June 18, 2026

The Strait of Hormuz Has Always Been the World's Most Fragile Pressure Point

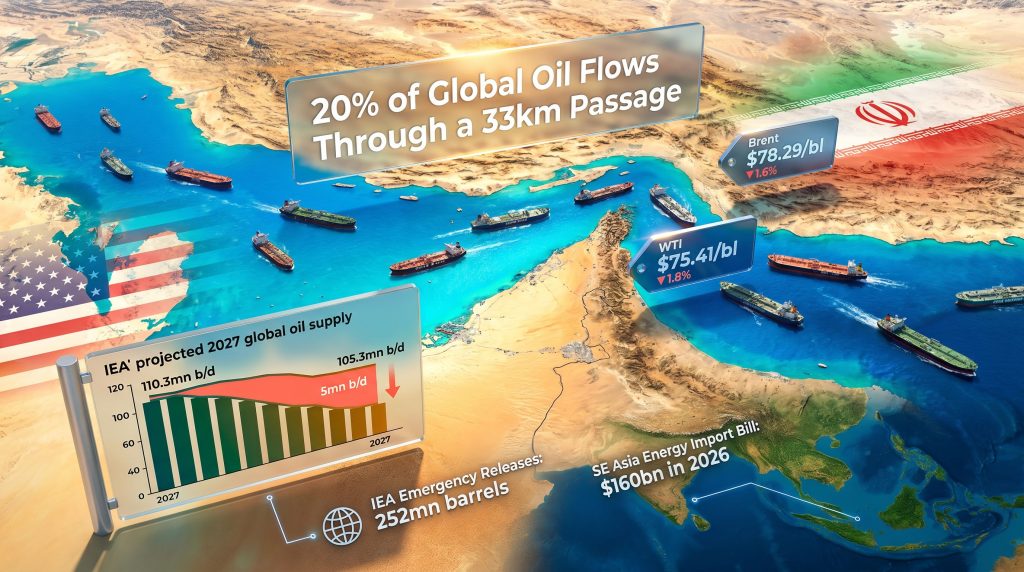

Roughly one-fifth of the world's daily oil supply moves through a passage so narrow that a single hostile actor can hold the entire global economy to ransom. The Strait of Hormuz, stretching just 33 kilometres at its tightest point, is not merely a shipping lane. It is the physical fulcrum of global energy pricing, petrochemical supply chains, and the fiscal stability of dozens of oil-importing economies. When that passage is disrupted, the consequences ripple from refinery margins in Rotterdam to cooking fuel availability in Manila within days.

The US-Iran peace deal, formalised on 18 June 2026 through the electronic signing of the Islamabad Memorandum of Understanding, is being framed in diplomatic circles as a resolution to one of the most disruptive geopolitical conflicts of the decade. However, anyone expecting a clean, settled outcome will find the reality considerably more complicated. What has been signed is an interim framework, not a final treaty. The 60-day negotiation window that follows leaves the most consequential questions entirely open.

Understanding what this deal actually means requires separating the immediate market mechanics from the long-term structural uncertainties. Furthermore, crude oil price trends heading into 2026 had already established a volatile baseline against which these diplomatic developments are being measured.

Disclaimer: This article draws on publicly available market data, IEA projections, and industry commentary. All forecasts and scenario analysis represent forward-looking estimates subject to material uncertainty. Nothing in this article constitutes financial advice.

When big ASX news breaks, our subscribers know first

What the Islamabad MoU Actually Commits Each Side To

The agreement, facilitated by Pakistani Prime Minister Shehbaz Sharif and signed separately by US President Donald Trump in Versailles and Iranian President Masoud Pezeshkian, establishes a ceasefire framework and a set of immediate obligations on both sides. Pakistan's role as mediator is itself a geopolitically significant development, reflecting the growing diplomatic weight of non-Western intermediaries in resolving major power conflicts. For context on how geopolitical trade tensions have reshaped diplomatic frameworks, this agreement represents a notable evolution.

Iran's Obligations Within the First 30 Days

- Restore vessel movement between the Mideast Gulf and the Gulf of Oman to pre-conflict levels, accounting for the need to neutralise mines and clear technical navigation obstacles

- Allow commercial vessels to transit the Strait of Hormuz without fees or tolls for an initial 60-day window, addressing Iran's earlier proposal to impose service charges on transiting ships

- Engage in joint consultations with Oman on the future administration and maritime governance of the strait, in accordance with applicable international law

US Obligations Under the MoU

- Lift the naval blockade of Iranian ports immediately upon the agreement entering into force

- Issue US Treasury waivers covering exports of Iranian crude oil, petrochemical products and their derivatives, along with all associated services including banking, insurance, and cargo transportation

- Participate in designing a rehabilitation and economic development financing framework for Iran, with a target of at least $300 billion

The Critical Unresolved Issues

The 60-day window that follows the MoU signing is where the real negotiation begins. The table below illustrates precisely how much remains unresolved.

| Issue | Status Under MoU | Next Phase |

|---|---|---|

| Iran's nuclear programme | Framework only, no binding terms | 60-day final agreement talks |

| Sanctions relief schedule | Conditional on nuclear compliance | To be negotiated |

| Hormuz toll structure post-60 days | Temporarily waived, future model unresolved | Iran-Oman consultations |

| Missile programme and proxy networks | Not addressed in MoU | Unclear if in scope |

| $300bn reconstruction fund sourcing | Concept agreed, funding mechanism open | Gulf Arab state contributions proposed |

Critical Caveat: Multiple credible sources characterise this agreement as an interim memorandum rather than a settled peace treaty. Iran's semi-official Fars news agency, which is close to the Islamic Revolutionary Guard Corps, described the toll-free transit exemption as explicitly temporary, signalling that Tehran retains long-term ambitions to assert sovereign control over Hormuz navigation.

The gap between the two sides' characterisations of the deal is itself a material risk. Trump publicly stated his view that Hormuz would be completely open by the signing date, while AIS vessel tracking data showed no material change in ship traffic through the strait in the days preceding the agreement. Consequently, shipowners appear to be exercising caution, waiting for confirmed operational clarity before attempting transits.

Why Trump Moved First: The Military Logic Behind Unprecedented Concessions

One of the most analytically significant aspects of the US-Iran peace deal is the nature of the concessions the United States agreed to make. Trump publicly acknowledged at the G7 leaders' summit in France that continued military pressure had reached a strategic ceiling. His stated reasoning was direct: sustained aerial bombardment could continue indefinitely, but it would not produce an open Strait of Hormuz.

That admission represents a fundamental recalibration of US leverage calculations. This is a rare instance in modern US foreign policy where a sitting president explicitly conceded the limits of military coercion as a tool for achieving a specific economic objective. The Atlantic Council's expert analysis of the interim deal highlights how the concessions extended to Iran — including the scope of sanctions relief and the scale of the reconstruction financing commitment — both exceed what many analysts had anticipated as a realistic negotiating floor.

Senator Lindsey Graham publicly raised concerns that Iran's interpretation of the agreement differed materially from the US negotiating team's account of what had been agreed, and formally called on Vice President JD Vance to present the full text to Congress for review. This creates a domestic political constraint that could complicate the delivery of US commitments, particularly the sanctions relief schedule.

How Oil Markets Priced the Deal the Moment It Was Confirmed

The immediate market response to the signing was a coordinated sell-off in crude futures, consistent with how energy markets typically price the removal of a geopolitical risk premium. In addition, the OPEC market influence factor looms large, as renewed Iranian supply would significantly alter the cartel's internal production dynamics.

- ICE Brent front-month (August contract): Fell to $78.29/bl as of 11:30 Singapore time on 18 June 2026, representing a 1.6% decline from the prior session's close

- Nymex WTI (July contract): Dropped to $75.41/bl, a 1.8% decline from the previous day

This price action reflects forward-pricing logic rather than current supply conditions. Markets are not responding to oil that is flowing yet. They are pricing the probability-weighted expectation of significantly higher supply volumes entering the market over the next 12 to 24 months, discounting that probability against the considerable uncertainties that remain.

The Supply Surplus Scenario That Is Driving Bearish Sentiment

The International Energy Agency's June 2026 Oil Market Report provides the quantitative foundation for understanding why energy markets moved so decisively on the signing news.

IEA Statistical Spotlight: Global oil supply is projected to surge by 8 million barrels per day in 2027, reaching 110.3mn b/d, as Mideast Gulf production recovers and OPEC+ raises output targets. Against a demand forecast of only 105.3mn b/d, this implies a structural surplus of approximately 5mn b/d, potentially the largest peacetime oversupply in modern history.

The IEA also revised its 2026 demand forecast downward to 103.3mn b/d, from 104mn b/d in its May report, citing the spread of consumption decline beyond the sectors initially most affected by the conflict. Preliminary data suggests second-quarter 2026 demand will be 5mn b/d lower than a year earlier, marking the first quarterly global demand decline since 2020.

Emergency Stock Drawdowns: Understanding How Deep the Buffer Has Been Used

The scale of coordinated emergency stock releases during the conflict illustrates the severity of the supply shock that preceded this deal.

- Global observed oil inventories have drawn down by an estimated 3.8mn b/d since the onset of the US-Iran conflict

- Preliminary data indicates a 4.6mn b/d stock draw in May alone, a figure that ranks among the most severe monthly inventory declines on record

- IEA coordinated emergency stock releases totalled 252mn barrels as of 12 June 2026, with a further 79mn barrels scheduled through the end of July

- A remaining 107mn barrels of emergency stock capacity stands available, to be deployed depending on evolving market conditions

The IEA noted that a post-deal supply recovery could present an opportunity to replenish these depleted inventories, or alternatively to build new strategic reserves, particularly across import-dependent regions.

The Tanker Market Transformation: From Shadow Fleet to Mainstream Shipping

One of the least-discussed but most commercially significant dimensions of the US-Iran peace deal concerns the global tanker market. Iranian crude has been transported under sanctions predominantly via what the industry calls the shadow fleet: older, underinsured vessels operating outside Western compliance frameworks, frequently with obscured ownership structures and flag-of-convenience registrations.

How the Shadow Fleet Worked and Why It Persisted

The shadow fleet model emerged as a commercial workaround to US sanctions, allowing Iranian crude to reach markets — primarily China's independent refining sector — without triggering Western regulatory penalties. These ships trade at a discount to mainstream vessels but provide a service that compliant operators cannot legally offer. China's independent refiners, known colloquially as teapot refineries, became the structural anchor of Iranian crude demand under this arrangement.

What Sanctions Relief Means for Mainstream Tanker Operators

Industry commentary at the Marine Money Conference in New York in June 2026 provided a clear picture of the commercial logic at play. Capital Tankers chief executive Jerry Kalogiratos argued that once Iranian crude achieves equivalent treatment to non-sanctioned barrels, importers have no remaining commercial rationale for routing cargo through substandard vessels. The compliance risk, insurance cost disadvantage, and reputational exposure all disappear simultaneously.

Frontline chief executive Lars Barstad characterised desanctioned Iranian crude as representing an entirely new barrel to the compliant tanker fleet — an important conceptual distinction. This is not simply a reallocation of existing cargo flows between ship types. It represents incremental demand creation for mainstream tanker capacity, since Iranian volumes previously invisible to compliant operators now enter their addressable market.

The Venezuela Precedent: A Comparable Template

An instructive parallel exists in the US Office of Foreign Assets Control's earlier issuance of a general licence on Venezuelan crude. That licence redirected Venezuelan export flows toward compliant mainstream vessels and produced a measurable supportive effect on crude tanker rates out of the US Gulf Coast. If OFAC issues a comparable general licence on Iranian crude, the scale effect could be substantially larger given Iran's significantly higher production capacity relative to Venezuela.

| Market Participant | Likely Outcome |

|---|---|

| Mainstream crude tanker operators | Increased cargo volume, potential rate support |

| Shadow fleet operators | Loss of Iranian cargo premium, structural demand decline |

| China's independent refiners | Compliant access to Iranian crude, reduced regulatory exposure |

| Gulf Arab state refiners | New competitive pressure from re-entering Iranian barrels |

| US adversary nations trading with Iran | Reduced sanctions risk, reduced pricing advantage |

Former OFAC head of policy Stephanie Connor noted at the same conference that a general licence, if issued rapidly, would primarily benefit countries already trading with Iran despite sanctions. This insight highlights an underappreciated asymmetry: the commercial winners from sanctions normalisation are not necessarily US-aligned economies.

Southeast Asia's Structural Exposure: The Region Most Transformed by Hormuz Disruption

No region has felt the consequences of Hormuz disruption more acutely than Southeast Asia, and no region has more at stake in the deal's success or failure. Furthermore, the broader oil market disruption of recent years had already placed extraordinary pressure on the region's energy budgets before the conflict escalated.

- The Middle East supplies approximately 60% of Southeast Asia's crude oil imports

- An estimated 45% of oil products refined or consumed across the region derive from Middle Eastern crude

- Southeast Asia's energy import bill is projected to reach a record $160 billion in 2026

- Under current policy trajectories, that bill could rise to $400 billion, equivalent to 5% of the region's GDP, by 2050

- The region accounts for nearly 20% of global energy demand growth projected through to 2035

The IEA's Southeast Asia Energy Outlook 2026, released on 16 June 2026, characterised the Hormuz disruption not merely as a supply shock but as a structural stress test that exposed the region's deep dependence on a single supply corridor. Shortages of naphtha, a critical petrochemical feedstock, and LPG, a primary cooking fuel across much of Southeast Asia, illustrated the breadth of downstream vulnerability beyond transport fuels alone.

Accelerated Diversification: What Governments Are Now Doing

Near-term government responses have included public transport incentives, remote working promotion, fuel tax reductions, and price controls. However, the more significant shift is structural. The energy transition pressures accelerated by the conflict have pushed governments across the region to fast-track renewable capacity targets.

- Renewable energy capacity across Southeast Asia stood at 120GW in 2024, projected to nearly triple by 2035 under current policy settings, or grow fivefold if announced targets are fully achieved

- Electricity demand is forecast to nearly double from 1,300 TWh/yr today to 2,000 TWh/yr by 2050

- Grid and storage investment requirements are projected to scale from $13 billion currently to $50 billion annually by 2050

- The Philippines emerged as the second-largest destination for Chinese solar exports in Q1 2026, a concrete signal of accelerating renewable momentum

The next major ASX story will hit our subscribers first

Three Scenarios for the Next 60 Days

Scenario 1: Full Agreement Reached

If Iran meets nuclear compliance benchmarks, sanctions are lifted on schedule, and Hormuz governance is formalised under international maritime law, Iranian crude production gradually scales toward pre-sanctions capacity of approximately 3.5 to 4mn b/d. The 2027 supply surplus materialises as projected, placing sustained downward pressure on global crude prices. Mainstream tanker demand rises structurally as shadow fleet cargo is redirected. Southeast Asian energy import costs moderate accordingly.

Scenario 2: Partial Agreement

If Hormuz reopens but nuclear talks stall and sanctions relief remains conditional and partial, oil prices stay range-bound with an elevated volatility premium. Shadow fleet operators retain a partial role. Mainstream tanker operators see incremental but not transformative demand uplift. Southeast Asian governments maintain emergency diversification measures as a precaution against renewed disruption.

Scenario 3: Deal Collapse

If the 60-day talks break down over nuclear compliance or Hormuz governance, crude prices spike sharply above $90/bl as supply disruption fears re-emerge. The remaining 107mn barrels of emergency IEA stock capacity is re-activated. Southeast Asia's energy import bill surges further beyond the 2026 record. Geopolitical risk premiums return across all commodity classes, and the shadow fleet resumes its central role.

The Macro Context: Rate Cycles, Inflation, and Energy Repricing

The energy price dynamics surrounding the US-Iran peace deal are intersecting with a complex global monetary policy environment. Brazil's central bank cut its benchmark rate to 14.25% in June 2026, with ongoing Mideast Gulf conflict uncertainty explicitly cited as a headwind to the economic outlook. Brazil's headline inflation accelerated to an annual 4.72% in May 2026, with inflation expectations remaining above target at 5.3% for 2026 and 4.1% for 2027.

The US Federal Reserve, meanwhile, held its target rate unchanged for a fourth consecutive meeting in June 2026, with policymakers indicating a possible rate increase by year-end. This signals that energy-driven inflation remains a live concern in US monetary policy deliberations even as crude prices pull back on the deal's signing. A sustained normalisation of Iranian supply could ease this pressure materially over a 12 to 18-month horizon, though the 60-day negotiating uncertainty prevents markets from pricing this outcome with confidence.

The $300 Billion Question: Who Actually Funds Iran's Reconstruction?

The reconstruction financing framework embedded in the MoU is analytically fascinating and practically unresolved. The proposed $300 billion figure is referenced in the agreement, with the US and its regional partners described as responsible for creating the plan. US Vice President JD Vance confirmed in televised interviews that Gulf Arab states were the implied source of funding, conditional on Iran meeting nuclear obligations.

The geopolitical complexity here is acute. The same Gulf Arab states being asked to fund Iranian reconstruction sustained significant infrastructure damage from Iranian missile and drone strikes during the conflict. As reported by The Guardian, no Gulf Arab government had publicly committed to reconstruction fund participation as of the MoU signing date. The silence from Riyadh, Abu Dhabi, and Doha on this specific question is the loudest unresolved variable in the entire diplomatic architecture.

FAQ: US-Iran Peace Deal and Global Energy Markets

Is the Islamabad MoU a Final Peace Treaty?

No. It is an interim memorandum of understanding that establishes a ceasefire framework and opens a 60-day period of formal negotiations. A binding final agreement covering Iran's nuclear programme, permanent sanctions architecture, and long-term Hormuz governance has yet to be concluded.

When Will the Strait of Hormuz Fully Reopen?

Under the MoU, Iran committed to restoring vessel traffic to pre-conflict levels within 30 days, subject to mine clearance and removal of technical obstacles. Full unrestricted commercial navigation is anticipated to resume progressively rather than instantly.

Will Iranian Crude Immediately Enter Global Markets?

US Treasury waivers form part of the MoU framework, but the precise sanctions relief schedule is subject to ongoing negotiation and conditional on nuclear compliance. A general OFAC licence, if issued, would be the formal mechanism opening compliant-fleet Iranian crude trade at scale.

What Happens to Oil Prices if the Deal Holds?

Based on IEA projections, a successful deal restoring full Mideast Gulf production could generate a global oil surplus exceeding 5mn b/d in 2027, placing sustained downward pressure on crude prices over a multi-year horizon.

What Is the Shadow Fleet and Why Does It Matter?

The shadow fleet refers to older, poorly insured tankers used to transport sanctioned crude outside Western compliance frameworks. If Iranian crude is formally desanctioned, the commercial rationale for shadow fleet usage collapses, redirecting cargo to mainstream compliant operators and reshaping global tanker market dynamics structurally.

How Does the Deal Affect Southeast Asian Consumers?

A sustained Hormuz reopening and normalisation of Iranian crude exports would, over time, ease the region's record $160 billion energy import bill, reduce fuel price inflation, and relieve pressure on LPG and petrochemical feedstock supply chains that the conflict disrupted severely. The BBC's coverage of the negotiations underscores how closely Asian economies have been monitoring every stage of these talks.

Further coverage of the Strait of Hormuz situation and global energy market developments connected to the US-Iran peace deal is available via Argus Media at argusmedia.com.

Want to Stay Ahead of the Commodity Discoveries Driving the Next Market Shift?

While geopolitical events like the US-Iran peace deal reshape global energy and commodity markets, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex data across 30+ commodities into actionable insights — explore historic discoveries and their market returns to understand what's possible, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next major opportunity.