June 22, 2026

The US-Iran war impact on Strait of Hormuz represents a critical geopolitical flashpoint that could reshape global energy markets and trigger widespread economic disruption. The interconnected nature of modern economies means that disruptions in one region can trigger price volatility, supply shortages, and economic instability across continents. Understanding these complex relationships becomes essential for investors, policymakers, and businesses seeking to navigate an increasingly uncertain global landscape.

Geographic Importance of the Strait of Hormuz in Global Energy Security

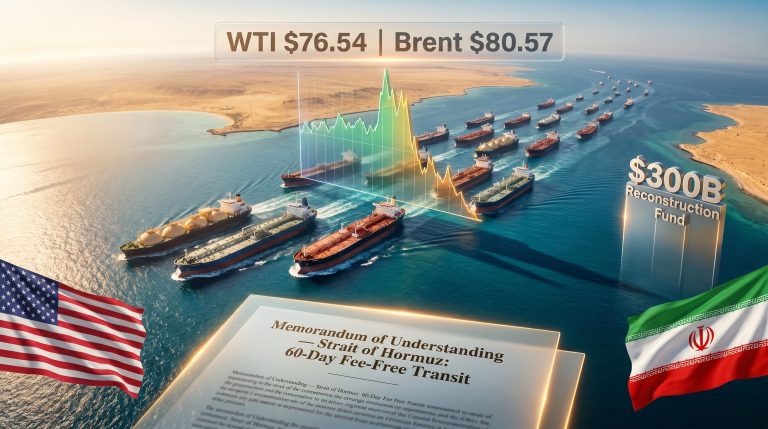

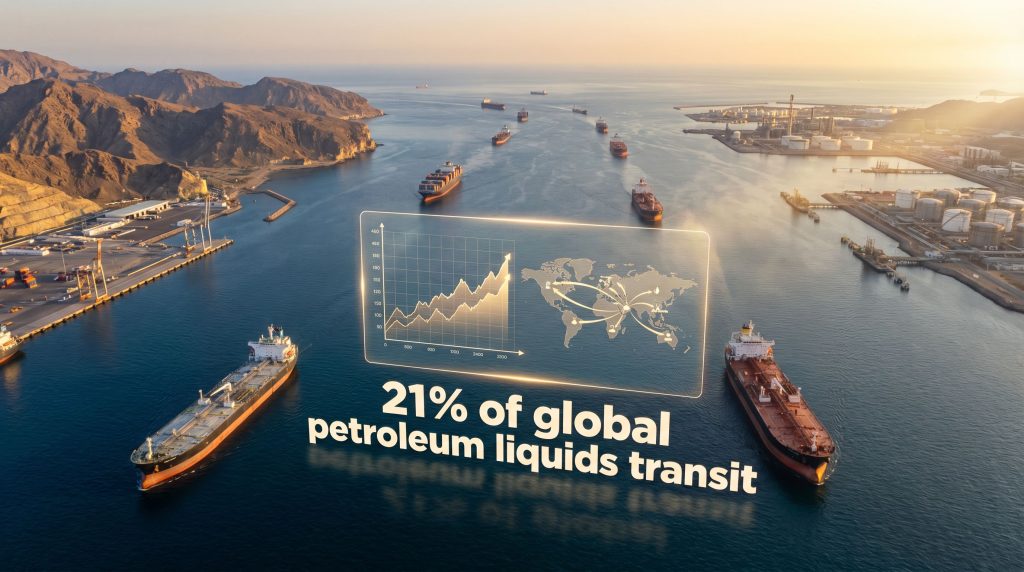

The Strait of Hormuz represents one of the world's most critical energy chokepoints, facilitating the movement of approximately 21% of global petroleum liquids to international markets. This narrow waterway connects the Persian Gulf to the Arabian Sea, serving as the primary export route for major oil-producing nations. Furthermore, Saudi Arabia exploration licenses have increased regional production capacity, making this transit route even more vital.

The strategic significance extends beyond crude oil transportation. The strait handles substantial volumes of liquefied natural gas (LNG), refined petroleum products, and critical industrial materials including aluminium, sulphur, and various fertiliser components. Major oil terminals and LNG facilities concentrate along the Gulf coastline, creating a dense network of energy infrastructure vulnerable to disruption.

Alternative transportation routes exist but carry significant economic penalties. Pipeline systems through Turkey, Jordan, and other regional corridors possess limited capacity compared to seaborne transportation. The additional costs associated with rerouting shipments through alternative channels can add substantial premiums to energy prices, particularly for Asian consumers who rely heavily on Gulf supplies.

Current market analysis suggests physical oil prices are trading approximately $25 per barrel above futures contracts, indicating significant supply concerns that paper markets have yet to fully acknowledge. This pricing divergence highlights the disconnect between theoretical market pricing and physical supply realities.

When big ASX news breaks, our subscribers know first

Supply Chain Vulnerabilities Beyond Energy Commodities

The potential for extended conflict creates disruption risks that extend well beyond crude oil markets. The Gulf region serves as a major source of industrial raw materials essential to global manufacturing processes.

Key commodity flows at risk include:

- Aluminium production: Gulf states contribute significantly to global aluminium smelting capacity

- Sulphur exports: Essential for fertiliser production and chemical manufacturing

- Petrochemical feedstocks: Base materials for plastics, synthetic materials, and industrial chemicals

- Natural gas liquids: Critical components for petrochemical processing

Manufacturing sectors dependent on these inputs face potential cost escalation and supply constraints. European industrial centres, Asian manufacturing hubs, and chemical processing facilities worldwide could experience cascading effects from supply disruptions. Recent data indicates several critical materials have already experienced significant price increases, with ferrovannium up 90%, tantalum surging 173%, and lithium carbonate rising 34% since December.

The timeline for supply chain adjustments creates particular vulnerability. Oil shipments typically require 6-8 weeks to transit from Gulf loading terminals to final destinations, meaning existing supplies will be exhausted by late April if disruptions continue. This physical delivery gap creates potential for acute shortages despite paper market pricing that fails to reflect underlying supply constraints.

Oil Price Scenarios Under Different Conflict Durations

Market analysts have developed multiple scenarios for oil price evolution depending on conflict duration and intensity. These models reveal the potential for extreme price volatility that current futures markets appear to underestimate. In addition, analysis of natural gas price trends suggests energy markets remain vulnerable to geopolitical shocks.

What Happens During Short-Term Disruptions?

Brief disruptions would likely push oil prices toward $125-150 per barrel, supported by inventory drawdowns and strategic petroleum reserve releases. Physical supply constraints would drive immediate price premiums, while paper markets gradually adjust to reflect underlying scarcity.

Demand elasticity remains extremely low in the short term, meaning price increases produce minimal consumption reduction. Industrial processes, transportation systems, and heating requirements cannot quickly substitute alternative energy sources, forcing consumers to absorb higher costs rather than reduce consumption.

How Might Extended Conflicts Affect Global Markets?

Longer disruptions create scenarios where oil prices could reach $350 per barrel or higher. Such extreme pricing would necessitate demand destruction through economic recession rather than voluntary consumption reduction. The global economy would likely contract significantly, with worldwide GDP growth potentially turning negative.

Infrastructure reconstruction in affected regions would require 18-24 months for basic repairs, with some permanently damaged facilities potentially taking years to restore. Approximately 80 production and transmission facilities have sustained damage since conflict began, with one-third severely impacted.

Historical precedent from the 1973 Yom Kippur War demonstrates how oil supply disruptions trigger global recession rather than gradual demand adjustment. Economic contraction becomes the primary mechanism for reducing oil consumption when prices reach extreme levels.

Regional Economic Winners and Losers

Conflict-driven supply disruptions create distinct winners and losers across different regions and economic sectors. Understanding these dynamics helps identify investment opportunities and economic vulnerabilities, particularly as the US-China trade war impact continues to reshape global trade patterns.

Vulnerable Import-Dependent Economies

Several regions face particularly acute vulnerability to extended supply disruptions:

- Asian manufacturing centres: Japan, South Korea, and Taiwan depend heavily on Gulf energy imports

- European industrial regions: Chemical processing and manufacturing sectors face input cost pressures

- Developing economies: Limited financial resources to absorb higher energy costs

- Island nations: Geographic isolation compounds supply chain challenges

These economies would experience inflation acceleration, current account deterioration, and potential industrial production constraints. Currency depreciation against major reserve currencies would compound import cost pressures.

Strategic Beneficiaries

Alternative energy producers stand to benefit substantially from Gulf supply disruptions:

- North American producers: US shale operations, Canadian oil sands

- Non-Gulf suppliers: Russia, Norway, Venezuela (subject to sanctions constraints)

- Strategic reserve holders: Nations with diversified supply sources

- Alternative energy systems: Accelerated adoption of renewable capacity

Russia particularly benefits as a major producer of oil, natural gas, aluminium, fertilisers, and other commodities disrupted in Gulf markets. China maintains substantial commodity inventories accumulated through strategic hoarding, providing near-term insulation from supply shortages.

Monetary Policy Amplification of Commodity Volatility

Central bank policies significantly amplify commodity price movements through multiple transmission channels. Current monetary conditions create particularly conducive environments for commodity price inflation. However, tariffs' investment impacts add another layer of complexity to global monetary dynamics.

Money Supply Growth Dynamics

US money supply growth currently exceeds optimal levels for price stability. Commercial bank credit expansion approaches 7% annually, above the 6% rate consistent with 2% inflation targets. The Federal Reserve switched from quantitative tightening to expansion in December, purchasing approximately $45 billion in Treasury bills and directly contributing to money supply growth.

Key monetary transmission mechanisms include:

- Credit creation through commercial banking systems expanding lending capacity

- Quantitative easing programmes directly monetising government deficits

- Reduced reserve requirements freeing bank capital for additional lending

- Increased bank profitability expanding lending capacity

This monetary expansion creates ideal conditions for commodity price appreciation by increasing aggregate demand while supply constraints limit production responses.

Inflation Expectations and Central Bank Credibility

Central bank credibility becomes crucial during supply-driven inflation episodes. Historical analysis indicates that monetary authorities struggle to maintain 2% inflation targets when faced with persistent supply shocks. The current environment combines supply constraints with accommodative monetary policy, creating upward pressure on inflation expectations.

Currency relationships also influence commodity pricing. Despite geopolitical tensions, the dollar-euro exchange rate remains relatively stable, indicating continued confidence in dollar-denominated assets. The US dollar's strength relative to historical norms suggests limited currency-driven inflation pressures, though regional currencies may experience significant volatility.

Investment Strategies for Energy Supply Crisis

Investors seeking to position for extended supply disruptions should consider both direct commodity exposure and indirect beneficiaries of higher energy prices. Consequently, understanding the US economy and tariffs relationship becomes crucial for strategic positioning.

Direct Commodity Positioning

Several commodity sectors offer attractive risk-adjusted returns during supply crisis periods:

Energy Sector Opportunities:

- Oil and gas producer equities with low-cost production profiles

- Energy infrastructure companies controlling strategic transportation assets

- Alternative energy systems benefiting from fossil fuel price increases

- Strategic petroleum storage and trading operations

Critical Materials Exposure:

- Lithium and vanadium for energy storage applications

- Rare earth elements controlled by Chinese supply chains

- Industrial metals facing supply constraints (aluminium, copper)

- Agricultural commodities affected by fertiliser shortages

Geographic Diversification Strategies

Supply chain resilience requires geographic diversification away from concentrated risk areas:

- Alternative supplier relationships: North American and African resource companies

- Regional energy partnerships: Bilateral supply agreements outside traditional channels

- Infrastructure redundancy: Multiple transportation routes and storage facilities

- Political risk management: Insurance products and hedging mechanisms

Investment portfolios should emphasise companies with diversified supply sources, strong balance sheets to weather volatility, and strategic positioning in alternative energy systems.

The next major ASX story will hit our subscribers first

Accelerated Energy Transition Implications

Extended energy supply crises often catalyse structural changes in energy systems by making alternative technologies economically competitive with traditional fossil fuels.

Policy-Driven Transformation

High fossil fuel prices create political pressure for energy independence initiatives. Governments typically respond with increased renewable energy investments, grid modernisation programmes, and strategic mineral supply chain diversification. These policy responses often persist beyond immediate crisis periods, creating long-term structural changes.

Critical mineral supply chains become strategic priorities during energy crises. Lithium, vanadium, rare earth elements, and other materials essential for renewable energy systems experience increased investment and development activity. China's dominance in critical material processing creates additional supply chain vulnerabilities that policy makers seek to address.

Market-Driven Innovation

Economic incentives drive technological innovation and adoption during high energy price periods:

- Industrial electrification becomes cost-competitive with fossil fuel processes

- Transportation sector accelerates electric vehicle adoption

- Distributed energy systems gain economic advantages over centralised generation

- Energy storage technologies receive increased investment and deployment

These market-driven changes often create permanent shifts in energy consumption patterns that persist after crisis periods end.

Long-Term Geopolitical Realignments

Extended supply disruptions accelerate geopolitical realignments as nations seek energy security through diversified partnerships and reduced dependence on volatile regions. For instance, recent analyses of Iranian naval activities highlight the strategic importance of maintaining alternative supply routes.

Energy Partnership Evolution

Traditional energy relationships face restructuring as consumers seek supply security:

- Bilateral agreements: Direct government-to-government supply contracts

- Regional partnerships: Energy sharing arrangements among allied nations

- Strategic reserve coordination: Joint stockpiling and emergency sharing protocols

- Alternative supplier development: Investment in non-traditional producing regions

These partnership changes often outlast immediate crisis periods, creating structural shifts in global energy trade patterns.

Economic Integration Adjustments

Trade and investment flows adjust to reflect new energy realities:

- Regional trade agreements incorporate energy security provisions

- Currency arrangements adapt to changing trade patterns

- Technology transfer agreements focus on energy independence

- Investment capital redirects toward supply chain resilience

Despite discussions of de-dollarisation, practical alternatives for large-scale capital investment remain limited. The US maintains the world's largest and most liquid capital markets, constraining meaningful diversification away from dollar-denominated assets.

Policy Framework for Extended Disruption

Effective crisis management requires comprehensive policy frameworks addressing both immediate disruptions and long-term resilience building. Furthermore, ongoing analysis by the Center for Strategic and International Studies provides valuable insights into the strategic dimensions of this crisis.

Emergency Response Protocols

Immediate policy tools for managing supply crises include:

| Policy Tool | Mechanism | Effectiveness Timeline |

|---|---|---|

| Strategic Reserve Release | Direct market supply injection | 30-90 days |

| Demand Management Programmes | Industrial rationing systems | 60-180 days |

| Import Diversification | Alternative supplier agreements | 90-365 days |

| International Coordination | Multilateral response mechanisms | Variable |

These tools provide temporary relief while longer-term supply alternatives develop. Success depends on coordination among major consuming nations and availability of alternative supply sources.

Structural Resilience Development

Long-term resilience requires systematic investment in alternative systems:

- Supply chain diversification: Multiple supplier relationships and transportation routes

- Strategic stockpiling: Emergency reserves of critical commodities

- Alternative energy acceleration: Renewable capacity and grid modernisation

- Economic shock absorption: Financial mechanisms for managing price volatility

Policy makers must balance immediate crisis response with long-term structural transformation, often requiring sustained political commitment beyond election cycles.

Economic Indicators for Crisis Monitoring

Effective crisis management requires real-time monitoring of key economic indicators that signal escalation or resolution of supply disruptions.

Market Signal Analysis

Critical indicators for tracking crisis evolution include:

Physical Market Metrics:

- Spot price premiums over futures contracts

- Shipping route utilisation rates and transit times

- Regional price differentials indicating supply constraints

- Inventory levels at strategic locations

Policy Response Indicators:

- Strategic reserve deployment rates and volumes

- Alternative supply activation success rates

- International cooperation agreement implementation

- Emergency sharing protocol utilisation

Current market signals suggest significant underpricing of supply risks. Physical oil markets trade approximately $25 per barrel above paper markets, indicating supply constraints not reflected in futures pricing.

Financial Market Transmission

Crisis escalation typically manifests through multiple financial market channels:

- Currency volatility in energy-importing nations

- Government bond yield movements reflecting fiscal pressures

- Equity market rotation toward energy and commodity sectors

- Credit market stress in energy-intensive industries

These financial indicators often provide early warning signals for economic deterioration before real economy impacts become apparent.

Understanding the complex interplay between geopolitical tensions and global commodity markets requires analysing multiple interconnected systems. The US-Iran war impact on Strait of Hormuz extends far beyond immediate energy price effects, potentially triggering worldwide recession, accelerating energy transition, and reshaping international economic relationships. Successful navigation demands diversified supply chains, flexible policy frameworks, and strategic positioning in alternative energy systems.

Investment Disclaimer: This analysis contains forward-looking statements and market projections subject to significant uncertainties. Commodity investments carry substantial risks including price volatility, geopolitical factors, and regulatory changes. Readers should conduct independent research and consult qualified financial advisers before making investment decisions based on this information.

Ready to Capitalise on Critical Commodity Market Disruptions?

As geopolitical tensions reshape global energy markets and create unprecedented opportunities in critical commodities, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, helping subscribers identify actionable opportunities ahead of broader market movements. Begin your 14-day free trial today to position yourself strategically whilst understanding why major mineral discoveries can generate substantial returns during periods of supply chain disruption.