May 16, 2026

The Hidden Cost of America's Record Energy Export Boom

Every era of American energy dominance eventually confronts the same uncomfortable arithmetic: when the United States becomes the world's most critical supplier during a global supply shock, the benefits of that position flow outward to international buyers while the costs accumulate domestically at the fuel pump. U.S. oil exporters under scrutiny as gas prices spike across 50 states has become the defining energy story of 2026, driven by the Hormuz crisis placing this tension under an intensity not seen since the Russian invasion of Ukraine rattled markets in mid-2022.

Understanding how this situation developed, what the data actually reveals about the scale of the export surge, and why proposed legislative remedies carry serious unintended risks is essential for consumers, investors, and policymakers attempting to navigate what may become the most consequential energy governance debate of the decade.

When big ASX news breaks, our subscribers know first

How the U.S. Became the World's Default Energy Backstop in 2026

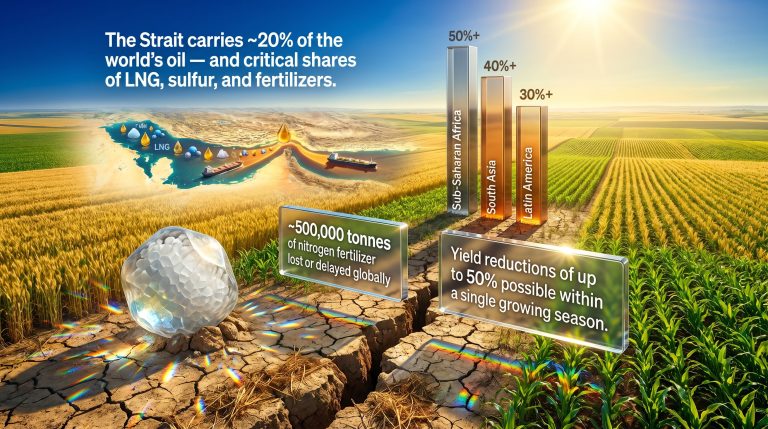

The Strait of Hormuz, a narrow waterway connecting the Persian Gulf to the Gulf of Oman, carries roughly 20% of the world's traded oil under normal conditions. When the Iran conflict disrupted those flows beginning in late February 2026, global energy markets faced a structural supply vacuum that no single producer could fully replace. The United States, however, moved faster and more aggressively than any other supplier to partially fill that gap.

Commodity intelligence data compiled by Kpler and reported through Reuters shows that U.S. shipments of crude oil, gasoline, LNG, diesel, jet fuel, and ethane reached 153 million tons between January and April 2026, representing a 20% year-over-year increase from the same period in 2025. When narrowed specifically to combined oil and refined product exports, the figure climbs even more steeply, reaching 14.2 million barrels per day in early 2026, a 33% jump relative to full-year 2025 averages.

This is not simply a story of opportunistic export growth. It reflects a fundamental repositioning of the United States as the marginal global energy supplier during a crisis, a role that carries both enormous commercial advantages and serious domestic consequences. Furthermore, the broader context of oil price geopolitics helps explain why American producers are so aggressively targeting international markets.

Breaking Down the 2026 Export Volume Figures by Commodity Type

The composition of the export surge reveals important details about where global demand pressures are concentrated:

| Commodity | Export Growth (YoY 2025-2026) | Key Driver |

|---|---|---|

| Total Oil, Fuels and LNG | +20% (153 million tons, Jan-Apr) | Highest recorded 4-month total |

| Combined Oil and Refined Products | +33% (14.2 million bpd) | Replacement buying across all regions |

| Gasoline | +27% | European and Asian panic procurement |

| Diesel | +23% | Freight and logistics demand surge |

| LNG | +26% | European energy security stockpiling |

| Jet Fuel | +82% | Largest single-commodity YoY surge |

The 82% year-over-year spike in jet fuel exports deserves particular attention. This scale of increase in a single refined product category is not explained by gradual demand growth. It reflects panic buying behaviour from international aviation hubs and fuel procurement desks that were scrambling to lock in supply before the Hormuz disruption deepened further.

When institutional buyers enter fear-driven procurement cycles, they systematically front-load purchases regardless of near-term price levels, creating demand spikes that look extreme against any historical baseline. In addition, the LNG supply outlook points to sustained European stockpiling demand well into the coming quarters.

Despite record-breaking export volumes, U.S. shipments replaced only approximately 30% of the Middle East supply deficit created by the Iran conflict. The approximately 82 million tons lost from Middle Eastern exporters since late February dwarfs the roughly 25 million tons added by the United States, leaving a net global supply gap of around 57 million tons that continues to exert persistent upward pressure on benchmark crude prices.

This coverage gap is the core reason why WTI crude reached $105.40 per barrel (up 4.20% in a recent session) and Brent crude climbed to $109.30 per barrel (up 3.35%) despite American producers operating at historically elevated output levels. Record U.S. production capacity does not automatically translate into the ability to replace structurally different supply streams from the Middle East.

What Is Happening to Gas Prices Across All 50 U.S. States

GasBuddy, which aggregates pricing data from more than 150,000 fuel stations across the United States, reported that the national average price of gasoline reached $4.54 per gallon as of early May 2026. That figure alone is alarming, but the more statistically significant element is the geographic uniformity of the increase. Consequently, U.S. oil exporters under scrutiny as gas prices spike across 50 states has dominated headlines in a way few energy stories have managed in recent years.

According to GasBuddy's head of petroleum analysis Patrick De Haan, every single state recorded a week-over-week price increase simultaneously, with some of the sharpest and most rapid movements concentrated in the Great Lakes region. States including Michigan, Indiana, Ohio, and Illinois experienced particularly steep price spikes, while Wisconsin saw more moderate but still significant gains.

Historical Gasoline Price Context

| Period | National Average | Triggering Event |

|---|---|---|

| Mid-2022 Peak | ~$5.00/gallon | Russia-Ukraine war energy shock |

| Current 2026 Level | $4.54/gallon | Iran-Gulf war, Hormuz disruption |

| Proposed Export Ban Trigger | $3.12/gallon (7-day threshold) | Gasoline Export Ban Act of 2026 |

| Feared Worst-Case Scenario | $6.00-$7.00/gallon | Prolonged Hormuz closure |

The simultaneous price increase across all 50 states is economically significant because it removes the regional buffering effect that typically moderates political pressure on energy policy. When only certain regions experience elevated pump prices, national legislative responses tend to be slower and more contested. When every state is affected simultaneously, the political calculus shifts rapidly, which is precisely the environment in which proposals like the Gasoline Export Ban Act gain legislative momentum.

A 50-state simultaneous increase also signals that the pricing pressure is originating from the wholesale and crude supply tier, not from regional refinery disruptions or localised distribution bottlenecks, which would produce uneven geographic patterns. This is a market-wide structural signal. However, understanding the relationship between oil prices and trade war dynamics adds further complexity to what is already a challenging pricing environment.

What Is the Gasoline Export Ban Act of 2026 and Would It Actually Work?

U.S. House Representative Ro Khanna reintroduced the Gasoline Export Ban Act of 2026 in late April, proposing a mechanism that would automatically prohibit gasoline exports whenever the national average price exceeds $3.12 per gallon for seven consecutive days. At $4.54 per gallon, the current national average already exceeds that trigger threshold by more than $1.40, meaning the ban would have been activated weeks ago had the legislation already been law.

The theoretical operating logic of the proposal follows a sequential supply chain argument:

- Trigger Activation – National average price exceeds $3.12 per gallon for seven consecutive days

- Export Prohibition Enacted – Gasoline shipments to foreign buyers are legally blocked

- Domestic Supply Increases – Fuel previously allocated for export enters the U.S. distribution network

- Refinery Allocation Shifts – Producers redirect output toward domestic rather than international channels

- Price Stabilization – Increased domestic supply creates competitive pressure that suppresses retail pump prices

The mechanism is straightforward in theory. The practical complications, however, are where the proposal runs into serious structural problems.

The Strongest Arguments Against a Gasoline Export Ban

The Crude Grade Mismatch Problem

The most technically significant objection to the proposed export ban involves the fundamental mismatch between the crude oil that American wells produce and the crude oil that American refineries are engineered to process.

The overwhelming majority of U.S. shale production yields light sweet crude, a lower-density, lower-sulfur oil that commands premium pricing on global markets. American refineries, however, were largely built and configured during an era when the dominant domestic and imported feedstock was heavy, complex crude containing higher sulfur content and requiring more intensive processing.

A gasoline export ban would redirect light sweet crude back into the domestic market, but U.S. refineries are not optimised to run exclusively on that feedstock. The result would be a domestic glut of light sweet crude that refineries cannot efficiently process at full capacity, occurring simultaneously with a shortage of the heavy complex crude grades those same refineries need to maintain optimal throughput.

This structural incompatibility could reduce refinery operating efficiency rather than increase it, potentially putting up to 1.3 million barrels per day of refining capacity at risk of curtailment or temporary closure. The paradox is striking: a ban designed to lower domestic fuel prices could actually reduce the volume of refined fuel produced in the United States.

Diplomatic and Trade Relationship Risks

Beyond the refinery mechanics, a unilateral export restriction would send a damaging signal to allied nations that have structured their energy security planning around reliable access to American supply:

- Europe – Having already dramatically reduced reliance on Russian pipeline gas following the 2022 invasion of Ukraine, European buyers have deepened procurement relationships with U.S. LNG and refined product exporters. An export ban would force European utilities and importers to accelerate emergency diversification plans.

- Asia – Major energy importers including Japan, South Korea, and India have incorporated U.S. crude and fuel exports into their strategic supply calculations. Sudden supply disruption from the United States would compound the damage already inflicted by the Hormuz closure.

- Latin America – Regional buyers reliant on U.S. Gulf Coast refinery output would face immediate supply gaps with limited alternative sourcing options in a crisis environment.

The Trump administration has consistently resisted the export restriction proposal, indicating a preference for maintaining the United States' position as a reliable global energy supplier while managing domestic price impacts through other mechanisms. The broader trade war economic impact on energy markets has further complicated the administration's room for manoeuvre on this issue.

At what price level that position becomes politically untenable remains the critical open question, particularly if pump prices approach the $6.00 to $7.00 per gallon range that some analysts have cited as a possibility if the Strait of Hormuz remains closed for an extended period.

The next major ASX story will hit our subscribers first

Comparing Policy Alternatives to an Export Ban

| Policy Option | Mechanism | Estimated Impact | Risk Level |

|---|---|---|---|

| Gasoline Export Ban | Prohibit foreign shipments | Increases domestic supply | High – refinery disruption risk |

| Strategic Petroleum Reserve Release | Inject federal reserves into market | Temporary price suppression | Medium – finite reserve capacity |

| Windfall Profits Tax on Exporters | Tax excess export revenues | Revenue redistribution | Medium – industry opposition |

| Diplomatic Resolution via Hormuz | Restore Middle East supply flows | Structural price normalisation | Low risk, high complexity |

| Demand-Side Fuel Subsidies | Direct consumer price relief | Immediate pump price reduction | High fiscal cost |

The comparison highlights a core policy design problem: the measures most likely to produce quick domestic price relief carry the highest risk of creating secondary market distortions or fiscal costs. The measure most likely to produce genuine structural price relief — a diplomatic resolution that restores Middle Eastern supply flows — is the most complex to execute and the least within any single government's direct control. Furthermore, U.S. natural gas prices are also responding to these broader supply pressures, adding another dimension to the domestic energy affordability debate.

The Diplomatic Off-Ramp and What It Could Mean for Energy Markets

Reports from early May 2026 indicate that the United States and Iran have been moving toward a potential ceasefire framework, with Pakistan serving as the primary mediating party. According to CNN reporting, negotiations had reached what officials described as their most optimistic stage since the conflict began, with a formal response from Tehran anticipated within 48 hours of the report's publication.

The framework under discussion involves a one-page, 14-point memorandum that would:

- Formally declare an end to the active conflict

- Initiate a 30-day period for detailed follow-up negotiations on permanent security and economic arrangements

- Commit Iran to a temporary suspension of uranium enrichment as a nuclear moratorium

- See the United States progressively lift sanctions and release frozen Iranian assets

- Phase out restrictions on shipping and the U.S. naval blockade to restore regional oil transit flows

If fully implemented, the restoration of Iranian export volumes combined with normalisation of Gulf shipping lanes would represent the single most structurally significant relief mechanism available to global energy markets. However, the timeline for complete market normalisation following any agreement would likely extend across multiple quarters, as physical supply chains, insurance markets, and shipping logistics would need to be fully reconstituted.

Energy markets were already pricing in some probability of diplomatic resolution, with Brent crude logging a 6% weekly gain as traders balanced ceasefire optimism against continued physical supply tightness.

A Governance Gap That Predates the Current Crisis

What the 2026 export debate has exposed is not merely a political disagreement about a single piece of legislation. It reveals a deeper governance gap: the United States does not have an established, codified framework for managing the tension between its commercial interests as a leading global energy exporter and its domestic obligation to protect consumers from supply-driven inflation during geopolitical crises.

The Gasoline Export Ban Act is a reactive legislative instrument, designed to treat the symptom rather than the underlying systemic condition. The broader question of how the world's largest energy-producing democracy should govern its export behaviour during geopolitical emergencies has never been formally resolved at the policy architecture level.

As American shale production continues to grow and U.S. LNG export capacity expands through projects like the recently approved $13 billion Commonwealth LNG facility in Louisiana, this tension will not diminish. It will become more structurally embedded in energy governance debates for years to come. For instance, USA Today's analysis of record oil exports underscores how this issue is resonating far beyond specialist energy circles.

Key Takeaways: What the U.S. Export Scrutiny Debate Means for Consumers, Markets, and Policy

U.S. oil exporters under scrutiny as gas prices spike across 50 states represents a pivotal moment in how America governs its role as a global energy powerhouse. In summary, the key facts are:

- U.S. energy exports surged 20% year-over-year in the first four months of 2026, reaching 153 million tons across crude, fuels, and LNG

- Combined oil and refined product exports hit 14.2 million barrels per day, a 33% increase from 2025 averages

- The national average gasoline price reached $4.54 per gallon, with all 50 states recording simultaneous week-over-week price increases for the first time

- The Great Lakes region, including Michigan, Indiana, Ohio, and Illinois, recorded the steepest localised price spikes nationally

- The proposed Gasoline Export Ban Act would activate at $3.12 per gallon, a threshold the current national average already exceeds by more than $1.40

- An export ban could threaten up to 1.3 million barrels per day of refining capacity due to the fundamental mismatch between domestically produced light sweet crude and the heavy complex grades American refineries are designed to process

- A diplomatic resolution between the United States and Iran, mediated by Pakistan, represents the most structurally significant potential relief mechanism for global energy markets, though full normalisation would span multiple quarters

- WTI crude is trading at $105.40 per barrel and Brent at $109.30 per barrel, reflecting a persistent global supply deficit that U.S. export volumes alone cannot close

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Energy price forecasts, legislative outcomes, and diplomatic developments referenced herein involve significant uncertainty. Past price behaviour is not indicative of future market conditions. Readers should conduct independent research before making any investment or financial decisions.

Want To Stay Ahead of Energy-Driven Commodity Discoveries on the ASX?

When geopolitical shocks like the Hormuz crisis reshape global energy markets, the flow-on effects for ASX-listed resource companies can be swift and substantial — Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries hit the ASX, transforming complex market data into actionable opportunities for investors at every level. Explore how historic discoveries have generated exceptional returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major market move.