July 12, 2026

US Navy Blockade Operations: Global Energy Market Implications

Global energy markets operate within an intricate web of vulnerabilities, where single points of failure can trigger cascading economic disruptions across continents. Modern industrial civilisation's dependence on petroleum-based energy systems creates systemic risks that extend far beyond regional conflicts, particularly when considering scenarios involving a US Navy blockade Strait of Hormuz operation. These risks potentially reshape international trade patterns, monetary policies, and technological adoption timelines.

When big ASX news breaks, our subscribers know first

Critical Maritime Energy Corridors and Global Vulnerability

The world's energy security hinges on several narrow waterways that facilitate the movement of petroleum products between producing regions and consuming markets. These maritime chokepoints represent fundamental structural weaknesses in the global energy system, where disruptions can rapidly escalate into worldwide economic crises.

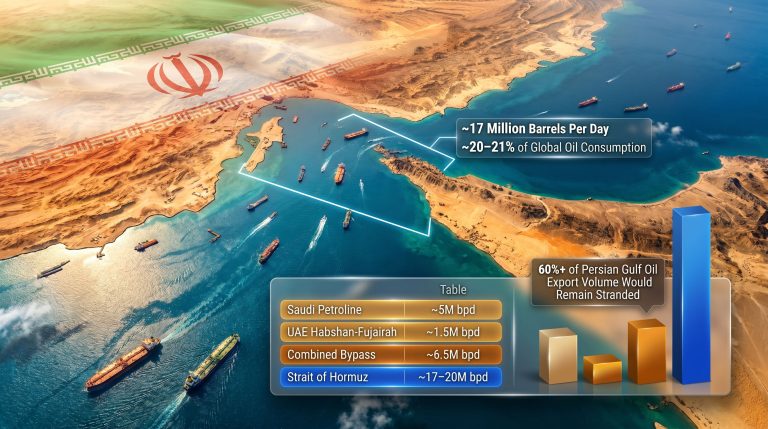

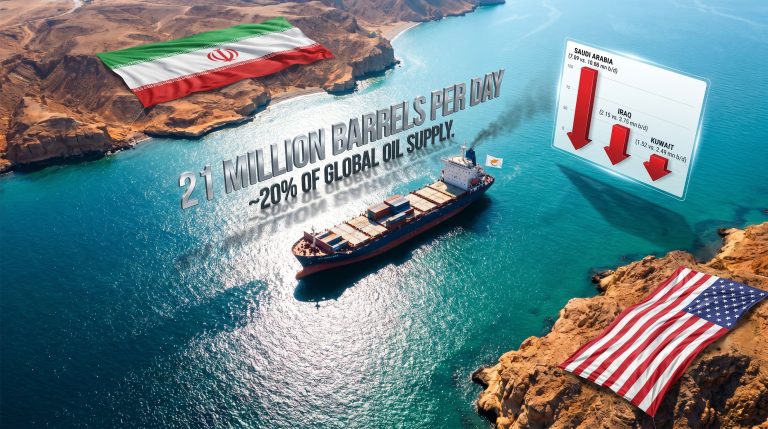

The Strait of Hormuz stands as the most strategically significant of these passages, facilitating approximately 21% of global petroleum liquids movement according to the U.S. Energy Information Administration. This narrow waterway, spanning just 21 miles at its narrowest point, connects the Persian Gulf to the Gulf of Oman and serves as the primary export route for major oil-producing nations including Saudi Arabia, Iraq, UAE, and Kuwait.

Key Strategic Dependencies:

- Daily throughput: Approximately 20-21 million barrels per day transit this corridor

- Regional concentration: The Persian Gulf contains roughly 48% of the world's proven crude oil reserves

- Export vulnerability: Saudi Arabia alone exports 7-8 million barrels daily, predominantly through this route

- Geographic constraints: No viable maritime alternatives exist for Persian Gulf producers

The strategic importance of this corridor becomes clear when examining historical disruptions. Furthermore, any analysis of oil price rally analysis reveals how rapidly geopolitical tensions translate into market volatility. The 1973 Arab Oil Embargo reduced global supply by approximately 5%, causing oil prices to quadruple. Similarly, the 1979 Iranian Revolution disrupted 4-6 million barrels per day of production, contributing to the second major oil price shock of that decade.

Economic Impact Modelling for Naval Interdiction Scenarios

Understanding how US Navy blockade Strait of Hormuz operations might unfold requires examining multiple economic variables and market response mechanisms. Energy markets respond to both physical supply disruptions and perceived future supply risks, often pricing in disruption expectations before physical impacts materialise.

Historical Price Response Patterns:

| Historical Event | Supply Impact | Peak Price Increase | Market Recovery Time |

|---|---|---|---|

| 1973 Oil Embargo | 5% reduction | 300% price increase | 6-8 months |

| 2022 Russia-Ukraine War | 3-4 million bpd | $139/barrel peak | 4-6 months |

| 2008 Financial Crisis | Demand collapse | $147 to $30/barrel | 12 months |

A comprehensive US Navy blockade Strait of Hormuz scenario would potentially eliminate 12-15 million barrels per day from global supply chains, representing approximately 12-15% of worldwide petroleum production. This disruption magnitude would exceed the 1973 embargo impact and rival major wartime production losses.

Strategic Reserve Response Capabilities:

- United States: Strategic Petroleum Reserve capacity of 714 million barrels

- International Energy Agency: Collective emergency reserves of 1.6 billion barrels

- China: National petroleum reserves estimated at 400-500 million barrels

- Combined duration: 60-90 day coverage at normal consumption rates

Market analysts project that comprehensive naval interdiction operations would trigger immediate price responses ranging from $130-175 per barrel, depending on market perception regarding disruption duration and strategic reserve coordination effectiveness. Moreover, recent research examining OPEC price stagnation demonstrates how quickly geopolitical tensions can override traditional supply-demand fundamentals.

Transportation Sector Transformation Under Energy Price Stress

Energy price escalation fundamentally alters transportation economics across all modes, forcing rapid operational adaptations and accelerating long-term technological transitions. The transportation sector's response patterns provide insights into broader economic resilience mechanisms during energy supply disruptions.

Aviation Industry Adaptation Mechanisms

Commercial aviation faces particularly acute vulnerability to energy price shocks, as jet fuel represents 20-30% of operating costs for major carriers according to the International Air Transport Association. A US Navy blockade Strait of Hormuz scenario would trigger multiple adaptation responses:

Immediate Response Strategies (0-30 days):

- Route optimisation and fuel load reduction

- Capacity adjustments through frequency reductions rather than aircraft downsizing

- Implementation of fuel surcharges averaging 10-15% of base fares

- Enhanced fuel hedging programme utilisation

Medium-term Operational Changes (30-180 days):

- Fleet redeployment to maximise fuel-efficient aircraft utilisation

- Strategic route restructuring to minimise fuel consumption

- Accelerated maintenance schedules to optimise engine efficiency

- Partnership agreements for fuel supply diversification

The 2008 oil price spike to $147 per barrel demonstrated these response patterns, with airlines globally reducing capacity by 5-10% and several carriers filing for bankruptcy protection due to unsustainable operating costs.

Maritime Shipping Route Economics

Global shipping companies would face immediate decisions regarding route optimisation and speed management during US Navy blockade Strait of Hormuz operations. Marine fuel represents 30-50% of shipping operating costs, making energy price volatility a critical operational factor.

Alternative Route Analysis:

| Route Option | Additional Distance | Extra Transit Time | Cost Increase |

|---|---|---|---|

| Cape of Good Hope | 4,000-4,500 nautical miles | 10-15 days | 10-20% |

| Suez Canal (partial) | 2,000-3,000 nautical miles | 2-3 weeks | 8-15% |

| Trans-Siberian Rail | Land-based alternative | 14-21 days | 15-25% |

Shipping companies historically respond through "slow steaming" practices, reducing vessel speeds from 20+ knots to 12-15 knots, which can decrease fuel consumption by 20-30% according to International Maritime Organisation research. Additionally, the broader implications of such disruptions, as explored in the US‑China trade war impact analysis, demonstrate how shipping route changes affect global supply chains.

Industrial Manufacturing Sector Vulnerability Assessment

Energy-intensive manufacturing industries face compound impacts from US Navy blockade Strait of Hormuz scenarios, experiencing both higher energy costs and feedstock price escalation. These sectors demonstrate varying degrees of operational flexibility and substitution capabilities.

Petrochemical Industry Exposure

Petrochemical production represents the most vulnerable industrial sector, with energy costs comprising 60-70% of production expenses and crude-derived feedstock representing an additional 15-25% of costs according to the U.S. Department of Energy.

Impact Cascade Analysis:

- Primary impact: 30-50% increase in feedstock costs

- Secondary impact: 20-35% rise in energy expenses for processing

- Tertiary impact: Supply chain disruptions affecting downstream manufacturers

- Market response: Price pass-through to consumer goods averaging 5-15%

Steel and Aluminium Manufacturing Adjustments

Steel manufacturing faces moderate vulnerability, with energy costs representing 20-30% of total production costs. A $20 per barrel crude increase typically adds approximately 5-8% to total steel production costs according to the American Iron and Steel Institute.

Aluminium smelting demonstrates higher energy sensitivity, as electricity costs comprise 30-40% of production expenses. During energy price spikes, aluminium producers historically implement:

- Production curtailment: 15-25% capacity reduction during peak price periods

- Geographic shifting: Moving production to regions with lower energy costs

- Technology upgrades: Accelerated adoption of energy-efficient smelting technologies

- Financial hedging: Enhanced energy price risk management programmes

Geopolitical Response Strategies and International Coordination

US Navy blockade Strait of Hormuz scenarios would trigger coordinated international responses designed to mitigate supply disruption impacts and maintain economic stability. These responses involve both short-term emergency measures and long-term strategic adjustments.

Strategic Petroleum Reserve Coordination

International Energy Agency member nations maintain sophisticated coordination mechanisms for emergency petroleum reserve releases during supply disruptions. These systems, developed following the 1973 oil crisis, enable rapid market intervention during critical shortage periods.

Coordinated Release Framework:

- Triggering mechanisms: Supply disruption exceeding 7% of global production

- Release schedules: Synchronised timing across major consuming nations

- Market messaging: Clear communication regarding release duration and volumes

- Replenishment planning: Strategic timing for reserve rebuilding operations

Historical precedent from the 2022 Russia-Ukraine conflict demonstrated effective coordination, with the United States releasing 180 million barrels from strategic reserves while IEA members contributed additional volumes to stabilise markets. However, understanding US oil production decline trends reveals additional complexities in managing domestic supply chains during international crises.

Alternative Supply Route Development

Operations would accelerate infrastructure development for alternative petroleum transportation corridors. These projects, while requiring significant capital investment and development time, represent critical strategic initiatives.

Priority Infrastructure Projects:

- Trans-Arabian Pipeline expansion: Enhanced capacity to Red Sea export terminals

- Central Asian corridor development: Increased pipeline flows through Turkey and Russia

- African supply diversification: Expanded production from West African producers

- Arctic route utilisation: Enhanced ice-class tanker capacity for northern passages

The next major ASX story will hit our subscribers first

Financial Market Dynamics During Energy Supply Disruptions

Energy supply disruptions trigger complex financial market responses extending far beyond commodity price movements. Currency fluctuations, equity sector rotations, and bond market dynamics create investment opportunities and risks across multiple asset classes.

According to BBC News analysis of recent maritime tensions, naval blockades create immediate ripple effects through global financial systems. Furthermore, detailed reporting from The Guardian on naval blockade strategies provides insight into how such operations affect market psychology.

Currency and Commodity Market Correlations

Scenarios would generate predictable currency market responses based on historical energy crisis patterns:

Expected Currency Movements:

- US Dollar strengthening: 5-8% appreciation against major currencies due to safe-haven demand

- Oil-exporting nation currencies: 10-15% appreciation for non-affected producers

- Energy-importing nation currencies: 3-7% depreciation against the dollar

- Emerging market pressure: Broad-based weakness due to energy import costs

Gold markets historically demonstrate strong correlation with energy price spikes, typically gaining $50-100 per ounce during initial crisis phases as investors seek inflation hedges and store-of-value assets.

Equity Market Sector Rotation Patterns

Energy supply disruptions create distinct winners and losers across equity market sectors, generating substantial relative performance differences:

Sector Performance Expectations:

| Sector | Expected Performance | Performance Range |

|---|---|---|

| Energy Companies | Strong outperformance | +20% to +40% |

| Transportation | Significant underperformance | -15% to -30% |

| Consumer Discretionary | Moderate underperformance | -5% to -15% |

| Utilities | Mixed performance | -5% to +10% |

| Technology | Defensive performance | -3% to +8% |

Inflation and Central Bank Policy Responses

Scenarios present central banks with challenging stagflation concerns, where energy-driven inflation coincides with economic growth deceleration. Historical precedent from the 1970s demonstrates the complexity of monetary policy responses during energy crises.

Central Bank Policy Dilemmas:

- Inflation targeting: Core inflation potentially rising 1.5-2.5 percentage points

- Growth concerns: GDP impact from higher energy costs

- Interest rate policy: Balancing inflation control with recession risks

- International coordination: Managing currency volatility through policy alignment

Accelerated Energy Transition Investment Patterns

Energy supply disruptions historically accelerate alternative energy investment and technology adoption timelines. US Navy blockade Strait of Hormuz scenarios would likely trigger unprecedented clean energy infrastructure development programmes across major economies.

Renewable Energy Infrastructure Acceleration

Energy security concerns drive renewable energy investment beyond climate considerations, creating dual motivations for clean energy transition. In addition to traditional security motivations, energy transition investment patterns reveal how crises accelerate technological adoption.

Investment Acceleration Areas:

- Solar manufacturing capacity: 40-60% demand increase for photovoltaic systems

- Wind turbine production: 25-35% capacity expansion requirements

- Energy storage systems: Enhanced battery and hydrogen storage deployment

- Grid infrastructure: Smart grid technologies enabling renewable integration

Nuclear Power Renaissance Indicators

Energy crisis conditions historically correlate with renewed nuclear power interest, as governments prioritise energy security alongside decarbonisation objectives:

Nuclear Development Trends:

- Small modular reactors: Accelerated licensing and deployment programmes

- Existing plant lifetime extensions: Enhanced regulatory support for operations

- New construction projects: Expedited permitting for large-scale facilities

- International cooperation: Technology sharing agreements between allied nations

Alternative Energy Market Beneficiaries

Scenarios would create substantial market opportunities for companies positioned within alternative energy value chains. These opportunities span technology manufacturing, infrastructure development, and energy service provision.

Electric Vehicle Ecosystem Expansion

Transportation electrification receives significant momentum during petroleum supply disruptions, as consumers and fleet operators seek energy cost stability:

Market Growth Catalysts:

- Vehicle purchase incentives: Government subsidies for electric vehicle adoption

- Charging infrastructure: Rapid deployment of public charging networks

- Fleet conversions: Commercial operators transitioning to electric vehicles

- Battery technology: Enhanced investment in energy storage capabilities

Energy Efficiency Technology Adoption

Industrial and commercial energy efficiency solutions experience accelerated adoption during high energy price periods:

Efficiency Market Expansion:

- Building automation: Smart building systems reducing energy consumption

- Industrial optimisation: Process efficiency technologies and services

- Cogeneration systems: Combined heat and power installations

- Energy management software: Data analytics for consumption optimisation

International Cooperation Frameworks for Energy Security

Operations would necessitate enhanced international cooperation mechanisms extending beyond traditional energy market coordination. These frameworks involve diplomatic, military, and economic components designed to maintain global energy system stability.

Multilateral Emergency Response Protocols

International energy security requires sophisticated coordination mechanisms enabling rapid response to supply disruptions:

Coordination Elements:

- Information sharing: Real-time supply and demand data exchange

- Reserve release synchronisation: Coordinated timing and volumes

- Alternative supply arrangements: Bilateral and multilateral supply agreements

- Financial market stabilisation: Central bank coordination for currency stability

Technology Development Partnerships

Energy security challenges drive collaborative technology development programmes among allied nations:

Partnership Focus Areas:

- Advanced energy storage: Joint research and development initiatives

- Hydrogen production: Shared infrastructure investment programmes

- Carbon capture technologies: Accelerated deployment cooperation

- Grid modernisation: Cross-border electricity integration projects

Corporate Risk Management and Operational Resilience

Organisations across all sectors must develop comprehensive risk management strategies addressing US Navy blockade Strait of Hormuz scenarios and similar energy supply disruptions. These strategies encompass financial hedging, operational flexibility, and supply chain diversification.

Energy Cost Hedging Strategies

Corporate energy risk management becomes critical during volatile price periods:

Hedging Mechanisms:

- Futures contract utilisation: 6-18 month forward price coverage

- Options strategies: Price ceiling protection with upside participation

- Currency hedging: Protection against exchange rate volatility

- Supplier diversification: Multiple sourcing arrangements reducing concentration risk

Operational Flexibility Development

Business continuity planning must address various energy availability and pricing scenarios:

Resilience Measures:

- Energy audit implementation: Identifying 15-25% efficiency improvement opportunities

- Alternative fuel capabilities: Dual-fuel system installations for critical operations

- Remote work infrastructure: Reducing transportation energy requirements

- Supply chain redundancy: Multiple supplier relationships across different regions

Investment Consideration: Organisations examining energy security investments should evaluate both defensive measures protecting against supply disruptions and offensive strategies capitalising on energy transition opportunities. The intersection of energy security concerns and technological advancement creates unique investment themes spanning traditional and alternative energy sectors.

Disclaimer: This analysis presents hypothetical scenarios for educational and strategic planning purposes. All price projections, market impact assessments, and policy responses represent modelling exercises rather than predictions. Investors should conduct independent research and consult financial advisors before making investment decisions based on energy market scenarios. Historical performance does not guarantee future results, and energy markets remain subject to numerous unpredictable factors including geopolitical developments, technological changes, and regulatory shifts.

Looking to Capitalise on Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including critical energy transition commodities that could surge during supply disruptions. Understand why major mineral discoveries can lead to exceptional returns by exploring historic examples of companies that delivered substantial gains to early investors.