July 17, 2026

The Resource Superpower Question: Who Really Controls the World's Critical Minerals?

The global scramble for battery metals, copper, and fertiliser minerals has redirected institutional attention toward a region that has quietly held geological supremacy for decades. Latin America sits atop an extraordinary concentration of the Earth's most commercially valuable deposits, and yet the strategic behaviour of the companies extracting these resources remains poorly understood outside specialist circles. The two organisations that matter most in this story operate under fundamentally different ownership philosophies, pursue divergent commodity strategies, and carry very different ESG legacies. Understanding how Vale and Codelco in Latin America mining are navigating this era is essential for any investor, policymaker, or analyst tracking the global energy transition.

When big ASX news breaks, our subscribers know first

Two Companies, Two Models, One Region

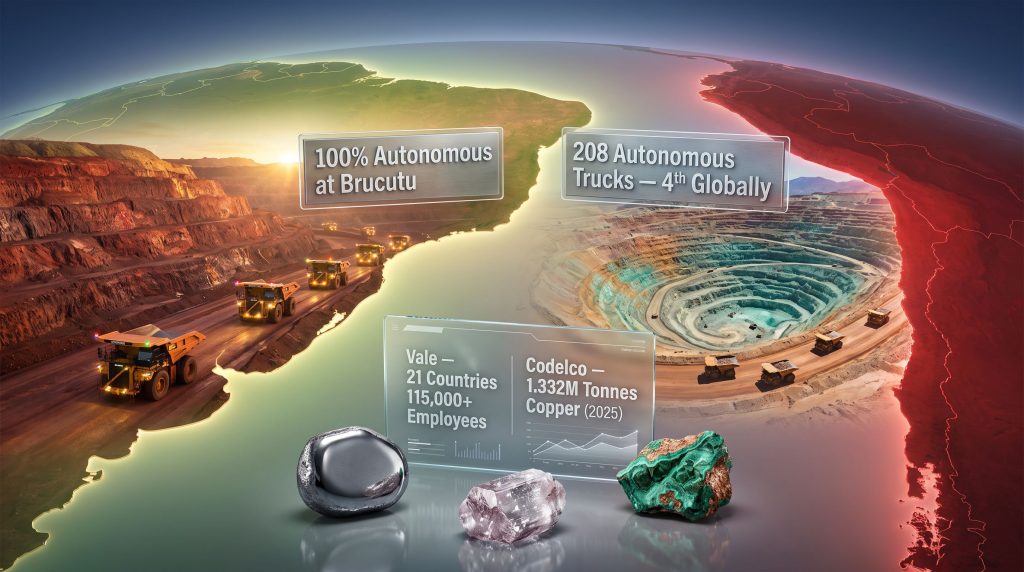

Latin America holds an estimated 65% of the world's lithium reserves, more than 40% of global copper reserves, and some of the planet's most prolific iron ore formations. This geological inheritance is not evenly distributed, nor is it evenly managed. Brazil and Chile function as the primary anchors of Latin American mining output, and Vale and Codelco are the institutional expressions of each country's relationship with its mineral wealth.

The comparison between these two organisations is analytically useful precisely because they are so structurally different. Vale operates as a privately held multinational with production and exploration activities across 21 countries, while Codelco functions as a 100% state-owned entity whose profits flow directly into Chile's national budget. One is driven by shareholder returns and international capital markets; the other operates as an extension of sovereign economic policy.

| Dimension | Vale (Brazil) | Codelco (Chile) |

|---|---|---|

| Primary Commodity | Iron ore | Copper |

| Ownership Structure | Private (formerly state-owned) | 100% Chilean state-owned |

| Geographic Footprint | 21 countries | Chile only (7 mining divisions) |

| Annual Production Benchmark | ~300M+ tonnes iron ore capacity | ~1.332M tonnes copper (2025) |

| Workforce Scale | 115,000+ employees globally | Tens of thousands across Chilean divisions |

| New Commodity Pivot | Lithium and nickel expansion | Lithium (National Lithium Strategy, 2023) |

| Autonomous Fleet Status | 50+ trucks at Carajás; 100% at Brucutu | 208 trucks across Chilean operations |

Despite operating in entirely different commodity markets, both companies are converging on the same strategic frontier: lithium and intelligent mining automation. This convergence reflects a shared response to global energy transition pressures rather than any coordinated strategy between them.

Vale's Operational Architecture: Iron Ore Dominance and Regional Diversification

The Geological Foundation: Carajás and the Iron Quadrangle

Vale's competitive position rests on a geological endowment that few mining companies anywhere in the world can match. The Carajás mine complex in Pará state, northern Brazil, hosts one of the largest and highest-grade iron ore deposits on Earth. The ore bodies at Carajás are notable not only for their scale but for the relatively high iron content of their output, which commands premium pricing in Asian steel markets where blast furnace efficiency depends heavily on feed grade quality.

The secondary production zone, the Quadrilátero Ferrífero (Iron Quadrangle) in Minas Gerais, has historically been Vale's heartland. It is also where the company's most consequential environmental failures occurred, a fact that continues to shape its governance and capital allocation decisions today.

Regional Investment Beyond Brazil's Borders

Vale's strategy is not confined to Brazilian iron ore. The company has made substantial capital commitments across Latin America that signal a deliberate diversification into adjacent mineral categories:

- Peru: $163 million committed to the Bayóvar phosphate operation, targeting the fertiliser mineral market

- Argentina: $1.393 billion allocated to the Río Colorado potash project, representing one of the largest single mining investment commitments in Argentine history

- Colombia: $102 million directed toward the El Hatillo coal operation

These investments reflect a calculated strategy to embed Vale deeper into Latin American supply chains across multiple commodity categories, reducing the revenue concentration risk that comes with heavy iron ore dependence.

The Autonomy Advantage: Intelligent Mining at Scale

Vale's deployment of 50 autonomous haul trucks at Carajás since 2020 marked a turning point in Brazilian mining technology adoption. The achievement of 100% autonomous haulage at the Brucutu mine in Minas Gerais is a global benchmark, demonstrating that large-scale autonomous operations are viable in complex Brazilian geological and topographical conditions.

What is less commonly discussed is the operational logic behind these deployments. Autonomous haulage systems eliminate shift-change downtime, reduce tyre wear through more consistent load and speed profiles, and remove the safety risks associated with human fatigue in high-tonnage environments. In iron ore operations where marginal cost efficiency determines competitive positioning against Australian producers, these gains compound meaningfully over multi-year operational horizons.

Codelco's Structural Position: The World's Largest Copper Producer Under Pressure

Seven Divisions, One National Mission

Codelco's operational structure spans seven distinct mining divisions, each with its own geological character and production profile:

- Chuquicamata (Antofagasta Region) – one of the world's largest open-pit copper mines, currently undergoing a technically complex transition to underground operations

- El Teniente (O'Higgins Region) – the world's largest underground copper mine by ore reserve volume

- Radomiro Tomic – a large-scale oxide copper operation in the Atacama Desert

- Gabriela Mistral – notable as the first mine in Latin America to deploy an autonomous truck fleet

- Salvador – a smaller but historically significant division in the Atacama

- Andina – a high-altitude operation northeast of Santiago

- Ventanas – the refinery complex undergoing a major environmental repositioning

The Ore Grade Problem: A Less-Discussed Structural Risk

One dimension of Codelco's challenge that receives insufficient attention in mainstream coverage is the secular decline in copper ore grades across Chilean deposits. As the world's largest deposits age, mineralisation becomes progressively more disseminated, meaning more rock must be processed per tonne of copper recovered. This raises energy consumption, water usage, and reagent costs per unit of output in a country where electricity and water are already scarce and expensive in northern mining regions.

This ore grade deterioration is not unique to Codelco or to Chile. It is an industry-wide phenomenon affecting global copper supply. What makes Codelco's situation distinctive is the combination of declining grades with the capital intensity of transitioning major open-pit operations to underground mining, particularly at Chuquicamata, where the underground project requires multi-billion dollar sustained investment over a decade-long development horizon.

Furthermore, the Chile copper price outlook adds another layer of complexity, as price volatility directly affects the economic viability of these capital-intensive underground transitions. Codelco copper production reached approximately 1.332 million tonnes of copper in 2025, sustaining its position among the world's top copper producers, but maintaining that output trajectory in the face of ageing ore bodies and rising operating costs is the central operational challenge of the coming decade.

The Ventanas Repositioning: Environmental Governance in Practice

The decision to cease smelting operations at the Ventanas complex near Quintero-Puchuncaví represents one of the more significant strategic environmental decisions in Chilean mining history. The region had long been associated with industrial contamination affecting nearby communities, and the operational shift toward refinery-only activities reflects both regulatory pressure and a broader commitment to repositioning the asset within an ESG-constrained operating environment.

For copper processing value chains, the distinction matters: smelting transforms copper concentrates into blister copper through high-temperature pyrometallurgical processes that generate sulphur dioxide emissions and toxic slag byproducts. Refining electrolytically purifies blister copper into cathode-grade metal. Removing the smelting step reduces Ventanas' environmental footprint significantly while retaining its role in Chile's copper export supply chain.

Latin America's Autonomous Mining Leadership

Chile's Quiet Technology Triumph

Chile's position as the 4th-ranked country globally in autonomous mining truck deployments, with approximately 208 autonomous haul trucks in operation, is one of the least-discussed success stories in Latin American industrial technology. The foundation was laid as early as 2008, when Codelco's Gabriela Mistral division became the first mine in Latin America to deploy an autonomous fleet, establishing a 15-year technology learning curve that now confers genuine competitive advantage.

| Country | Leading Operator | Autonomous Trucks Operating | Global Ranking |

|---|---|---|---|

| Chile | Codelco | 208 | 4th globally |

| Brazil | Vale | 50+ (Carajás); 100% at Brucutu | Emerging leader |

| Peru | Various operators | Limited deployments | Early stage |

The technology partnerships enabling this transformation primarily involve Caterpillar's Command for Hauling and Komatsu's FrontRunner autonomous systems, both of which have been extensively customised for the altitude, dust, and gradient conditions present at Chilean and Brazilian mine sites.

ESG Governance: From Crisis to Structural Reform

Vale's Tailings Legacy and the Accountability Architecture

The Mariana tailings dam failure in 2015 and the catastrophically larger Brumadinho collapse in 2019 are defining events in Vale's institutional history. Brumadinho alone claimed over 270 lives and released approximately 12 million cubic metres of iron ore tailings into the Paraopeba River system, causing one of the worst environmental disasters in Brazilian history.

The governance response went beyond remediation payments and dam decommissioning programmes. Vale restructured its executive compensation framework to directly link sustainability key performance indicators to variable pay, creating a financial accountability mechanism designed to align managerial incentives with long-term environmental performance rather than short-term production metrics. The company also accelerated its transition toward dry-stack tailings management, which eliminates the water-saturated impoundment structures that are prone to liquefaction failure.

ESG performance has ceased to be a reputational consideration alone. For major mining companies operating in regulatory environments shaped by Brumadinho-scale events, it has become a capital allocation and operational continuity issue that directly affects debt access, insurance costs, and social licence to operate.

Codelco's Water Scarcity Challenge

Codelco's northern operations occupy some of the most water-stressed environments on Earth. The Atacama Desert, which hosts Chuquicamata, Radomiro Tomic, Gabriela Mistral, and Salvador, receives less than 15 millimetres of rainfall annually in many locations. Groundwater extraction from this hyperarid basin raises complex questions about long-term aquifer sustainability and the rights of indigenous communities, particularly Atacameño peoples, whose traditional territories overlap with major copper production zones.

The regulatory and social scrutiny around water usage is intensifying as Chilean environmental frameworks evolve. Mining companies operating in these regions are increasingly required to demonstrate closed-loop water recycling systems and to participate in multi-stakeholder water governance arrangements that give indigenous communities a meaningful voice in allocation decisions.

The next major ASX story will hit our subscribers first

The Lithium Pivot: Battery Metals and Strategic Repositioning

Vale's Nickel Foundation and Lithium Ambitions

Vale's existing nickel assets in Brazil and Canada provide a strategically valuable foundation for energy transition positioning. Nickel's role in nickel-manganese-cobalt (NMC) battery chemistries used in high-energy-density electric vehicle applications makes it a critical input in the same supply chains that are reshaping copper demand. Vale's early-stage lithium exploration activities in Minas Gerais, part of Brazil's emerging lithium triangle centred on the Jequitinhonha Valley, represent an attempt to capture a third battery metal position alongside nickel.

What is underappreciated by many observers is that Brazil's lithium geology is predominantly hard rock spodumene rather than the brine-hosted deposits that dominate Chilean and Argentine production. Spodumene processing requires different conversion chemistry and generates lithium hydroxide more readily than lithium carbonate, which may align more closely with the cathode chemistry preferences of next-generation battery manufacturers. Consequently, shifts in the global lithium market could significantly influence which deposit types attract the most investor capital in the years ahead.

Codelco and Chile's National Lithium Strategy

Chile's 2023 National Lithium Strategy extended Codelco's mandate beyond copper for the first time in its institutional history, designating the state miner as a vehicle for developing lithium as a nationally managed strategic resource. The Chile lithium strategy positions the Atacama lithium brine deposits within Codelco's development scope among the world's highest-grade lithium resources, characterised by lithium concentrations and favourable magnesium-to-lithium ratios that reduce processing complexity and cost relative to lower-quality brine operations elsewhere in the Lithium Triangle.

Codelco's entry into lithium reshapes competitive dynamics in a market currently dominated by SQM and Albemarle, the two incumbents holding operating rights in the Atacama under long-term contracts with Chile's development agency CORFO. How the transition of development rights and operational responsibilities proceeds will be one of the more consequential regulatory processes in Latin American mining over the next five years. In addition, the broader Codelco copper strategy provides important context for understanding how the organisation is balancing its traditional copper mandate with these expanding lithium ambitions.

Structural Risks and the Decade Ahead

Political Exposure and Resource Nationalism

Codelco's 100% state ownership makes its capital allocation, workforce decisions, and strategic priorities directly susceptible to Chilean political cycles. Changes in government can alter the balance between dividend extraction (which funds public spending) and reinvestment in production capacity. This tension between short-term fiscal needs and long-term operational sustainability is a structural feature of state-owned mining companies globally, and Chile is not immune.

Vale faces a different but equally significant political risk profile. Brazilian environmental licensing reform, indigenous land rights litigation, and shifting federal attitudes toward the Amazon region all create regulatory uncertainty for a company whose primary production assets are concentrated in Pará and Minas Gerais states.

Key Forward Indicators for Investors and Analysts

- Codelco's copper production trajectory through 2030 as Chuquicamata underground ramps up and older divisions reach ore body maturity

- Vale's Río Colorado potash project timeline and Argentine political stability as preconditions for capital deployment

- Autonomous fleet expansion rates at both companies as a proxy for operational modernisation velocity

- ESG rating trajectories and tailings safety compliance as indicators of capital market access quality

- Codelco's lithium project milestones and the pace of regulatory transition away from SQM and Albemarle incumbency

The trajectory of Vale and Codelco in Latin America mining over the coming decade will be shaped less by geology, which remains extraordinarily favourable, and more by the quality of institutional decisions made under conditions of commodity price uncertainty, technological disruption, and evolving social licence requirements. Both companies possess the resource endowments to be transformational players in a decarbonising global economy. Whether their governance structures, capital discipline, and environmental performance allow them to capture that potential remains the central question for anyone tracking Latin American resource markets.

Readers seeking additional context on Latin American mining industry developments, company profiles, and project pipelines may find value in exploring BNamericas' regional mining coverage, which tracks infrastructure, energy, and extractive industry activity across the region.

Want to Track the Next Major Mineral Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly converting complex mineral data across more than 30 commodities into clear, actionable insights for both short-term traders and long-term investors — explore the historic returns major discoveries have generated and begin your 14-day free trial to position yourself ahead of the market.