June 15, 2026

Understanding Heavy Rare Earth Elements in Modern Defense Systems

The global defense industry operates within an intricate web of technological dependencies that few civilian observers fully comprehend. Modern military platforms rely on specialized materials whose scarcity creates strategic vulnerabilities that can determine the outcome of prolonged conflicts. At the heart of this materials challenge lies a category of elements that possess unique magnetic and electronic properties essential for next-generation weapons systems, making US strategic defence rare earths supply a critical national security priority.

Heavy rare earth elements represent the most critical subset of the seventeen lanthanide elements, with dysprosium and terbium emerging as particularly strategic materials. These elements enable the production of high-performance permanent magnets capable of maintaining their properties under extreme temperature and stress conditions encountered in military applications.

Strategic Defense Applications Requiring HREE

Military hardware demands materials that can withstand conditions far beyond civilian technology requirements. F-35 fighter aircraft incorporate dozens of permanent magnets containing dysprosium for actuators, sensors, and flight control systems that must function reliably at altitudes exceeding 50,000 feet and temperatures ranging from -65°F to 160°F.

Missile guidance systems rely on terbium-enhanced magnets for precision targeting mechanisms. These components must maintain magnetic field strength within tolerances of less than 0.1% over operational temperature ranges while resisting electromagnetic interference from defensive countermeasures.

• Radar Platform Integration: Phased array radar systems require dysprosium-based magnets for beam steering mechanisms

• Electronic Warfare Systems: Terbium enables compact, high-power electromagnetic pulse generation

• Navigation Systems: HREE-enhanced components provide GPS accuracy within three-metre tolerances under jamming conditions

• Communication Arrays: Military-grade transceivers depend on HREE magnets for signal amplification and filtering

Current Supply Vulnerability Metrics

The United States maintains strategic reserves that industry experts consider inadequate for extended conflict scenarios. Current stockpile levels provide approximately six months of heavy rare earth elements for defense applications, falling significantly short of the two to three-year buffer recommended by defense logistics specialists.

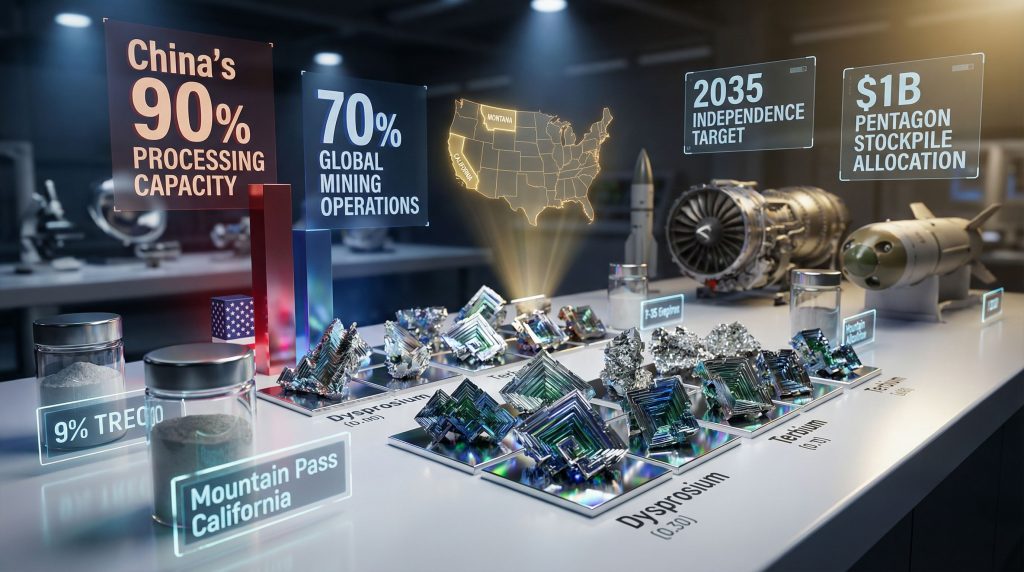

China controls approximately 90% of global rare earth processing capacity and 70% of mining operations, creating a single-point-of-failure vulnerability in American defense supply chains. Furthermore, this concentration enables potential export restrictions that could halt weapons production within quarters rather than years.

Historical precedents demonstrate the economic warfare potential of rare earth supply disruptions. In 2010, China temporarily restricted rare earth exports to Japan during diplomatic tensions, causing neodymium prices to increase by 500% within six months and highlighting the strategic leverage these materials provide.

When big ASX news breaks, our subscribers know first

Domestic US Rare Earth Project Development

American efforts to establish supply chain independence centre on developing domestic mining and processing capabilities that can substitute for foreign sources without compromising material quality or defense system performance. The approach requires coordination between geological resource development, advanced metallurgy, and defense procurement planning.

Mountain Pass California: Foundation Infrastructure

Mountain Pass represents the only currently operational rare earth mining facility in the United States, providing a baseline for domestic production capabilities. The facility produces primarily light rare earth elements with limited heavy rare earth content, necessitating additional sources for dysprosium and terbium requirements.

Recent developments include Pentagon partnership agreements focused on processing facility expansion and strategic minerals reserve contribution. The Department of Defense has committed to purchasing 100% of domestic magnet production for the first three years of expanded operations, providing revenue certainty for facility investments exceeding $150 million.

Processing facility upgrades target separation technology improvements that can extract higher purity heavy rare earth concentrates from existing ore bodies. These modifications require specialised chemical engineering expertise and environmental compliance systems that meet both civilian and military quality standards.

High-Grade Domestic Deposits

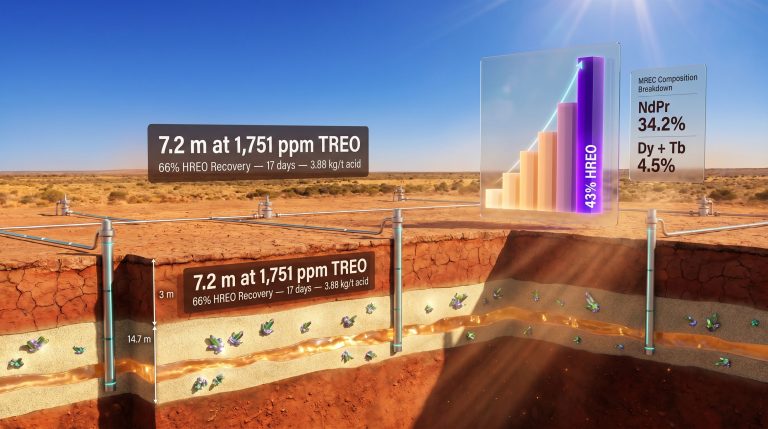

The Sheep Creek project in Montana has emerged as a potential game-changing resource for US strategic defence rare earths supply security. Independent laboratory analysis by Activation Laboratories and Idaho National Laboratory confirms rare earth oxide concentrations averaging 89,932 parts per million across a 7,277.5-acre land package.

This grade represents approximately 9% total rare earth oxide content, significantly higher than most global deposits and comparable to the highest-grade Chinese facilities. The geological formation consists of over 60 identified carbonatite intrusions, each potentially containing economic rare earth concentrations.

Table: US Domestic Rare Earth Project Comparison

| Project | Location | Grade (TREO) | Key Elements | Development Stage |

|---|---|---|---|---|

| Mountain Pass | California | 7.98% | Light REE focus | Operational |

| Sheep Creek | Montana | 9.0% | Heavy REE rich | Pre-development |

| Bear Lodge | Wyoming | 3.05% | Mixed REE profile | Feasibility stage |

| Round Top | Texas | 0.06% | Heavy REE + critical minerals | Pilot testing |

Heavy rare earth confirmation at Sheep Creek includes verified dysprosium and terbium presence, the two most strategically sensitive elements for defense applications. Moreover, metallurgical testing programmes are advancing processing flowsheet optimisation to maximise heavy rare earth recovery rates while minimising environmental impact.

Strategic Offtake Framework Development

Recent partnership announcements indicate growing coordination between domestic mining projects and defence-focused processing facilities. REalloys, a Nasdaq-listed company specialising in rare earth-to-magnet production, has established framework agreements for up to 10% offtake from Sheep Creek production.

This arrangement creates a potential pathway for domestically mined heavy rare earths to feed directly into defence stockpile programmes without foreign processing intermediaries. The agreement emphasises zero Chinese involvement at any supply chain stage, addressing defence security requirements for adversary-free sourcing.

Advanced midstream and downstream operations capability represents a critical bottleneck in US supply chain independence. Processing rare earth concentrates into defence-ready metals requires specialised separation chemistry, waste management protocols, and quality assurance systems that few facilities worldwide can provide.

Allied Nation Partnership Strategies

American rare earth reserves analysis extends beyond domestic resources to include strategic partnerships with allied nations that share democratic values and defence cooperation agreements. This approach reduces dependency on any single source whilst maintaining supply chain security through trusted international relationships.

Multi-Source Procurement Networks

REalloys CEO Lipi Sternheim emphasises a fundamentally different strategy compared to single-source dependency models. The company is partnering with highest-grade developers across allied nations to build diversified supply networks specifically designed to counteract Chinese market dominance.

Government collaboration plays a central role in identifying strategic assets that integrate with advanced midstream and downstream processing ecosystems. Consequently, this coordination fortifies supply chain security for protected and strategic markets whilst maintaining zero Chinese involvement at any stage.

• Canadian Rare Earth Integration: Cross-border processing agreements with Quebec and Northwest Territories projects

• Australian Mining Partnerships: Lynas Corporation separation technology collaboration and feed material agreements

• European Processing Initiatives: Joint research and development programmes for advanced separation methodologies

• Technology Transfer Protocols: Allied nation sharing of proprietary separation and refining techniques

Geographic Distribution Benefits

Diversified sourcing across multiple allied nations provides several strategic advantages beyond simple supply security. Political stability in democratic countries reduces the risk of supply interruptions due to government policy changes or diplomatic tensions.

Logistics optimisation through multiple ports and transportation routes prevents single-point-of-failure vulnerabilities in shipping and customs processing. In addition, allied nation regulatory frameworks typically align with US environmental and safety standards, simplifying quality assurance protocols.

Long-term offtake agreements spanning 10 to 20 years provide supply security whilst offering allied nations stable revenue streams for resource development. These partnerships create mutual dependencies that strengthen defence cooperation beyond rare earth supply considerations.

"Diversified allied-nation supply networks represent a fundamental shift from cost-based procurement to security-focused sourcing. Success requires sustained government commitment to premium pricing for strategic materials and long-term partnership agreements that extend beyond traditional commercial relationships."

Legislative Framework and Government Policy Support

Congressional action has established statutory requirements for rare earth supply chain independence that mandate specific timeline achievements and funding allocations. The legislative framework creates both procurement restrictions on adversarial sources and positive incentives for domestic development.

National Defense Authorization Act Mandates

Section 1411 of the National Defense Authorization Act for 2024 establishes complete independence from adversarial nation rare earth sources by 2035. This mandate requires the Department of Defense to develop alternative supply chains capable of supporting all defence applications without Chinese materials.

The timeline creates intermediate milestones for domestic production capacity, strategic reserve accumulation, and allied nation partnership development. Each phase requires coordinated investment between government funding and private sector development.

Critical Materials Security Program allocation of $1 billion for Pentagon stockpile development provides immediate funding for strategic reserve enhancement. These resources target heavy rare earth elements specifically, addressing the most vulnerable aspects of current supply chains.

Financial Incentives and Investment Programs

Defense Production Act utilisation enables emergency procurement authorities and accelerated development timelines for critical projects. Recent invocations have focused on processing facility development rather than mining operations, addressing the primary bottleneck in domestic supply chain completion.

• DOE Loan Guarantee Programs: $150 million+ financing for rare earth processing facilities with defence offtake agreements

• Tax Credit Structures: Domestic mining and processing incentives specifically targeting heavy rare earth elements

• Strategic Partnership Funding: Government-industry collaboration models for technology development and capacity expansion

• R&D Grants: Advanced separation technology development focused on environmental compliance and efficiency improvement

Buy American provisions mandate domestic content requirements for defence contracts involving rare earth materials. However, these regulations create guaranteed market demand for domestic production whilst premium pricing compensates for higher development costs compared to Chinese alternatives.

Economic and Technological Implementation Challenges

Establishing competitive rare earth processing capabilities requires overcoming significant technological barriers that have historically favoured Chinese integrated production systems. The challenges span metallurgical complexity, environmental compliance, capital requirements, and specialised workforce development.

Processing Technology Barriers

Heavy rare earth separation demands multi-stage chemical processing using specialised solvents and precipitation techniques that require precise temperature and pH control throughout production runs lasting several weeks. Dysprosium and terbium extraction typically achieves yields between 85-92%, with higher purity levels requiring additional processing cycles that increase costs exponentially.

Environmental compliance represents a substantial technological challenge due to the acidic waste streams and radioactive byproducts associated with rare earth processing. Modern facilities require closed-loop water systems, waste neutralisation equipment, and long-term radioactive material storage capabilities that can add 30-40% to facility construction costs.

• Separation Chemistry Complexity: Multi-stage solvent extraction requiring specialised equipment and process control

• Waste Management Protocols: Radioactive byproduct handling and long-term storage requirements

• Quality Control Systems: Defence-grade material specifications demanding 99.9%+ purity levels

• Equipment Manufacturing: Specialised corrosion-resistant processing equipment with limited global suppliers

Capital intensity requirements for complete processing facilities range from $500 million to over $1 billion depending on capacity and integration levels. These investments require sustained government support or long-term offtake agreements to achieve acceptable return on investment timelines.

Workforce Development Requirements

Technical expertise shortages represent a critical constraint on rapid capacity expansion. Specialised metallurgical and chemical engineering talent with rare earth processing experience exists primarily in China, creating technology transfer challenges for US facility development.

Universities are expanding rare earth research programmes to develop domestic expertise, but developing operational-level competence typically requires 5-7 years of hands-on experience. This timeline constraint limits the speed of domestic capacity development regardless of funding availability.

Training programmes coordinated between industry and academic institutions focus on separation chemistry, process optimisation, and environmental compliance specific to rare earth applications. Furthermore, government funding supports fellowship programmes and research partnerships that accelerate knowledge transfer.

Strategic Reserve Enhancement and Defense Readiness

Current US rare earth stockpiles provide insufficient buffer capacity for extended conflict scenarios, necessitating substantial reserve expansion focused specifically on heavy rare earth elements critical to advanced weapons systems. Strategic stockpile management requires balancing immediate availability with long-term material integrity.

Current Reserve Assessment Limitations

Six-month supply limitations reflect historical procurement patterns optimised for peacetime consumption rather than wartime production requirements. Extended conflict scenarios could require sustained weapons production at levels 300-500% above current peacetime rates for multi-year periods.

Critical element prioritisation focuses on dysprosium and terbium as the most supply-constrained materials with the highest defence impact. Current reserves of these elements provide even shorter duration coverage, potentially limiting missile production within 3-4 months of conflict initiation.

Storage protocols for rare earth materials require specialised environmental controls to prevent oxidation and contamination that can render materials unsuitable for defence applications. Proper storage facilities with controlled atmosphere systems represent substantial infrastructure investments beyond material procurement costs.

Target Reserve Objectives and Rotation Systems

Two to three-year supply buffer objectives align with defence logistics planning for major conflict scenarios requiring sustained domestic weapons production. Achieving these levels requires coordinated procurement from multiple domestic and allied sources over several years.

Strategic Reserve Target Metrics:

• Dysprosium Reserve: 850 metric tons for three-year conflict scenario coverage

• Terbium Reserve: 425 metric tons for extended defence production requirements

• Neodymium Reserve: 2,100 metric tons for broader weapons system applications

• Geographic Distribution: Minimum five storage locations across different climate zones

Material rotation and refresh programmes prevent degradation whilst maintaining strategic readiness. Regular quality testing ensures stored materials meet defence specifications throughout storage periods, with cycling programmes that release older inventory to civilian markets whilst acquiring fresh supplies.

Emergency release mechanisms enable rapid deployment of strategic reserves to defence contractors within 48-72 hours of authorisation. Pre-positioned logistics networks and transportation agreements facilitate distribution without relying on commercial supply chains that might be disrupted during crisis periods.

The next major ASX story will hit our subscribers first

Investment Opportunities in Domestic Rare Earth Development

The convergence of national security requirements, government funding commitments, and supply chain vulnerabilities creates substantial investment opportunities across the rare earth value chain. Public-private partnership models provide risk mitigation whilst enabling participation in strategic resource development.

Government-Backed Financing Models

Loan guarantee programmes through the Department of Energy reduce private investor risk whilst accelerating project development timelines. Recent commitments exceed $150 million specifically for rare earth processing facility development with defence department offtake agreements providing revenue certainty.

Revenue sharing agreements with government agencies create stable cash flow streams that support project financing at favourable interest rates. These arrangements typically include price floor mechanisms that protect against Chinese market manipulation whilst sharing upside potential during supply shortage periods.

• Infrastructure Cost-Sharing: Government co-investment in processing facility development with technology transfer requirements

• Research Partnerships: Joint R&D initiatives for advanced separation technology with intellectual property sharing agreements

• Tax Incentive Structures: Accelerated depreciation and investment credits specifically targeting heavy rare earth projects

• Strategic Partnership Frameworks: Long-term government commitments providing investment certainty for private capital

Market Opportunity Valuation

Domestic demand growth encompasses both defence applications and civilian technology expansion requiring secure supply chains. Annual US critical minerals strategy imports currently exceed $2-3 billion, representing the addressable market for import substitution through domestic production.

Export potential to allied nations creates additional market opportunities as European and Pacific partners seek Chinese supply alternatives. NATO standardisation agreements and defence cooperation treaties facilitate market access for US-produced materials meeting allied defence specifications.

Vertical integration benefits enable companies controlling mine-to-magnet production chains to capture value across the entire supply chain whilst providing supply security that commands premium pricing. Defence contractors increasingly prioritise supply security over cost minimisation for critical materials.

Global Supply Chain Transformation Implications

American rare earth independence initiatives will fundamentally reshape global supply chains and geopolitical relationships surrounding critical materials. The transition creates both opportunities for allied cooperation and risks of escalating resource competition with adversarial nations.

Geopolitical Response Scenarios

Chinese market responses to reduced US demand could include accelerated export restrictions to other nations, creating supply pressures that drive additional countries toward domestic development or allied partnerships. Price manipulation through dumping or supply constraints represents a likely competitive response.

Allied nation coordination becomes essential as collective bargaining power enables smaller countries to negotiate favourable terms with alternative suppliers whilst sharing development costs and technical expertise. Coordinated stockpiling and emergency sharing agreements strengthen overall alliance security.

The rare earth upgrade breakthrough acceleration between democratic nations creates competitive advantages in processing efficiency and environmental compliance that could eventually challenge Chinese cost leadership through productivity improvements rather than labour cost differences.

Long-term Strategic Outcomes Assessment

Defence capability assurance through supply chain independence enables sustained weapons production regardless of diplomatic tensions or trade disputes. This capability provides strategic deterrence value beyond the immediate supply security benefits.

Economic leverage restoration reduces Chinese influence over US defence planning and procurement decisions whilst creating leverage for broader trade negotiations. For instance, successful US strategic defence rare earths supply independence demonstrates domestic capability for other critical material supply chains.

Innovation catalyst effects emerge as government investment in rare earth technology development creates spillover benefits for civilian applications including renewable energy, electric vehicles, and advanced manufacturing. These secondary benefits help justify the premium costs of domestic development.

The transformation timeline extends through 2035, requiring sustained political commitment across multiple presidential administrations and congressional sessions. Success depends on maintaining bipartisan support for strategic resource development regardless of broader political changes.

International collaboration frameworks established for rare earth supply security create templates for addressing other critical material dependencies including lithium, cobalt, and specialised semiconductor materials. However, the United States-Australia Framework for securing critical minerals provides lasting strategic value through established institutional relationships and cooperation mechanisms.

Moreover, ongoing rare earth market talks between allies continue to shape the future landscape of US strategic defence rare earths supply security, ensuring that democratic nations maintain technological superiority whilst reducing dependence on adversarial sources.

Disclaimer: This article contains forward-looking statements and strategic analysis that involve inherent uncertainties. Rare earth market conditions, government policies, and international relationships may change significantly from current assumptions. Readers should conduct independent research and consult qualified professionals before making investment or business decisions based on this information.

Are You Tracking the Next Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, providing subscribers with immediate access to strategic opportunities in rare earths and critical minerals before broader market awareness. Begin your 14-day free trial today to position yourself ahead of the market in this rapidly evolving sector.