June 22, 2026

The global transition toward renewable energy and defence modernisation has created unprecedented demand for permanent magnets, yet Western nations remain critically dependent on Chinese processing capabilities for the rare earth elements essential to these technologies. This dependency represents both a strategic vulnerability and a market opportunity for companies capable of establishing integrated supply chains outside China's sphere of influence. The proposed USA Rare Earth French magnet plant exemplifies this strategic shift toward Western-controlled rare earth infrastructure.

Traditional mining companies have historically focused on extraction operations, leaving processing and manufacturing to downstream partners. However, the current geopolitical landscape increasingly rewards vertical integration models that eliminate foreign intermediaries, particularly in sectors deemed critical to national security. The race to establish Western-controlled rare earth value chains has accelerated dramatically, driven by policy support mechanisms and growing recognition of supply chain fragility.

USA Rare Earth's Transatlantic Integration Strategy

Coordinated Investment Architecture

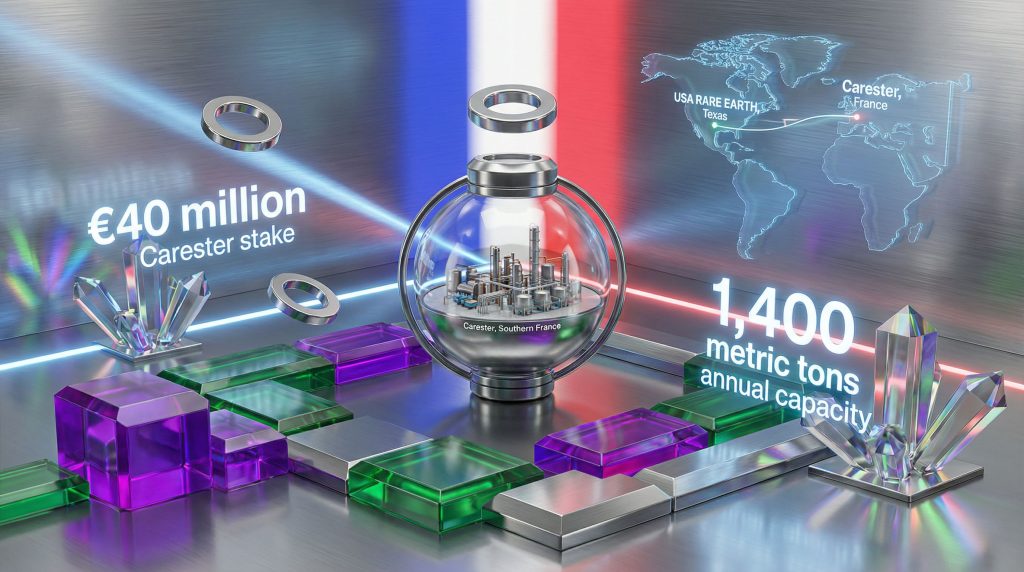

USA Rare Earth's €40 million acquisition of a 12.5% stake in French processing firm Carester represents more than traditional corporate expansion. The investment mirrors an identical stake purchased simultaneously by InfraVia, a critical minerals fund backed by French state resources, creating a coordinated US-European partnership structure.

This parallel investment approach demonstrates sophisticated geopolitical alignment between Western allies seeking to reduce dependency on Chinese rare earth processing. Furthermore, the $1.6 billion debt-and-equity funding package USA Rare Earth received from the US government in January 2024 provides the financial foundation for this international expansion strategy.

The timing correlation between US government funding and European CRM facility development suggests policy-level coordination extending beyond individual corporate decisions. Such alignment indicates Western governments view rare earth supply chain diversification as a strategic priority warranting substantial public investment.

Fifteen-Year Supply Agreements Create Structural Lock-In

The Carester partnership includes comprehensive 15-year supply and offtake agreements establishing contractual frameworks for material flow from USA Rare Earth's Round Top mine in Texas through French processing facilities. This arrangement enables the company to send raw materials for processing while securing purchase rights for resulting rare earth oxides.

Long-term contract structures eliminate spot market exposure and provide predictable feedstock costs for downstream magnet manufacturing operations. In addition, the extended timeframe reflects confidence in sustained demand growth from automotive, renewable energy, and defence sectors requiring permanent magnet technologies.

Key Components of USA Rare Earth's Integrated Strategy:

- Upstream Security: Round Top mine provides heavy rare earth extraction capability

- Processing Partnership: Carester stake ensures access to European refining capacity

- Manufacturing Footprint: Stillwater, Oklahoma facility plus proposed French magnet plant

- Geographic Diversification: Operations spanning Texas, Oklahoma, and southern France

When big ASX news breaks, our subscribers know first

Carester's Strategic Position in European Critical Minerals Development

Technical Specifications of the Caremag Facility

Carester's Caremag processing unit represents sophisticated rare earth refining infrastructure designed for 1,400 metric tons annual production of rare earth oxides. The facility processes dual feedstock streams: recycled permanent magnets and mining concentrates, providing input source diversification that reduces dependency on primary extraction operations.

The €216 million funding structure combining Japanese investment with French state support demonstrates international recognition of Europe's need for domestic rare earth processing capability. This capital commitment reflects the technical complexity and infrastructure requirements necessary for competing with established Chinese processing operations.

Heavy rare earth elements, particularly dysprosium and terbium, require specialised separation techniques due to their similar chemical properties and low natural abundance. The Caremag facility's focus on these elements addresses specific supply bottlenecks in permanent magnet manufacturing, where these materials serve as essential additives for high-temperature performance applications.

Recycling Integration and Circular Economy Benefits

The facility's capability to process recycled permanent magnets alongside primary mining concentrates creates operational flexibility whilst supporting circular economy principles. End-of-life magnets from electric vehicles, wind turbines, and consumer electronics contain concentrated rare earth elements that can be recovered through specialised processing.

Recycling reduces environmental impact compared to primary mining whilst providing cost advantages when magnet scrap becomes available at scale. This dual-input model positions Carester to capitalise on both growing primary demand and increasing availability of end-of-life magnet materials as clean energy infrastructure reaches replacement cycles.

Carester's Operational Advantages:

- Location proximity to European automotive manufacturing clusters

- Regulatory environment supporting critical minerals processing investments

- Transportation infrastructure enabling efficient feedstock import and product distribution

- Technical expertise in heavy rare earth separation methodologies

Market Dynamics Driving Western Rare Earth Development

Chinese Processing Dominance and Strategic Vulnerabilities

China currently controls an estimated 60-70% of global rare earth processing capacity, creating single-point-of-failure risks for Western manufacturers requiring these materials. This concentration extends beyond mining operations to encompass the more technically complex refining and separation processes essential for producing magnet-grade materials.

Chinese processing advantages stem from decades of accumulated technical expertise, lower environmental compliance costs, and integrated supply chain infrastructure connecting mining operations directly to manufacturing facilities. Consequently, Western companies attempting to compete must overcome both cost disadvantages and technical knowledge gaps.

The strategic vulnerability becomes apparent during geopolitical tensions when export restrictions or trade disputes can disrupt critical material supplies. Recent policy initiatives in both the United States and European Union specifically target this dependency through funding mechanisms supporting domestic processing development.

Permanent Magnet Demand Projections

Growing demand for permanent magnets in electric vehicle motors, wind turbine generators, and defence applications creates market pull-through effects supporting rare earth processing investments. Automotive sector electrification alone represents substantial volume growth potential as manufacturers transition from internal combustion engines.

Wind energy expansion requires large quantities of permanent magnets for direct-drive turbine generators, particularly offshore installations where reliability demands favour permanent magnet technologies. Defence applications, whilst smaller in volume, command premium pricing for high-performance magnets meeting military specifications.

Demand Growth Vectors:

- Electric Vehicles: Motor and battery cooling system applications

- Wind Energy: Direct-drive generator systems for offshore installations

- Defence Systems: Guidance systems, electronic warfare equipment, and propulsion

- Consumer Electronics: High-efficiency motors and speakers

USA Rare Earth's Business Model Evolution

From Mining to Integrated Manufacturing

USA Rare Earth's transformation from single-operation mining company to vertically integrated manufacturer represents fundamental business model evolution. The company's Round Top mine in Texas provides upstream feedstock security, whilst processing partnerships and manufacturing facilities create value-added revenue streams.

The Stillwater, Oklahoma magnet manufacturing facility, expected to begin operations in 2024, establishes domestic US production capability for North American markets and defence applications. This facility complements the proposed USA Rare Earth French magnet plant, which would serve European automotive and renewable energy sectors.

Geographic distribution of manufacturing capabilities provides operational resilience whilst enabling market-specific customisation for regional customer requirements. Additionally, this approach supports the broader defence-critical materials strategy being implemented across allied nations.

Financial Structure and Capital Allocation Strategy

The company's $1.6 billion government funding package provides substantial capital for facility development whilst demonstrating official recognition of rare earth supply security as a national priority. This funding structure enables aggressive expansion without diluting existing shareholders through equity financing.

USA Rare Earth's Integrated Operations Timeline:

| Facility | Location | Function | Status | Timeline |

|---|---|---|---|---|

| Round Top Mine | Texas, USA | Heavy rare earth extraction | Development | 2026-2027 production target |

| Wheat Ridge Pilot | Colorado, USA | Hydrometallurgical testing | Operational | Pilot scale validation |

| Stillwater Plant | Oklahoma, USA | Magnet manufacturing | Launch phase | Commercial production 2024 |

| French Facility | Southern France | Magnet manufacturing | Planning | Timeline undisclosed |

Revenue diversification through multiple operational stages creates cash flow stability whilst reducing exposure to commodity price volatility. However, processing and manufacturing operations typically command higher margins than primary extraction, improving overall profitability potential.

Technical Challenges in European Magnet Production

Heavy Rare Earth Processing Complexity

Heavy rare earth elements require sophisticated separation techniques due to their similar ionic radii and chemical properties. Dysprosium and terbium separation demands precise control of hydro-metallurgical processes, including ion exchange resins, solvent extraction cascades, and precipitation chemistry.

Quality control requirements for automotive and aerospace applications necessitate consistent purity specifications and trace element monitoring. Contaminants affecting magnetic properties can render finished products unsuitable for high-performance applications, requiring comprehensive testing protocols throughout processing operations.

The Carester facility's ability to process mixed rare earth streams from both recycled magnets and mining concentrates requires flexible processing protocols. Recycled materials often contain alloy additions and oxidation products not present in primary ores, demanding specialised treatment methodologies.

Technology Transfer and Workforce Development

Establishing European magnet production capabilities requires transferring specialised knowledge from USA Rare Earth's existing operations. This includes process optimisation techniques, quality control methodologies, and safety protocols specific to rare earth handling.

Critical Technical Requirements:

- Separation Chemistry: Ion exchange and solvent extraction expertise

- Quality Assurance: Purity testing and magnetic property validation

- Environmental Compliance: EU regulations for rare earth processing

- Safety Protocols: Handling procedures for radioactive elements present in rare earth ores

Training programmes must address both technical processing knowledge and regulatory compliance requirements specific to European operations. The complexity of rare earth chemistry requires experienced personnel familiar with hydrometallurgical principles and analytical techniques.

Supply Chain Resilience and Strategic Stockpiling

Buffer Capacity Creation Through Geographic Diversification

The 1,400 metric tons annual capacity at Carester's Caremag facility creates potential buffer inventory during periods of stable demand whilst providing surge capability during supply emergencies. This strategic stockpiling capability reduces vulnerability to temporary supply disruptions from geopolitical events or facility maintenance requirements.

Less Common Metals, USA Rare Earth's British subsidiary, provides existing European operational foundation and customer relationships supporting the French expansion. Furthermore, this established presence reduces execution risk whilst enabling immediate market access for processed materials.

Dual-sourcing capabilities through both recycled and primary feedstock streams create operational redundancy. If mining operations experience temporary shutdowns, recycled magnet processing can continue providing partial capacity utilisation and customer service continuity.

Emergency Production Protocols

Government funding mechanisms often include provisions for emergency production mobilisation during national security situations. The integrated structure spanning US mining, French processing, and multiple manufacturing locations provides flexibility for prioritising critical applications during supply stress scenarios.

Strategic Advantages of Integrated Operations:

- Supply Security: Reduced dependence on Chinese processing

- Quality Control: End-to-end oversight of production standards

- Cost Optimisation: Elimination of intermediary markups

- Emergency Response: Rapid prioritisation of critical applications

The next major ASX story will hit our subscribers first

Investment Implications and Market Outlook

Risk Assessment for Rare Earth Market Participants

Rare earth investment carries inherent volatility due to concentrated production sources, complex processing requirements, and policy-driven demand fluctuations. However, the strategic importance of these materials for clean energy transition and defence applications provides fundamental demand support, particularly as the mining industry evolution continues.

Technology advancement risks in alternative magnet materials could potentially reduce rare earth demand, though current research suggests permanent magnet advantages will persist for high-performance applications. Solid-state batteries and other emerging technologies may alter demand patterns but unlikely to eliminate rare earth requirements entirely.

Regulatory changes affecting import/export policies represent both opportunities and risks for Western rare earth companies. Increased restrictions on Chinese imports could benefit domestic processors, whilst trade policy reversals might restore competitive disadvantages.

Strategic Positioning for Long-Term Value Creation

USA Rare Earth's French magnet plant concept represents logical extension of vertical integration strategy, positioning the company to serve both North American and European markets with domestically-controlled supply chains. This geographic diversification reduces regulatory risk whilst enabling market-specific product customisation.

The timeline for achieving meaningful market share depends on production ramp-up success at multiple facilities simultaneously. Consequently, coordination challenges between Texas mining, French processing, and dual magnet manufacturing locations require sophisticated project management and technical expertise.

This integrated approach aligns with broader trends in energy transition security and advances in battery recycling breakthrough technologies that complement rare earth processing capabilities.

Key Success Factors for Integrated Rare Earth Operations:

- Technical Execution: Successful facility development and production ramp-up

- Cost Competitiveness: Achieving pricing parity with Chinese suppliers

- Customer Development: Securing long-term supply contracts with major manufacturers

- Policy Continuity: Maintaining government support for strategic minerals initiatives

Global Industry Implications and Future Developments

Market participants should monitor facility development progress, customer contract announcements, and production cost revelations as key indicators of commercial viability. The success of USA Rare Earth's integrated model may influence broader industry consolidation trends and government policy approaches toward critical minerals security.

The strategic importance of establishing Western-controlled rare earth supply chains extends beyond individual company success to encompass national security and economic competitiveness. Furthermore, international cooperation between allied nations on rare earth magnet plant investments demonstrates the coordinated approach required to challenge Chinese market dominance.

Recent developments in French rare earth processing capabilities indicate growing momentum behind Western supply chain development initiatives. These investments represent more than commercial opportunities; they constitute strategic infrastructure essential for maintaining technological competitiveness in an increasingly multipolar world.

The USA Rare Earth French magnet plant exemplifies this transformation from Chinese dependency toward Western self-sufficiency in critical materials processing. Success in this endeavour will likely accelerate similar investments across allied nations, creating a foundation for sustained technological leadership in clean energy and defence applications.

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and policy frameworks. Rare earth investments involve substantial technical and market risks, including commodity price volatility, regulatory changes, and execution challenges in complex processing operations. Readers should conduct independent research and consider professional financial advice before making investment decisions.

Looking to Invest in Critical Minerals Infrastructure?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial today and secure your market-leading advantage in the evolving critical minerals landscape.