July 19, 2026

The Hidden Vulnerability in North American Bulk Mineral Supply Chains

Most commodity analysts spend their careers tracking copper spreads, lithium carbonate premiums, and iron ore futures. Yet one of the most structurally exposed bulk materials in North America trades without an exchange listing, lacks any derivatives mechanism, and cannot be hedged through options or forward contracts. US salt import reliance and USMCA reviews have become, quietly, one of the clearest case studies for how trade-policy uncertainty compounds supply risk in freight-sensitive industrial markets.

Understanding why requires looking beyond the commodity itself and into the architecture of the supply chains that move it. When margins per tonne are thin, freight costs consume a disproportionate share of the delivered price, and import sources are geographically concentrated, the commercial consequences of trade-policy disruption arrive faster and with less warning than in higher-value industries.

When big ASX news breaks, our subscribers know first

US Salt Import Reliance: A Structural Gap, Not a Seasonal Blip

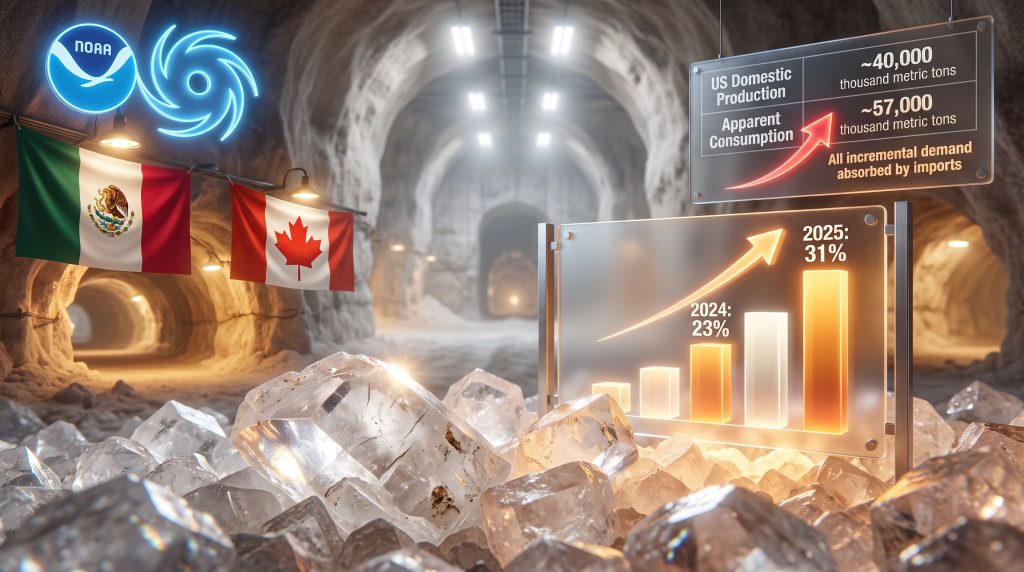

The numbers published by the US Geological Survey in its Mineral Commodity Summaries 2026 reveal a supply picture that deserves more attention than it typically receives.

| Metric | 2024 | 2025 (Estimated) |

|---|---|---|

| US Domestic Salt Production | ~40,000 thousand metric tons | ~40,000 thousand metric tons |

| Apparent Consumption | ~53,000 thousand metric tons | ~57,000 thousand metric tons |

| Imports for Consumption | ~12,000 thousand metric tons | ~19,000 thousand metric tons |

| Net Import Reliance | 23% | 31% |

The critical detail here is not the absolute import volume but the trajectory. Domestic production held essentially flat at approximately 40 million metric tons across both years, while apparent consumption climbed to an estimated 57 million metric tons in 2025. Every tonne of incremental demand was satisfied through imports rather than expanded domestic output. That is a structural signal, not a weather-driven anomaly.

The USGS documented a regional rock salt shortage in New York during early 2025, driven by severe winter demand colliding with constrained local supply. That event functioned as a leading indicator of national supply tightening that the aggregate import-reliance data later confirmed.

Key Insight: The steepest single-year increase in US salt net import reliance on record occurred not because domestic production contracted, but because no new underground salt mine has been commissioned in the US since 2001. The supply response mechanism simply does not exist in its current form.

Where US Salt Actually Comes From

The geographic concentration of US salt imports adds another layer of vulnerability. Furthermore, between 2021 and 2024, the country's import mix broke down roughly as follows:

| Country | Share of US Salt Imports (2021-2024 Average) |

|---|---|

| Mexico | ~26% |

| Canada | ~21% |

| Chile | ~23% |

| Egypt | ~6% |

Mexico and Canada together account for approximately 47% of US salt imports. Critically, Chile and Egypt, which supply a combined ~29%, cannot serve as rapid substitutes. Salt's low value relative to freight costs creates structural switching barriers. Established rail corridors and port infrastructure connecting the US to Mexican and Canadian suppliers have been built over decades and cannot be replicated on short notice through long-haul ocean freight from South America or North Africa.

What the USMCA Review Mechanism Actually Changes

The United States-Mexico-Canada Agreement contains a built-in review mechanism under Article 34.7, which required a formal joint assessment by July 1, 2026, six years after the agreement entered into force. All three parties were required to confirm in writing whether they wished to extend USMCA for a further 16 years, carrying the framework through to 2036.

The US declined to renew the agreement in its current form. The Office of the US Trade Representative confirmed this outcome, leaving USMCA operational but replacing the 16-year planning horizon with a recurring annual review cycle that will continue until 2036. According to analysis from the Atlantic Council, what is at stake extends well beyond automotive provisions to encompass the stability of deeply integrated North American supply chains.

For most industries, this distinction may appear technical. However, for salt, it changes the commercial calculus in concrete ways:

- Long-term supply contracts that previously relied on stable duty-free access now face renegotiation uncertainty every 12 months

- Procurement officers who previously locked in multi-year sourcing from Mexican and Canadian suppliers must now reassess their strategies with each contracting cycle

- Salt buyers have no financial hedging instrument to price in trade-policy risk, unlike base-metals purchasers who can reference liquid forward markets

- Alternative import sources are economically unviable at scale given freight economics, meaning USMCA-dependent supply has no near-term substitute

Policy Context: The USMCA review's central priorities encompass automotive supply chain provisions, labor standards, and reducing dependence on Chinese inputs. The downstream effects on freight-sensitive bulk commodities like salt are rarely featured in mainstream trade-policy commentary, yet the exposure is structurally comparable.

How Trade-Policy Risk Compares Across Commodity Types

| Commodity Type | Exchange-Traded? | Derivatives Hedge Available? | USMCA Exposure | Ability to Absorb Trade Shock |

|---|---|---|---|---|

| Copper / Base Metals | Yes | Yes | Moderate | High |

| Agricultural Commodities | Yes | Yes | High | Moderate-High |

| Salt (Bulk Mineral) | No | No | High | Low |

| Potash / Industrial Minerals | Limited | Limited | Moderate | Low-Moderate |

A characteristic that distinguishes salt from most other trade-exposed commodities is that price signals do not emerge until after regional shortages materialise. There is no futures curve to read, no options skew to analyse, and no exchange-cleared forward market to monitor. This information asymmetry means that procurement officers and investors are often reacting to tightening conditions rather than anticipating them. Indeed, the broader impact on global commodity markets from shifting trade policy is already being felt across multiple bulk mineral categories.

El Niño as a Demand Multiplier: The 2026-27 Procurement Environment

On July 13, 2026, NOAA's Climate Prediction Center issued an El Niño Advisory, replacing the weak La Niña baseline that had informed procurement planning for the prior deicing season. NOAA estimated a 97% probability that El Niño conditions would strengthen through year-end 2026 and persist into early spring 2027.

This is the second consecutive planning-cycle revision, and it matters because road-salt demand is fundamentally a function of winter precipitation intensity and geographic distribution.

| Climate Pattern | Typical US Winter Conditions | Road-Salt Demand Implication |

|---|---|---|

| La Niña | Milder, drier in southern US | Lower demand in Gulf Coast and Southeast |

| El Niño | Wetter, stormier in Gulf Coast and Southeast | Higher demand in regions with underdeveloped deicing infrastructure |

The less-obvious dimension of an El Niño shift is that it increases demand uncertainty in regions that do not typically contract large volumes of road salt. Municipal buyers in the Gulf Coast and Southeast generally operate without the sophisticated forward procurement programmes that snowbelt transportation departments have developed over decades. Greater weather uncertainty in these markets creates additional incentive to secure contracted supply ahead of winter rather than rely on spot purchasing, which tightens the contracting environment for the entire bid season.

An analogy drawn from mining practice is instructive here: just as grade reconciliation forces mine operators to compare actual mined tonnes and grades against the mine plan and revise forecasts accordingly, El Niño-Southern Oscillation updates force road-salt buyers to reconcile their procurement assumptions against revised seasonal weather models. The difference is that mine operators have established protocols for this exercise; many municipal buyers in non-traditional markets do not.

Why Domestic Supply Cannot Respond Quickly

A reasonable question to ask is why US salt producers cannot simply expand output to meet rising demand. The answer lies in the geology, permitting, and capital structure of underground salt mining.

Step-by-Step: The Development Timeline for a New Underground Salt Mine

- Exploration and resource definition — Geological surveys, drilling programs, and resource estimation establish the basis for project development

- Environmental and regulatory permitting — Multi-agency review processes that frequently span two to five years, involving federal, state or provincial, and municipal authorities. Understanding the basics of grade, permitting, and mine planning is essential context for appreciating why this phase is so difficult to compress

- Feasibility study completion — Full engineering, cost estimation, and financial modelling including NPV and IRR analysis; a definitive feasibility study is typically the gateway to project financing

- Project financing — Securing senior secured debt, equity capital, and in some cases export credit agency support across a process that can itself take 12 to 24 months

- Construction and commissioning — Surface works, shaft sinking, and underground development representing major capital commitments

- Ramp-up to steady-state production — Typically 12 to 24 months post-commissioning before full capacity is reached

Structural Reality: The combined timeline from exploration through to steady-state production for a greenfield underground salt mine is measured in years, not quarters. Annual trade-policy reviews and seasonal climate shifts will consistently outpace any domestic supply response in the near term.

No new underground salt mine has been commissioned in the US since 2001. Several existing underground operations are approaching the end of their operational lives within a five-to-ten year horizon. This combination of aging infrastructure and zero new capacity additions creates a structural foundation for sustained import dependence.

Development-Stage Projects and the Path to New Domestic Capacity

Because US domestic supply cannot expand through existing operations alone, the meaningful pathway to reducing import reliance runs through development-stage projects advancing toward construction.

The benchmarks that separate viable candidates from exploratory-stage aspirations are relatively well-defined:

| Project Metric | Benchmark for Viability |

|---|---|

| Planned Annual Production | 2 million tonnes per annum or above |

| Mine Life | 20 years or longer |

| After-Tax NPV (8% discount rate) | Positive with meaningful margin |

| After-Tax IRR | 15% or higher |

| Payback Period | 5 years or less |

| Financing Status | Senior debt under active due diligence |

One project that currently meets or exceeds these benchmarks is Atlas Salt's Great Atlantic Salt Project, located near St. George's on the west coast of Newfoundland and Labrador. The project's September 2025 Updated Feasibility Study reported an after-tax NPV of $920 million at an 8% discount rate, an after-tax IRR of 21.3%, and a payback period of 4.2 years based on planned steady-state production of 4.0 million tonnes per annum over a 25-year mine life.

Atlas Salt commenced Early Works on February 27, 2026, with the surface earthworks contractor mobilising to site in early May 2026. The transition from Early Works to Capital Works construction remains contingent on closing a targeted $350 million to $400 million senior secured debt package, which is currently under non-binding due diligence with prospective lenders and export credit agencies.

The project's stated commercial focus is supplying deicing road salt to underserved markets in the northeast United States, eastern Canada, and the Atlantic provinces — regions where supply constraints are already measurable in the USGS import-reliance data.

Jurisdictions that offer streamlined municipal and provincial permitting processes provide a genuine competitive advantage in bulk mineral development, allowing projects to compress the regulatory phase of the development timeline meaningfully relative to US-based equivalents.

The next major ASX story will hit our subscribers first

Salt as a Template for Broader Bulk Mineral Trade-Policy Risk

The analytical value of salt extends beyond the commodity itself. Because the USGS publishes detailed annual import-reliance data at the country level, salt provides one of the most transparent windows available for measuring how trade-policy changes propagate through bulk mineral supply chains.

The structural characteristics that create vulnerability in the salt market apply broadly across other freight-sensitive industrial minerals:

| Commodity | Primary USMCA Import Source | Exchange-Traded? | Hedging Available? |

|---|---|---|---|

| Salt | Mexico / Canada | No | No |

| Potash | Canada | Limited | Limited |

| Lime / Limestone | Mexico / Canada | No | No |

| Construction Sand and Gravel | Canada / Mexico | No | No |

The transition from a 16-year USMCA planning framework to annual reviews may introduce comparable uncertainty across this broader category of bulk commodities. S&P Global's assessment of the USMCA review highlights that North American supply chains face high-stakes tests across multiple sectors. The difference is that equivalent import-reliance data series rarely exist for these materials, making the systemic risk harder to quantify and therefore easier to overlook. Consequently, the broader impact of trade wars on supply chains remains a critical consideration for any procurement strategy built around USMCA-sourced bulk minerals.

Key Indicators to Monitor Through the 2026-27 Bid Season

The upcoming North American road-salt bid season will serve as the first real-world stress test of a supply chain operating simultaneously under elevated import reliance, recurring trade-policy uncertainty, and an uncertain El Niño-driven demand outlook. Three measurable indicators will determine whether current market tightness represents a temporary imbalance or the beginning of a sustained structural shortfall:

- Progress in bilateral trade negotiations — US-Mexico and US-Canada discussions under the annual USMCA review process will determine whether duty-free salt imports from the two largest supply sources remain competitively priced heading into the next contracting cycle

- Development-stage project advancement — Financial close and the transition from Early Works to Capital Works construction at projects like the Great Atlantic Salt Project will establish a concrete timeline for new domestic capacity

- 2026-27 bid season outcomes — Contract prices, awarded volumes, and term structures negotiated during the bidding process will reveal whether buyers are absorbing higher procurement costs or restructuring their sourcing strategies in response to market tightening

Investor Framework: The shift from a 16-year trade framework to annual USMCA reviews does not immediately disrupt supply, but it introduces a recurring uncertainty premium that compounds with each review cycle. For freight-sensitive bulk commodities with no financial hedging mechanism, this premium has nowhere to go except into physical contract pricing once regional shortages materialise.

Producers entering the bid season with stronger balance sheets are better positioned to pursue commercial execution at scale. The ability to commit to volume and term without balance-sheet constraints becomes a genuine competitive differentiator in a market where buyers are increasingly motivated to secure supply rather than rely on spot availability.

Frequently Asked Questions: US Salt Import Reliance and USMCA Reviews

Why did US salt net import reliance increase so sharply between 2024 and 2025?

Domestic production held flat at approximately 40 million metric tons while apparent consumption rose to approximately 57 million metric tons in 2025. Because no new underground salt mine has entered US production since 2001, all incremental demand was absorbed through imports, driving net import reliance from 23% to 31% in a single reporting year. The USGS-documented rock salt shortage in New York during early 2025 provided an early regional signal of the national tightening later confirmed in aggregate data.

What happens to USMCA salt trade if annual reviews fail to produce agreement?

The agreement remains in force but continues under annual review until 2036. Each cycle without renewal extends trade-policy uncertainty for another 12 months. For salt, this means procurement officers must renegotiate sourcing assumptions each contracting year without knowing whether duty-free access from Mexico and Canada will remain intact — which is a materially different planning environment than the 16-year framework USMCA originally established.

Can the US realistically replace Mexican and Canadian salt imports through other sources?

Not quickly, and not at comparable cost. Salt's low value relative to freight makes long-distance ocean shipping from alternative suppliers like Chile or Egypt economically unviable as a short-notice substitute for USMCA-sourced volumes. Established rail and port infrastructure linking the US to Mexican and Canadian suppliers represents a decades-built logistics network that cannot be replicated through spot-market sourcing.

How does the El Niño shift affect road-salt procurement planning?

El Niño conditions increase the probability of wetter and stormier winters across the Gulf Coast and Southeast, regions with less-developed deicing infrastructure than the traditional snowbelt. Greater demand uncertainty in markets that do not typically secure large contracted volumes creates additional incentive for forward purchasing, tightening the overall contracting environment for the 2026-27 deicing season.

What is the most important near-term indicator of whether supply risk is structural or temporary?

Watch two developments in parallel: progress in US bilateral trade negotiations with Mexico and Canada under the annual USMCA review process, and financial close for development-stage domestic salt projects. A project's transition from Early Works to Capital Works construction establishes a concrete production timeline. Until one or both of these developments materialise, the conditions supporting elevated import reliance remain firmly in place.

This article references data from the US Geological Survey Mineral Commodity Summaries 2026 and the NOAA Climate Prediction Center July 2026 outlook. Forward-looking statements regarding trade negotiations, project financing, and market conditions involve inherent uncertainty and should not be construed as financial advice. Readers should conduct their own due diligence before making investment decisions.

Want to Identify the Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, transforming complex geological and commodity data into actionable investment insights — explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.