July 13, 2026

The Geography of Vulnerability: Why One Narrow Passage Controls Global Energy

Roughly a third of the world's seaborne oil trade passes through a corridor no wider than 33 nautical miles at its narrowest point. The Strait of Hormuz, separating the Iranian coastline from the Omani peninsula, functions less like a shipping lane and more like a pressure valve for the global economy. When that valve is threatened, energy markets, insurance underwriters, and naval planners across four continents respond simultaneously. The US Iran strikes Strait of Hormuz situation in 2026 has brought this vulnerability into sharp focus.

That structural reality is precisely what makes the escalation cycle of July 2026 so consequential. Unlike prior standoffs that were largely rhetorical or involved limited skirmishes, the current crisis involves coordinated military strikes, commercial vessel targeting, competing declarations over Hormuz's operational status, and simultaneous diplomatic fragmentation across multiple allied governments.

Understanding what is actually happening, what markets are pricing, and what the realistic resolution pathways look like requires separating political signalling from operational reality.

When big ASX news breaks, our subscribers know first

The Strait's Strategic Anatomy: Why There Is No Substitute

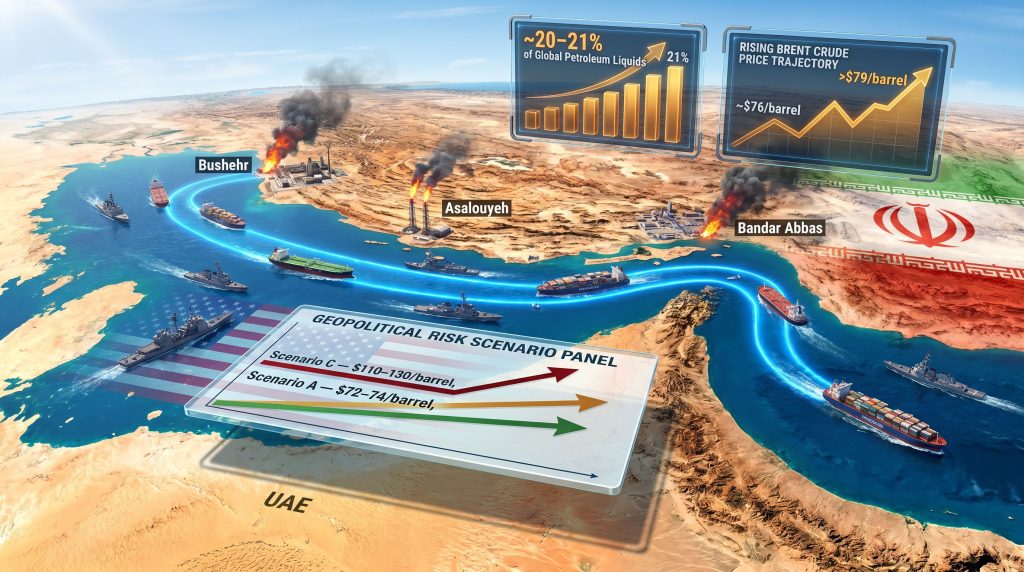

The Strait of Hormuz carries approximately 20 to 21 percent of global petroleum liquids annually, alongside a disproportionately large share of global LNG supply exports. The navigable shipping corridor within the strait is effectively constrained to two lanes, each roughly two miles wide, separated by a median zone. Supertankers and LNG carriers operating at full load have limited manoeuvrability within these corridors, creating physical chokepoints that cannot simply be rerouted.

The Gulf producers most exposed to Hormuz dependency include:

- Saudi Arabia, which exports the majority of its crude through the strait despite partial capacity via the East-West Pipeline to Yanbu

- Qatar, the world's largest LNG exporter, with virtually no viable alternative export route at scale

- UAE, Kuwait, and Iraq, whose upstream production funnels almost entirely through Hormuz passage

- Iran itself, whose oil and petrochemical exports depend on Hormuz and its southern coastal port infrastructure

The often-cited alternative of rerouting via the Cape of Good Hope adds 10 to 15 days to voyage times and introduces significant cost escalation. More critically, however, it cannot absorb the volume. The global LNG tanker fleet and VLCC (Very Large Crude Carrier) fleet simply cannot reroute at scale without causing structural supply shortfalls.

Historical Precedents: The Tanker War and Beyond

The 1980s Tanker War between Iran and Iraq offers the most instructive historical parallel. Between 1984 and 1988, over 400 commercial vessels were attacked in the Persian Gulf, prompting the United States to launch Operation Earnest Will in 1987, the largest naval convoy operation since World War II. Oil prices during that period exhibited sharp but ultimately transient spikes, with markets adjusting as the operational corridor remained partially functional.

The critical difference in 2026 is that the adversarial dynamic has evolved significantly. Iran's asymmetric maritime doctrine now incorporates fast-attack craft, anti-ship missile systems, underwater drone capabilities, and coastal radar networks that did not exist in the 1980s. Consequently, US freedom-of-navigation operations face a qualitatively different threat environment than Operation Earnest Will encountered.

The 2026 Escalation Architecture: What Actually Happened

The current crisis traces its origins to Operation Epic Fury on February 28, 2026, a US-Israeli military operation that fundamentally restructured Iran's leadership. The aftermath created a sustained period of commercial vessel targeting in Hormuz as Iran's surviving command structure sought leverage through maritime disruption. Furthermore, the broader crude oil geopolitics of the region were already under significant strain before these events unfolded.

A June 17, 2026 interim ceasefire agreement appeared to stabilise the situation temporarily, but it carried a structural weakness common to conflict-zone ceasefires: no enforcement mechanism. The agreement left Iran's nuclear programme negotiations unresolved, which functioned as an ongoing source of diplomatic tension undermining the truce's durability.

The collapse came swiftly. On July 6 and 7, 2026, three commercial tankers were targeted in the strait: the M/T Al Rekayyat, M/T Wedyan, and M/T Cyprus Prosperity. Reuters reports that the Islamic Revolutionary Guard Corps framed these interceptions as enforcement actions against vessels it claimed were travelling along what it described as "illegal routes," a framing rejected by the United States, international maritime law bodies, and Western governments broadly.

The US military response was significant in both scale and pace:

| Strike Phase | Date | Targets Engaged | Primary Infrastructure Targeted |

|---|---|---|---|

| Initial US Response | July 7, 2026 | ~80 targets | Missile sites, command centres, fast-attack boats |

| Follow-on Strikes | July 8, 2026 | ~90 targets | Air defence systems, coastal radar, naval assets |

| Expanded Operations | July 12-13, 2026 | ~140 cumulative | Drone systems, missile depots, coastal installations |

The deliberate targeting of air defence systems and coastal radar infrastructure reflects a clear strategic logic: by degrading Iran's ability to track and engage commercial vessels, US forces aimed to restore operational viability to the transit corridor without requiring permanent naval escort of every vessel.

US Central Command confirmed strikes against approximately 140 targets across the escalation period, representing the most extensive US military action against Iran in the modern era.

Iran's Multi-Front Retaliation: Reading the Target Selection

Iran's response moved beyond maritime harassment into a geographically expanded campaign targeting US military infrastructure across multiple sovereign states. Strike reports confirmed attacks against:

- Kuwait: Drone strikes against US Army positions, with a separate attack damaging a drilling platform operated by Kuwait's state-run oil company

- Bahrain: IRGC strikes targeting helicopter maintenance facilities, a P-8 electronic warfare aircraft hangar, and drone command and control centres at a US base

- Jordan: Missile and drone strikes against Prince Hassan Air Base, a NATO-adjacent facility, targeting missile depots and fuel storage tanks

- Oman: Strikes reported against US naval logistics hubs and aircraft carrier refuelling platforms at the Port of Duqm

The specificity of Iranian target selection is analytically significant. Precision strikes against P-8 aircraft hangars and drone command centres suggest Iranian intelligence possessed detailed positional data on US military assets across the region, which has implications for operational security planning well beyond the immediate conflict.

The collateral escalation dimension also intensified. The UAE activated air defences in response to a detected missile threat near its borders, while Qatar reported civilian casualties from debris following the interception of Iranian missile attacks. Three people were wounded in Qatar, a country that simultaneously hosts the largest US air base in the Middle East and serves as the world's leading LNG exporter, creating an acutely exposed strategic position.

The Hormuz Closure Declaration: Signal vs. Reality

Tehran declared the Strait of Hormuz closed "until further notice." US Central Command immediately disputed this characterisation, asserting that the waterway remained open to all vessels and that US naval forces were prepared to guarantee freedom of navigation. The Joint Maritime Information Center, a global monitoring body, independently confirmed that the strait's southern route remained transitable as of July 13, 2026.

Operational data supports the US position. Approximately 20 commercial vessels successfully transited the strait in coordination with US military escort over the period. Ship-tracking data confirmed the LNG tanker Al Hamra transited the strait over the weekend and was subsequently tracked in the Gulf of Oman.

The divergence between Iran's closure declaration and actual vessel transits illustrates a fundamental feature of Hormuz crises: political signalling and operational reality frequently diverge. Markets price the signal; logistics adapt to the reality. Understanding this gap is critical for energy traders and supply chain planners.

How Oil Markets Are Pricing the Conflict

Brent crude responded sharply to each escalation trigger, functioning as a real-time barometer of geopolitical risk pricing. In addition, the broader pattern of oil price movements associated with geopolitical crises provides important context for interpreting current volatility:

| Trigger Event | Brent Crude Movement | Price Level |

|---|---|---|

| Initial July 7-8 US strikes | +3% surge | ~$76/barrel |

| Continued escalation (July 12-13) | +4.3% intraday gain | >$79/barrel |

| Iran's Hormuz closure declaration | Sustained elevated volatility | Structurally elevated |

A critical distinction for market participants is the difference between disruption risk pricing and actual supply interruption pricing. Markets during Hormuz events tend to price the probability-weighted expected disruption, not the worst-case scenario outright. This means that even with Brent trading above $79/barrel, markets are implicitly assigning relatively low probability to a full, sustained closure.

Historical analysis of prior Hormuz disruption events suggests that oil price spikes from transit threats tend to mean-revert relatively quickly, typically within 4 to 8 weeks, provided the physical corridor remains operationally functional. The key variable is whether vessel insurance markets trigger a broader withdrawal of commercial shipping, which can operationally achieve what a military blockade cannot.

Sanctions Re-Escalation: The Compounding Variable

A dimension that energy markets must price alongside the physical conflict is the US revocation of its temporary suspension of Iranian oil sanctions, which had been part of the June 2026 interim agreement. Iranian barrels that had been flowing under the sanctions waiver are now effectively re-sanctioned, compounding the supply-side risk beyond what the physical conflict alone represents.

Estimating the exact volume removed depends on the waiver's scope, but any reduction in Iranian export capacity at a moment of Hormuz transit uncertainty creates a dual supply shock that markets must absorb simultaneously. This oil market disruption compounds existing pressures that were already reshaping global energy trade flows.

Iranian Energy Infrastructure: Long-Term Petrochemical Consequences

Reported strikes at Bushehr and Asalouyeh, Iran's primary energy and petrochemical export hubs, carry consequences that extend well beyond the immediate conflict. Asalouyeh is the operational centre of Iran's South Pars gas field development, the world's largest natural gas field by recoverable reserves (shared with Qatar's North Dome field). Damage to processing and export infrastructure at this location has asymmetric downstream consequences for global petrochemical supply chains, particularly for feedstocks used in plastics, fertilisers, and specialty chemicals.

Port infrastructure damage at Bandar Abbas and Bandar-e Dayyer directly affects Iran's crude oil and refined products export capacity. Furthermore, reported extensive damage to Iran's power grid infrastructure, confirmed by the state-run utility Tavanir, introduces broader operational constraints across the Iranian economy that will compound recovery timelines.

The next major ASX story will hit our subscribers first

Three Scenarios for Hormuz: Probability and Market Impact

Scenario A: Negotiated De-escalation (30 to 60 day horizon)

- European diplomatic pressure (UK, France, Germany joint statement) provides the framework for ceasefire restoration

- US-Iran nuclear and sanctions talks resume with Omani or Qatari intermediation

- Brent crude normalises toward the $72 to $74/barrel range

- Shipping insurance war risk premiums begin declining as transit volumes recover

Scenario B: Sustained Attrition (3 to 6 month horizon)

- Tit-for-tat strikes continue without escalating to full-scale conventional war

- Hormuz remains operationally open but under persistent threat, maintaining elevated war risk premiums

- Brent crude stabilises in the $78 to $85/barrel range with structurally elevated volatility

- LNG spot markets carry a geopolitical risk premium as Asian and European buyers accelerate contingency sourcing

Scenario C: Full Strait Closure (Low probability, extreme impact)

- Physical blockade through mining operations or sustained naval engagement closes the navigable corridor

- Historical disruption modelling suggests Brent could reach $110 to $130/barrel under a sustained closure

- IEA member states activate strategic petroleum reserves, with the US, Japan, South Korea, and Germany holding the largest accessible stockpiles

- Cape of Good Hope rerouting adds 10 to 15 days to voyage times, structurally reshaping freight markets

The Nuclear Negotiation Paradox

The deepest structural driver of this conflict remains unresolved: Iran's nuclear programme. Military escalation creates a strategic paradox where the pressure applied to force a diplomatic resolution simultaneously makes that resolution harder to achieve. Negotiating teams cannot function effectively when the parties are exchanging active military strikes.

President Trump publicly declared the June 2026 ceasefire agreement effectively terminated while simultaneously confirming that diplomatic talks with Tehran would continue. This dual posture reflects the genuine complexity of managing military operations and diplomatic channels concurrently. However, it also introduces significant ambiguity about what framework, if any, governs the conflict's rules of engagement.

The UK-France-Germany joint statement condemning Iranian strikes and calling for ceasefire restoration carries diplomatic weight as a signal of Western unity but has limited operational leverage in an active military exchange. Sky News coverage of the ongoing situation highlights how NATO's characterisation of US strikes as necessary for freedom of navigation reinforces alliance cohesion publicly, while Arab Gulf states navigate the more difficult position of US security dependency versus direct exposure to Iranian retaliatory reach.

Key Indicators for Energy Markets and Policymakers to Track

The following variables will determine which of the three scenarios materialises. In addition, OPEC market influence over production decisions will play a significant role in shaping how the broader supply picture evolves:

- Daily vessel transit data through the Hormuz southern corridor, as a direct measure of operational status vs. political signalling

- Brent crude options market implied volatility, which functions as a leading indicator of escalation expectations before price moves

- War risk insurance premiums from Lloyd's of London and affiliated underwriters, which can operationally close Hormuz to commercial shipping even if the corridor remains physically open

- IRGC communications framing, specifically any shift from "enforcement" language toward formal "blockade" declarations

- Diplomatic back-channel signals through Oman or Qatar, both of which have historically maintained functional communication with Tehran

- Operational status of Asalouyeh and Bandar Abbas, as a measure of Iranian export capacity under sustained infrastructure pressure

The US Iran strikes Strait of Hormuz crisis has exposed the structural fragility of ceasefire agreements that lack enforcement architecture. The convergence of active military exchange, sanctions re-escalation, and energy infrastructure targeting creates a compounding risk environment that no single policy lever can quickly resolve.

What remains clear is that the world's most consequential energy chokepoint is under its most serious operational stress in decades. Consequently, the gap between political signalling and ground-level reality will define both market outcomes and diplomatic pathways in the weeks ahead.

For ongoing updates on oil market developments and upstream industry impacts related to the US Iran strikes Strait of Hormuz situation, Rigzone's energy news coverage provides continuous reporting from the sector.

Want to Capitalise on Energy Market Volatility Driven by Geopolitical Shocks Like Hormuz?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, empowering investors to identify actionable opportunities—including those in the energy and resources sector—ahead of the broader market. Explore historic examples of exceptional returns from major discoveries and begin your 14-day free trial today to position yourself ahead of the next market-moving event.