August 2, 2026

The US-Japan critical minerals action plan represents a pivotal response to growing supply chain vulnerabilities in an increasingly fragmented global economy. Critical minerals supply chains face unprecedented strategic challenges as nations reassess their resource dependencies in an era of heightened geopolitical tensions. Furthermore, the global economy's reliance on concentrated sources for essential materials has created vulnerabilities that traditional trade frameworks struggle to address. These supply chain fragilities become particularly acute when examining battery metals, rare earth elements, and processing capabilities that underpin modern industrial infrastructure.

Strategic Framework Analysis

Multi-scenario planning reveals three distinct pathways for critical minerals security: accelerated decoupling from dominant suppliers, selective diversification across multiple sources, and integrated resilience models that combine domestic capacity with trusted partner networks. Each approach carries distinct risk profiles and investment requirements that shape long-term strategic positioning.

Multi-Scenario Supply Chain Architecture

Risk probability matrices demonstrate that supply disruption scenarios vary significantly across mineral categories. Rare earth elements present the highest vulnerability coefficients, with current market concentration creating single-point-of-failure risks across multiple industrial sectors. Lithium supply chains exhibit moderate diversification potential through expanded processing capabilities, while cobalt markets face geographic concentration challenges that limit near-term alternatives.

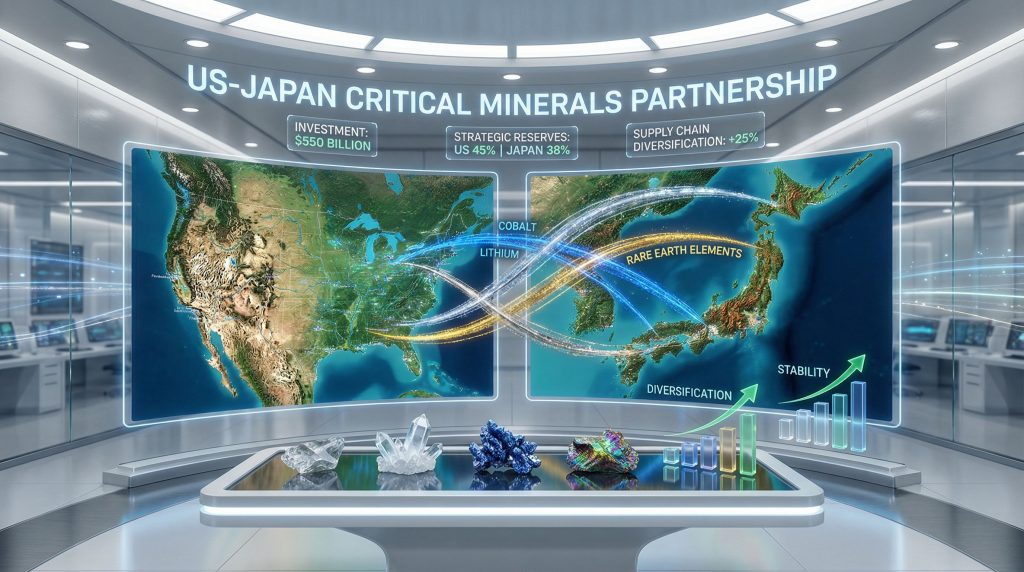

The US-Japan critical minerals action plan addresses these vulnerabilities through bilateral coordination mechanisms designed to reduce dependencies on constrained global sources. Recent analysis indicates that strategic partnerships focusing on trusted supply chains can achieve 25-40% risk reduction across critical mineral categories within a 5-7 year implementation timeline.

Investment threshold analysis suggests that commercially viable operations require initial capital commitments ranging from $2-5 billion for processing facilities to $8-12 billion for integrated mining-to-market operations. These figures reflect the scale necessary to achieve meaningful supply chain impact rather than marginal capacity additions.

Deep-Sea Mining as Strategic Game-Changer

Seabed rare earth extraction near Japan's Minamitorishima Island represents a paradigm shift in supply geography. Technical feasibility assessments indicate that rare-earth mud deposits contain significantly higher concentrations than many terrestrial sources, with preliminary studies suggesting extraction yields that could support large-scale industrial applications. However, deep‐sea mining concerns continue to influence regulatory frameworks and public acceptance.

Environmental regulatory frameworks for oceanic mining operations require coordination across multiple jurisdictions, including Japanese territorial waters, international maritime zones, and bilateral environmental standards. Processing costs for seabed-extracted materials typically exceed terrestrial alternatives by 40-60% initially, though economies of scale and technological improvements could narrow this gap substantially.

The memorandum of cooperation between both nations specifically targets joint research and development for commercially viable deep-sea mineral extraction technologies. This approach addresses the $15-25 billion investment requirement for developing comprehensive seabed mining capabilities from exploration through processing.

When big ASX news breaks, our subscribers know first

What Makes This Partnership Different from Previous Critical Minerals Agreements?

Institutional Innovation Framework

Comparative analysis with existing partnerships reveals distinct architectural differences in the US-Japan approach. Unlike voluntary coordination frameworks, this initiative incorporates binding commitments supported by price stabilisation mechanisms and trade policy coordination.

| Partnership | Investment Scale | Enforcement Mechanism | Geographic Focus | Timeline |

|---|---|---|---|---|

| US-Australia Critical Minerals | $4.6 billion | Voluntary coordination | Australia, US | 5 years |

| EU-Canada Agreement | €7.2 billion | Trade preferences | Canada, EU | 3 years |

| US-Japan Action Plan | $50+ billion regional | Binding commitments | Indo-Pacific | Long-term |

The framework establishes ministerial coordination mechanisms that enable rapid response to supply disruptions, contrasting with slower multilateral consultation processes typical of broader alliance structures. This institutional design prioritises operational efficiency over consensus-building procedures that can delay crisis responses.

Financial Architecture and Investment Flows

Investment flow analysis indicates the partnership leverages both public and private capital across multiple sectors. The Indo-Pacific Energy Security Ministerial and Business Forum identified more than $50 billion in projects and investments across the region, providing context for the bilateral initiative's scale and ambition.

Consequently, trade policy measures include strategic tariff structures and border mechanisms designed to protect downstream industries from supply manipulation. These mechanisms create cost-predictability frameworks that enable long-term industrial planning despite volatile global commodity markets.

Risk-adjusted return calculations for critical minerals infrastructure projects typically require 7-12% internal rates of return to attract private capital, necessitating government risk-sharing mechanisms or strategic investment incentives to achieve commercial viability.

Which Critical Minerals Will Drive the Partnership's Success?

Priority Minerals Matrix

Strategic importance rankings prioritise rare earth elements, lithium, cobalt, and specialty metals essential to advanced manufacturing and energy transition technologies. The importance of critical minerals energy security cannot be overstated in this context. Current supply vulnerability assessments reveal:

• Rare Earth Elements: 85% processing concentration in single-source markets

• Lithium: 60% production from three countries, processing concentration higher

• Cobalt: 70% mining concentration, limited alternative sources

• Nickel: Moderate diversification, processing constraints remain

• Manganese: Geographic distribution favourable, processing gaps exist

Market concentration risk analysis demonstrates that China's processing dominance creates strategic vulnerabilities across multiple mineral categories simultaneously. The partnership specifically targets these processing bottlenecks through joint facility development and technology sharing agreements.

Geographic Distribution Strategy

Existing US and Japanese mining assets provide foundation capabilities that require significant expansion to achieve strategic impact. Japan's advanced materials processing expertise combined with US mineral resources and technological innovation creates complementary capability sets that enhance partnership effectiveness.

Third-country partnership opportunities with Australia, Canada, and Chile offer geographic diversification benefits while maintaining democratic governance and environmental standards alignment. Transportation and logistics optimisation between partner nations reduces supply chain vulnerabilities compared to single-source dependencies.

Processing capacity analysis indicates that joint facilities located strategically between major consumption centres could reduce transportation costs by 20-35% while improving supply chain resilience through redundant processing capabilities.

How Will China Respond to This Strategic Realignment?

Competitive Response Scenarios

Market intelligence suggests several potential Chinese countermeasures ranging from price manipulation to alternative partnership formation. Export restriction scenarios could temporarily disrupt markets but would accelerate alternative supplier development and technology innovation.

Chinese processing capacity advantages stem from 15-20 year investment cycles in refining infrastructure and technology development. Competitive responses might focus on maintaining cost advantages through economies of scale rather than direct market manipulation that could trigger retaliatory measures.

Alternative partnership formations with Russia, African mineral producers, and ASEAN nations represent potential Chinese strategies for maintaining global market influence. These arrangements could create competing supply chain networks that fragment global markets along geopolitical lines.

Market Share Redistribution Projections

Quantitative modelling suggests 5-10 year horizons are necessary for meaningful supply chain shifts given the capital intensity and regulatory timelines involved in mining and processing facility development. Market share redistribution typically occurs gradually through capacity additions rather than dramatic shifts in existing operations.

Price volatility during transition periods could range from 20-40% above historical averages as markets adjust to new supply configurations and increased competition for alternative sources. Technology innovation acceleration under competitive pressure historically reduces costs by 3-7% annually once commercial operations achieve scale.

What Are the Implementation Challenges and Success Metrics?

Regulatory and Permitting Streamlining

Environmental approval processes present significant timeline challenges, with US permitting requirements typically requiring 2-5 years for mining projects and Japanese regulations adding comparable timeframes for seabed operations. Regulatory harmonisation between both nations could reduce combined approval timelines by 25-40% through coordinated review processes.

Cross-border regulatory frameworks must address environmental standards, worker safety requirements, and international maritime law considerations for deep-sea mining operations. Streamlined approval mechanisms require legislative coordination and bilateral regulatory cooperation agreements.

Technology Transfer and Innovation Acceleration

Joint research and development initiatives focus on mineral processing efficiency, recycling technology advancement, and extraction method innovation. Intellectual property frameworks must balance commercial interests with strategic cooperation objectives whilst encouraging private sector participation.

University and research institution collaboration structures provide foundation for long-term technological advancement beyond immediate commercial requirements. Innovation acceleration metrics should track patent development, technology commercialisation timelines, and cost reduction achievements across key mineral processing categories.

How Does This Partnership Fit Into Broader Indo-Pacific Strategy?

Alliance Network Integration

Coordination mechanisms with QUAD partners create opportunities for expanded cooperation across Australia, India, and existing bilateral relationships. AUKUS technology sharing implications for critical minerals include advanced materials development and manufacturing process innovation that supports defence technology requirements.

For instance, partnerships like the Australia critical reserve and India's lithium strategy demonstrate how regional cooperation can strengthen overall supply chain resilience.

Indo-Pacific Economic Framework initiatives provide multilateral coordination platforms that could expand bilateral agreements into regional frameworks. Supply chain resilience objectives align with broader strategic competition dynamics and democratic alliance strengthening goals.

Long-term Strategic Positioning

2030-2040 supply chain resilience scenarios depend heavily on technological breakthrough achievements and competitive responses from alternative suppliers. Partnership expansion potential to European allies, North American partners, and democratic mineral-producing nations could create comprehensive alternative supply networks.

Economic security integration with traditional defence cooperation reflects recognition that resource dependencies constitute national security vulnerabilities equivalent to conventional military threats in their potential impact on industrial capacity and economic resilience.

The next major ASX story will hit our subscribers first

Investment and Market Implications

Sector-Specific Impact Analysis

Electric vehicle supply chain transformation projections indicate that secure critical minerals access could accelerate domestic manufacturing competitiveness and reduce foreign dependency risks. Battery manufacturing facilities require consistent mineral inputs with predictable pricing to achieve commercial viability.

Renewable energy infrastructure development depends on reliable access to specialty metals for wind turbines, solar panels, and grid storage systems. Partnership arrangements could reduce project development risks and improve financing availability for clean energy initiatives.

Advanced manufacturing competitiveness enhancement through secure supply chains enables long-term industrial planning and capacity expansion decisions. Supply chain predictability reduces operational risks and supports private sector investment in manufacturing expansion.

Risk-Adjusted Investment Opportunities

Mining company positioning for partnership benefits requires strategic assessment of reserves, processing capabilities, and geographic advantages. Companies with existing operations in partner nations or third-country alliance members may capture preferential access to partnership benefits and investment opportunities.

Processing and refining capacity expansion requirements present significant capital investment opportunities, particularly for joint venture arrangements between partner nation companies. Technology development contracts and facility construction projects offer multiple investment entry points across the value chain.

Recycling technology investment potential increases as partnerships emphasise circular economy approaches to critical minerals management. Advanced recycling capabilities could reduce primary extraction requirements whilst maintaining industrial supply adequacy.

Measuring Success: Key Performance Indicators

Quantitative Success Metrics

Supply chain diversification percentages should track progress toward reducing single-source dependencies below 50% for priority minerals within the partnership timeframe. Cost competitiveness benchmarks must demonstrate that alternative sources achieve price parity with existing suppliers within acceptable timeframes.

Timeline achievements for major mining and processing project completions provide concrete measures of implementation progress. Operational facility counts and production capacity additions offer quantifiable evidence of partnership effectiveness.

Strategic Resilience Indicators

Crisis response capability testing through scenario exercises and market disruption simulations validates partnership operational effectiveness. Market stability maintenance during supply disruption scenarios demonstrates the partnership's practical value for industrial security.

Innovation output measurements should track patent applications, technology commercialisation successes, and cost reduction achievements across critical mineral processing technologies. Research collaboration productivity indicates long-term partnership sustainability and technological advancement potential.

Partnership success ultimately depends on achieving measurable supply chain resilience improvements whilst maintaining economic competitiveness and environmental responsibility standards. These objectives require sustained coordination across government agencies, private sector participants, and international partners over multi-year implementation cycles.

The US-Japan critical minerals action plan represents a significant evolution in strategic resource management, combining bilateral cooperation with broader alliance integration to address fundamental supply chain vulnerabilities in the global economy. Success will be measured not only in production volumes and market shares, but in the partnership's ability to demonstrate that democratic nations can create reliable, sustainable alternatives to concentrated supply chains that have become sources of strategic vulnerability rather than economic efficiency.

Ready to Capitalise on Critical Minerals Investment Opportunities?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, including critical minerals and rare earth elements that are becoming increasingly strategic in global supply chains. With major partnerships like the US-Japan critical minerals action plan reshaping the sector, subscribers gain immediate access to actionable investment opportunities that could benefit from these strategic developments, ensuring informed decisions ahead of broader market recognition.