August 6, 2026

Why Grid-Scale Storage Is Forcing a Rethink of Battery Chemistry

The global energy storage industry is undergoing a quiet but consequential reorientation. For years, lithium-ion dominated the conversation around grid-scale batteries, driven by falling costs and the momentum of electric vehicle manufacturing. Yet as power grids absorb ever-larger shares of intermittent renewable generation, a fundamental limitation is becoming harder to ignore: most lithium-ion systems are engineered for short bursts of discharge, typically two to four hours, which is increasingly insufficient for the multi-hour balancing requirements of modern electricity networks.

This tension between what grids need and what dominant battery chemistry delivers has opened a meaningful commercial window for vanadium redox flow batteries. Furthermore, the critical minerals energy transition playing out globally has created policy tailwinds that are accelerating investment. And within that window, the Richmond Vanadium Technology and RKP Global vanadium flow battery agreement represents one of the more structurally complete attempts to build a domestic mine-to-battery industry from the ground up in Australia.

When big ASX news breaks, our subscribers know first

The Richmond-Julia Creek Project: Queensland's Upstream Anchor

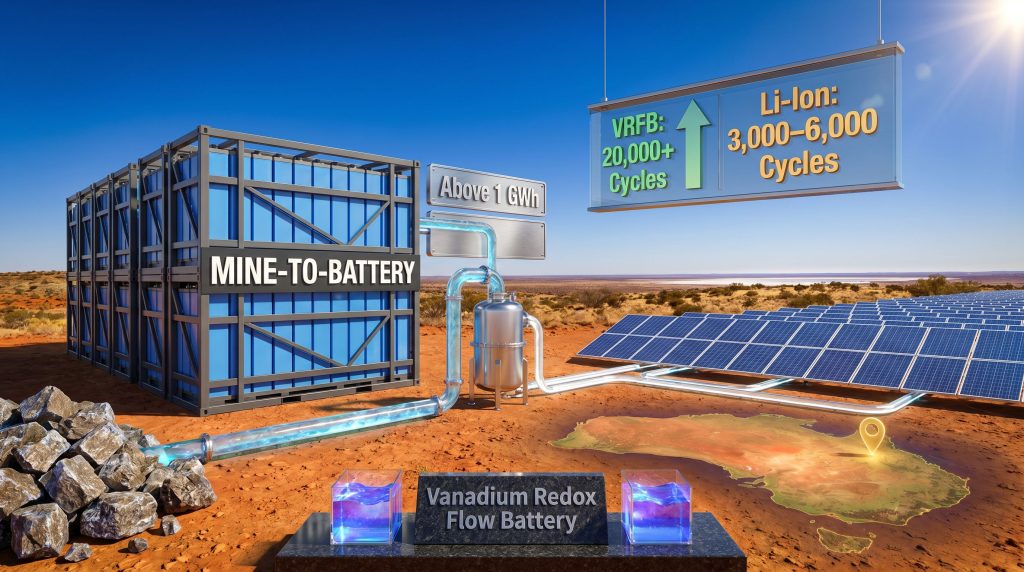

Richmond Vanadium Technology, listed on the ASX, is developing the Richmond-Julia Creek vanadium project in Queensland, which serves as the upstream foundation for the broader value chain the company is attempting to construct. The project's vanadium concentrate output is not simply a commodity to be exported. Under the strategic framework established through this agreement, it becomes the raw material input for a domestic electrolyte processing pathway, feeding directly into locally manufactured vanadium flow battery systems.

Queensland's geographic and industrial profile makes it a logical home for this kind of vertically integrated model. The state has significant renewable energy solutions ambitions, a tradition of large-scale resource processing, and a regional industrial corridor capable of hosting manufacturing operations at scale.

RVT Energy: Separating Risks to Unlock Capital

A detail that investors and project finance professionals will note is the use of RVT Energy, a wholly-owned subsidiary of Richmond Vanadium Technology, as the designated Australian project development and coordination platform under the agreement. This structure is not incidental. By housing downstream energy storage project development within a separate legal entity, RVT effectively ring-fences the electrochemical storage business from the mining operation, allowing each to attract project-specific financing, equity structures, and partnerships without cross-contaminating their respective risk profiles.

This kind of structural separation is standard practice in large-scale infrastructure development but remains relatively uncommon in the junior mining sector, where vertically integrated ambitions are often announced without the corporate architecture to support them. Its presence here suggests a level of commercial sophistication that goes beyond a simple strategic announcement.

Who Is RKP Global and What Does the Partnership Actually Contribute?

RKP Global is a Hong Kong-headquartered company with an operational profile spanning vanadium electrolyte production, battery system manufacturing, and the deployment of utility-scale long-duration energy storage projects across international markets. Its integrated capabilities across the entire VRFB technology stack, from electrolyte chemistry through to commissioned storage assets, are precisely what RVT's upstream resource position lacks on its own. You can review RKP's collaboration details to better understand the scope of the three-party arrangement.

The addition of Trina Solar's Australian operations as a third participant in the collaboration introduces a renewable energy systems dimension. This creates a three-party structure capable of delivering a combined generation-plus-storage solution to Australian grid operators, renewable energy project developers, and industrial offtakers. In practical procurement terms, this bundled capability is increasingly what large-scale energy buyers require, as they seek single-counterparty accountability for integrated renewable firming assets rather than assembling separate technology and resource supply contracts.

How Vanadium Redox Flow Batteries Actually Work

Understanding why this agreement has technical merit requires a working knowledge of VRFB electrochemistry, which differs fundamentally from lithium-ion in ways that matter enormously at grid scale.

A vanadium redox flow battery stores energy in liquid electrolyte solutions held in external tanks rather than within solid electrode materials. During charging and discharging, vanadium ions in four distinct oxidation states circulate through an electrochemical cell stack separated by a proton-exchange membrane. On the negative side, vanadium cycles between its V²⁺ and V³⁺ states. On the positive side, it transitions between VO²⁺ and VO₂⁺ forms.

What makes vanadium uniquely suited to this application is that it is the only element capable of existing in four stable oxidation states in aqueous solution, allowing it to serve as both the anolyte and catholyte in the same system. This eliminates the cross-contamination degradation that afflicts other flow battery chemistries over time, where ionic mixing between the two sides of the cell permanently reduces capacity.

The architectural consequence of this electrochemistry is the decoupled power-energy design: the cell stack determines how fast energy can be delivered (measured in kilowatts or megawatts), while the volume of electrolyte stored in the tanks determines how long it can be delivered (measured in kilowatt-hours or megawatt-hours). These two parameters can be scaled independently, which is the defining commercial advantage over lithium-ion at longer discharge durations.

VRFB vs. Lithium-Ion: A Performance Comparison for Grid Applications

| Performance Dimension | Vanadium Redox Flow Battery | Lithium-Ion (LFP) |

|---|---|---|

| Discharge Duration | 4 to 12+ hours (independently scalable) | Typically 2 to 4 hours |

| Cycle Life | 20,000+ cycles | 3,000 to 6,000 cycles |

| Capacity Degradation | Near-zero (electrolyte retains chemistry) | Progressive degradation over time |

| Thermal and Fire Risk | Very low (aqueous, non-flammable electrolyte) | Higher risk of thermal runaway |

| Scalability Model | Power and energy scaled independently | Fixed energy-to-power ratio |

| End-of-Life | Electrolyte fully recoverable and reusable | Complex and costly recycling |

| Optimal Use Case | Long-duration grid firming and industrial load shifting | Short-duration, high energy-density applications |

Key Concept: The vanadium electrolyte in a VRFB functions as a liquid asset in the most literal sense. Unlike lithium-ion cells, which degrade chemically and lose value over time, vanadium electrolyte retains its vanadium content indefinitely. It can be reprocessed, repurified, and redeployed across successive generations of battery hardware, meaning the electrolyte itself carries a residual asset value that can be refinanced or securitised.

The Concentrate-to-Electrolyte Pathway: A Critical Cost Lever

One of the most commercially significant elements of the Richmond Vanadium Technology and RKP Global vanadium flow battery agreement is the planned evaluation of a vanadium concentrate-to-electrolyte processing pathway. This is not yet confirmed as commercially operational at the scales required, and its viability will depend on processing economics that need to be demonstrated at an Australian industrial scale.

If successfully developed, domestic electrolyte production would fundamentally alter the cost structure of Australian VRFB projects. Currently, the battery raw materials market shows that vanadium electrolyte is predominantly produced in China and imported to markets where VRFB projects are being developed. This import dependency introduces currency risk, supply chain fragility, and logistics costs that erode project economics. An Australian project able to source electrolyte from a domestically processed supply linked to the Richmond-Julia Creek resource would hold a structural cost advantage over any competitor relying on offshore supply.

This is the economic rationale behind vertical integration in the vanadium energy storage sector: margin capture at multiple points in the value chain, combined with supply chain sovereignty that reduces exposure to geopolitical and logistical disruptions.

The Queensland VRFB Manufacturing Facility: Scale and Strategic Significance

The agreement contemplates the development of a local VRFB manufacturing and assembly facility in Queensland with a potential capacity exceeding 1 GWh. To contextualise that figure, a single 100 MW / 400 MWh VRFB installation would be considered a large-scale grid storage asset by current Australian market standards. A facility capable of producing more than 1 GWh of battery systems annually would represent a step-change in domestic battery manufacturing capability, creating industrial infrastructure that does not currently exist in Australia at this chemistry and scale.

The industrial policy implications extend beyond the energy sector. Queensland has been positioning itself as a destination for critical minerals processing and clean energy manufacturing, and a large-scale VRFB assembly facility would represent exactly the kind of downstream industrial activity that transforms a resource-rich state into a value-added manufacturing economy. You can explore RVT's latest investor presentation for further detail on the facility's planned scope and timeline.

The next major ASX story will hit our subscribers first

Australia's LDES Market: The Commercial Environment This Agreement Is Entering

Australia's National Energy Market is undergoing a structural transition driven by the accelerating retirement of coal-fired generation, which has historically provided not just energy but also the inertia and dispatchable capacity that grids rely on for stability. Replacing that dispatchable capacity with intermittent wind and solar requires a corresponding build-out of storage assets capable of operating across multiple hours. Consequently, the critical minerals demand surge underpinning this transition is reshaping procurement strategies across the sector.

The federal government's Capacity Investment Scheme is one of several policy mechanisms designed to accelerate storage deployment, creating a procurement pathway for long-duration assets. VRFBs compete in this landscape against pumped hydro, compressed air energy storage, and emerging chemistries such as iron-air batteries.

Where VRFBs hold a defensible structural advantage is in applications requiring:

- Co-located renewable firming at solar and wind farms where long discharge duration is commercially essential

- Remote grid stabilisation in areas where transmission augmentation is prohibitively expensive

- Industrial load shifting for mining and processing operations with predictable but variable energy demand profiles

- Locations where fire safety requirements make flammable battery chemistries commercially or regulatorily problematic

International deployment precedents in China, Europe, and North America indicate that VRFB technology is commercially ready at grid scale. China in particular has commissioned multiple projects in the hundreds of megawatt-hour range, providing operational data that significantly de-risks the technology proposition for Australian developers and financiers.

Investment Considerations and Risk Factors

The binding nature of this agreement, as distinct from a non-binding memorandum of understanding, signals a higher level of commercial commitment. However, investors should evaluate the opportunity against a realistic set of execution risks:

- Technology scaling risk: Moving from agreement to gigawatt-hour-scale manufacturing in Australia involves capital formation, supply chain development, and regulatory approvals that will take multiple years to navigate.

- Electrolyte processing validation: The concentrate-to-electrolyte pathway remains under evaluation. Its commercial viability at Australian industrial scale has not yet been demonstrated.

- Offtake market development: Australia's LDES procurement market, while growing, requires grid operator engagement and competitive tender processes before large volumes of storage capacity can be contracted.

- Three-party coordination complexity: Aligning RVT, RKP Global, and Trina Solar's Australian business across different corporate cultures, jurisdictions, and commercial priorities introduces coordination risk that single-party projects do not face.

This article is informational in nature and does not constitute financial advice. Readers considering investment decisions should conduct independent due diligence and consult a licensed financial adviser.

Key Takeaways for the Vanadium and Energy Storage Sectors

The Richmond Vanadium Technology and RKP Global vanadium flow battery agreement is significant not because it completes a mine-to-battery value chain, but because it credibly assembles the components needed to build one. The combination of a Queensland vanadium resource, an experienced VRFB technology and electrolyte partner, and a solar integration capability creates a more complete development framework than most comparable announcements in the Australian market have achieved. In addition, the battery metals investment landscape suggests that institutional appetite for vertically integrated storage plays is strengthening as grid transition timelines compress.

Several structural themes emerge from this agreement that are worth tracking:

- Vertical integration from resource extraction through to battery deployment is becoming the dominant commercial model for vanadium energy storage companies seeking durable competitive advantage.

- Domestic electrolyte production is the critical cost lever that will determine whether Australian VRFB projects can compete on economics, not just on policy support.

- The decoupled power-energy architecture of VRFBs makes them increasingly cost-competitive with lithium-ion at discharge durations above four to six hours, which is precisely the duration gap that Australia's grid transition most urgently needs to fill.

- Execution over a multi-year horizon, across capital formation, processing technology validation, and offtake market development, will determine whether this agreement produces operational infrastructure or remains a strategic framework on paper.

The vanadium sector's long-duration storage opportunity is real and growing. Whether this particular collaboration converts that opportunity into commissioned gigawatt-hours will depend on the discipline, capital, and technical execution that follows from today's binding commitment.

Want to Capitalise on the Next Major ASX Resource Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including battery and critical minerals plays driving the energy transition — instantly translating complex data into actionable investment insights for traders and long-term investors alike. Explore Discovery Alert's discoveries page to see how historic ASX mineral discoveries have generated substantial returns, and begin your 14-day free trial today to position yourself ahead of the market.