June 23, 2026

The Structural Fault Lines Beneath Corporate Governance at Major Resource Companies

Resource nationalism does not announce itself with a press release. It accumulates quietly through regulatory friction, shareholder campaigns, and boardroom resignations until the governance architecture of even the most financially powerful mining companies begins to show visible stress fractures. For investors tracking commodity exposure in Latin America, understanding how political influence penetrates corporate governance at the institutional level is just as important as understanding iron ore prices or production volumes.

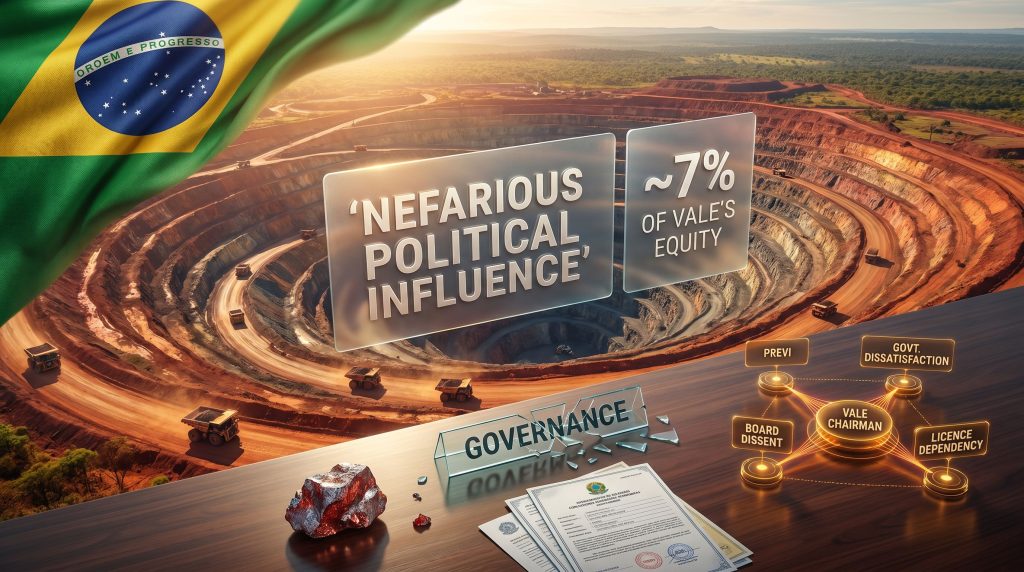

Vale, the world's largest iron ore producer and a critical supplier of nickel and copper to global markets, is currently navigating precisely this kind of slow-moving governance crisis. The dynamics at play offer a masterclass in how political cycles intersect with corporate independence at state-adjacent mining giants, and why the consequences of Vale chairman political pressure extend far beyond Brazil's borders.

When big ASX news breaks, our subscribers know first

Why Vale's Ownership Architecture Creates a Governance Fault Line

To understand the current situation, it helps to first understand the company's unusual shareholder composition. Unlike Rio Tinto or BHP, which operate primarily under institutional and retail ownership structures in Anglo-Saxon capital markets, Vale exists within a Brazilian ownership ecosystem where state-linked pension funds hold meaningful equity positions and carry implicit political expectations alongside their financial mandates.

The most consequential of these shareholders is Previ, the pension fund for employees of Banco do Brasil, which holds approximately 7% of Vale's equity. While 7% may appear modest in isolation, its significance is amplified by two factors:

- Previ's mandate is inherently linked to the Brazilian state, giving it a natural alignment with federal government priorities rather than purely commercial investment objectives.

- Vale's broader ownership is dispersed across thousands of institutional and retail shareholders, meaning concentrated blocks held by politically sensitive entities carry disproportionate governance influence.

This creates what governance analysts describe as a structural fault line: dispersed ownership combined with concentrated institutional blocs that are not fully independent of the political environment. The result is a company that is legally private but operationally and governmentally entangled in ways that create recurring vulnerability to political cycles. Furthermore, the geopolitical mining landscape in 2025 is making these dynamics increasingly visible to international investors.

Daniel Andre Stieler, the Chairmanship, and the Removal That Did Not Happen

Vale's current chairman, Daniel Andre Stieler, occupies a role that carries enormous strategic weight in the post-Brumadinho era. Following the catastrophic 2019 tailings dam collapse at Brumadinho, which killed more than 270 people and triggered one of Brazil's largest corporate liability settlements, Vale's board underwent a fundamental restructuring designed to demonstrate genuine governance independence and corporate accountability.

The chairmanship became a focal point of that rebuild. A credible, independent chair was central to restoring Vale's social licence to operate, its ESG ratings, and its relationships with international institutional investors who had grown deeply uncomfortable with the company's safety and governance record.

Previ's push to remove Stieler from the chairmanship therefore did not occur in a vacuum. The board's rejection of this proposal was significant for several reasons:

- It demonstrated that a majority of the board was willing to resist a politically connected institutional shareholder's demand.

- It set a temporary precedent for governance independence, though one that remains fragile given the structural pressures that produced the challenge in the first place.

- It drew public attention to the degree of political leverage that state-linked shareholders are willing to exercise over Vale's leadership composition.

When a pension fund with government-linked obligations moves to dislodge a sitting chairman, the motivations rarely reduce to pure financial logic. The action signals a misalignment between the board's strategic course and the political priorities of an incumbent government seeking to reshape corporate behaviour through institutional pressure rather than direct regulatory intervention.

A Cyclical Pattern: Government-Influenced Leadership at Vale

Does History Repeat Itself at Vale?

What makes the current situation particularly significant for long-term investors is that it does not represent an isolated episode. Vale has a documented history of government intervention in mining that stretches back well over a decade, with executive transitions repeatedly shaped by political considerations.

The most frequently cited precedent is the departure of former CEO Roger Agnelli in 2011, which occurred under conditions that observers widely interpreted as the product of political pressure from the Dilma Rousseff administration. The Brazilian government at the time was dissatisfied with Vale's perceived prioritisation of shareholder returns over domestic industrial development, including insufficient investment in Brazilian steel and fertiliser production.

Agnelli's exit reinforced the perception that Vale's executive suite is not fully insulated from the preferences of whoever occupies Brasília. Subsequent leadership transitions at Vale attracted similar scrutiny, establishing what amounts to an informal institutional memory among investors: that CEO succession at Vale carries a political risk dimension that does not exist to the same degree at comparable global miners.

The resignation of board member José Luciano Duarte Penido added a new dimension to this pattern. His departure, accompanied by public statements characterising the interference in Vale's CEO selection process as deeply problematic for the company's governance integrity, was notable precisely because the criticism originated from within the institution. When a sitting board member resigns and publicly describes the interference as corrosive to governance standards, the signal carries an entirely different weight with ESG-focused institutional investors and proxy advisory firms.

The Government's Strategic Grievances Against Vale

To fully grasp the intensity of Vale chairman political pressure, it is necessary to understand what the Brazilian government actually wants from Vale and why it believes the current leadership is failing to deliver it.

The core tension is a fundamental strategic disagreement between Vale's globally oriented capital allocation model and the Brazilian government's developmental agenda:

| Government Priority | Vale's Current Approach | Resulting Tension |

|---|---|---|

| Higher domestic steel production output | Global iron ore export focus | Investment allocation mismatch |

| Downstream value-add within Brazil | International base metals diversification | Industrial policy divergence |

| Increased domestic capex commitments | Shareholder return optimisation | Capital deployment conflict |

| Greater employment and infrastructure investment | Operational efficiency programmes | Social contract friction |

The Mariana tailings dam disaster in 2015, operated through the Samarco joint venture with BHP, and the far more deadly Brumadinho collapse in 2019 have further complicated this relationship. These disasters dramatically altered the political calculus around Vale's social licence. They created ongoing legal liabilities that political actors can leverage when seeking influence over Vale's governance, positioning the Brazilian government as a legitimate stakeholder in Vale's internal decision-making in ways that extend beyond standard regulatory relationships.

Vale's reported plan to create a dedicated vice president of institutional relations represents an acknowledgement that its existing stakeholder management framework is structurally insufficient for the political environment it currently operates within. In addition, considerations around natural capital in mining are increasingly shaping how regulators and governments assess corporate accountability at companies like Vale.

How Vale's Situation Compares to Global Mining Peers

A useful way to contextualise Vale's governance challenges is to examine how comparable global miners manage the tension between state expectations and commercial independence.

Rio Tinto, BHP, and Glencore all operate across politically complex jurisdictions, but their exposure to government intervention in board composition is structurally different from Vale's for several reasons:

- Concession structure: Companies operating under long-term, contractually defined production-sharing agreements have greater visibility over regulatory stability than those, like Vale, that depend on discretionary concession renewals across multiple Brazilian states.

- Shareholder base: The absence of state-linked institutional shareholders with explicit political mandates in Anglo-Saxon mining companies' registers reduces the vector through which political pressure can be applied at the board level.

- Legal framework: Brazilian corporate governance law and the specific structures governing Vale's shareholder agreements create different pressure dynamics than the frameworks governing London or Melbourne-listed miners.

For proxy advisory firms and ESG rating agencies, the documentation of repeated attempts to politically influence Vale's board composition creates measurable governance risk. This risk is ultimately reflected in Vale's cost of capital, as international institutional investors apply a governance discount to equity valuations where board independence cannot be reliably assumed. Consequently, considerations around global taxes and royalties are also being factored into how investors assess the long-term sustainability of politically exposed miners.

The next major ASX story will hit our subscribers first

Three Scenarios for Vale's Governance Trajectory

The resolution of the current standoff between Vale's board and its politically connected shareholders is unlikely to follow a clean or permanent path. Three plausible scenarios are worth mapping:

Scenario A: Partial Capitulation

Vale installs leadership aligned with government priorities. Capital allocation shifts toward domestic industrial projects. Short-term political tension eases, but Vale's global competitive positioning and international investor confidence deteriorate over the medium term.

Scenario B: Continued Board Resistance

The board maintains its current composition but faces compounding friction across environmental approvals, concession renewals, and regulatory interactions. The cost is not a single decisive confrontation but a grinding attrition of operational flexibility.

Scenario C: Negotiated Realignment

Vale's leadership proactively expands its institutional relations function, offers meaningful commitments on domestic investment levels, and creates enough political accommodation to reduce pressure without surrendering board independence. This is the scenario the new institutional relations vice president appointment appears designed to facilitate.

Commodity Market and Supply Chain Implications

Vale's governance instability carries implications that extend well beyond Brazil. As the world's dominant iron ore producer and a significant supplier of nickel for battery supply chains, any politically driven distortion of Vale's capital allocation has downstream effects on:

- Global iron ore pricing: Supply-side uncertainty at Vale introduces volatility into a market where the company's production decisions are closely tracked by steelmakers from China to Europe.

- Battery metals supply chains: Vale's growing copper and nickel portfolios are increasingly material to electric vehicle and energy storage supply chains. Political redirection of these investments toward domestic Brazilian priorities could affect project timelines that global manufacturers are depending on.

- Investor risk pricing: Governance instability at a company of Vale's scale contributes to a broader risk premium on Brazilian resource equities, affecting sector-wide capital flows into Latin American mining.

Furthermore, the mining claims framework emerging across resource jurisdictions globally underscores how governance and regulatory structures are becoming increasingly scrutinised by institutional investors assessing long-term country risk.

Frequently Asked Questions: Vale Chairman Political Pressure

What is driving political pressure on Vale's board leadership?

The pressure stems from a combination of government dissatisfaction with Vale's capital allocation decisions, the influence of state-linked pension funds within the shareholder register, and a long-established pattern of political actors seeking to shape executive and board appointments at the company.

Who attempted to remove Vale's chairman and what was the outcome?

Previ, the pension fund for Banco do Brasil employees holding approximately 7% of Vale's equity, advocated for the removal of chairman Daniel Andre Stieler. The board rejected the proposal, however the episode highlighted the degree of institutional pressure being applied to Vale's governance framework.

Why does a board member's resignation matter more than external criticism?

Board resignations citing governance interference originate from within the institution, making them impossible to dismiss as competitive or media-driven commentary. When José Luciano Duarte Penido resigned and publicly described problematic political influence in Vale's CEO selection process, it provided documented, insider-level evidence of governance pressure that carries significant weight with institutional investors and rating agencies. Indeed, former board members have spoken openly about the scale of political influence in Vale's succession processes.

How does Vale's structural dependency on government concessions amplify political risk?

Vale's operations span multiple Brazilian states, each requiring ongoing environmental licences, operational permits, and concession renewals. This multi-jurisdictional dependency creates numerous leverage points through which political dissatisfaction with Vale's strategic decisions can be translated into regulatory friction, giving the government significant informal power over a company it no longer directly owns.

What governance reforms is Vale implementing to address these pressures?

Vale is reported to be establishing a dedicated vice president role focused on institutional relations, signalling a structural recognition that its stakeholder management capabilities need strengthening. This comes as Vale chairman political pressure continues to test the boundaries of corporate independence across one of the world's most consequential resource companies. Analysts tracking the Previ governance battle note that navigating an environment defined by ongoing environmental liabilities, political scrutiny, and competing shareholder mandates will remain a defining challenge for Vale's leadership in the years ahead.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice or an investment recommendation. All forward-looking scenarios and governance assessments reflect analytical perspectives based on publicly available information and are subject to change as circumstances evolve. Readers should conduct independent due diligence before making any investment decisions.

Want to Stay Ahead of Significant ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex mineral data into actionable investment insights for both short-term traders and long-term investors — explore historic examples of exceptional discovery returns to understand the magnitude of opportunities involved. Begin your 14-day free trial at Discovery Alert today and secure your market-leading advantage.