July 11, 2026

The Architecture of Emergency: How Strategic Reserves Became Europe's Crude Oil Lifeline

Global oil markets have always operated on a fundamental tension between geographic concentration of supply and the dispersed nature of demand. Roughly 20% of the world's entire crude oil trade has historically moved through a single 33-kilometre-wide waterway connecting the Persian Gulf to the Arabian Sea. When that corridor closes, the reverberations reach every refinery, every petrol station, and every national energy ministry simultaneously. The question is never whether emergency reserves can fully replace such a loss, but rather how efficiently they can be deployed and who captures the most value when they are.

The answer, as of late April 2026, is increasingly clear: Europe has emerged as the dominant buyer of U.S. Strategic Petroleum Reserve oil, absorbing discounted transatlantic barrels at a pace that is reshaping Atlantic Basin crude trade flows, pressuring regional benchmark pricing, and revealing deep structural vulnerabilities in European energy security that persist long after the geopolitical headlines fade.

When big ASX news breaks, our subscribers know first

The Supply Disruption That Forced a Historic Coordinated Response

The Strait of Hormuz closure did not merely tighten global markets. According to Standard Chartered analysis, the conflict effectively removed an estimated 8 million barrels per day from accessible global supply chains, a volume equivalent to roughly 8% of total daily world consumption. This is not a marginal shortfall. It is a structural rupture in the plumbing of global energy trade, and no existing supply source can simply step in to cover such a deficit at scale.

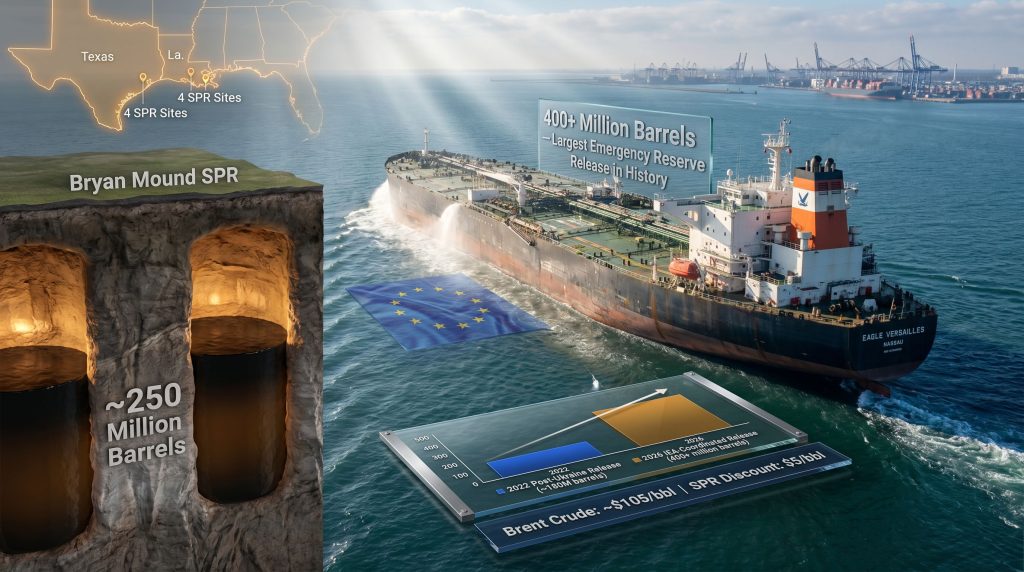

The International Energy Agency's response was to authorise a coordinated release of more than 400 million barrels from member-nation strategic reserves, the largest emergency intervention of its kind in the agency's history. The IEA exists specifically for moments like this: it was founded in 1974 following the Arab oil embargo precisely to provide a multilateral mechanism for collective crisis management. However, even by the IEA's own historical standards, the scale of this release is extraordinary, and it reflects the severity of the underlying supply shock rather than confidence in an imminent resolution.

Why 400 Million Barrels Is Both Large and Insufficient

The mathematics of this crisis expose an uncomfortable reality that investors and policymakers alike must confront directly. Furthermore, Standard Chartered's arithmetic is stark:

- The Hormuz disruption removes approximately 8 million barrels per day from global markets

- The IEA's combined 400+ million barrel release covers this deficit for only approximately 50 days

- The U.S. contribution of ~172 million barrels represents roughly 43% of the total coordinated release

- This U.S. contribution alone would cover the daily deficit for approximately 21 days

Strategic petroleum reserves were engineered to absorb short-term supply shocks, not to substitute for the sustained loss of a major global shipping corridor. The Strait of Hormuz disruption is a structural problem; SPR releases are a tactical instrument designed for a different scale of crisis.

This mismatch between the scale of the emergency tool and the magnitude of the crisis it is addressing is why oil prices remain elevated near $105 per barrel for Brent crude despite the release. Consequently, European buyers are still competing aggressively for every discounted barrel they can source from the U.S. Gulf Coast. Tracking current crude oil prices confirms how persistent this elevation has been across Atlantic Basin benchmarks.

Inside the U.S. SPR: Scale, Infrastructure, and the 120-Day Clock

Understanding why the U.S. can deploy barrels to European refineries with such speed requires an appreciation of the SPR's physical infrastructure. The reserve holds approximately 727 million barrels of authorised storage capacity distributed across 60 underground salt caverns at four Gulf Coast sites spanning Texas and Louisiana. Salt cavern storage provides natural geological pressure containment, thermal stability, and resistance to seismic disruption, making it far superior to above-ground tank storage for long-duration emergency stockpiling.

Before the current drawdown commenced, the SPR held approximately 415 million barrels, representing roughly 60% of total capacity. This baseline was already historically low following the large-scale 2022 post-Ukraine drawdown, which left reserves at between 350 and 370 million barrels before partial replenishment occurred.

The current release is structured across a 120-day window beginning in late March 2026, designed to allow market absorption rather than flooding supply chains simultaneously. As of late April 2026, approximately 79.7 million barrels had already been allocated across 12 companies, representing a distribution rate of roughly 3 million barrels per day, a meaningful daily injection into tight global markets.

The Bryan Mound Advantage: Why Grade Matters for European Buyers

The Bryan Mound SPR site in Texas holds approximately 250 million barrels, making it the single largest crude repository within the U.S. reserve system. Crucially, Bryan Mound stores medium sour crude, a grade characterised by higher sulphur content relative to light sweet crude benchmarks like WTI or Brent. This grade distinction has direct commercial implications for which refineries can process these barrels and at what economic efficiency.

Mediterranean European refineries were largely configured in the 1970s and 1980s to process medium to heavy sour crude grades, which were then abundant and cheap from Middle Eastern producers. This historical infrastructure decision now works in their favour: when U.S. sour crude from the SPR enters European markets at a discount, these refineries can process it without costly configuration adjustments, making the economics of transatlantic sourcing compelling.

How the SPR Exchange Mechanism Actually Functions

A critical distinction that market participants frequently overlook is that the current SPR distribution is structured as an exchange mechanism, not an outright sale of government assets. Understanding this legal and financial architecture is essential for assessing the medium-term market implications.

Under an SPR exchange, the U.S. Department of Energy loans barrels from emergency stockpiles to commercial recipients, typically refiners or commodity trading firms. These recipients are contractually obligated to return equivalent volumes of crude oil at a specified future date, plus a contractual premium. The exchange mechanism allows emergency barrels to reach refineries quickly while preserving the government's long-term reserve reconstitution rights.

For the 2026 tranche of loans involving high-sulphur sour crude, the DOE has structured repayment requirements that include:

- Return of equivalent crude volumes by 2028

- Interest rates of up to 22%, typically payable in sweeter, higher-value crude grades rather than cash

- Grade upgrade obligations, meaning recipients who borrow sour crude frequently repay in light sweet grades of higher commercial value

This interest structure creates a subtle but important market dynamic. When 2028 return obligations fall due, a large volume of higher-quality crude will need to flow back into the SPR, creating measurable demand pressure on sweet crude grades at that point in the forward curve. Traders and refiners sophisticated enough to model this replenishment cycle are already incorporating it into their medium-term hedging strategies.

The 2022 Precedent and Its 2026 Consequences

The current drawdown cycle cannot be understood without reference to the 2022 post-Ukraine crisis release, in which the Biden administration authorised large-scale SPR loans with repayment timelines deliberately deferred to 2026. That policy decision, designed to prevent secondary market tightening during 2022 and 2023, means that a portion of the barrels currently entering the SPR replenishment queue are legacy obligations from a crisis four years prior. In other words, the U.S. reserve system is simultaneously being drawn down for a new crisis while still processing the replenishment obligations of the last one.

Europe received approximately 21 million barrels, representing roughly 10% of the 2022 total release. However, current flow patterns suggest that Europe's proportional share of the 2026 release will be substantially larger.

Who Is Receiving the Barrels and Where Are They Going?

According to Bloomberg data cited by OilPrice.com, the allocation of the first 79.7 million barrels across 12 companies has been dominated by large commodity trading firms and integrated oil majors:

| Recipient | Barrels Allocated | Primary Function |

|---|---|---|

| Trafigura | ~21.4 million | Commodity trading, re-marketing |

| Shell Plc (NYSE: SHEL) | ~18.1 million | Refinery feedstock + trading |

| Marathon Oil (NYSE: MRO) | ~9.7 million | Refinery feedstock |

| BP Plc (NYSE: BP) | ~6.0 million | Refinery feedstock + trading |

| Vortexa Ltd + others | ~50 million (combined) | Distribution intermediary |

The concentration of early allocations among global trading firms such as Trafigura, Vitol, and Mercuria reveals something important about how SPR barrels actually move through global supply chains. These firms are not end-use refiners. They acquire barrels, optimise logistics and blending, and re-market cargoes into spot and term supply contracts.

This intermediation layer means that SPR barrels are not always flowing directly and immediately to the refineries that need them most. Instead, they are entering a commercial redistribution system that prioritises price arbitrage over proximity. This is not necessarily problematic, since trading intermediaries perform a genuine price discovery and logistics function, but it does mean that the market impact of SPR releases is diffused across multiple commercial steps before reaching the refinery gate.

Tracking Physical Flows: Rotterdam as the Entry Point

Shipping intelligence from Kpler confirms that supertanker Eagle Versailles is currently en route to Rotterdam, Netherlands, carrying approximately 2.1 million barrels of Bryan Mound medium sour crude. Rotterdam is not an arbitrary destination. As northwest Europe's largest crude oil trading and distribution hub, it serves as the central nervous system for European crude supply chains, with pipeline connections radiating into Germany, Belgium, and beyond.

In addition, SPR crude is also reaching other regions:

- Latin America: Peru's state oil company purchased a cargo of Bayou Choctaw crude in March 2026, scheduled for May delivery

- Asia: Some SPR barrels have been marketed toward Asian buyers, though the recent softening of oil prices may reduce the economic attractiveness of transatlantic cargoes for buyers facing higher freight costs

The Pricing Arbitrage Driving Europe's Transatlantic Buying

The fundamental economic logic driving Europe as key buyer of U.S. Strategic Petroleum Reserve oil is straightforward: U.S. SPR sour crude is being offered to European buyers at approximately $5 per barrel below local benchmark grades. With Brent crude trading near $105 per barrel, this discount is commercially meaningful for refiners operating on thin margins in a high-cost energy environment.

Trading firms including Vitol, Trafigura, Shell, and Mercuria have been acquiring medium sour grades from Bryan Mound and West Hackberry and marketing cargoes to refiners across the Mediterranean and northwest Europe at approximately $5 per barrel premiums to North Sea Dated on a delivered basis. The spread between their acquisition cost and delivered sale price constitutes the commercial incentive driving this flow. Understanding the broader context of crude oil trade geopolitics helps explain why these flows are accelerating at this particular moment.

When multiple major trading houses simultaneously market large volumes of discounted transatlantic crude into a regional market, the effect is not additive, it is recalibrating. Regional benchmark pricing adjusts downward, squeezing margins for producers of competing local grades.

This price pressure on local European crude grades has implications that extend well beyond immediate refinery economics. Norwegian producers, West African exporters, and even North Sea field operators are all competing against a temporary but substantial injection of discounted U.S. SPR crude into their primary sales market.

Why European Refiners Have No Better Alternative Right Now

Europe's structural energy vulnerability since 2022 has fundamentally altered the continent's crude procurement calculus. The loss of affordable Russian pipeline crude created a persistent feedstock deficit across Mediterranean and northwest European refinery systems that has never been fully resolved. Key supply realities facing European refiners include:

- Norway, Europe's largest domestic crude supplier, is pumping near capacity with minimal spare output buffer, as confirmed by recent production data

- Russian supply channels remain severed for most EU member states, with no equivalent pipeline alternative in place

- EU member nations have not tapped their own strategic reserves, with officials publicly stating there is no justification for domestic reserve drawdowns at this stage

- West African crude, while available, commands premium pricing without the $5/barrel discount available on U.S. SPR barrels

The absence of a cheaper, readily available regional alternative is precisely why Europe has moved so decisively to capture transatlantic SPR flows. These geopolitical trade tensions have, furthermore, accelerated European procurement decisions in ways that are reshaping long-term supply relationships.

The next major ASX story will hit our subscribers first

The Strait of Hormuz: Understanding the Chokepoint That Started Everything

The Strait of Hormuz remains effectively closed to most commercial shipping as of late April 2026. Iranian authorities have indicated the waterway will remain restricted, citing alleged violations of the ceasefire by the U.S. and Israel. The operational reality for commercial shipping is severe:

- Only approximately 5% of pre-conflict shipping volumes are currently transiting the waterway

- Insurance premiums for Hormuz-adjacent voyages have surged by up to 10 times since the conflict began

- Toll charges reportedly exceed $1 million per vessel

- All transiting vessels require IRGC-issued permits

- Physical hazards including sea mines, drone attacks, and seizure risk compound the commercial deterrents

Iranian authorities have, however, granted priority passage to vessels from a specific set of nations under a selective access regime:

| Permitted Nations | Conditions Required |

|---|---|

| China | Toll payment + IRGC permit compliance |

| Russia | Toll payment + IRGC permit compliance |

| India | Toll payment + IRGC permit compliance |

| Iraq | Toll payment + IRGC permit compliance |

| Pakistan | Toll payment + IRGC permit compliance |

This selective access framework has bifurcated global crude supply chains along geopolitical lines in a manner without modern precedent. Nations aligned with Western energy systems are effectively denied routine access to Middle Eastern crude exports, amplifying European dependence on Atlantic Basin alternatives precisely when those alternatives are needed most.

The IEA has characterised the conflict as the single largest energy security threat in the agency's history, a statement that reflects not merely the volume of crude displaced, but the duration and structural nature of the disruption. This oil market disruption has consequently forced energy ministries across Europe to reconsider their entire supply security frameworks.

Comparing 2022 and 2026: Two Crises, Two Drawdowns

Context matters when evaluating the current SPR deployment. Placing the 2026 release alongside the 2022 post-Ukraine drawdown reveals both the escalation in scale and the accumulating stress on U.S. reserve buffers:

| Metric | 2022 Post-Ukraine Release | 2026 IEA-Coordinated Release |

|---|---|---|

| Trigger Event | Russia's invasion of Ukraine | Middle East conflict / Hormuz closure |

| U.S. Contribution | ~180 million barrels | ~172 million barrels |

| IEA Total Volume | ~240 million barrels | 400+ million barrels |

| European Share | Significantly larger (ongoing) | |

| Repayment Timeline | Returns deferred to 2026 | Returns required by 2028 |

| SPR Level Post-Release | ~350-370 million barrels | Declining from ~415 million barrels |

| Market Price Impact | Temporary softening | Limited; structural deficit persists |

A less discussed but important dynamic is the cumulative nature of successive SPR drawdowns. The 2022 release depleted U.S. reserves to historically low levels. Only partial replenishment occurred before the 2026 crisis triggered a new drawdown cycle. Each successive emergency deployment leaves the reserve system thinner, narrowing the buffer available for future supply emergencies. This gradual erosion of strategic depth is a material long-term energy security risk for the United States.

The Risks That Complicate Europe's SPR Dependency

While the economics of purchasing discounted U.S. SPR crude are currently compelling for European refiners, several structural and market risks deserve careful consideration:

- Replenishment demand: The exchange mechanism means every barrel released today creates future crude demand when recipients must fulfil return obligations by 2028

- Grade mismatch at the margins: Bryan Mound medium sour crude is compatible with many European refineries but does not perfectly substitute for the light sweet grades that dominate North Sea and Mediterranean supply chains

- Price floor erosion: If Brent crude retreats from its current elevated level near $105/barrel, the $5/barrel discount narrows in absolute terms, potentially reducing European demand for transatlantic barrels

- Freight cost exposure: Transatlantic shipping adds both freight cost and voyage time compared to regional supply, making the economics more sensitive to oil price movements than domestic European sourcing

- Strategic dependency risk: Reliance on U.S. emergency reserves as a quasi-structural supply source creates a new form of energy dependency that is politically and logistically fragile

An emerging secondary signal worth monitoring is the acceleration of clean energy investment across Europe in response to the current energy shock. European rooftop solar installation orders have reportedly tripled as gas prices have surged. This suggests that the current crisis is simultaneously intensifying energy transition pressures at the consumer level, even as refiners scramble for emergency crude supply at the industrial level. Europe's emergence as a key buyer of U.S. SPR oil is, therefore, unfolding alongside a parallel acceleration of the continent's longer-term energy reorientation.

Frequently Asked Questions: Europe and U.S. SPR Oil

What grades of crude oil are being released from the U.S. SPR to Europe?

The primary grade flowing toward European buyers is medium sour crude sourced from the Bryan Mound SPR site in Texas. West Hackberry Sweet is also being marketed by trading firms. European Mediterranean refineries configured to process sour grades make these barrels a practical feedstock fit without costly refinery adjustments.

How much of the SPR release is going to Europe?

While precise final allocation data is still developing, shipping intelligence confirms supertankers are en route to Rotterdam carrying Bryan Mound sour crude. The 2022 precedent saw approximately 21 million barrels, roughly 10% of the total, reach Europe. Current flow patterns suggest Europe's proportional share in 2026 is substantially larger.

Is the SPR release lowering oil prices?

The $5/barrel discount on SPR sour crude provides refinery-level relief, but with Brent crude remaining near $105/barrel and the Strait of Hormuz still constraining global supply, the macroeconomic price impact is limited. Standard Chartered's analysis indicates the entire 400+ million barrel coordinated release covers only approximately 50 days of the supply deficit created by the Hormuz disruption.

When does the U.S. SPR oil need to be returned?

For 2026 loan tranches involving high-sulphur sour crude, the DOE requires repayment by 2028, with interest of up to 22%, typically payable in sweeter, higher-value crude grades rather than cash. The IEA's coordinated framework, which underpins the current market supply response, further governs how member nations structure their individual return obligations.

Why isn't Europe releasing its own strategic reserves?

EU officials have publicly stated there is no justification for tapping European strategic stocks at this stage, leaving member-nation reserves intact while European refiners instead purchase discounted U.S. SPR barrels through commercial trading channels. Consequently, Europe as key buyer of U.S. Strategic Petroleum Reserve oil has become the de facto mechanism through which the continent is managing its immediate supply gap.

This article is intended for informational and educational purposes only and does not constitute financial or investment advice. Oil price forecasts, supply estimates, and geopolitical scenarios referenced herein involve significant uncertainty. Past precedents from prior SPR release events may not be indicative of future market outcomes. Readers should conduct independent research and consult qualified financial advisers before making investment decisions related to energy markets or commodity exposure.

Want to Capitalise on the Next Major Commodity Discovery Before the Market Does?

While Europe scrambles for emergency crude supply and energy markets remain under structural pressure, Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across oil, gas, and more than 30 other commodities — turning complex data into actionable investment insights the moment they are announced. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.