June 15, 2026

The Rare Earth Equation That Western Strategists Cannot Ignore

Permanent magnets are quietly embedded in nearly every technology that defines the modern economy. From the motors inside electric vehicles to the pitch-control systems on offshore wind turbines, and from missile guidance units to the drive trains of military drones, these magnets depend on a precise cocktail of rare earth elements that the world currently sources from a dangerously narrow geographic base. China controls an estimated 85 to 90 percent of global rare earth separation capacity and an even higher share of finished magnet production, according to the U.S. Geological Survey. For Western industrial planners, that concentration is not merely an economic inconvenience; it is a structural vulnerability with direct implications for energy transition security and defence readiness.

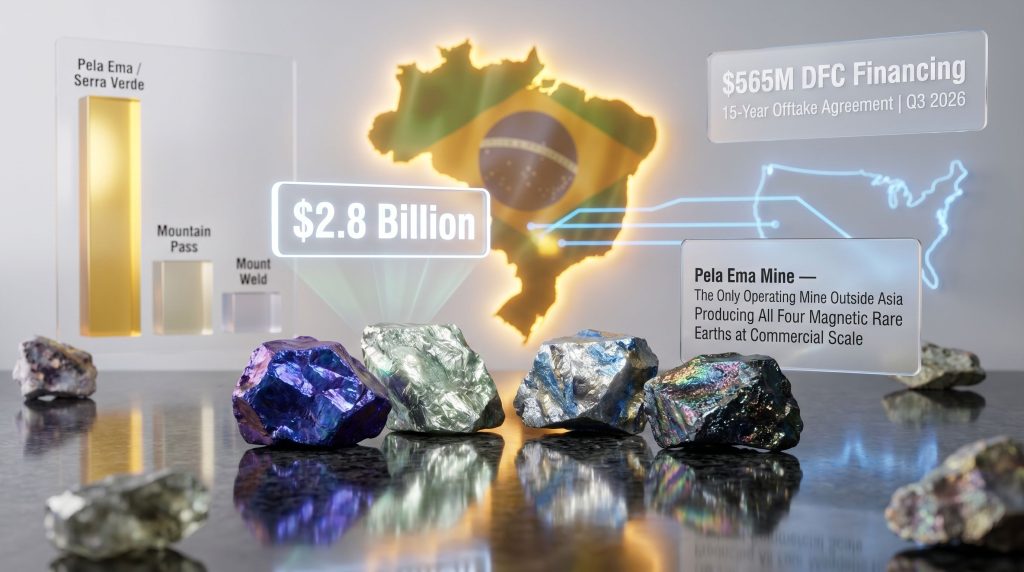

It is against this backdrop that the USA Rare Earth acquisition in Brazil has attracted scrutiny well beyond the mining investment community. The proposed purchase of Serra Verde, operator of the Pela Ema ionic clay mine, for approximately $2.8 billion is not simply a large M&A transaction. It is arguably the most consequential non-Chinese rare earth deal of the current decade, precisely because the asset being acquired occupies a category of its own in the global supply landscape.

When big ASX news breaks, our subscribers know first

Understanding the Serra Verde Asset and Why It Stands Apart

The Pela Ema Mine: One of a Kind Outside Asia

Serra Verde's Pela Ema mine, located in the Brazilian state of Goiás, hosts what analysts currently identify as the only commercially operating mine outside Asia capable of producing all four magnetic rare earth elements simultaneously: neodymium, praseodymium, dysprosium, and terbium. That distinction carries enormous weight.

Most Western rare earth operations produce meaningful quantities of the light rare earths (LREEs) neodymium and praseodymium, which are the primary inputs for standard NdFeB permanent magnets. However, high-performance magnets used in demanding applications such as EV traction motors operating at elevated temperatures, advanced wind turbine generators, and defence-grade systems require the addition of dysprosium and terbium to maintain coercivity. These two heavy rare earth elements (HREEs) are extraordinarily scarce outside of China's ionic clay deposits in Jiangxi Province, and Serra Verde's Pela Ema deposit replicates that same ionic clay geology in South America.

Why Ionic Clay Geology Changes the Economics

Ionic clay rare earth deposits differ fundamentally from the hard-rock carbonatite and monazite-bearing systems that underpin most non-Chinese producers. In an ionic clay deposit, rare earth ions are physically adsorbed onto clay mineral surfaces rather than locked within crystalline mineral structures. The practical consequence is transformative for project economics:

- No grinding or fine crushing required: Ore does not need the energy-intensive comminution circuits that add capital and operating cost to hard-rock projects.

- Heap leaching or in-situ leaching compatible: Rare earth ions can be displaced from clay surfaces using dilute ammonium sulphate or similar lixiviant solutions, dramatically simplifying the metallurgical flowsheet.

- Lower strip ratios in many deposits: Ionic clay mineralisation is often found at or near the surface as a weathered profile, reducing waste movement costs.

- Faster ramp-up potential: The absence of complex mineral processing circuitry means projects can reach production targets more quickly than comparable hard-rock developments.

The trade-off is that ionic clay deposits typically carry lower total rare earth oxide grades than carbonatite systems, but the relative enrichment of HREEs and the favourable processing characteristics often more than compensate on a value-per-tonne basis.

Breaking Down the $2.8 Billion Transaction

Deal Structure and Financial Architecture

The acquisition is structured predominantly as a stock transaction, reflecting both the scale of the deal and the need to preserve cash for operational and expansion purposes. Furthermore, the stock-heavy structure aligns vendor returns with the combined entity's future performance.

| Deal Component | Detail |

|---|---|

| Total Consideration | ~$2.8 billion |

| Cash Component | ~$300 million |

| Stock Component | ~126.9 million newly issued shares |

| Target | Serra Verde (Brazil) |

| Core Asset | Pela Ema mine and integrated processing facility |

| Expected Closing | Q3 2026 |

The stock-heavy structure means existing USA Rare Earth shareholders will experience dilution, but it also conserves liquidity at a time when the company is simultaneously managing its U.S. asset base and planning downstream expansion. The $300 million cash component represents a meaningful upfront commitment, while the share consideration ties vendor returns to the combined entity's future performance, aligning incentives between the parties.

The DFC Financing Package and Offtake Agreement

Two structural features of the Serra Verde deal make it considerably more de-risked than a typical emerging-market mining acquisition. As reported by Chemical & Engineering News, this transaction has drawn significant institutional attention precisely because of these features.

First, the U.S. International Development Finance Corporation (DFC) has committed a $565 million financing package to support Serra Verde's operations and expansion trajectory. The DFC is a U.S. government development finance institution whose mandate includes advancing American foreign policy and national security interests through strategic investments. Its financial commitment to Serra Verde reflects an institutional assessment that the asset serves U.S. critical mineral security objectives.

Importantly, this financing was extended to Serra Verde as an entity, and investors should note that its transfer and continuity under new ownership would be subject to confirmation as part of the deal close process.

Second, a 15-year offtake agreement is in place, providing a long-duration revenue anchor for the asset. Offtake agreements of this length are rare in the rare earth sector, where price volatility and market opacity have historically deterred long-term supply commitments. A 15-year term effectively transforms a meaningful portion of Serra Verde's future production into contracted revenue, substantially improving the bankability of the asset.

The combination of sovereign-backed project financing and a decade-and-a-half offtake commitment represents a risk profile that most greenfield rare earth projects will never achieve, making Serra Verde an unusually well-structured upstream acquisition target.

How Pela Ema Compares to the Western Rare Earth Peer Group

The rare earth sector outside China has advanced considerably over the past decade, but gaps in the supply picture remain stark when examined at the HREE level. Indeed, rare earth supply chains continue to expose critical vulnerabilities for Western economies.

| Producer | Country | Deposit Type | Magnetic REE Profile | Stage |

|---|---|---|---|---|

| Pela Ema (Serra Verde) | Brazil | Ionic Clay | All four magnetic REEs (incl. Dy, Tb) | Commercial |

| Mountain Pass (MP Materials) | USA | Carbonatite | Primarily NdPr, minimal HREEs | Commercial |

| Mount Weld (Lynas) | Australia | Carbonatite | Primarily NdPr, minimal HREEs | Commercial |

| Various projects | Canada, Africa, Australia | Mixed | Partial REE profiles | Development stage |

MP Materials and Lynas Rare Earths are legitimate, scaled producers, but their deposit types yield concentrates heavily weighted toward LREEs. Neither operation provides meaningful volumes of dysprosium or terbium. This means that even as Western LREE supply has improved, the HREE supply problem has remained structurally unresolved. Serra Verde's ionic clay profile directly addresses that gap, which is why the USA Rare Earth acquisition in Brazil is being tracked so closely by supply chain analysts across the defence and clean energy sectors.

USA Rare Earth's Mine-to-Magnet Vision

Vertical Integration as a Competitive Moat

USA Rare Earth has articulated a mine-to-magnet integration strategy that seeks to capture value across the entire rare earth supply chain rather than stopping at concentrate or separated oxide production. Adding Serra Verde's upstream output to its existing U.S. asset portfolio would give the company rare earth feedstock spanning the Americas, from Brazilian ionic clay all the way through to magnet manufacturing on U.S. soil.

Full vertical integration in the rare earth sector involves several distinct value-adding stages:

- Mining and ore extraction from the deposit

- Beneficiation to produce a mixed rare earth concentrate

- Separation into individual rare earth oxides or carbonates

- Reduction and alloying to produce rare earth metals and alloys

- Magnet manufacturing to produce sintered or bonded NdFeB permanent magnets

China currently dominates every stage of this chain. Western companies have made real progress at stage one, and Lynas has demonstrated capability through stage three, but stages four and five remain almost entirely absent from the Western industrial base. USA Rare Earth's ambition to bridge that gap explains why securing a reliable, multi-element upstream source in Brazil is a prerequisite for the broader strategy to function.

Brazil's Underappreciated Rare Earth Endowment

Brazil holds some of the largest rare earth reserves on the planet, yet has historically contributed almost nothing to global rare earth supply. The country's geological endowment includes not only the ionic clay deposits around the Pela Ema area but also substantial carbonatite-hosted deposits and monazite-bearing coastal sands.

Despite this resource richness, a combination of regulatory complexity, infrastructure gaps, and historically depressed rare earth prices kept Brazil on the periphery of the global market for decades. The Serra Verde acquisition may consequently represent an inflection point for Brazilian rare earths more broadly, potentially attracting further investment into the country's underexplored rare earth regions.

Political Resistance and Regulatory Risk in Brazil

The Nature of the Opposition

The deal is not proceeding without friction. A Brazilian political party has formally moved to challenge the acquisition, raising concerns rooted in resource nationalism and the question of who benefits when a country's strategically significant mineral wealth passes into foreign hands. This type of opposition is becoming increasingly common across resource-rich nations as governments reassess the terms on which critical mineral assets are made available to foreign capital.

The specific concerns driving Brazilian opposition include:

- Whether the economic benefits of Serra Verde's expanded production will accrue meaningfully to Brazilian workers and communities

- Whether foreign ownership of a nationally significant rare earth asset is consistent with Brazil's long-term resource sovereignty interests

- How the transaction interacts with Brazil's regulatory framework governing foreign investment in strategic sectors

Brazil has a history of asserting sovereign interests over strategic resource sectors, most notably in oil and gas through Petrobras and its pre-salt framework. Whether rare earths will be treated with comparable sensitivity is an open question that the regulatory process will need to answer. Furthermore, how Brazil handles this transaction will likely influence rare earth geopolitics across the broader region.

Scenario Analysis: Three Possible Outcomes

| Scenario | Key Driver | Supply Chain Impact | Investor Implication |

|---|---|---|---|

| A: Closes as structured (Q3 2026) | Regulatory clearance granted | Immediate HREE supply diversification | Validates USA Rare Earth integration thesis |

| B: Restructured under political pressure | Political compromise with partial state involvement | Partial diversification; reduced control | Diluted upside, longer timeline |

| C: Blocked entirely | Nationalist opposition succeeds | Western HREE gap persists | Significant strategic setback for USA Rare Earth |

Risk consideration: The regulatory outcome in Brazil carries implications beyond this single transaction. How Brazil handles foreign acquisition of a nationally significant rare earth operation will likely be observed carefully by other resource-holding nations across Latin America and beyond.

The next major ASX story will hit our subscribers first

Demand Acceleration and Why Timing Matters

The Convergence of Three Demand Vectors

The urgency surrounding the USA Rare Earth acquisition in Brazil is inseparable from the demand dynamics unfolding across three interconnected sectors. In addition, the broader surge in critical minerals demand is intensifying pressure on existing supply chains.

Electric vehicles: NdFeB permanent magnet motors are the dominant drivetrain architecture for battery electric vehicles. As EV penetration accelerates globally, demand for both NdPr and the HREE additions that enable high-temperature performance is growing at a pace that existing non-Chinese supply cannot match.

Wind energy: Offshore and onshore wind turbines using direct-drive permanent magnet generators are gaining market share over geared alternatives due to their reliability and lower maintenance requirements. Each multi-megawatt direct-drive turbine can require substantial quantities of rare earth magnets, with HREE content becoming more significant as turbines are deployed in higher-temperature environments.

Defence systems: Advanced weapons platforms, electronic warfare systems, precision-guided munitions, and autonomous drone systems all rely on rare earth permanent magnets. The growing sophistication of defence electronics has made HREE supply a genuine national security consideration for the United States and its allies.

The convergence of these three demand vectors, against a backdrop of persistent Chinese supply concentration, is what gives the Serra Verde asset its outsized strategic significance relative to its current production volume. Moreover, Americas rare earth supply considerations are becoming central to how policymakers approach long-term industrial strategy.

Frequently Asked Questions

What makes Serra Verde's Pela Ema mine different from other rare earth mines?

Pela Ema is an ionic clay deposit, which means rare earth ions sit loosely adsorbed on clay mineral surfaces rather than locked within hard crystalline rock. This geology enables simpler, lower-cost processing and, critically, produces all four magnetic rare earths including the heavy elements dysprosium and terbium. No other operating mine outside Asia currently achieves this combination at commercial scale.

Why are dysprosium and terbium so strategically important?

These two heavy rare earths are added to NdFeB magnets to improve their resistance to demagnetisation at elevated operating temperatures. Without them, high-performance magnets in EV traction motors, wind turbine generators, and defence systems would lose effectiveness under thermal stress. China currently controls the overwhelming majority of global dysprosium and terbium supply, as analysed by MarketWatch in its coverage of the Serra Verde transaction.

What is the DFC and what does its involvement signal?

The U.S. International Development Finance Corporation is a U.S. government institution that deploys capital in support of American foreign policy and development objectives. Its $565 million financing commitment to Serra Verde reflects a strategic assessment that the asset is important to U.S. critical mineral security. Investors should treat this as a signal of institutional interest rather than a guarantee of project outcomes.

What is the timeline and what could delay it?

The deal is expected to close in Q3 2026, subject to regulatory approvals in Brazil and other standard conditions. Political opposition from a Brazilian political party represents the most visible risk to that timeline, though the ultimate regulatory pathway remains open.

Key Takeaways for Investors and Industry Observers

- The $2.8 billion Serra Verde acquisition is the largest non-Chinese rare earth M&A transaction of the current decade by strategic significance, not just by dollar value

- Pela Ema's ionic clay geology produces all four magnetic rare earths, including the HREEs dysprosium and terbium that remain almost entirely absent from Western supply chains

- The $565 million DFC financing and 15-year offtake agreement provide structural risk mitigation that is genuinely unusual for an asset of this type

- Political opposition in Brazil introduces material execution risk that should be monitored closely through the expected Q3 2026 close date

- The outcome of this regulatory process may influence how other Latin American nations approach foreign investment in critical mineral assets going forward

- For investors, the deal's strategic logic is compelling, but the gap between strategic logic and regulatory reality is where risk resides

This article contains forward-looking statements and scenario analysis that are speculative in nature. Readers should conduct their own due diligence and seek independent financial advice before making investment decisions. All figures cited are based on publicly available information and are subject to change as the transaction progresses through regulatory review.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across rare earths and more than 30 other commodities — turning complex data into actionable investment insights. Explore historic discoveries and their returns to understand what early positioning can mean, then start your 14-day free trial at Discovery Alert to secure your market-leading edge.