down in June 2026?

The market is forecasting a modest average increase of approximately +2.0% month-on-month for June 2026, though sentiment varies considerably by participant type, with sellers bullish at 67.1 and buyers cautious at 47.5.

What is the most expensive scrap grade in June 2026?

Shredded auto scrap leads pricing at approximately $415 per ton, closely followed by #1 busheling at $410 per ton, both supported by strong EAF compatibility.

Why are HMS 80/20 and sheet metal prices significantly lower than premium grades?

Lower-grade materials contain higher levels of residual impurities and require greater processing effort by steelmakers, reducing their economic value. They are also more sensitive to export demand fluctuations, which adds downward pricing pressure when international buying activity weakens.

What does a Trend Indicator reading of 54.9 mean?

A reading above 50 indicates net bullish market sentiment. At 54.9, participants are modestly positive but lack the conviction typically associated with strong upward momentum, which historically requires readings approaching or exceeding 65 to generate pronounced price gains.

How does June 2026 compare to June 2025?

June 2025 was characterised by bearish sentiment and a forecasted price decline of -1.7%. June 2026 is considerably more constructive at +2.0% forecasted, reflecting meaningfully improved underlying market conditions year-over-year.

Key Takeaways for Market Participants

The US ferrous scrap prices in June 2026 present a nuanced picture that resists simple characterisation as either a bull or bear market. Instead, it represents a transitional environment where structural tailwinds for premium grades coexist with persistent macro headwinds for the broader market.

- Buyers should monitor EAF utilisation rate trends closely, as any acceleration in mill operating rates would reduce the leverage they currently hold at a Trend Indicator reading of 47.5

- Sellers have measurable support in their 67.1 reading, but buyer resistance caps near-term upside, suggesting that negotiation strategy and timing will matter more than directional conviction in June trades

- Brokers sitting at perfect neutrality face a market where execution quality and spread management will determine profitability rather than directional positioning

- All participants should track export demand recovery from Turkey and Southeast Asia, as restoration of international buying activity would materially strengthen the bull case for H2 2026

The grade divergence theme is arguably the most important structural signal embedded in the current price landscape. The widening spread between premium EAF-compatible grades and lower-tier materials is not a temporary artifact of cyclical conditions. It reflects the long-term transition of the US steel industry toward cleaner, more efficient production methods, and that transition has further to run.

For regular updates on US ferrous scrap market trends, price benchmarks, and the survey-based forecasting methodology underlying the Trend Indicator, Fastmarkets publishes the US Scrap Trends Outlook report for industry participants at fastmarkets.com.

Want to Capitalise on the Next Major ASX Mineral Discovery Before the Broader Market Catches On?

The structural shifts reshaping steel and ferrous commodities underscore just how quickly market dynamics can evolve — and how critical it is to act on significant discoveries the moment they are announced. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex data across more than 30 commodities into clear, actionable insights, so investors can explore historic discovery returns or begin a 14-day free trial at Discovery Alert to position themselves ahead of the market.