July 8, 2026

The Sanctions Architecture Behind the US Decision to Revoke Iranian Oil Purchase Authorization

Energy markets have long operated within the shadow of geopolitical risk, but few mechanisms generate as much structured uncertainty as the US sanctions regime against Iran. The apparatus that governs Iranian oil flows is not a simple on/off switch. It is a layered system of general licenses, specific authorisations, wind-down provisions, and escrow requirements — each component calibrated to serve both economic and diplomatic objectives simultaneously. Understanding how that architecture functions is essential to interpreting what it means when the US revokes authorization to buy Iranian oil, and why the distinction between what was revoked and what remains technically active carries enormous practical weight.

When big ASX news breaks, our subscribers know first

How OFAC Uses Time-Limited Licenses as Geopolitical Instruments

The Treasury Department's Office of Foreign Assets Control administers US sanctions programmes with a precision that is often underappreciated by market participants. Within that framework, general licenses function as broad policy instruments, granting categorical permissions to defined classes of transactions without requiring individual case-by-case approval. Specific licenses, by contrast, are narrower authorisations issued for particular transactions or entities.

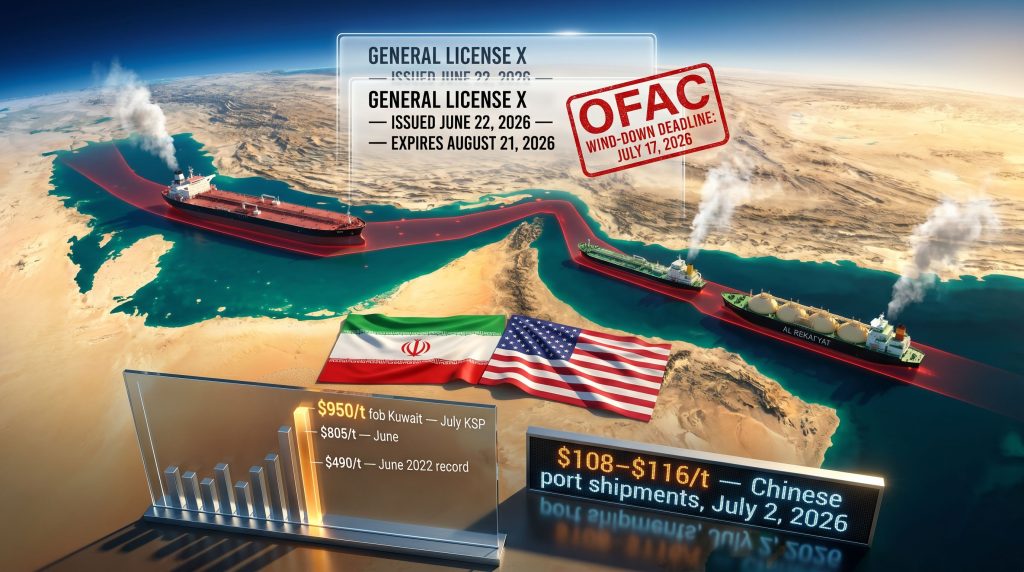

What makes time-limited general licenses particularly significant as diplomatic tools is their built-in conditionality. A 60-day authorisation is not merely an administrative convenience; it is a policy signal that communicates both willingness to engage and the retention of leverage. The authorisation that OFAC issued on June 22, 2026, and which was initially set to expire on August 21, 2026, exemplified this approach at its most expansive. It permitted:

- Purchases of Iranian crude oil, refined petroleum products, and petrochemicals

- Transactions involving the National Iranian Oil Company (NIOC), including those using blocked vessels

- Dollar-denominated payments flowing directly to Iran's central bank

This combination represented the broadest relaxation of US oil sanctions against Iran since the 1979 Islamic Revolution. No previous sanctions relief cycle had simultaneously unlocked NIOC access, dollar transaction permissions, and central bank revenue flows within a single general license framework.

The 60-day architecture of General License X was deliberately designed to create a compliance deadline that incentivised Iranian diplomatic performance rather than establishing a permanent sanctions carve-out.

Distinguishing What Was Revoked from What Remains Active

Market participants and compliance teams need to understand a critical distinction at the heart of the July 7, 2026 OFAC action. The US did not revoke the entirety of General License X on that date. What Treasury Secretary Scott Bessent had previously terminated in April 2026 was a narrower, earlier waiver that covered only oil already in transit before March 11, 2026. That authorisation had already expired by April.

What OFAC revoked on July 7, 2026 was the specific authorisation for new purchases of Iranian oil, refined products, and petrochemicals under the June 22 framework. The broader General License X structure nominally remains active until August 21, 2026, but the revocation of purchase authorisation effectively renders it commercially inert for new supply arrangements.

| Policy Instrument | Status | Scope | Expiry |

|---|---|---|---|

| Prior transit waiver (pre-March 11, 2026 oil) | Revoked / Not Renewed | Limited to oil in transit only | Ended April 2026 |

| General License X (issued June 22, 2026) | Active but purchase authorisation revoked | Broad: crude, refined products, petrochemicals | August 21, 2026 |

| NIOC transaction permissions | Active under General License X framework | Includes blocked vessels | August 21, 2026 |

| New purchase authorisation | Revoked effective July 7, 2026 | All Iranian oil commodity channels | Terminated |

Buyers who contracted for Iranian oil during the June 22 authorisation window have until July 17, 2026 to settle outstanding transactions. All payments owed to Iranian counterparties must be deposited into escrow accounts rather than transferred directly to Tehran, a mechanism that preserves US leverage over Iranian revenue access even during the wind-down period.

Furthermore, according to reporting on the US license revocation, oil markets reacted immediately to the announcement, with prices gaining as traders reassessed supply security across Gulf commodity channels.

Compliance Warning: The July 17, 2026 wind-down deadline is non-negotiable under current OFAC license terms. Failure to complete transaction settlement or establish compliant escrow arrangements by this date exposes buyers to both primary and secondary sanctions liability.

The Hormuz Attacks That Fractured the Interim Agreement

The diplomatic context underpinning the June 22 authorisation was a US-Iran interim agreement signed on June 18, 2026, which established two core commitments: mutual restraint from the use of force, and the full reopening of the Strait of Hormuz to commercial navigation. The agreement's fragility became apparent almost immediately as Iranian forces continued asserting jurisdictional claims over the waterway.

The precipitating event for the July 7 revocation was a series of Iranian attacks on commercial vessels transiting the southern Strait of Hormuz corridor. Three vessels were targeted:

- A very large crude carrier (VLCC) struck 16 nautical miles east of Khor Fakkan, UAE, while exiting the strait

- A tanker hit 6 nautical miles off the Musandam Peninsula, Oman, sustaining minor structural damage with no reported casualties

- An LNG tanker identified as the Al Rekayyat, subsequently reported as abandoned following the strike

The significance of these attacks extends beyond the immediate physical damage. The southern Oman-coast corridor had been positioned as a US-protected safe transit lane for the two weeks preceding the attacks. Iranian forces choosing to strike vessels along that specific route sent an unambiguous signal: Tehran was deliberately challenging the US military's capacity to enforce the Hormuz reopening commitment embedded in the June 18 agreement.

Following the attacks, the UK Trade Maritime Organisation (UKTMO) elevated the Strait of Hormuz threat level from substantial to severe — the second-highest classification on the Joint Maritime Information Committee's threat scale. Maritime security firm Windward characterised the safety of the southern corridor as being in serious doubt, noting that strikes had occurred even in areas where US air support had been active.

The targeting of an LNG tanker introduces a dimension of risk that energy markets had not previously priced fully. LNG carrier vulnerability in the strait had historically been considered lower than that of crude tankers. The Al Rekayyat incident challenges that assumption directly, and consequently, the broader LNG supply outlook for Asian buyers now carries substantially elevated risk.

Commodity Market Stress Signals Across Multiple Sectors

The cascading market effects of sustained Hormuz disruption are visible across several commodity categories simultaneously, each reflecting a different dimension of supply chain stress.

How Are Sulphur Markets Responding?

Sulphur markets are experiencing record pricing pressure. Kuwait's state-owned KPC set the July Kuwait Sulphur Price (KSP) at $950/t fob Kuwait, an increase of $145/t from June's figure of $805/t. More strikingly, this level sits $460/t above the previous all-time record of $490/t fob set in June 2022. Freight rates for sulphur shipments of 30,000 to 35,000 tonnes to Chinese ports were running at $108 to $116/t as of July 2, 2026, implying delivered costs of $1,058 to $1,066/t cfr before additional insurance premiums.

What Pressure Are European Fuel Markets Facing?

European fuel markets are absorbing compounding pressure. Germany's temporary fuel tax reduction, introduced from early May 2026 to cushion consumers from the price surge caused by the US-Iran conflict, expired on June 30, 2026. The reduction had lowered rates by €14.04 per 100 litres. Its expiry is already compressing demand as consumers and filling stations that had built stocks ahead of the return to regular tax rates are now drawing down inventories before re-entering the spot market.

In addition, these commodity market pressures are intensifying across interconnected sectors, with hedging strategies coming under significant strain as volatility persists.

LNG supply chains serving Asian buyers face compounding exposure. Qatar and UAE LNG exports both transit the Strait of Hormuz, and the direct targeting of an LNG carrier fundamentally alters the risk calculus for vessels that insurers had previously treated as lower-risk assets within the strait.

Step-by-Step Compliance Framework for the July 17 Wind-Down

Organisations that contracted for Iranian oil under the June 22 authorisation need to execute wind-down procedures with precision. The following framework outlines the required steps:

- Audit all active Iranian oil contracts entered into from June 22, 2026 onward under the General License X authorisation window

- Confirm wind-down eligibility — only transactions contracted during the active General License X period qualify for the July 17 settlement extension

- Establish compliant escrow accounts for all outstanding payments directed toward Iranian counterparties, as mandated under updated OFAC license terms

- Halt all new procurement immediately — no new purchases of Iranian crude, refined products, or petrochemicals may be initiated following the July 7 revocation

- Assess secondary sanctions exposure for any affiliated petrochemical feedstock or downstream processing transactions that may carry indirect Iranian commodity linkages

- Monitor OFAC guidance updates before August 21, 2026, as further policy amendments remain possible if US-Iran diplomatic engagement resumes

Compliance Note for Legal Teams: Conflating the revoked purchase authorisation with the broader General License X framework creates material compliance risk. Each transaction must be assessed against the specific authorisation that governed it at the time of contracting.

The next major ASX story will hit our subscribers first

Scenario Pathways: Could the Authorization Be Restored?

Three credible policy trajectories exist beyond the August 21, 2026 General License X expiry date, each with distinct market implications.

| Scenario | Probability Driver | Market Outcome |

|---|---|---|

| Full reinstatement | Verifiable Iranian withdrawal from Hormuz control assertions; diplomatic resolution | Iranian crude re-enters global supply; downward pressure on benchmark prices |

| Extension of General License X | Ongoing negotiations past August 21; precedent for rolling extensions exists | Prolonged market uncertainty; buyers cautious about long-term supply commitments |

| Permanent revocation | Continued Iranian military action; breakdown of interim deal | Sustained upward crude price pressure; war-risk insurance premiums spike further |

The Trump administration's framing of the General License X authorisation as economically reciprocal — positioning Iranian oil revenues as being channelled toward purchases of American agricultural products — provides a structural incentive for reinstatement. The escrow requirement for pending payments is not merely a compliance mechanism; it is an active diplomatic lever that preserves Washington's ability to condition Iranian revenue access on behavioural changes.

However, the broader US-China trade dynamics also shape the sanctions landscape, as Chinese buyers represent a critical variable in determining how effectively any Iranian oil purchasing restriction can be enforced in practice.

Lessons from Prior US-Iran Sanctions Cycles

Historical precedent offers important context for assessing both the likely effectiveness and the limitations of the current revocation. Indeed, the history of US sanctions against Iran demonstrates a consistent pattern of escalation, partial relief, and renewed pressure across multiple administrations.

- 2012 coordinated EU/US sanctions: Reduced Iranian crude exports from approximately 2.5 million b/d to under 1 million b/d within 18 months, demonstrating the power of multilateral enforcement alignment

- 2018 JCPOA withdrawal and maximum pressure campaign: Re-imposed comprehensive oil sanctions; China and India continued purchasing Iranian crude through alternative payment mechanisms that circumvented dollar-denominated transaction requirements

- 2019 to 2020 sanctions waivers: Eight countries, including China, India, and Turkey, received temporary authorisations for continued Iranian oil purchases, establishing the precedent for time-limited general licenses as diplomatic tools

- 2026 General License X: The most expansive single authorisation since 1979, encompassing NIOC access, dollar transactions, and central bank revenue flows in a framework with no historical precedent

Each prior cycle demonstrated a consistent structural limitation: unilateral US enforcement faces erosion when major consuming nations, particularly China, maintain alternative payment and settlement channels. The current revocation occurs against a backdrop of active Hormuz hostilities that complicate operational logistics even for buyers willing to absorb secondary sanctions risk. Furthermore, the broader tariff and trade environment in 2025 and beyond compounds the difficulty of achieving coordinated multilateral enforcement.

The Strait of Hormuz as a Systemic Market Variable

Approximately 20 to 21 million barrels per day of crude oil and petroleum products transit the Strait of Hormuz, representing roughly 20% of global oil consumption. The strait's minimum navigable width is approximately 2 nautical miles in each direction, creating acute vulnerability to interdiction that no alternative routing can fully substitute.

The southern Oman-coast corridor had represented the most viable lower-risk pathway through the strait. Its compromise following the July 7 attacks reduces the effective number of defensible transit routes to one, concentrating risk and creating upward pressure on freight insurance premiums across crude oil, refined products, LNG, and petrochemical feedstocks simultaneously.

For energy market participants, the Strait of Hormuz has historically functioned as a tail-risk variable — something priced into options markets but rarely activated at the operational level. The sustained pattern of Iranian interdiction activity following the June 18 interim agreement suggests that the strait has transitioned from a tail-risk variable into a recurring operational constraint. Consequently, this shift carries significant implications for how market participants model supply security across all Gulf-sourced commodity flows, and reinforces the structural importance of understanding when and how the US revokes authorization to buy Iranian oil as a forward-looking policy signal.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. Readers should conduct independent due diligence and consult qualified legal and compliance professionals before making decisions related to Iranian oil transactions or sanctions compliance. All figures, dates, and regulatory details are based on publicly available information as of the time of writing and are subject to change as the policy environment evolves.

Want to Stay Ahead of the Commodity Disruptions Reshaping ASX Markets?

When geopolitical shocks like Hormuz supply disruptions ripple through energy and commodity markets, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying mineral discovery opportunities across more than 30 commodities — explore historic discovery returns on Discovery Alert's dedicated discoveries page to understand the scale of what early positioning can mean, and begin a 14-day free trial to ensure market-moving announcements never catch you off guard.