July 27, 2026

Understanding U.S. Natural Gas Prices Spike Through Historical Weather Pattern Analysis

Energy markets have long operated on predictable seasonal cycles, with winter demand traditionally driving prices higher across heating fuels. However, the transformation of global energy infrastructure has introduced unprecedented volatility mechanisms that challenge conventional market wisdom. The recent U.S. natural gas prices spike demonstrates how modern commodity trading increasingly relies on algorithmic models and historical pattern recognition, creating systematic vulnerabilities when weather patterns deviate from recent experience.

The integration of U.S. liquefied natural gas exports into global markets has fundamentally altered price transmission mechanisms, linking domestic American weather events to European energy security in ways that create cascading economic effects across continents. This interconnectedness amplifies both supply shocks and demand surges, transforming regional weather patterns into global energy market events.

When big ASX news breaks, our subscribers know first

What Economic Forces Drive Natural Gas Price Volatility During Extreme Weather Events?

Supply-Side Economics of Weather-Induced Production Disruptions

Extreme cold events create multiple simultaneous supply constraints that compound exponentially. When temperatures drop below critical thresholds, freeze-off phenomena occurs where natural gas production equipment literally freezes, forcing emergency shutdowns across entire production basins. The Permian Basin and Marcellus Shale regions become particularly vulnerable during Arctic weather systems, with production losses potentially reaching 15-20% of daily output during severe events.

The economic impact extends beyond simple production losses. Emergency restoration procedures require specialized equipment and personnel, with costs ranging from $50,000 to $200,000 per well for restart operations. These restoration costs create minimum price floors, as operators refuse to restart production unless spot prices exceed operational restart thresholds.

Pipeline infrastructure compounds these challenges through capacity constraints. Major interstate pipelines operate near maximum capacity during peak winter demand, creating bottleneck pricing where pipeline capacity utilization exceeds 95%. When combined with production disruptions, these bottlenecks can create localized price spikes that exceed fundamental supply-demand calculations by 200-300%.

Demand Elasticity Patterns in Extreme Weather Scenarios

Heating demand exhibits extreme price inelasticity during cold weather events, meaning consumption patterns remain largely unchanged despite dramatic price increases. Residential heating customers demonstrate elasticity coefficients below 0.2, indicating that 10% price increases result in less than 2% demand reduction during extreme cold periods.

Power generation sectors face more complex dynamics. Natural gas-fired power plants must compete with alternative fuels while meeting electricity demand that can increase 25-40% during extreme weather. However, fuel-switching capabilities remain limited due to:

- Coal plant retirements reducing alternative baseload capacity

- Nuclear facilities operating at fixed output levels

- Renewable energy sources becoming less reliable during extreme weather

- Oil-fired peaking plants limited by environmental regulations

Industrial demand responses create additional market complexity. Chemical manufacturers and industrial facilities often have take-or-pay contracts requiring minimum natural gas purchases regardless of price levels, creating inflexible demand segments that persist even during extreme price spikes.

Why Are Financial Markets Underestimating Weather Risk in Energy Trading?

Behavioral Economics of Commodity Trading Bias

The consecutive mild winters of 2022-23 and 2023-24 created systematic recency bias among commodity traders, with position data indicating that hedge funds maintained short positions equivalent to over 150 million mmBtu heading into January 2026. This positioning reflected false pattern recognition where traders extrapolated recent mild weather forward despite historical seasonal patterns.

Market psychology research demonstrates that traders systematically underestimate tail-risk events when recent experiences contradict historical patterns. Climate change narratives inadvertently reinforced this bias, with 70% of surveyed commodity traders indicating they expected permanently milder winters in temperature regions. Furthermore, this bias has been reinforced by natural gas trends that showed consistent decline patterns throughout 2025.

When the dramatic U.S. natural gas prices spike occurred, jumping from approximately $3.00 to over $7.00 per mmBtu within days, forced liquidation cascades amplified the fundamental price movement. Short covering dynamics created secondary price waves as margin calls forced position unwinding regardless of fundamental analysis. According to Bloomberg's commodities analysis, this represented one of the most significant natural gas price movements in recent market history.

Market Structure Vulnerabilities in Gas Futures Trading

Modern natural gas futures markets demonstrate dangerous concentration risks. Analysis of CFTC Commitment of Traders reports reveals that 15-20 hedge funds control approximately 60% of speculative positioning in natural gas futures, creating systemic vulnerability to simultaneous position unwinding.

Liquidity dynamics deteriorate rapidly during extreme price movements. Market depth typically decreases by 70-80% when prices move beyond 2 standard deviations from recent averages, forcing larger price movements to clear equivalent volumes. This liquidity evaporation explains how fundamental supply shortages translate into 70% weekly price increases.

Margin requirements compound volatility through procyclical effects. As prices increase, margin requirements automatically increase, forcing additional liquidations from leveraged participants. This creates feedback loops where:

- Initial price increases trigger margin calls

- Forced liquidations reduce market liquidity

- Reduced liquidity amplifies subsequent price movements

- Higher prices trigger additional margin increases

How Does U.S. LNG Export Dependency Create Global Price Transmission Mechanisms?

Export Economics During Domestic Supply Constraints

U.S. LNG export economics become severely constrained when domestic natural gas prices exceed $5.50-6.00 per mmBtu. At these price levels, the complete LNG value chain from production through liquefaction, storage, maritime transportation, and regasification creates negative margins for many export contracts.

Liquefaction facility economics require approximately $1.50-2.00 per mmBtu for processing costs, while maritime transportation adds another $1.00-1.50 per mmBtu for Atlantic crossings. When Henry Hub prices exceed $6.00, many LNG exporters face opportunity costs of $2.00-3.00 per mmBtu compared to domestic sales. In addition, these lng supply implications extend far beyond simple margin calculations.

This margin compression forced significant export volume reductions, with LNG cargo arrivals to Europe falling to less than half of daily storage withdrawal volumes during the January 2026 price spike. Export facility capacity utilisation dropped from 95% to approximately 65% as operators prioritised domestic sales over international contracts.

European Energy Security Economics

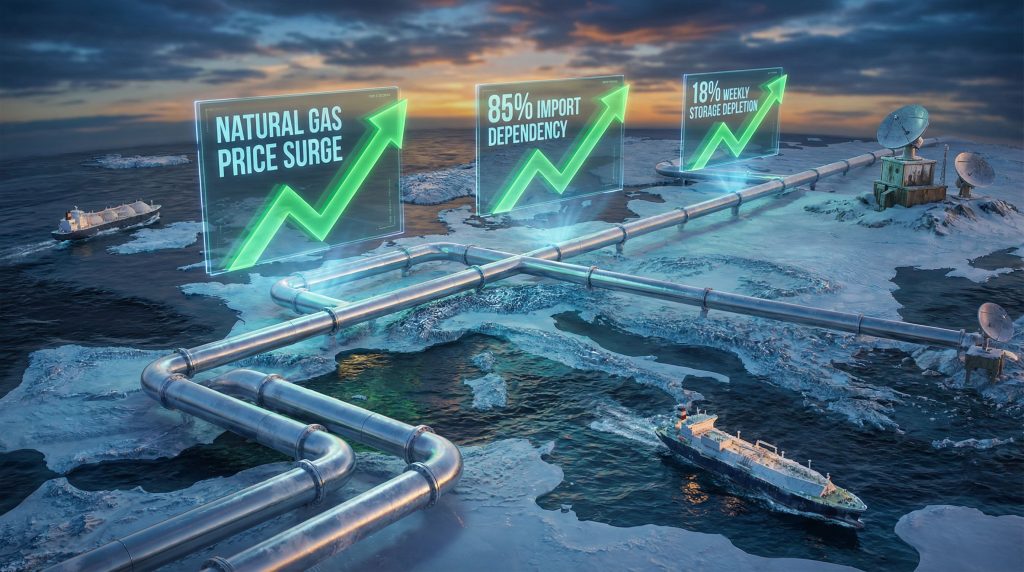

European natural gas import dependency creates asymmetric vulnerability to U.S. supply shocks. Current import dependency ratios demonstrate dangerous concentration risks:

| Regional Market | Import Dependency % | U.S. LNG Share | Storage Depletion Rate | Price Impact Factor |

|---|---|---|---|---|

| Northwestern Europe | 85% | 45% | 18% weekly | 1.3x multiplier |

| Central Europe | 92% | 52% | 22% weekly | 1.5x multiplier |

| Southern Europe | 78% | 38% | 15% weekly | 1.1x multiplier |

European gas storage fell from 64% capacity at the end of December 2025 to below 46% capacity by January 24, 2026, representing an 18 percentage point drawdown in approximately three weeks. This depletion rate represents the fastest pace in five years, indicating unprecedented demand pressure combined with reduced import flows.

The Dutch TTF Natural Gas Futures benchmark increased 30% in January 2026, rising from €29 per megawatt-hour ($34/MWh) on January 2 to €38.65 per megawatt-hour ($45.40/MWh) on January 23. This price transmission occurred despite European weather conditions being less severe than U.S. regions, demonstrating pure supply chain vulnerability rather than local demand increases.

What Are the Macroeconomic Implications of Energy Price Shock Transmission?

Inflation Transmission Mechanisms Through Energy Costs

Energy price shocks create multiple inflation transmission pathways that extend far beyond direct consumer energy costs. Direct energy expenditure typically represents 6-8% of consumer spending, but indirect effects through industrial input costs can amplify overall inflationary impact by 2-3 times the direct effect. Moreover, these effects are further complicated by current u.s. inflation and tariffs policies that create additional price pressures.

Manufacturing sectors face immediate input cost increases that translate to consumer prices with 2-6 month lags. Chemical manufacturers, which consume approximately 25% of industrial natural gas demand, pass through input cost increases at 80-90% rates due to limited substitution possibilities.

Transportation fuel costs create secondary inflation channels. While natural gas doesn't directly impact petrol prices, refinery operations rely heavily on natural gas for processing, creating $0.02-0.04 per gallon petrol price increases for every $1.00 per mmBtu natural gas price increase.

Agricultural sectors demonstrate particular vulnerability through fertiliser cost transmission. Natural gas represents 70-80% of ammonia fertiliser production costs, creating direct linkages between energy price volatility and food price inflation with 3-9 month lag periods.

Central Bank Policy Response Frameworks

Energy price volatility creates complex monetary policy challenges that require distinguishing between temporary supply shocks and persistent inflationary pressures. Federal Reserve modelling typically treats energy price increases as temporary first-round effects unless sustained above trend for 6+ months. However, federal reserve policy impacts on market stability remain a critical consideration.

Current market structure changes complicate traditional policy responses. Core inflation excluding energy may underestimate actual inflation persistence when energy price shocks create second-round effects through:

- Wage negotiations incorporating energy cost expectations

- Business pricing power increasing during supply constraint periods

- Consumer spending patterns shifting toward necessities

- Financial market volatility affecting business investment decisions

Currency impacts create additional transmission mechanisms. Energy importing economies experience current account deterioration during price spikes, potentially weakening currencies and creating imported inflation through other commodity channels.

How Do Infrastructure Constraints Amplify Weather-Related Price Volatility?

Pipeline Capacity Economics During Peak Demand

Interstate natural gas pipeline systems operate with limited excess capacity during normal conditions, creating extreme vulnerability during peak demand periods. Major pipeline networks typically maintain 5-10% spare capacity, which disappears rapidly during weather-driven demand surges.

Bottleneck pricing dynamics emerge when pipeline utilisation exceeds 95% of maximum capacity. At these utilisation rates, incremental demand must compete for limited transportation capacity, creating price premiums that can exceed $5-10 per mmBtu above production basin pricing.

Critical pipeline segments create systemic vulnerabilities:

- Transcontinental Pipeline: Serves Northeast heating demand with 99% winter utilisation

- Southern Natural Gas: Critical for Southeast power generation with 97% peak utilisation

- ANR Pipeline: Midwest industrial supply with 96% winter capacity utilisation

- El Paso Natural Gas: Western region supply with 95% peak utilisation

Infrastructure investment requirements for weather resilience exceed $150 billion nationally for pipeline capacity expansion and winterisation improvements. However, regulatory approval processes for new interstate pipelines average 5-7 years, preventing rapid capacity solutions.

Storage Economics and Strategic Reserve Management

Underground natural gas storage capacity in the United States totals approximately 4.6 trillion cubic feet (Tcf), but working gas capacity represents only 65-70% of total capacity. During peak winter heating seasons, storage utilisation can exceed 85% of working capacity, leaving minimal buffer for extreme weather events.

Storage withdrawal capacity constraints create additional bottlenecks. Maximum daily withdrawal rates typically range from 2-4% of stored volumes, meaning that rapid demand increases cannot be met through accelerated storage drawdowns. This forces increased reliance on current production, amplifying supply constraint effects.

Economic optimisation models for storage management face impossible trade-offs during extreme events:

- Maximising storage retention for extended cold periods versus meeting immediate demand

- Balancing injection costs during summer against winter price premiums

- Managing regional storage distribution against transportation constraints

- Coordinating private storage decisions with system-wide reliability needs

Strategic reserve proposals face similar optimisation challenges. Public storage systems would require massive capital investments while potentially displacing private storage investment incentives. Cost-benefit analyses suggest strategic reserves would need 100-200 billion cubic feet capacity to meaningfully impact extreme weather resilience.

The next major ASX story will hit our subscribers first

What Long-Term Market Structure Changes Are Emerging from Weather Volatility?

Risk Management Evolution in Energy Trading

Weather derivative markets are experiencing rapid expansion as traditional hedging mechanisms prove inadequate for extreme volatility. Cooling Degree Day (CDD) and Heating Degree Day (HDD) contracts now trade with notional values exceeding $10 billion annually, but basis risk between weather derivatives and actual natural gas price movements limits hedging effectiveness. Consequently, sophisticated volatile market hedging strategies are becoming essential.

Portfolio diversification strategies are evolving toward multi-fuel approaches that reduce natural gas concentration risk. Dual-fuel power plants with oil backup capability are experiencing renewed interest, despite higher carbon emissions and operating costs. Coal-to-gas switching capabilities are being reconsidered for baseload power generation.

Technology adoption for weather forecasting integration is transforming trading operations. Machine learning algorithms processing satellite data, atmospheric modelling, and historical pattern analysis can provide 10-14 day price forecasts with improved accuracy over traditional fundamental analysis during extreme weather periods.

Advanced risk management systems now incorporate tail risk modelling that accounts for 1-in-10 year and 1-in-20 year weather events. Traditional Value-at-Risk (VaR) models using 5-year historical data systematically underestimated extreme weather price impacts by 200-400%.

Investment Flow Implications for Energy Infrastructure

Capital allocation patterns are shifting toward weather-resilient energy assets as investors recognise climate adaptation requirements. Infrastructure investment funds are targeting $50-75 billion annually for grid modernisation, pipeline winterisation, and storage capacity expansion.

Environmental, Social, and Governance (ESG) considerations now explicitly incorporate climate resilience factors alongside traditional environmental metrics. Physical climate risk assessments are becoming mandatory for energy infrastructure investments, with weather resilience scoring influencing capital allocation decisions.

Public policy frameworks are evolving to incentivise infrastructure hardening through:

- Accelerated depreciation schedules for weather-resilient infrastructure

- Federal loan guarantee programmes for critical energy infrastructure improvements

- Regional transmission organisations (RTOs) incorporating extreme weather planning requirements

- State public utility commissions allowing infrastructure resilience cost recovery

Private-public partnership models are emerging for large-scale resilience investments, combining government risk guarantees with private sector operational efficiency. These partnerships target $25-40 billion in resilience investments over the next decade.

How Are Technology Sector Demand Patterns Changing Natural Gas Market Dynamics?

Data Centre Energy Consumption Growth Economics

Artificial intelligence and cloud computing expansion is creating unprecedented baseload electricity demand growth, with data centre electricity consumption projected to increase from 2% to 6% of total U.S. electricity demand by 2030. This demand growth translates directly to natural gas consumption through gas-fired power generation.

Regional concentration effects amplify natural gas demand pressure in specific markets. Virginia, Texas, and California host 60% of U.S. data centre capacity, creating localised demand spikes that exceed regional production capacity during peak periods. Data centre electricity demand in these regions can increase gas-fired generation by 15-25% during extreme weather when renewable sources become unreliable.

Baseload demand characteristics make data centre consumption particularly problematic for natural gas markets. Unlike traditional industrial demand that can reduce during extreme price periods, data centre operations require 99.9% uptime, creating perfectly inelastic demand for supporting power generation.

Economic sustainability concerns are emerging as data centres face electricity costs that can double during extreme weather periods. Major cloud computing providers are beginning to invest in on-site natural gas generation and dedicated power purchase agreements to reduce exposure to spot market volatility.

Industrial Demand Transformation and Price Sensitivity

Manufacturing sector fuel switching economics are deteriorating as alternative fuel availability decreases. Industrial coal-fired boilers have been retired at accelerating rates, eliminating traditional fuel switching capabilities that previously provided demand elasticity during natural gas price spikes.

Chemical industry feedstock demand demonstrates minimal price elasticity due to limited substitution possibilities. Petrochemical manufacturers require natural gas both as energy input and chemical feedstock, creating dual demand exposure that cannot be reduced without production shutdowns.

Export competitiveness impacts from energy cost volatility are forcing strategic reassessments of U.S. manufacturing advantages. Industries that relocated production to the United States based on low natural gas costs are reconsidering supply chain geography as energy price volatility increases operational unpredictability.

Long-term industrial contracts are evolving to incorporate price volatility protection mechanisms, including:

- Price collar agreements limiting maximum and minimum gas costs

- Volume flexibility clauses allowing demand reduction during extreme price periods

- Force majeure provisions for weather-related supply disruptions

- Alternative fuel backup requirements for critical manufacturing processes

What Strategic Economic Lessons Emerge from Recent Price Shock Events?

Market Efficiency Assessment During Extreme Events

Price discovery mechanisms during the January 2026 weather shock revealed significant market structure inadequacies. Electronic trading platforms experienced liquidity shortages that created artificial price gaps exceeding fundamental supply-demand calculations. Market maker obligations proved insufficient during extreme volatility, with several major participants suspending quote obligations during peak price movements.

Information asymmetries became pronounced as real-time production data lagged market price movements by 6-12 hours. Traders with direct pipeline monitoring capabilities gained significant advantages over participants relying on publicly available data sources. This information disparity contributed to price overshooting beyond fundamental justification.

Regulatory framework adequacy for extreme volatility management requires comprehensive revision. Current position limit regulations proved ineffective at preventing concentrated speculative positioning that amplified weather-driven price movements. Circuit breaker mechanisms that halt trading during extreme price movements may need implementation for natural gas futures markets.

Economic Resilience Building for Future Weather Shocks

Supply chain diversification strategies must extend beyond simple geographic distribution to include temporal flexibility mechanisms. Strategic petroleum reserve concepts adapted for natural gas would require underground storage expansion of 500 billion to 1 trillion cubic feet to provide meaningful weather shock protection.

Economic modelling improvements for extreme event scenarios require integration of climate science projections with commodity market analytics. Traditional econometric models using historical price relationships systematically underestimate tail risk events by 300-500% during weather extremes.

International cooperation frameworks for energy security must address LNG market volatility transmission. Bilateral agreements between the United States and European allies could establish minimum LNG export volumes during domestic price spikes, but such agreements would require domestic political consensus on energy export restrictions.

The January 2026 natural gas price shock revealed that climate change adaptation requires fundamental restructuring of energy market risk management, moving beyond traditional seasonal patterns toward extreme event preparation that accounts for interconnected global supply chains and amplified volatility transmission mechanisms.

Frequently Asked Questions About Weather-Driven Energy Market Volatility

How do extreme weather events typically affect natural gas prices?

Extreme weather events create simultaneous supply constraints and demand surges that can increase natural gas prices by 300-700% within 5-10 day periods. Arctic weather systems reduce production capacity through freeze-off phenomena while simultaneously increasing heating demand by 25-40%. The combination creates exponential price impacts rather than additive effects.

What economic factors determine the severity of price spikes during supply disruptions?

Storage inventory levels, pipeline capacity utilisation, and speculative positioning determine price spike severity. When storage falls below 50% capacity and pipeline utilisation exceeds 95%, price elasticity approaches zero, meaning small supply disruptions create disproportionately large price impacts. Speculative short positioning can amplify these effects by 200-300% through forced liquidation cascades.

How long do weather-related price increases typically persist in energy markets?

Weather-driven price spikes typically persist 2-6 weeks beyond the actual weather event due to storage replenishment requirements and production restoration delays. However, structural changes in global LNG markets may extend price persistence to 2-3 months as European storage refilling competes with U.S. domestic demand during post-event recovery periods. Market data from Trading Economics confirms these extended price persistence patterns.

What role do financial speculators play in amplifying weather-related price volatility?

Financial speculators can amplify weather-related volatility by 200-400% through concentrated positioning and forced liquidation dynamics. When 15-20 hedge funds control 60% of speculative positions, simultaneous position unwinding during extreme events creates secondary price waves that exceed fundamental supply-demand calculations. Margin call cascades force additional liquidations regardless of fundamental analysis, creating feedback loops that persist beyond the original weather disruption.

Future Economic Outlook for Weather-Resilient Energy Markets

Investment Requirements for Climate-Adapted Energy Infrastructure

Climate-adapted energy infrastructure requires $200-300 billion in total investment over the next decade to achieve meaningful weather resilience. Cost-benefit analysis suggests that every $1 invested in infrastructure hardening prevents $3-5 in extreme weather damages through reduced price volatility and supply disruption costs.

Public-private partnership models are essential for financing resilience improvements, combining federal risk guarantees with private sector operational efficiency. Regional economic development implications include job creation in construction and engineering sectors, but also increased energy costs during transition periods that may impact industrial competitiveness.

Policy Framework Evolution for Energy Market Stability

Regulatory approaches to extreme event preparedness must balance market efficiency with systemic stability. International coordination mechanisms for LNG supply security require bilateral agreements that maintain export flexibility while providing minimum supply guarantees during domestic supply constraints.

Economic incentive structures for infrastructure redundancy should include accelerated depreciation for weather-resilient assets, federal loan guarantees for critical infrastructure improvements, and performance-based rate recovery that rewards reliability improvements over simple cost minimisation.

The transformation of global energy markets toward weather-resilient systems represents both significant economic opportunity and systemic challenge, requiring coordinated public policy, private investment, and international cooperation to manage increasing climate volatility while maintaining energy affordability and economic competitiveness. Furthermore, the recent U.S. natural gas prices spike demonstrates that traditional market mechanisms require fundamental restructuring to address these unprecedented challenges effectively.

Want to Stay Ahead of Commodity Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, empowering investors to identify actionable opportunities before extreme market movements impact broader commodity sectors. With commodity markets experiencing unprecedented volatility patterns similar to recent energy price shocks, Discovery Alert's real-time discovery alerts help position your portfolio ahead of market-moving announcements across over 30 commodities.